VRE - REIT Earnings Halftime Report

2023-05-02 09:00:00 ET

Summary

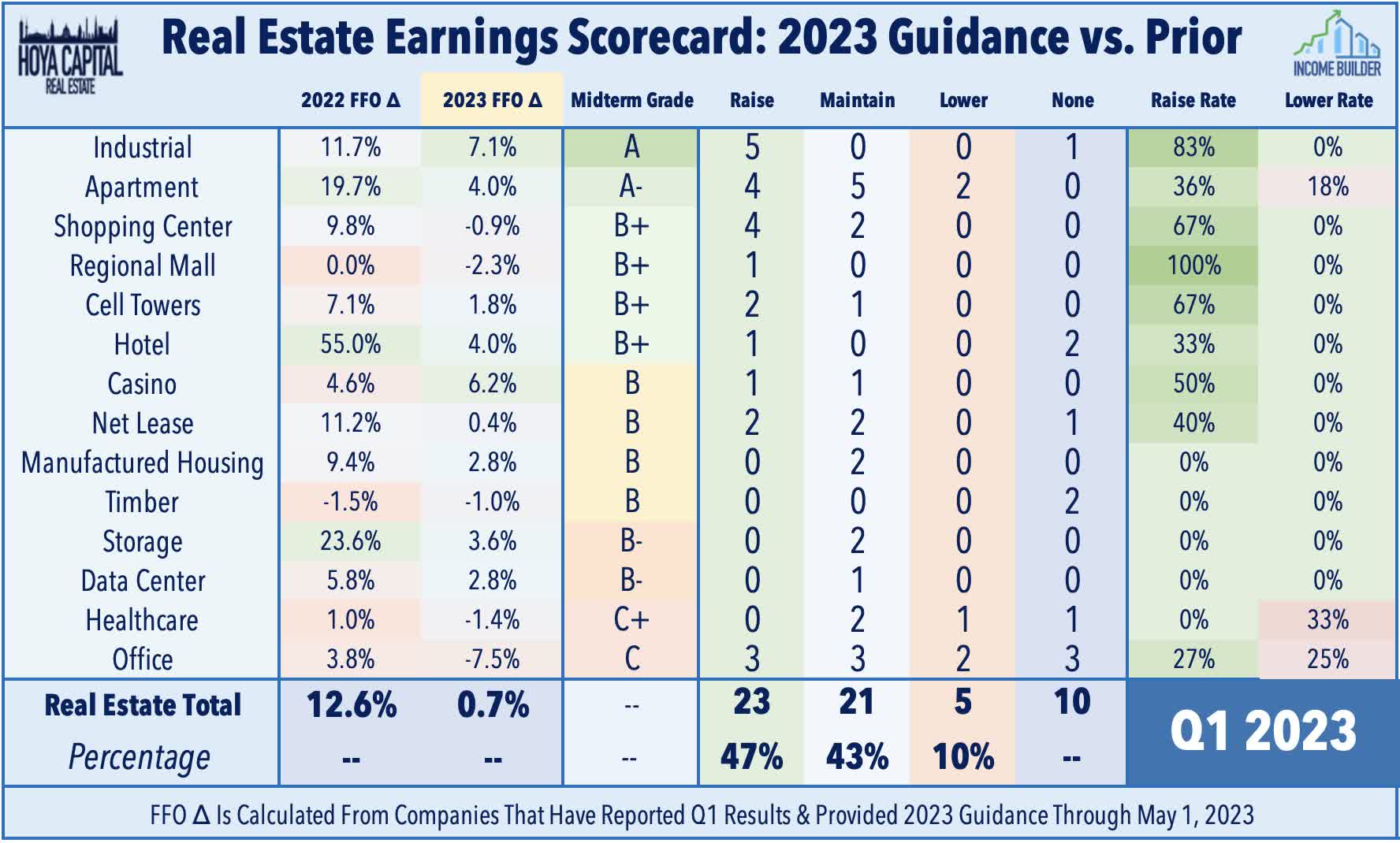

- We're now at the halfway point of real estate earnings season with roughly 60 equity REITs and 14 mortgage REITs representing 50% of the total market capitalization having reported first-quarter.

- Results thus far have been better than the prevailing narrative would suggest. Of the 49 REITs that provide guidance, 23 (47%) raised their full-year earnings outlook while 5 (10%) lowered.

- Office and commercial mortgage REITs have been in focus given the stiff work-from-home headwinds and shaky dividend outlook. Vornado suspended its dividend, but results have otherwise been decent thus far.

- Apartment and Industrial REITs have accounted for nearly half of the guidance boosts thus far. Residential rent growth appears to have firmed in recent months after a rather sharp cooldown in late 2022 amid a broader Spring revival across the housing sector.

- While still early in earnings season for other sectors, retail REITs have reported impressive leasing momentum. Healthcare REITs' operator issues have remained status-quo. More broadly, REITs appear content in remaining hunkered down with muted appetite for aggressive external growth.

Real Estate Earnings Halftime Report

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on April 27th.

