REK - REIT Earnings Halftime Report

Summary

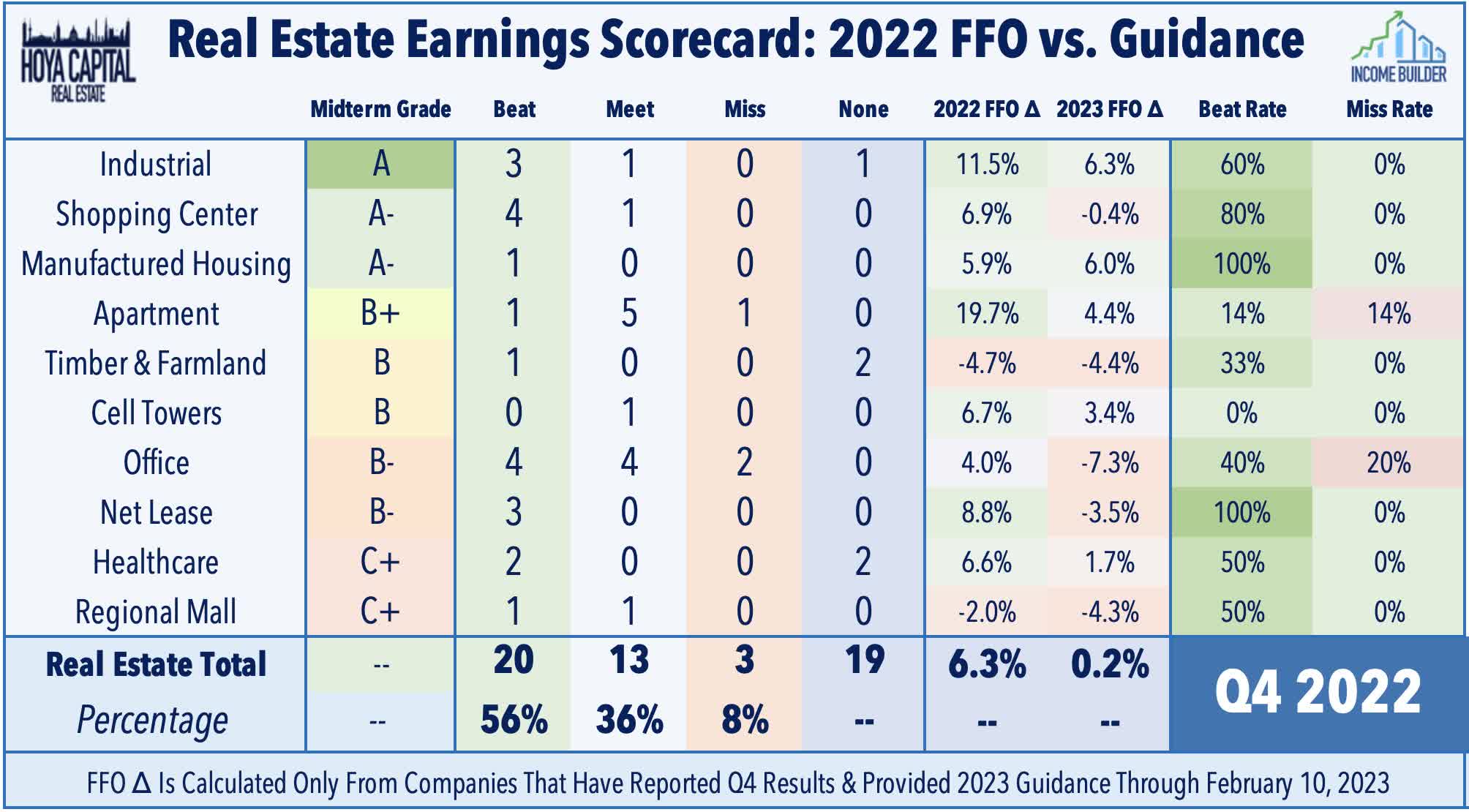

- We're approaching the halfway point of another consequential real estate earnings season with roughly 40 equity REITs and 15 mortgage REITs representing 50% of the total market capitalization reporting results.

- Results thus far have modestly exceeded expectations. Of the 36 REITs that provide guidance, 20 (56%) reported 2022 Funds From Operations ("FFO") above their prior guidance while 3 (8%) missed.

- Industrial, Manufactured Housing, and Apartment REITs all forecast mid-single-digit FFO growth in 2023. Retail REIT FFO is expected to be flat in 2023 while Office REITs forecast mid-single-digit FFO declines.

- For Residential REITs, while rent growth has indeed moderated, renewal spreads remained quite impressive in Q4 and into January, which should keep blended rent growth positive through 2023. Strength in Northeast and Southeast markets has offset weakness out West. Similar fundamental themes also apply to Industrial REITs.

- Results from the Strip Center REITs have been quite impressive with all five REITs reporting a sequential acceleration in rent growth and improvement in occupancy rates while expressing confidence in re-leasing space vacated by Party City and Bed Bath Beyond.

REIT Earnings Halftime Report

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on February 9th.

{kind=link}

We're approaching the halfway point of another consequential real estate earnings season with roughly 40 equity REITs and 15 mortgage REITs representing 50% of the total market capitalization having reported results thus far. REIT earnings results to this point have modestly exceeded expectations. Of the 36 REITs that provide guidance, 20 (56%) reported 2022 Funds From Operations ("FFO") above their prior guidance while 3 (8%) missed. While conservative forward guidance was expected given the heightened economic and interest rate uncertainty, the 2023 outlook has been mixed. While Industrial and Residential REITs have been upside standouts - forecasting mid-single-digit FFO growth in 2023 - strip center, net lease, and healthcare REIT FFO is expected to be roughly flat in 2023 while office and mall REITs forecast mid-single-digit FFO declines for the year.

{kind=link}

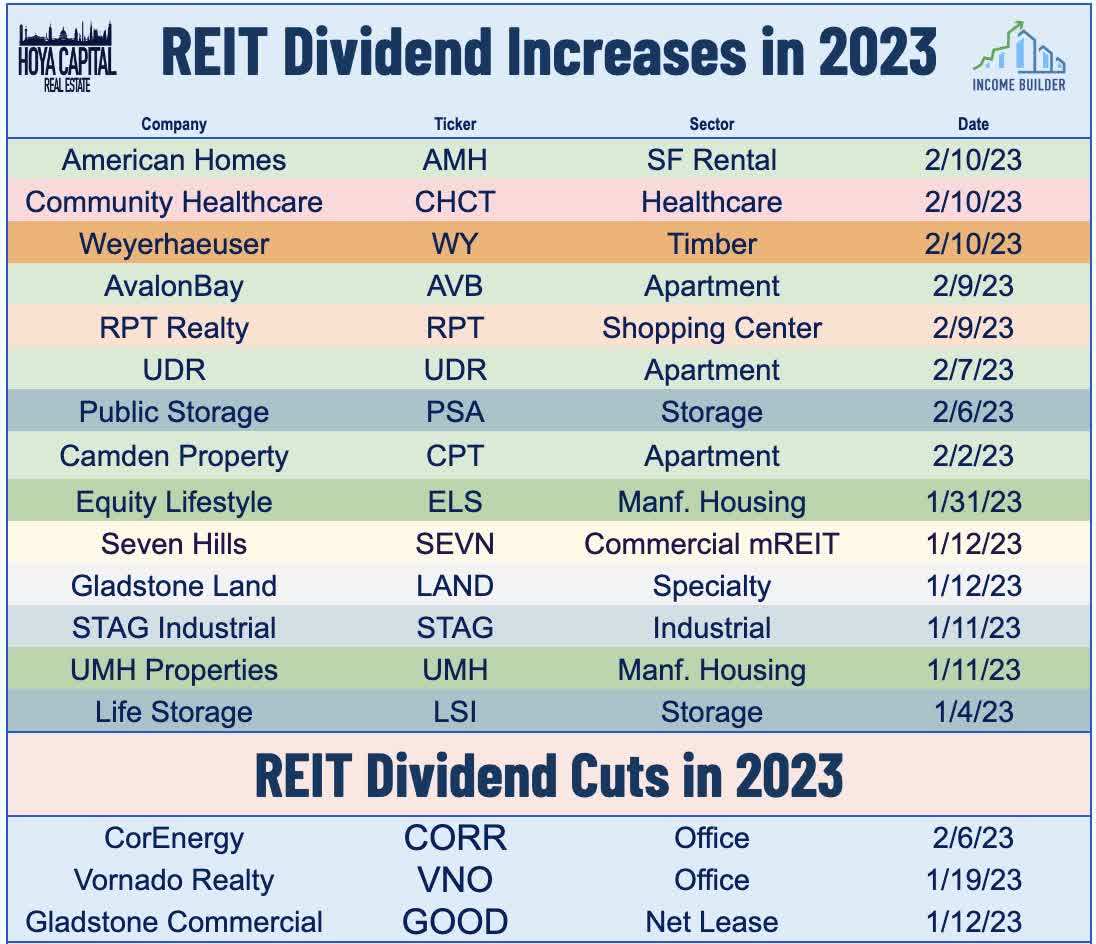

As discussed in our Earnings Preview , the major higher-level themes that we're focused on this earnings season include 1) Cap Rates & Private Market Valuations; 2) Balance Sheets & Rate Expectations; and 3) Full-Year 2023 FFO Guidance. Apart from these themes, we've also been focused on dividend commentary - particularly in sectors at the upper-end of the payout ratio spectrum. We've so far seen encouraging dividend news with another half-dozen REITs hiking their payouts over the past two weeks, bringing the full-year total across the REIT sector to 14 - offset by three dividend reductions and commentary from several REITs warning of potential future reductions. Below, we discuss our halftime analysis and grades for each property sector.