{kind=link}

We're now at the halfway point of real estate earnings season with roughly 60 equity REITs and 14 mortgage REITs representing 50% of the total market capitalization having reported first-quarter. Results thus far have been far-better than the prevailing narrative would suggest. Of the 49 REITs that provide guidance, 23 (47%) raised their full-year earnings outlook, while 5 (10%) lowered guidance, which is pacing slightly ahead of the historic average for the first-quarter. Apartment and Industrial REITs have accounted for nearly half of the guidance boosts thus far. Residential rent growth appears to have firmed in recent months after a rather sharp cooldown in late 2022 amid a broader Spring revival across the housing sector.

{kind=link}

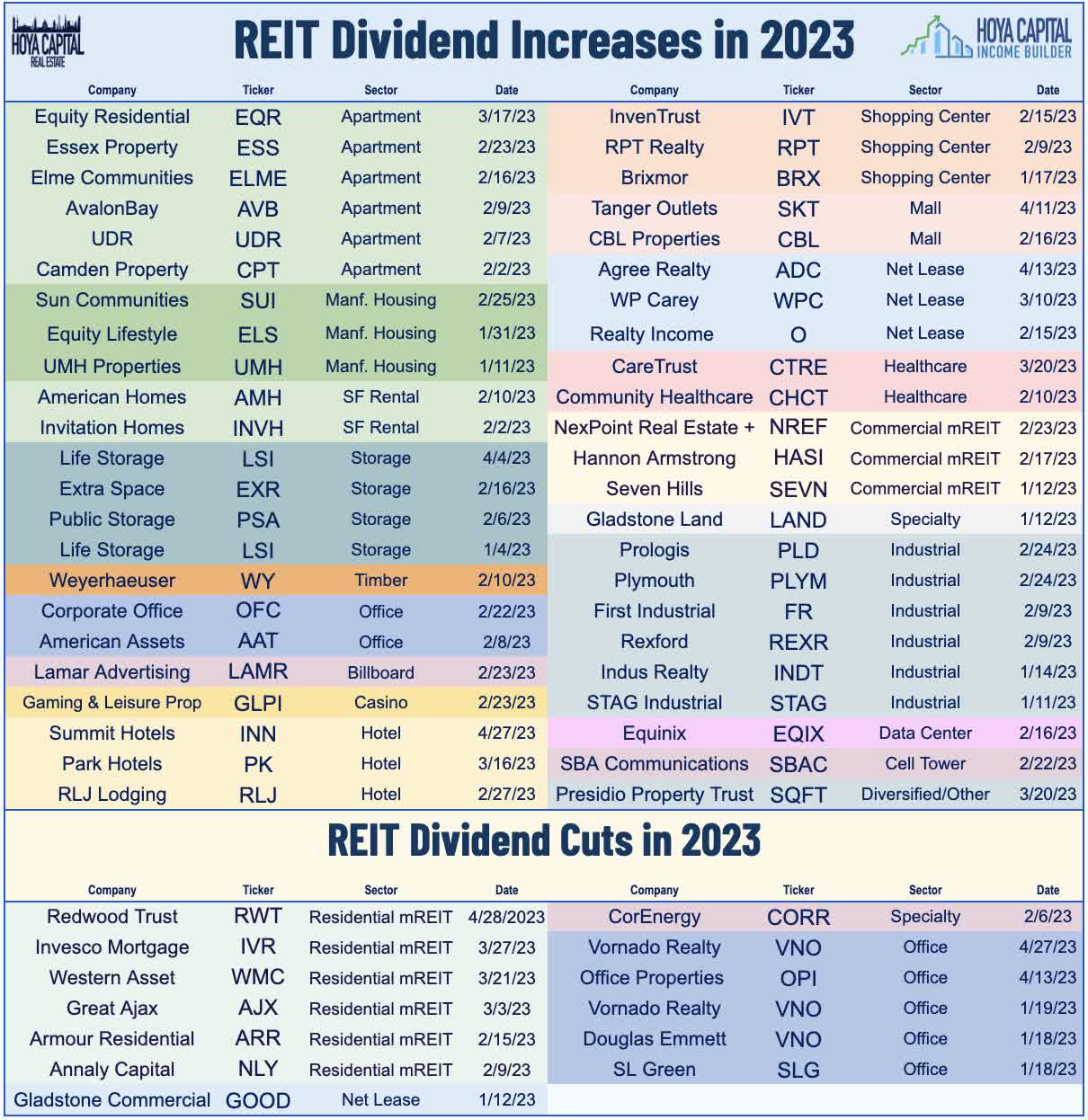

As discussed in our Earnings Preview , the major higher-level themes that we're focused on this earnings season include: 1) Cap Rates, Valuations, and Credit Conditions; 2) Acquisition Plans & Distress Opportunities; 3) Balance Sheets & Variable Rate Debt Exposure; and 4) Full-Year 2023 Guidance Updates. Overall, commentary across earnings calls indicates that REITs appear content in remaining "hunkered-down" for now, expressing muted appetite for aggressive external growth. Apart from these themes, we've also been focused on dividend commentary - particularly in sectors at the upper end of the payout ratio spectrum. We've seen two REITs add their names to the dividend cut list: office REIT Vornado ( VNO ) and residential mortgage REIT Redwood Trust ( RWT ), bringing the full-year total to 13 REIT dividend cuts. A trio of names have hiked their dividend over the past two weeks: Tanger Factory Outlet ( SKT ), Summit Hotel ( INN ), and Community Healthcare ( CHCT ), lifting the full-year total to 46 REIT dividend hikes.

{kind=link}

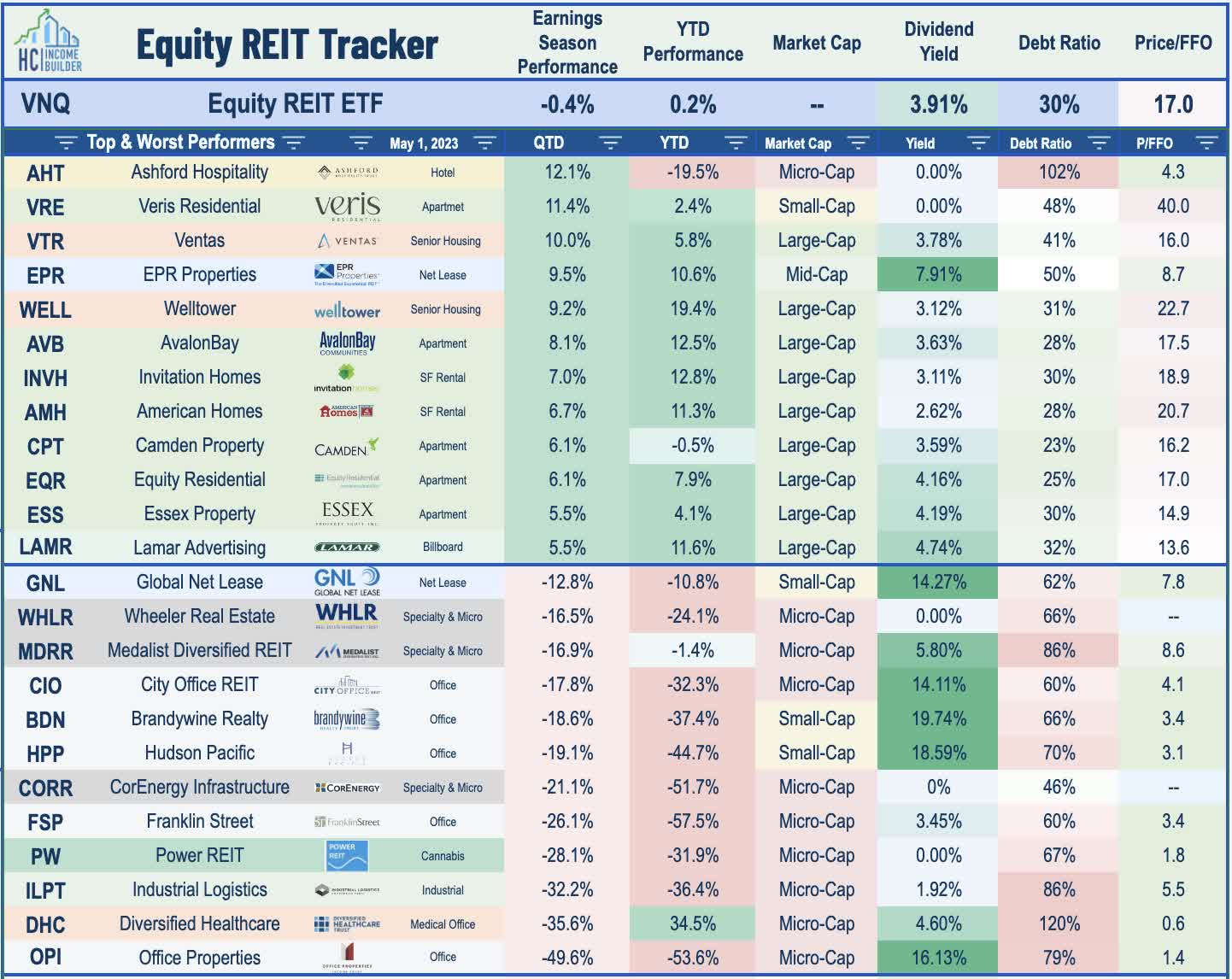

Performance trends have been generally consistent with these trends, with apartment and industrial REITs producing the strongest returns since the start of earnings season in early April. Senior housing REITs have also been notable upside standouts ahead of their results in the back half of earnings season. Office REITs have remained under pressure, as have other more-highly-levered small- and micro-cap REITs, consistent with a "flight to quality" theme we've observed throughout the year. A trio of RMR-managed REITs have been the losers this earnings season thus far following the controversial merger between Office Properties ( OPI ) and Diversified Healthcare ( DHC ), which has sent shares of both companies sharply lower. Below, we discuss our halftime analysis and grades for each property sector.