{kind=link}

Residential Real Estate Halftime Report

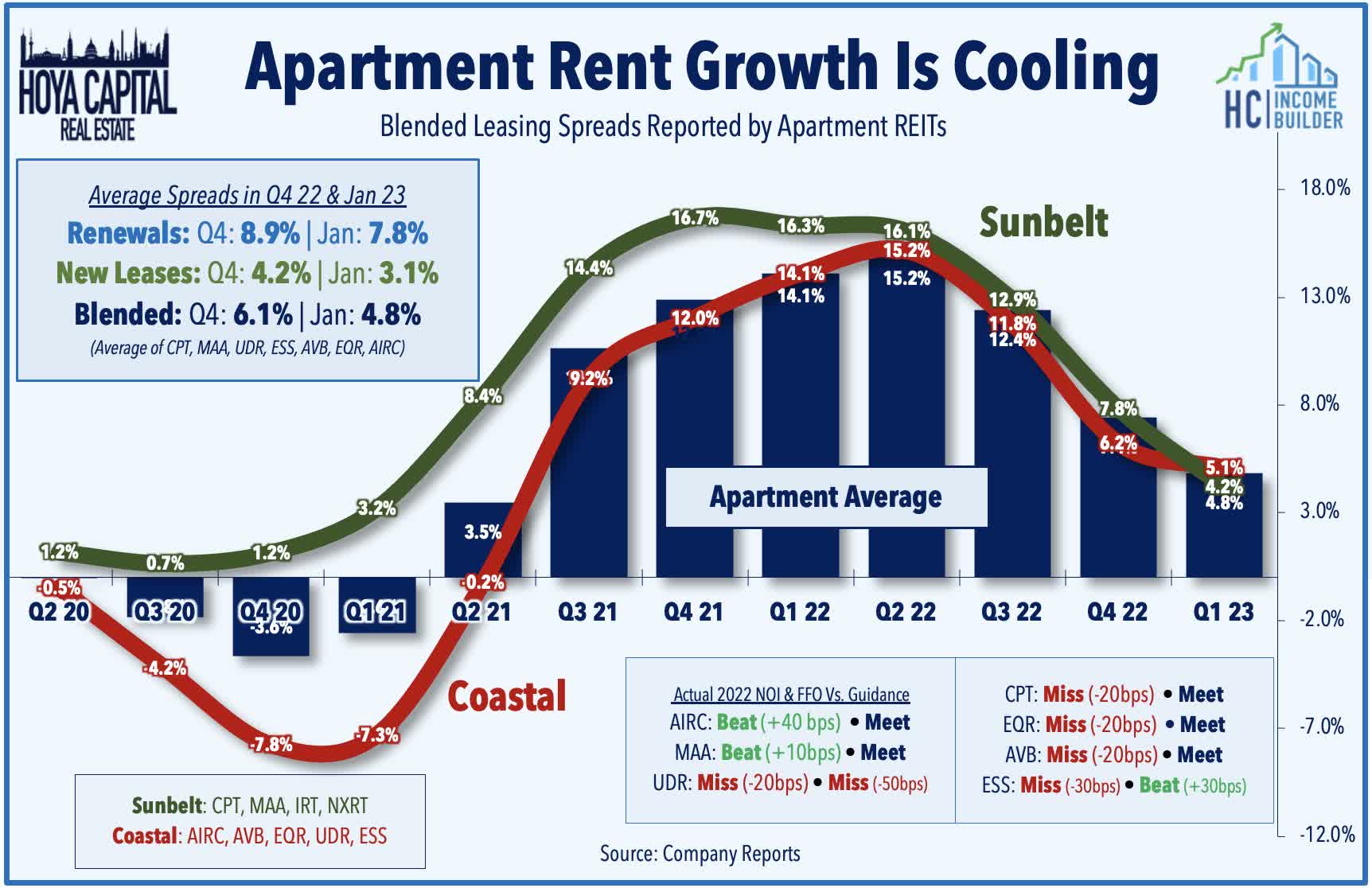

Apartment : (Halftime Grade: B+) While earnings season hasn't yet begun for many property sectors, apartment REIT earnings season is nearly complete with all seven of the largest apartment REITs reporting results. As expected, rent growth has indeed moderated from the historic pace, but renewal spreads remained quite impressive in Q4 and into January, which should keep blended rent growth firmly positive through 2023. Apartment Income ( AIRC ) has reported the most impressive rent growth trends, reporting roughly 11% blended spreads in both Q4 and January - far exceeding the sector average of 6.1% and 4.8% for those periods. Across most reports - most notably from AvalonBay ( AVB ) - we've observed notable recent strength in Northeast markets and continued outperformance from Sunbelt markets to help offset weakness out West. Essex ( ESS ) notably highlighted an uptick in unpaid rents in Q4 which it attributes to the ongoing eviction moratorium in California.

{kind=link}

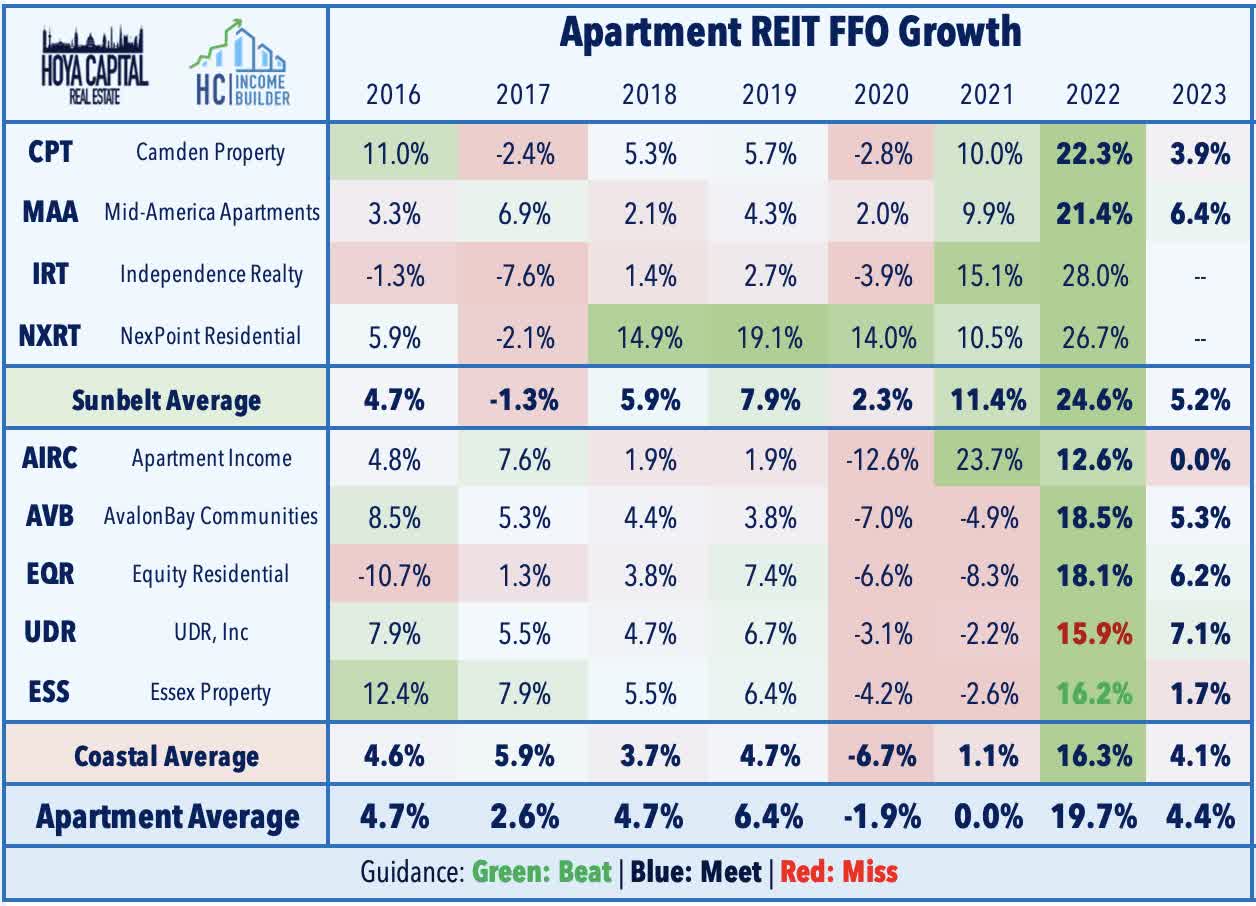

Five of the seven apartment REITs reported full-year 2022 FFO that matched their prior outlook while one - Essex ( ESS ) topped its guidance and one - UDR ( UDR ) - missed its forecast. UDR, however, is currently the leader in the clubhouse on the guidance front, projecting sector-leading FFO growth of 7.1% for 2023, above the average forecast of 4.1%. A trio of REITs have raised their dividends this earnings season - Camden ( CPT ) raised its quarterly dividend by 6.4%, UDR hiked its quarterly dividend by 10.5%, and AvalonBay ( AVB ) raised its quarterly dividend by 4% - its first dividend increase since 2019. If apartment REITs deliver on their 2023 guidance projections, Sunbelt-focused apartment REITs will have delivered cumulative FFO growth of over 40% between 2019 and 2023 - far above the 14% growth from Coastal REITs.