{kind=link}

Residential Real Estate Halftime Report

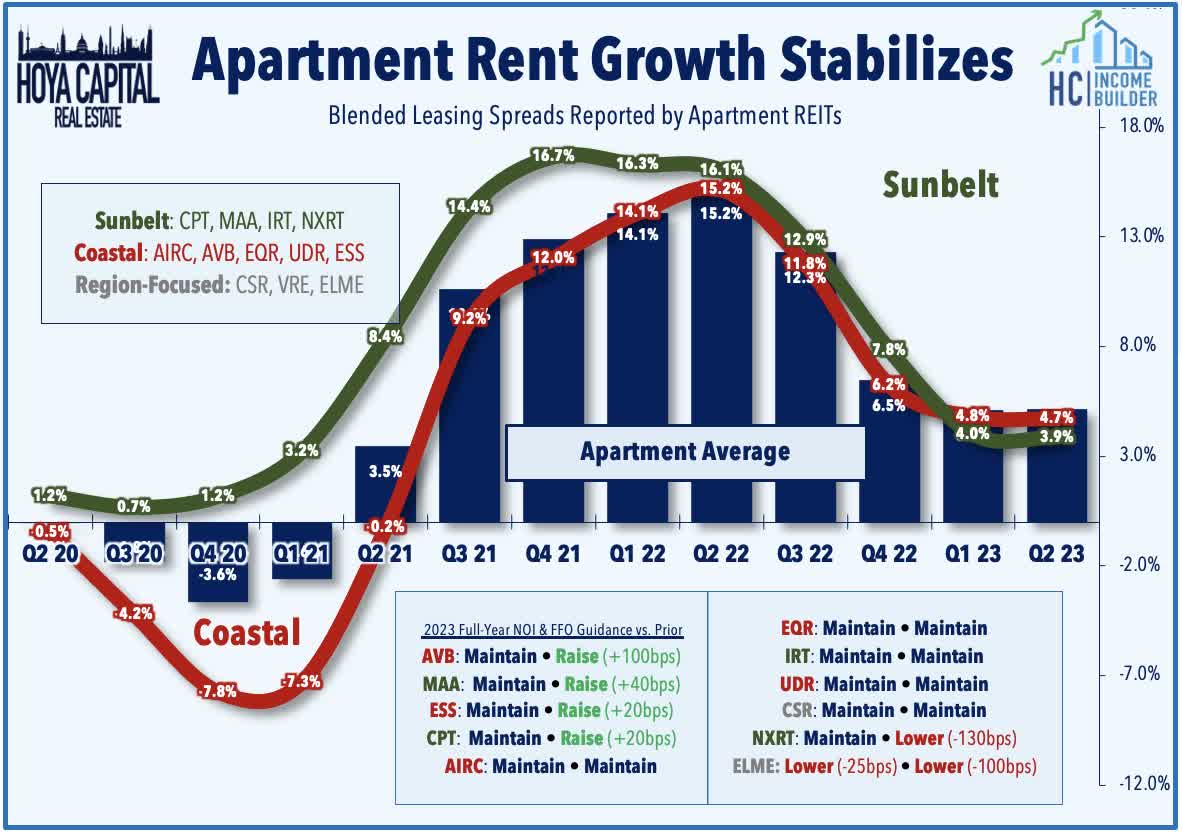

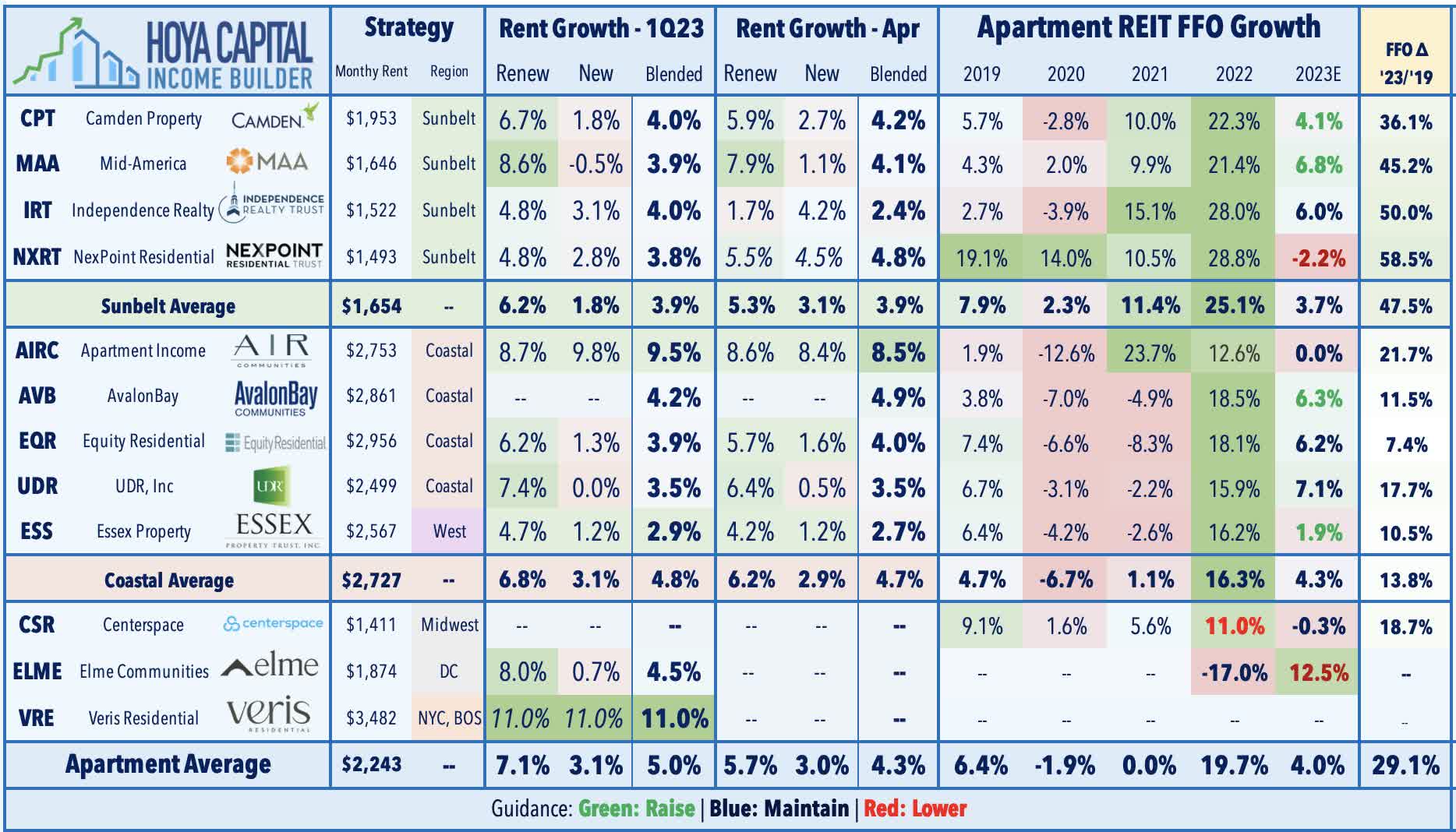

Apartment : (Halftime Grade: A-) While several property sectors haven't yet started earnings season, apartment REIT earnings season is essentially complete. Results have generally been better than expected as residential rent growth appears to have firmed in recent months after a rather sharp cooldown in late 2022 amid a broader Spring revival across the housing sector. Four apartment REITs hiked FFO estimates - two Sunbelt-focused REITs and two coastal-focused REITs - while both regions reported nearly identical 4% blended rent growth in Q1 with a slight acceleration in April, consistent with recent data from Apartment List and Zillow showing that rental rate trends have firmed in recent months following a sharp deceleration in late 2022. While commentary indicated expectations of supply headwinds later this year, most REITs have seen a slowdown in starts given tighter credit conditions.

{kind=link}

AvalonBay ( AVB ) raised its full-year FFO growth outlook to 6.3% - up 100 basis points from last quarter. AVB commented that its recent leasing activity is "materially exceeding initial rent and yield expectations." Mid-America ( MAA ) reported similarly strong results and raised its full-year FFO growth outlook to 6.8% - up 40 basis points from its prior outlook. Results from West Coast-focused Essex ( ESS ) were surprisingly solid, echoing commentary from Equity Residential ( EQR ), which noted that rent collection in California hasn't been as problematic as initially feared. Results from Veris Residential ( VRE ) showed surprisingly strong rent trends in the NYC market, recording a sector-leading 11% rent spread. NexPoint Residential ( NXRT ) was the lone major apartment REIT to lower its FFO outlook - a revision driven by higher interest expense - but the small-cap REIT also reported perhaps the strongest property-level metrics, reiterating its call for 11% NOI growth this year.

{kind=link}

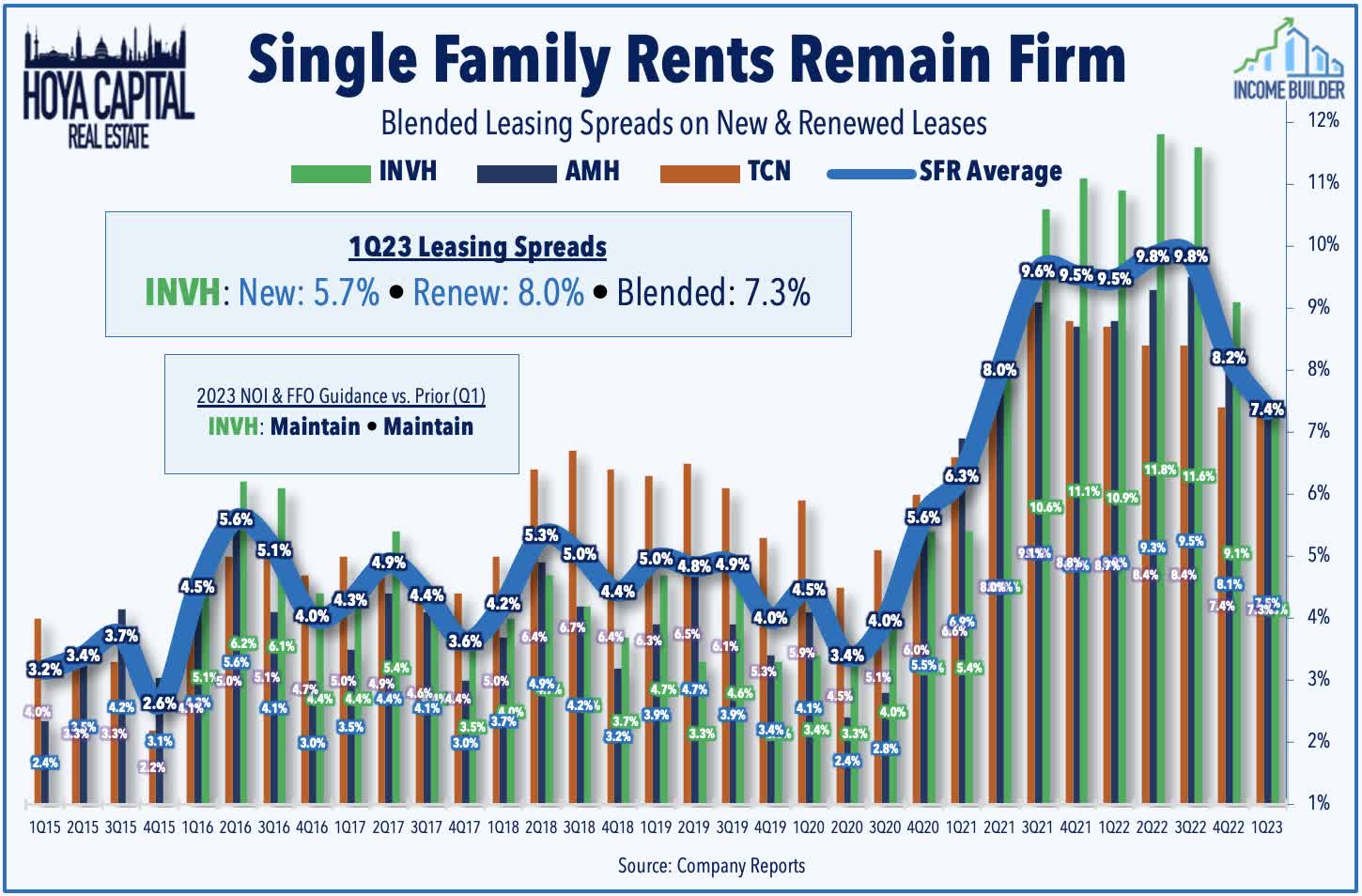

Single-Family Rental : (Halftime Grade: B) Just one of the three SFR REITs has reported results thus far. Invitation Homes ( INVH ) reported in-line results and maintained its full-year outlook, which calls for FFO growth of 4.3% and NOI growth of 4.8%. Rent collection was better than expected at 99% of the company's historical average - steady with Q4 - as concerns of significant rent loss in its California markets haven't materialized. Consistent with reports from apartment REITs this earnings season, INVH reported relatively buoyant rental rate trends in Q1, with renewal rent growth of 8.0% and new lease rent growth of 5.7%, resulting in blended rent growth of 7.3%. As with MH RETIs, operating expenses remain in focus and Q1 did little to ease concerns over cost pressures as core operating expenses jumped 14.0% year over year, driven primarily by an increase in property tax.