{kind=link}

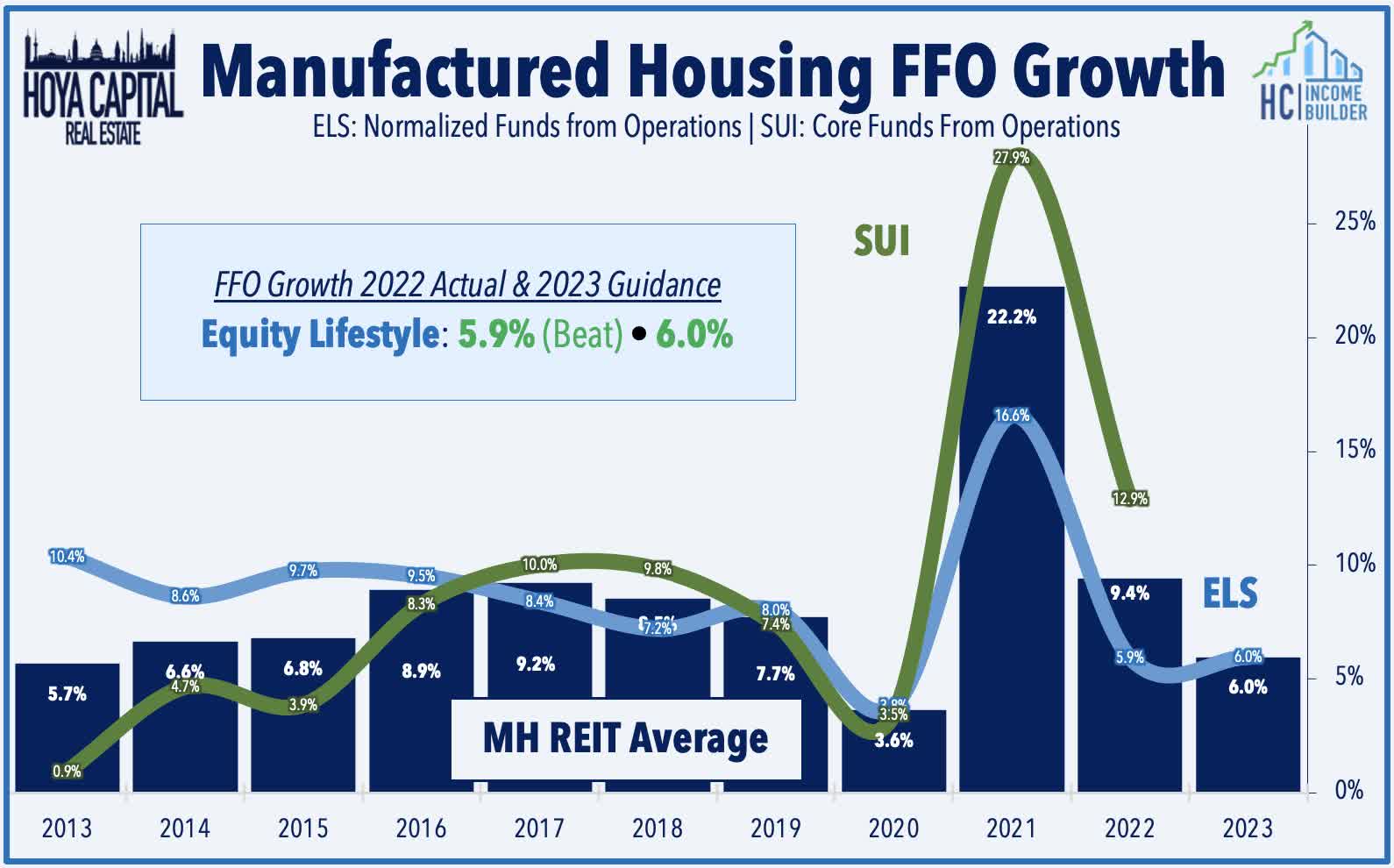

Manufactured Housing : (Halftime Grade: A-) Sticking in the residential sector, results from Equity LifeStyle ( ELS ) at the start of earnings season were a positive read-through for Sun Communities ( SUI ) and UMH Properties ( UMH ). ELS provided full-year guidance calling for FFO growth of 6.0% - an acceleration from the 5.9% growth it achieved in 2022 - while boosting its dividend by 9.1% to $0.15/share. Notably, ELS upwardly revised its guidance for MH revenue growth which is now expected to rise 6.5% this year, up from the prior outlook of 6.4%. ELS' balance sheet remains one of the strongest in the industry with an average of 11 years to maturity on its debt and no meaningful amount of debt rolling over until 2026. Guidance was slightly above consensus with solid expectations coming from all three lines of business - manufactured housing, recreational vehicles, and marinas.

{kind=link}

Industrial & Technology REIT Halftime Report

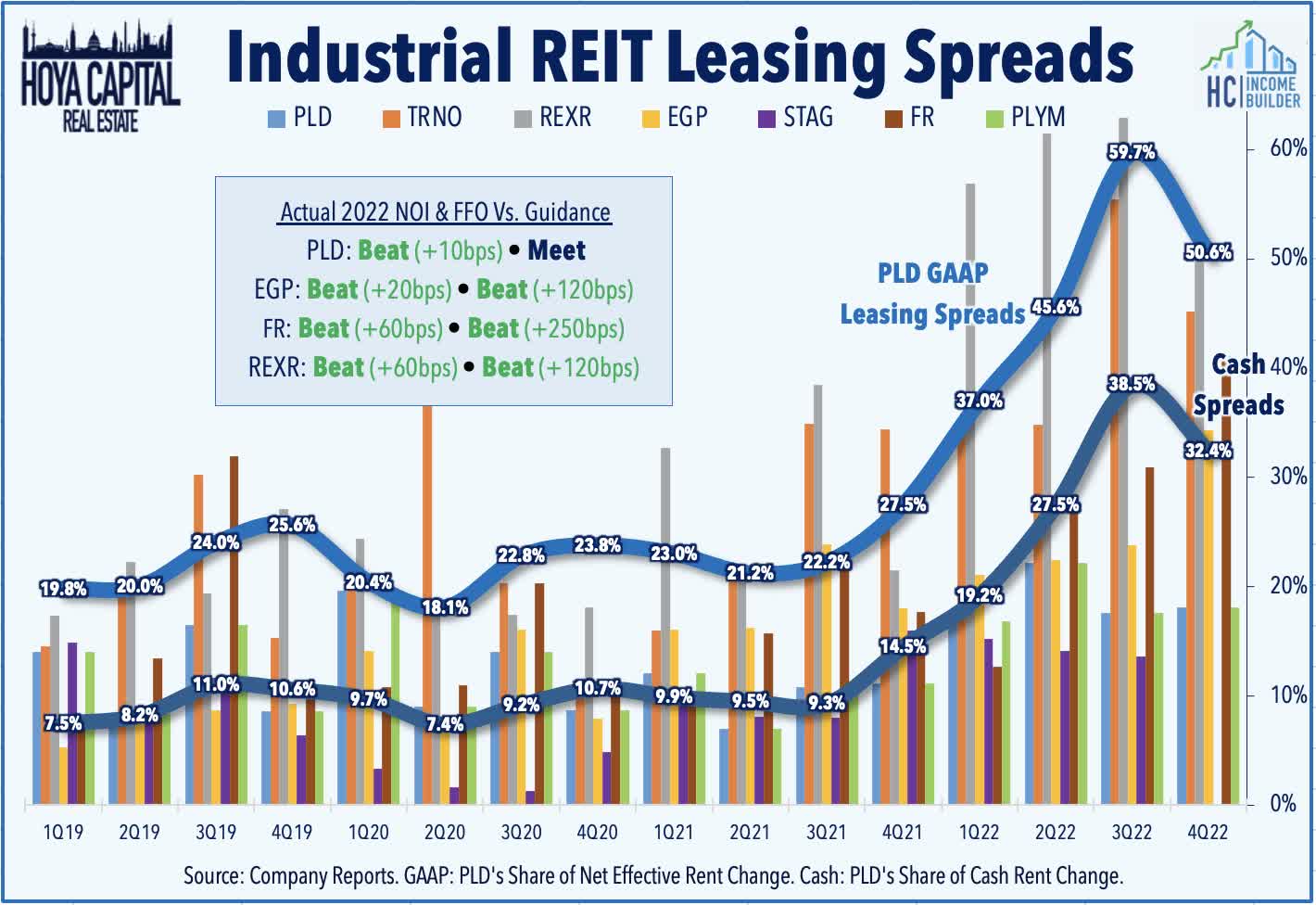

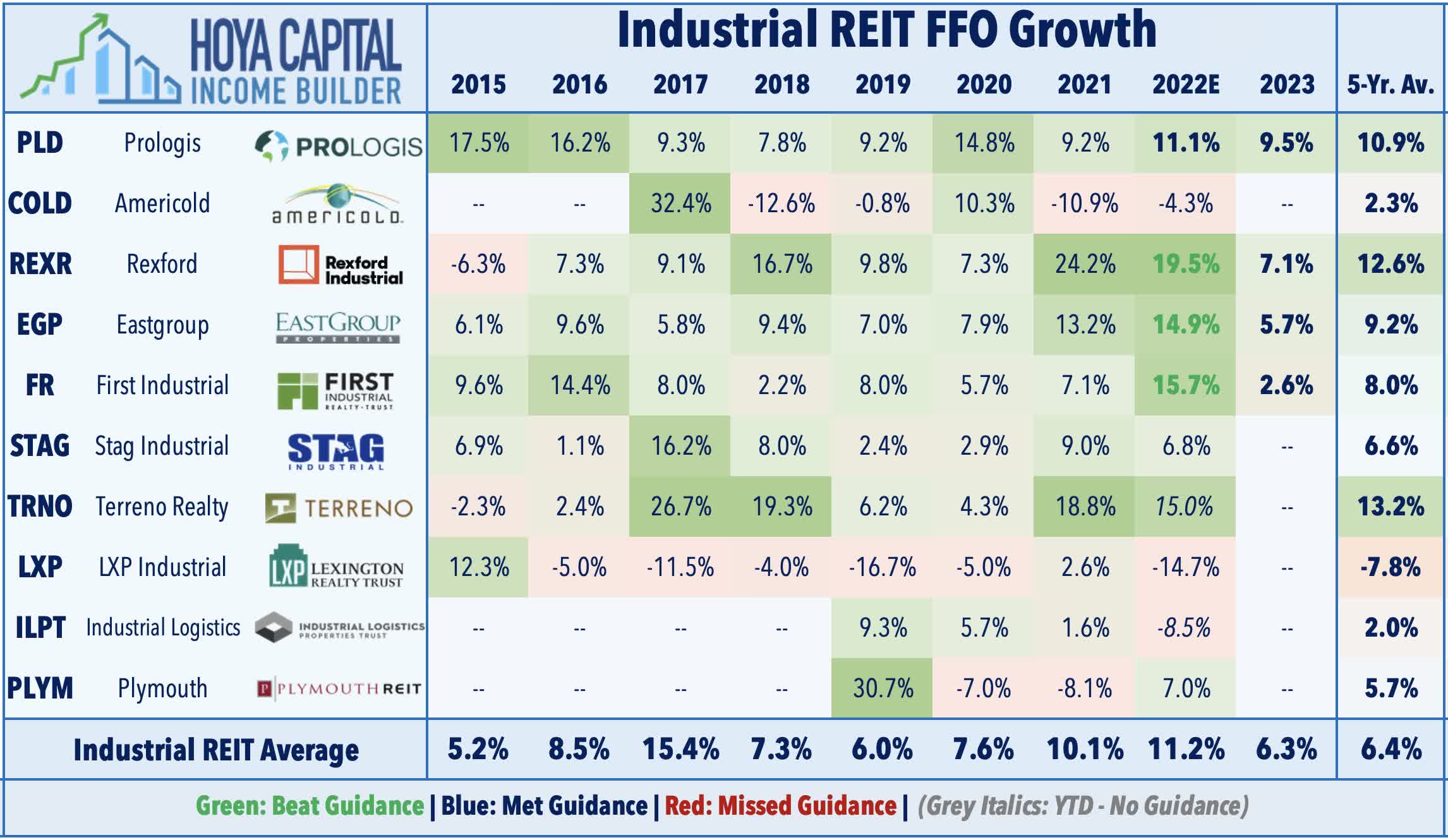

Industrial : (Halftime Grade: A) We've seen results from the five largest industrial REITs - a very strong slate of reports which have shown few noticeable signs of a slowdown in logistics demand. Similar themes of strong-but-normalizing fundamentals that we observe in residential REITs are seen here as well with rent growth on new and renewed leases rising 37% from last year, on average, cooling slightly from the 40% rate in Q3 - but still showing that demand continues to substantially outpace available supply while occupancy rates also remained near record highs in Q4. Results from First Industrial ( FR ) have been the most impressive of the group, reporting that its full-year FFO rose 18.5% in 2022 - 250 basis points above its prior guidance - driven by stellar rent spreads of 41.1% in Q4 - a notable acceleration over Q3.

{kind=link}

Results from EastGroup ( EGP ) were also impressive with FFO growth of 14.9% in 2022 - 110 basis points above its prior guidance - and provided initial 2023 guidance calling for FFO growth of 5.7%. EGP also reported a sequential acceleration in leasing spreads, which rose by 34.3% in Q4. Similar to results from Prologis ( PLD ) early in earnings season and Terreno ( TRNO ) this past week, Rexford ( REXR ) reported decent results but noted a sequential deceleration in rent growth following a pair of record quarters. Among the four industrial REITs that provided 2023 guidance, the initial outlook calls for 6.3% FFO growth this year - the highest in the REIT sector - while same-store NOI growth is expected to rise 8.2% for the year, which would actually represent a slight acceleration from 2022.

{kind=link}

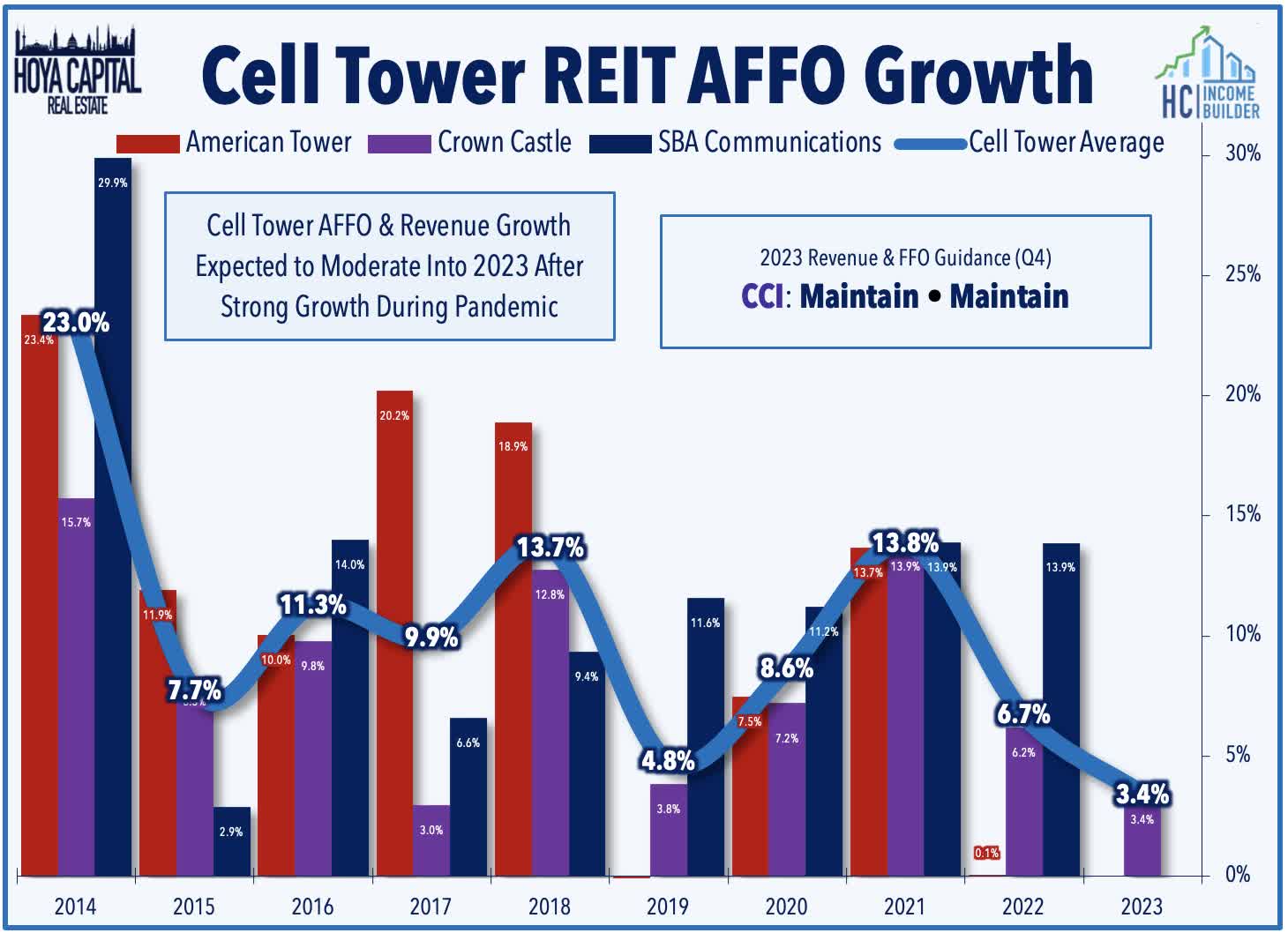

Cell Tower : (Halftime Grade: B) We've seen results from just one of the three cell tower REITs and we're still waiting on the first data center REIT report as well. Crown Castle ( CCI ) reported in-line results, recording full-year revenue growth of 10% and FFO growth of 6.2% in 2022 - each slightly above the midpoint of its guidance - while maintaining its outlook for full-year 2023 which calls for revenue growth of 3.0% and FFO growth of 3.4%. Near-term headwinds from higher interest rates and the effects of the Sprint churn are expected to offset projected organic revenue growth of 6.8% (4.2% excluding Sprint). We appreciated that CCI began providing enhanced segment-level data with this report, which showed that this 4.2% organic growth consists of 5% growth in towers, 8% growth in small cells, and flat revenue in fiber solutions. We'll hear results from American Tower ( AMT ) and SBA Communications ( SBAC ) towards the end of February.