{kind=link}

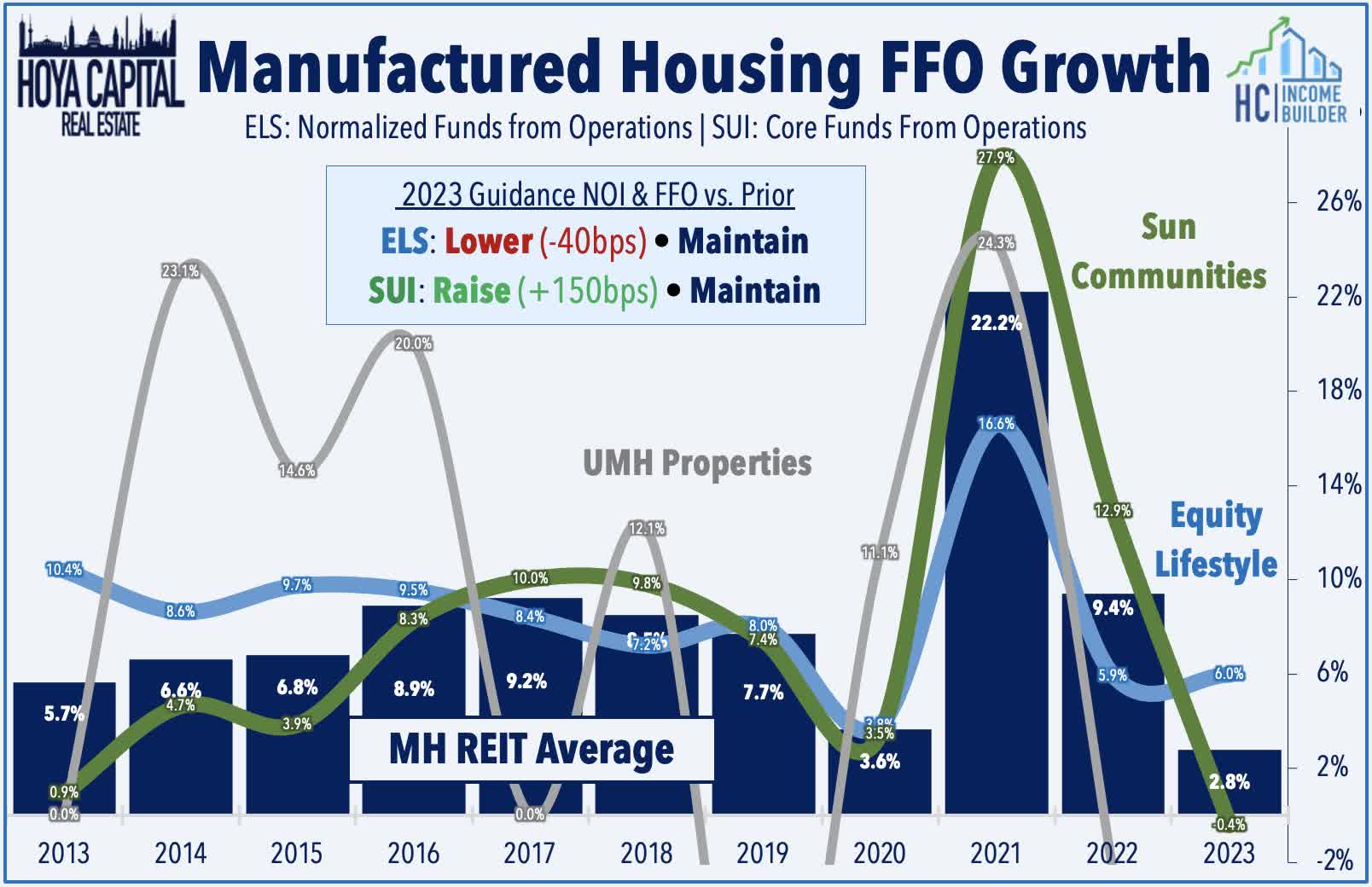

Manufactured Housing : (Halftime Grade: B) Sticking in the residential sector, results from Equity LifeStyle ( ELS ) and Sun Communities ( SUI ) were generally in line with expectations, with each maintaining their full-year FFO outlook. Both cited strong pricing trends in their core manufacturing housing segment and their marina divisions, which was offset by some lingering softness in their RV segment - an area that has been impacted by higher fuel prices and a post-COVID normalization. Expense concerns - primarily related to weather and insurance premiums - have also been a focus. Of note, ELS reported that its premiums on its property and casualty insurance increased by 58% year-over-year, with SUI incurring a similar double-digit increase in the prior quarter. While SUI's marina investments appear to be working out well, performance from SUI's UK portfolio has raised concerns following a rather significant downward revision to its revenue guidance for this segment, which it attributes to lower home sales expectations.