{kind=link}

Office & Healthcare Halftime Report

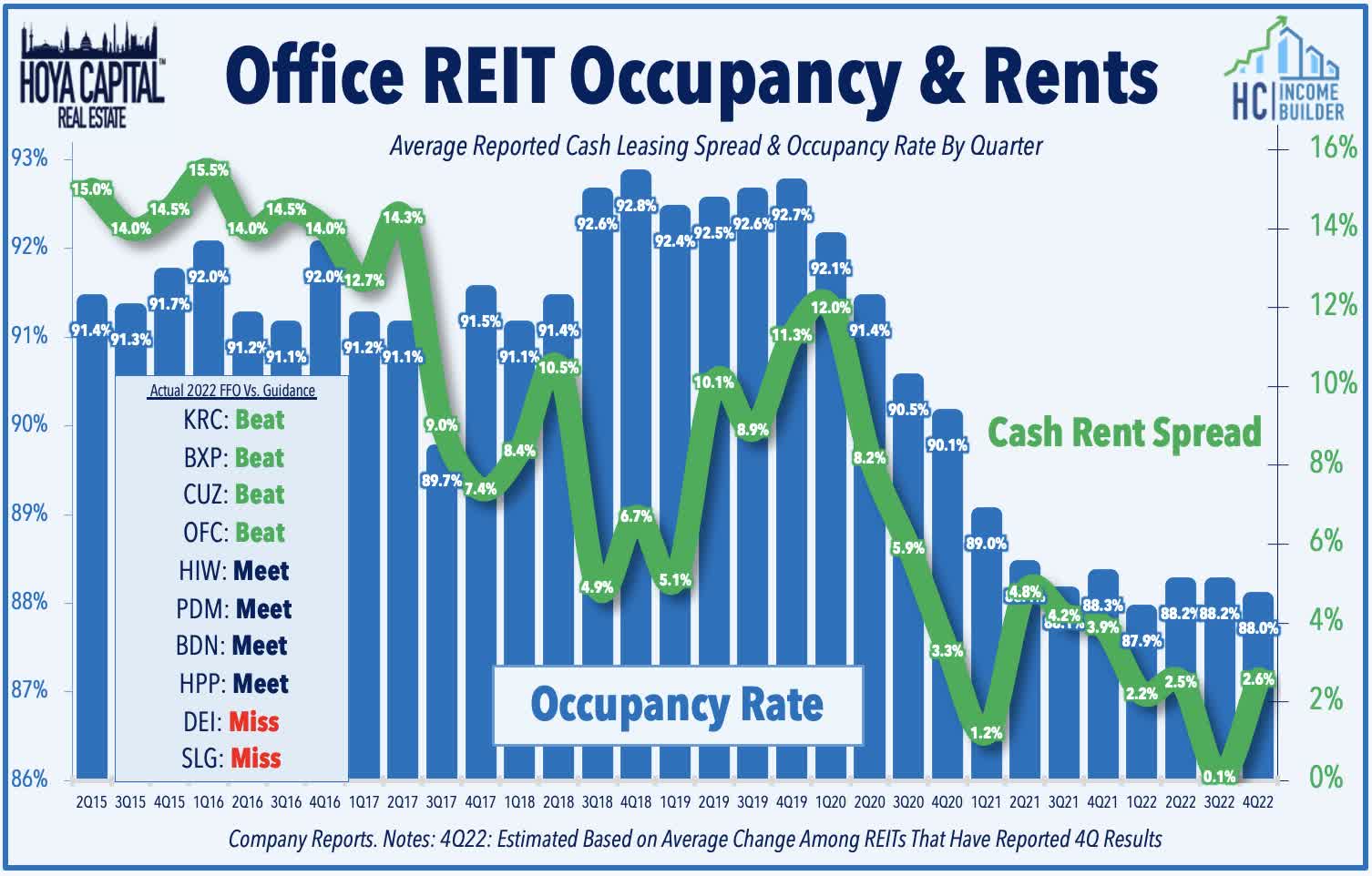

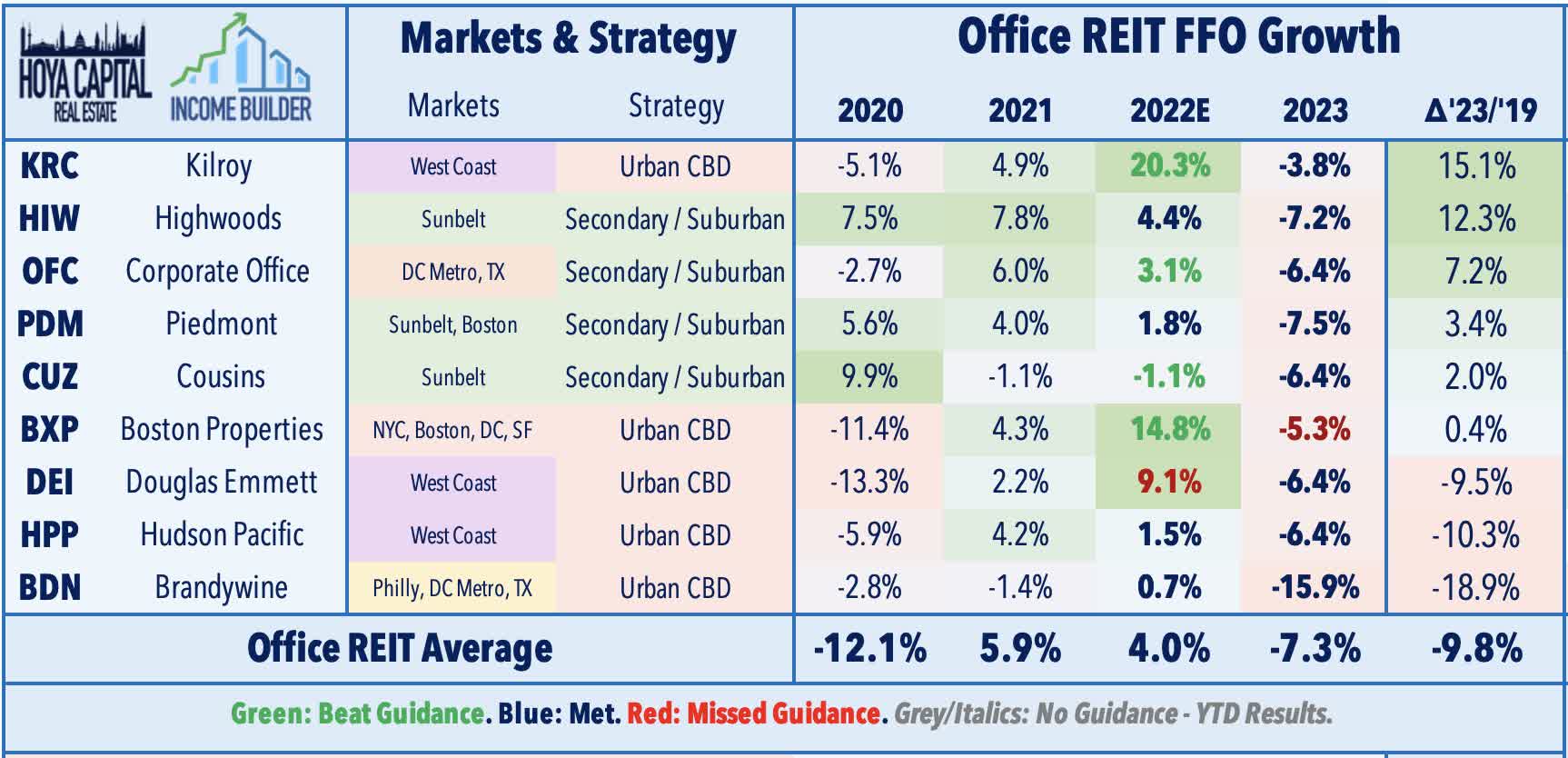

Office : (Halftime Grade: B) We've seen results from 10 of the 22 office REITs - reports that provided both reasons for optimism and for pessimism. Thus far, office REITs have reported relatively steady demand with total leasing volume still hovering at around 75% of pre-pandemic levels - a decent velocity considering the still-depressed utilization rates in major markets - and rent spreads that have remained modestly positive for most REITs - particularly those focused outside of the NYC and California markets. Among the ten reports, four REITs reported full-year FFO that exceeded their prior guidance with upside standouts being Cousins ( CUZ ) and Kilroy ( KRC ). A pair of REITs missed their prior forecast - SL Green ( SLG ) and Douglas Emmett ( DEI ) - amid particular weakness in their Manhattan and Los Angeles markets.

{kind=link}

The FFO outlook for 2023, however, has been notably soft across the sector with all 9 REITs projecting a decline in FFO of at least 5%. We've observed a continued outperformance from REITs focused on Sunbelt and secondary markets with all four of these REITs ( HIW , CUZ , PDM , and OFC ) projecting 2023 FFO that will remain above their pre-pandemic level from 2019. Among the urban-focused REITs, we were pleasantly surprised by Hudson Pacific ( HPP ), which noted that its full-year FFO rose 1.5% in 2022 - in-line with its prior guidance - and forecasts that its FFO will decline by 6.4% for full-year 2023, which is a less-steep decline than the office sector-average. Leasing demand was surprisingly solid with total volume of 517k SF - its third-highest-volume quarter since 2019 - with cash rent spreads and occupancy rates each essentially flat for the quarter. Brandywine ( BDN ) also deserves recognition for successfully completing $705M in asset sales in Q4 and using the proceeds to refinance its looming $350M debt maturity and pay down its $600M line of credit, pushing out the majority of its maturities beyond 2026.

{kind=link}

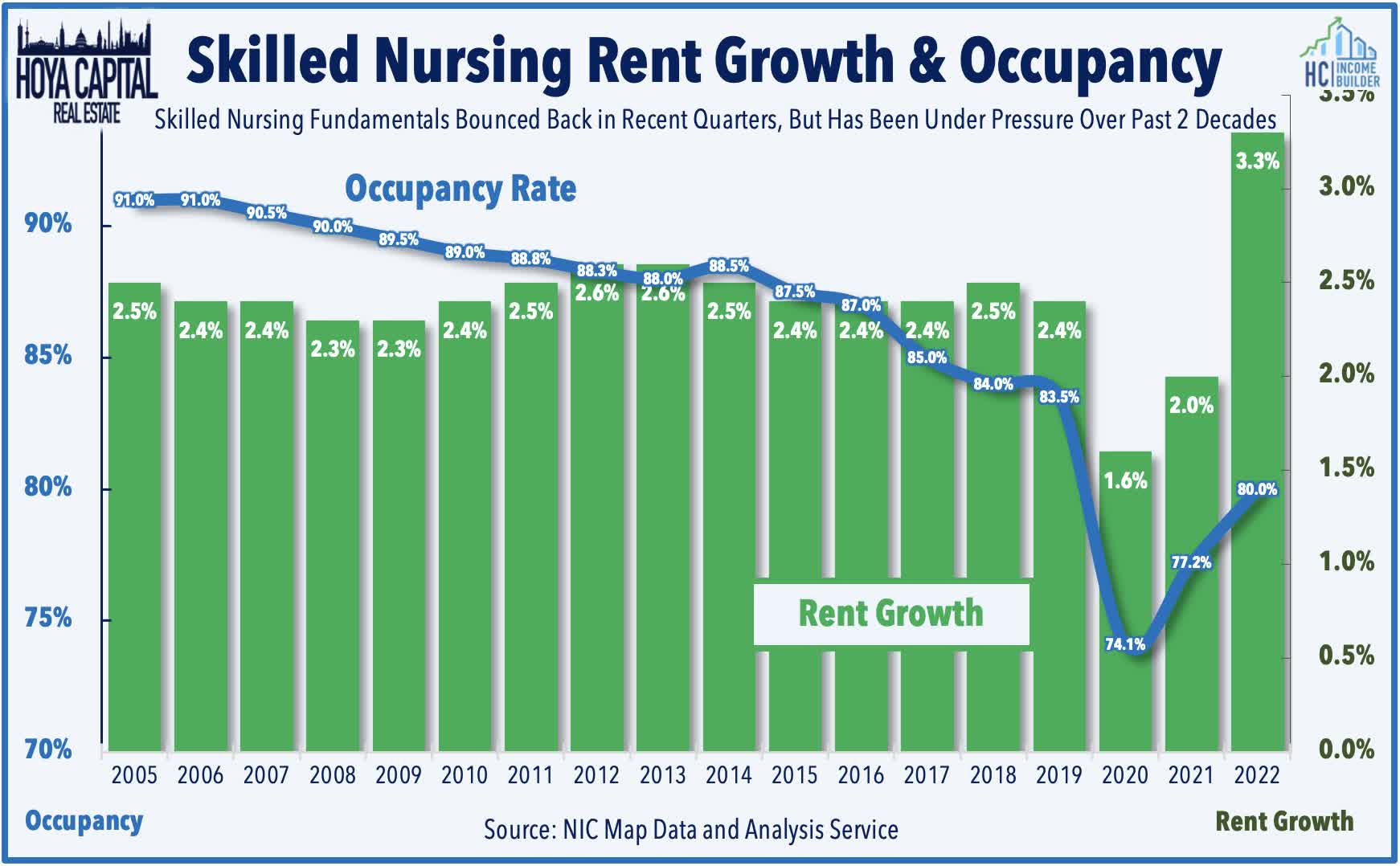

Healthcare : (Halftime Grade: C+) Tenant operator struggles have again become the major focus of healthcare REIT reports as pandemic-related government support has waned in recent quarters. Skilled nursing REIT Omega Healthcare ( OHI ) highlighted some progress in lease restructurings which it expects will result in improved operating performance as the year progresses and the ability to cover its dividend with its Funds Available for Distribution. OHI commented that it remains "optimistic on the long-term skilled nursing facility industry prospects, [but] cautious in the near-term as our operators contend with staffing issues" and a relatively slow return of occupancy levels back towards pre-pandemic levels. Gibbins Advisors reported last month that bankruptcy filings for healthcare companies nearly doubled in 2022 compared to the prior year which it attributes to a “COVID hangover” resulting from waning government support and higher labor costs.

{kind=link}

Lab space owner Alexandria ( ARE ) has been the upside standout within the healthcare sector, reporting very strong results, projecting 2023 full-year FFO growth of 6.4% while recording blended leasing spreads of 19.6% in Q4 and 22.1% for full-year 2022 - its second-highest annual cash-basis rental rate growth in its history. Notably, after three-quarters of sequentially declining leasing volume following a record surge in late 2021, ARE reported an acceleration in leasing volume to 2.0M square feet - its fourth-best quarter on record - pushing back on concerns over softening demand from reduced biotech and pharmaceutical hiring. ARE projects that it will achieve cash rent spreads between 11-16% for full-year 2023 with an occupancy rate of 95.3% while achieving same-store NOI growth of 5.0% at the midpoint.

{kind=link}

Retail REIT Halftime Report

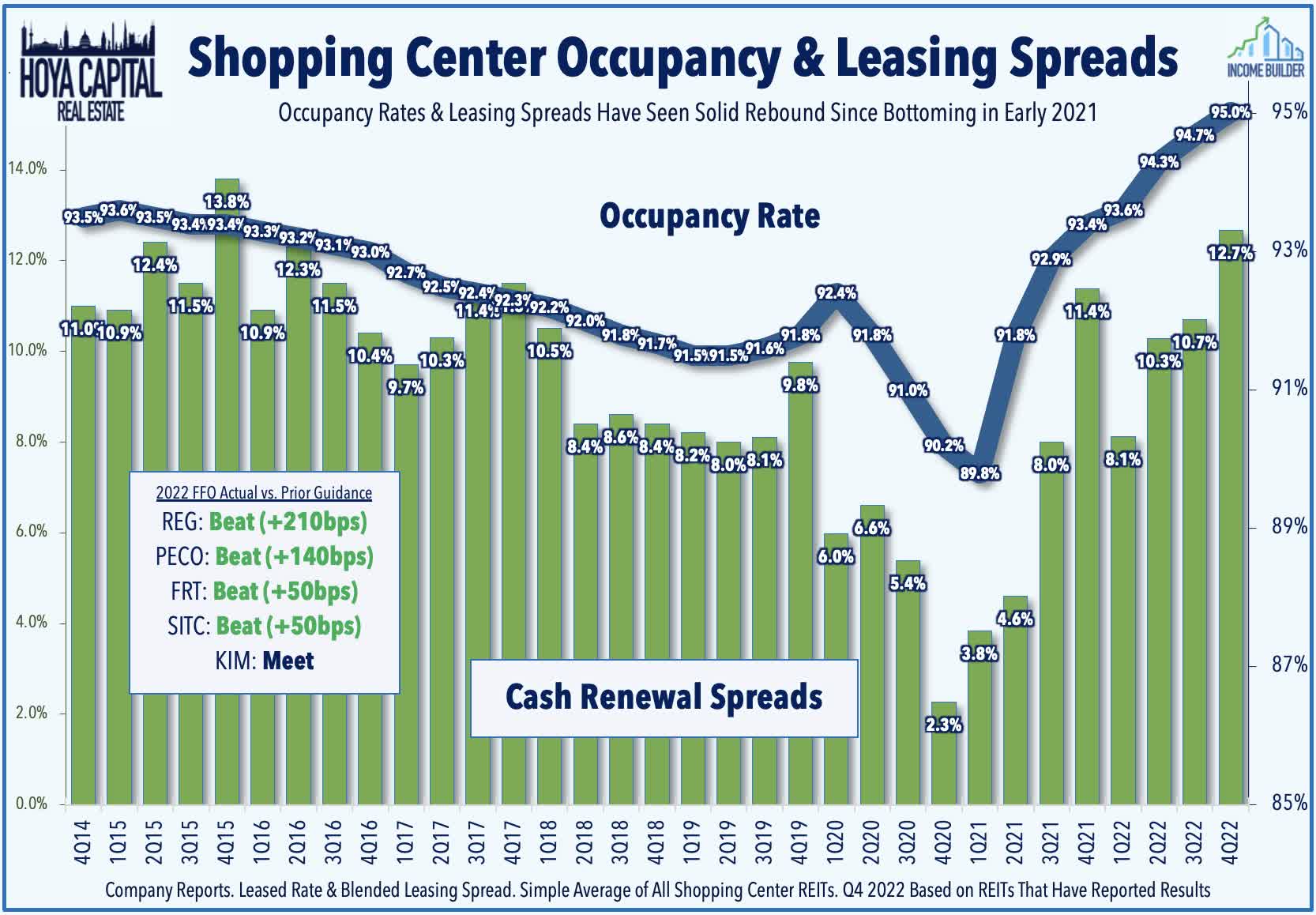

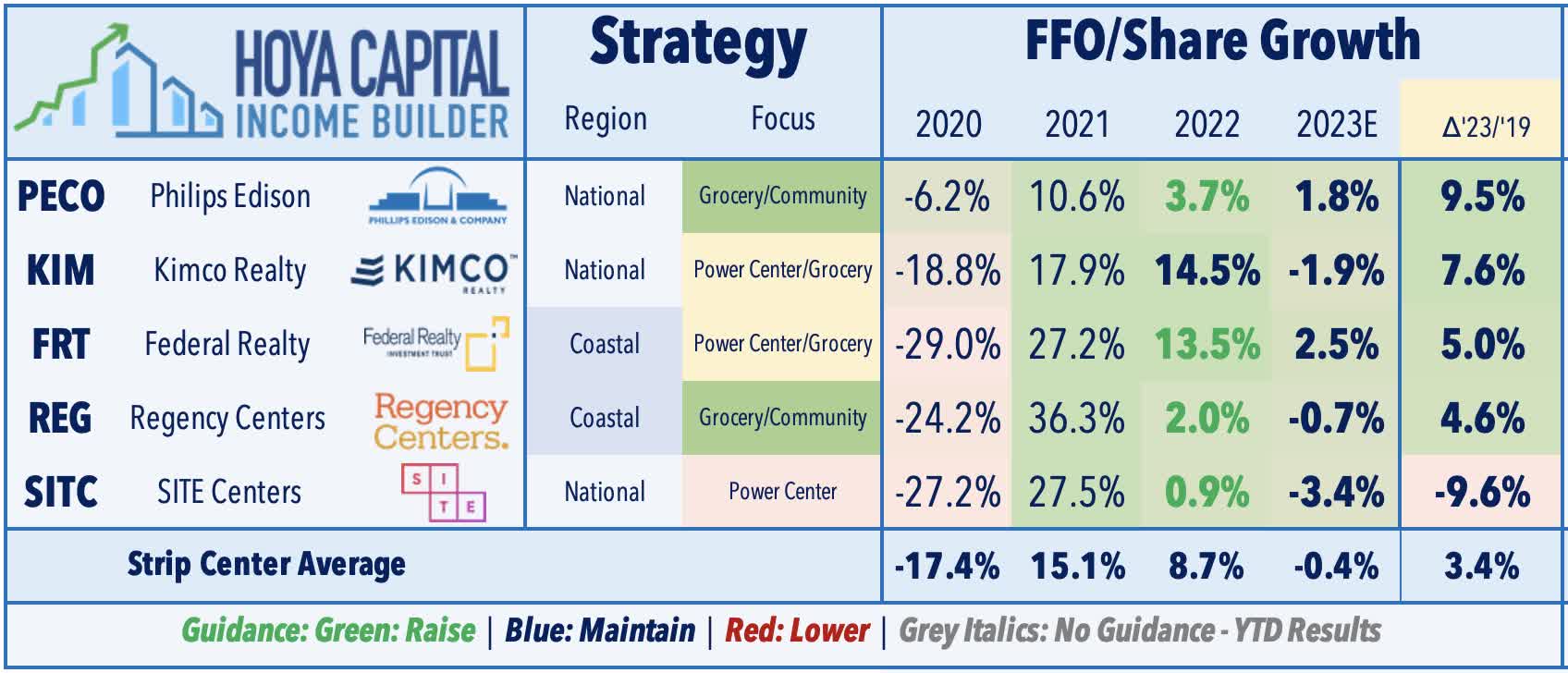

Strip Centers : (Halftime Grade: A-) Earnings season is still young for the retail sector, but results thus far have been quite solid - continuing a trend of better-than-expected results stretching back to late 2021 as demand for "big box" space has significantly exceeded the available supply. We've heard results from five of the 16 shopping center REITs - four of which have reported full-year FFO that was above their prior guidance. Regency Centers ( REG ) has been an early upside standout, reporting full-year 2022 FFO that topped its prior forecast by 210 basis points. Importantly, all five REITs have reported a sequential acceleration in rent growth - which are on-pace for the second-best quarter in a decade - and an improvement in occupancy rates to the highest on record. Kimco ( KIM ) reported the most significant sequential acceleration in rent growth to 8.7% in Q4 - its strongest in three years - while achieving its highest year-over-year occupancy rate increase in 15 years alongside solid rent growth trends with blended cash leasing spreads of 8.7%

{kind=link}

Same-store occupancy rates among these five REITs climbed by an average of 35 basis points from last quarter and 140 from last year while rent growth is on-pace to be in the double-digits for a third-straight quarter. These five shopping center REITs see muted FFO growth in 2023, however, due in part to expectations of near-term vacancies from several bankrupt or near-bankrupt retailers including Pa rty City and Bed Bath ( BBBY ). Notably, SITE Centers ( SITC ) noted that several tenants are eying potentially-vacated space from these two retailers and that it expects to pursue an "aggressive recapture of space" given the backlog of demand rather than renegotiate leases. Four of the five REITs expect 2023 FFO to remain above that of 2019, led on the upside by Phillips Edison ( PECO ) and Kimco ( KIM ).

{kind=link}

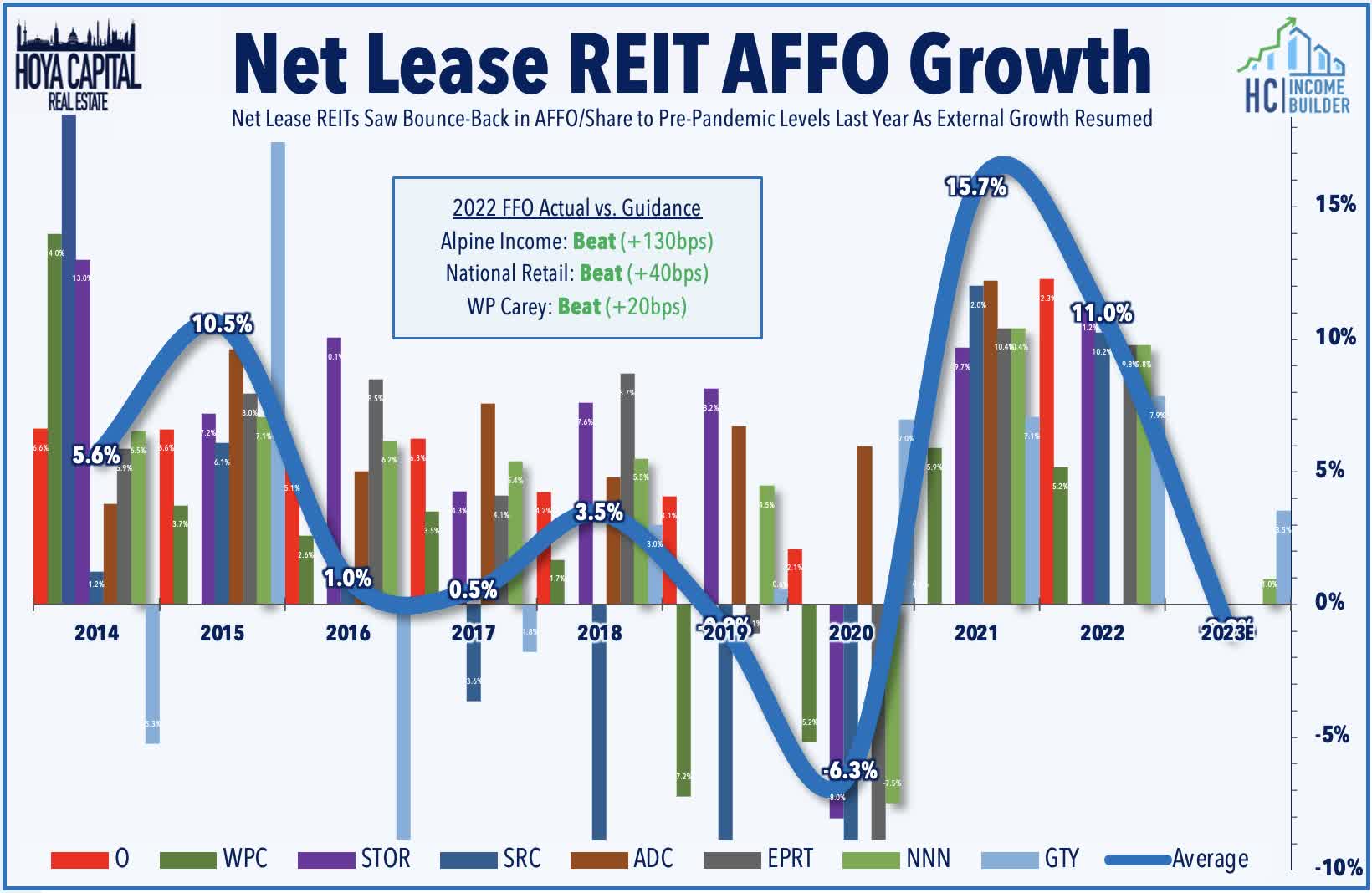

Net Lease : (Halftime Grade: B-) While still very early in net lease earnings season with results from just 3 of 16 REITs, the lack of movement in cap rates and the "business as usual" tone has been notable. National Retail ( NNN ) kicked-off net lease earnings season with an in-line report, noting that its full-year FFO rose 9.8% in 2022 - 40 basis points above its prior guidance - and forecasts FFO growth of 1.0% for full-year 2023. Most notably, NNN acquisition cap rate of 6.6% in Q4 was only 10 basis points above its 6.5% cap rate in Q4 of 2021 during which time the 10-Year Treasury Yield surged 230 basis points - a topic we discussed in Net Lease REITs: Calling The Fed's Bluff , which noted that net lease executives, investors, and asset owners have seemingly never bought into the idea of a "new normal" of sustained higher interest rates. W.P. Carey ( WPC ) reported stronger results, however, which continues to benefit from the embedded CPI-based rent increases in its portfolio. WPC noted that its acquisition cap rates averaged 6.8% in Q4 - up 80 basis points from last year while Alpine Income ( PINE ) recorded a 120 basis point increase in acquisition cap rates from last year.

{kind=link}

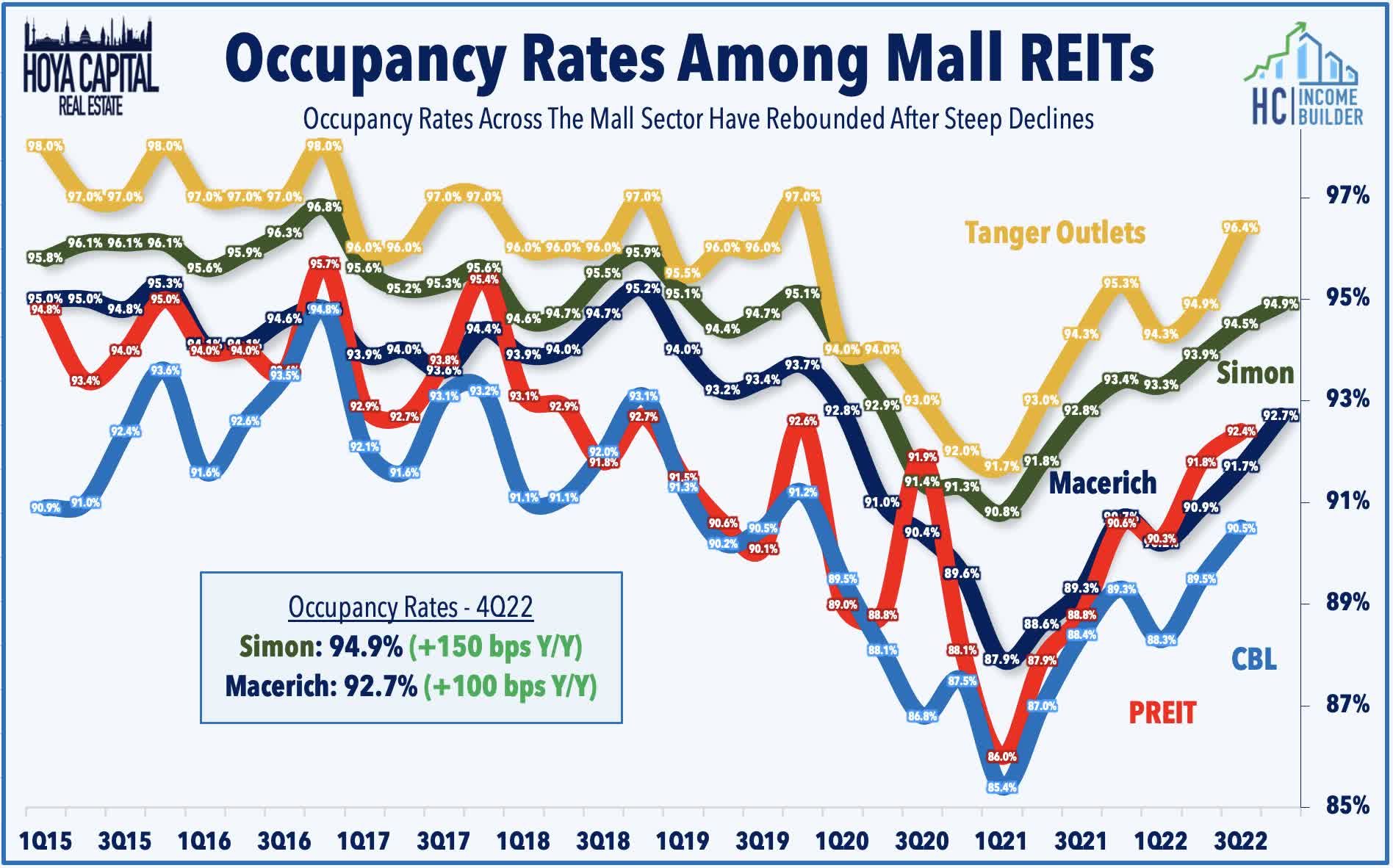

Mall : (Halftime Grade: C+) While not displaying the outright strength seen in the strip center format, mall fundamentals have stabilized in recent quarters for properties in the upper-end of the quality tiers. Simon Property ( SPG ) reported decent results, noting that its FFO declined 0.6% in 2022 - slightly above the midpoint of its prior guidance - while projecting that its 2023 FFO will be roughly even with 2022. Comparable occupancy climbed to 94.9% in Q4 - up 150 basis points from last year and exceeding the average pre-pandemic occupancy rate of 94.8% in full-year 2019. Average base rents rose 2.3% in Q4, which was the highest since Q1 2020. Macerich ( MAC ) reported relatively weaker results, however, noting its FFO declined by 3.4% in 2022 - matching the midpoint of its prior guidance range - but projecting an 8.2% decline in FFO for full-year 2023. MAC's comparable occupancy rates rose to 92.7% - up 100 basis points from last year but still 100 basis points below its pre-pandemic level. Leasing spreads rose 0.3% on a trailing twelve-month basis, a deceleration from the 3.3% rate reported last quarter.

{kind=link}

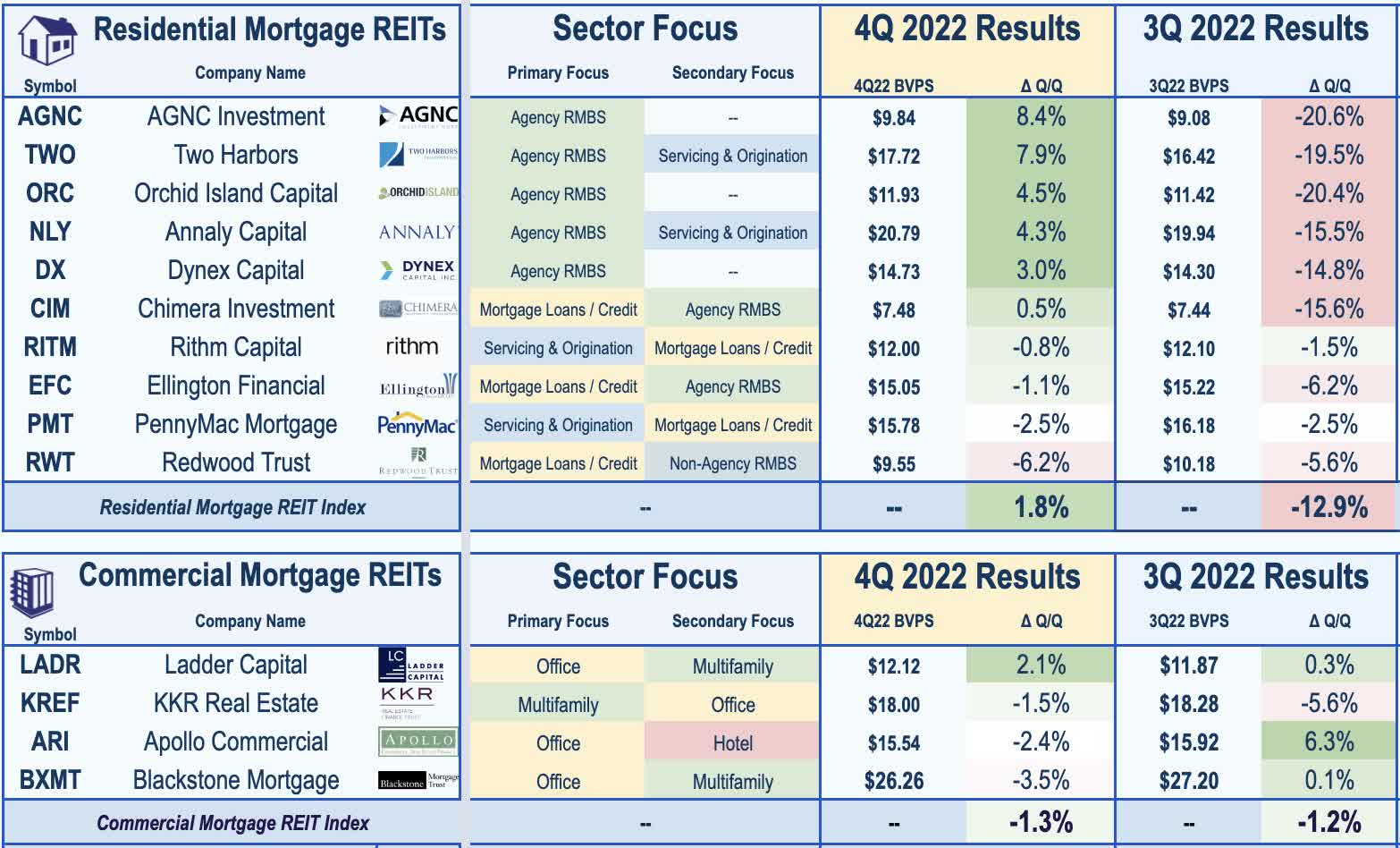

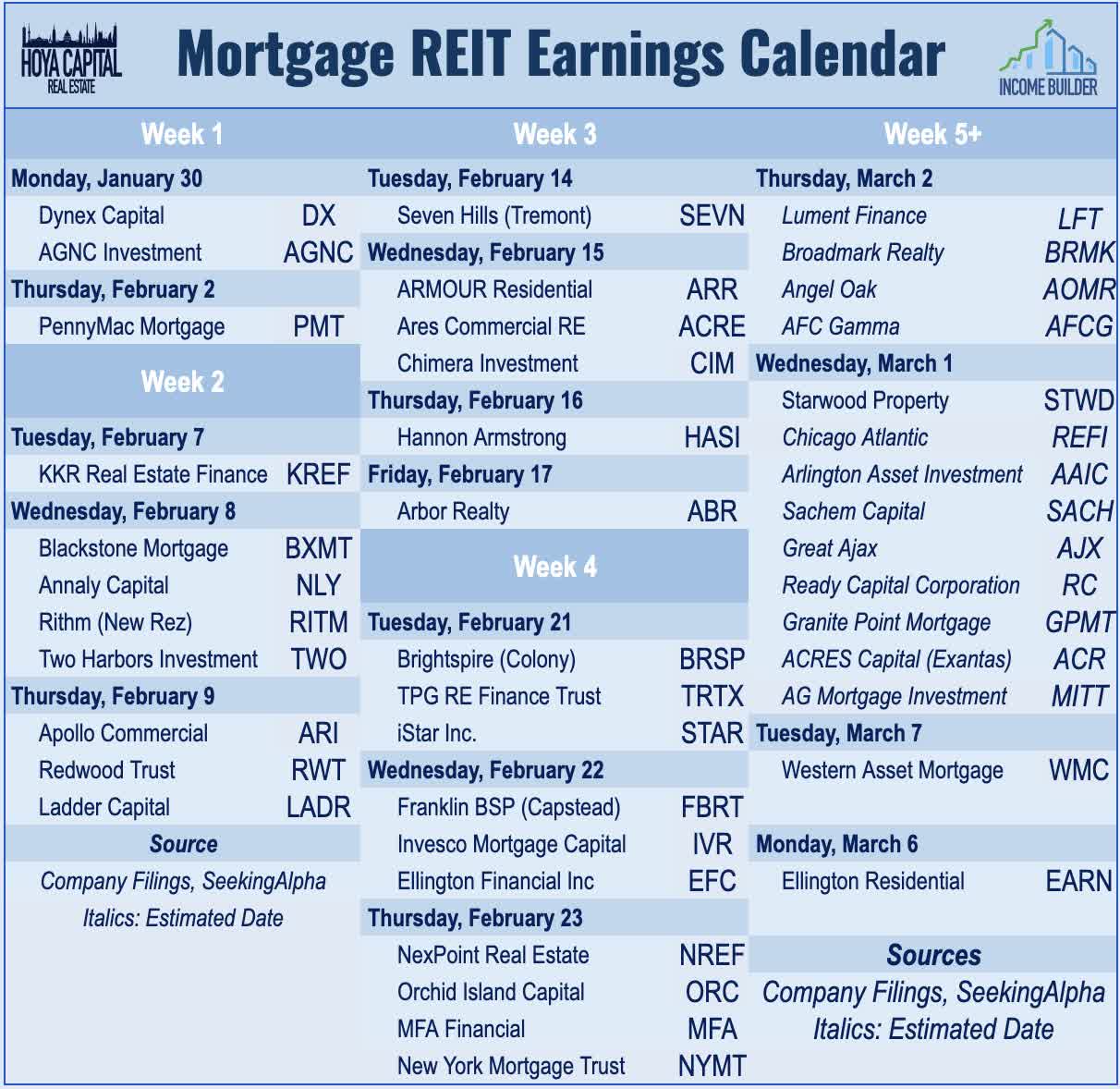

Mortgage REITs Halftime Report

Residential mREITs : (Halftime Grade: B-) We've seen results and/or preliminary fourth-quarter results from 10 of the 24 residential mREITs. Consensus expectations called for Book Value Per Share ("BVPS") to increase in the low-to-mid-single digits following a period of steep declines in mid-2022. and thus far, we've seen an average BVPS increase of roughly 2%. As expected, we've seen a more pronounced rebound from the agency-focused mREITs led by AGNC Investment ( AGNC ), which reported an 8.4% bounce in its BVPS followed by Two Harbors ( TWO ) at 7.9%. Results from credit-focused and servicing-oriented mREITs Rithm Capital ( RITM ) were also solid, recording muted changes in its BVPS for a second-straight quarter. Annaly Capital ( NLY ) reported decent results but warned that it expects to reduce its quarterly dividend by about 25% in Q1 in anticipation of "some further pressure on Earnings Available For Distribution going forward."

{kind=link}

Commercial mREITs : (Halftime Grade: B) On the commercial mREIT side, we've seen results from 4 of the 17 commercial mREITs, where the movement in BVPS remains far more muted on a quarter-to-quarter basis. Declining interest rates in Q4 have put mild downward pressure on floating-rate-focused mREITs including Blackstone Mortgage ( BXMT ) - which reported a 3.5% decline in its BVPS following a 0.1% increase in Q3 - and Apollo Commerical ( ARI ) - which reported a 2.4% decline in its BVPS following an impressive 6.3% increase in Q3. Ladder Capital ( LADR ) is the leader in the clubhouse thus far, reporting a 2.1% increase in its BVPS. None of the four mREITs reported any major issues with loan performance with BXMT noting 100% interest collection while loan repayment and refinancing activity remains muted. LADR specifically noted "stable performance" in its office loan portfolio, pushing back on recent concerns. Dividend-related commentary on earnings calls has been reassuring with no indication of imminent reductions among these four commercial mREITs.

{kind=link}

Previewing The Second-Half of Earnings

At the halfway point of another consequential real estate earnings season, results have modestly exceeded expectations with 56% of REITs reporting 2022 Funds From Operations ("FFO") above their prior guidance while 3 (8%) missed their guidance. For the back-half of REIT earnings season, we remain focused on the three high-level themes discussed in our REIT Earnings Preview: 1) Cap Rates & Private Market Valuations; 2) Balance Sheets & Rate Expectations; and 3) Full-Year 2023 FFO Guidance. Apart from these themes, we've also been focused on dividend commentary - particularly in sectors at the upper-end of the payout ratio spectrum. We'll continue to provide real-time coverage in our Daily Recap Blogs along with extended follow-up analysis for Hoya Capital Income Builder members throughout earnings season.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

REIT Earnings Halftime Report