{kind=link}

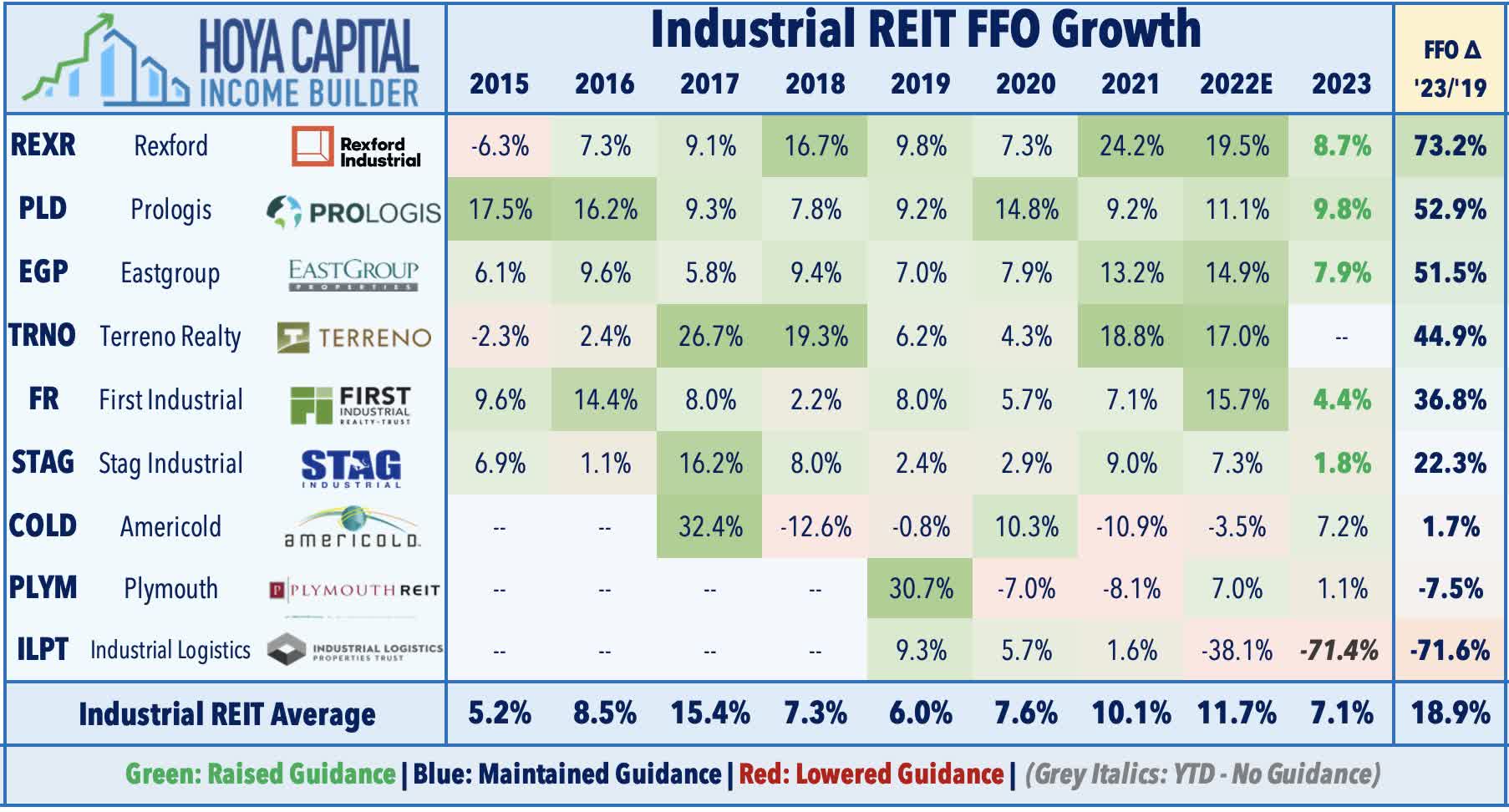

Industrial & Technology REIT Halftime Report

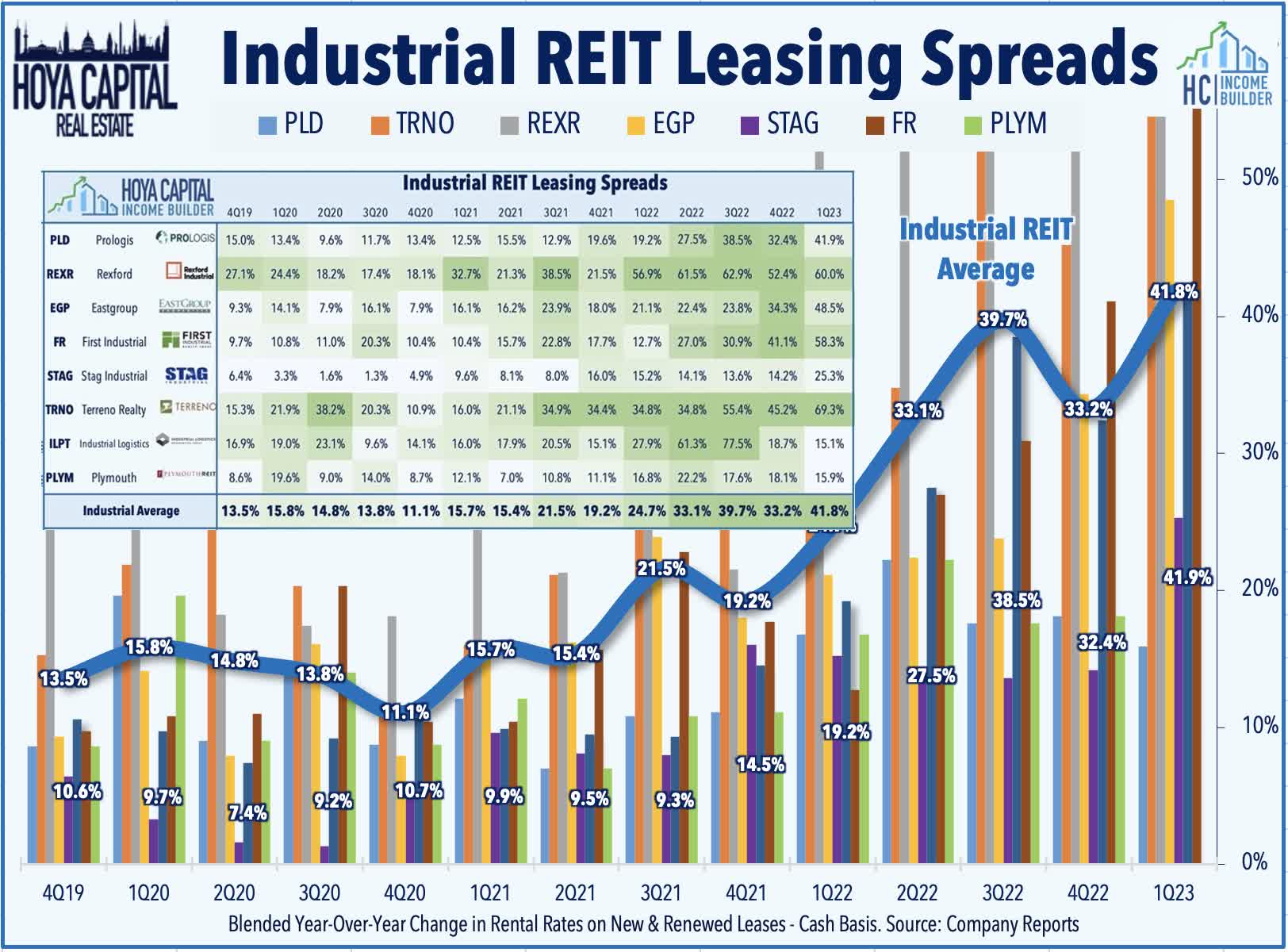

Industrial : (Halftime Grade: A) "Beat and raise" has been the prevailing theme thus far across the results from the five largest industrial REITs, each of which have increased their full-year NOI and FFO guidance. After a rent growth moderating in late 2022 - which many expected to continue throughout this year - rent spreads have actually reaccelerated in early 2023, perhaps credited to a moderation in cost pressures for tenants in other areas of the supply chain, specifically freight costs, which are now as much as 90% lower than their peak in September 2021. Rent growth on new and renewed leases rose 42% from last year - climbing to a fresh record-high for the sector - while occupancy rates also increased from last quarter to new highs, showing that demand continues to substantially outpace available supply.

{kind=link}

STAG Industrial ( STAG ) - which we own in the REIT Focused Income Portfolio - has been the upside standout, boosting its NOI growth outlook to 5.0% - up 25 basis points from last quarter - and raising its FFO growth outlook to 1.8% - up 45 basis points from last quarter. STAG recorded impressive cash leasing spreads of 25.3% in Q1 - and over 30% through April - a record-high for the company - and noted that it expects leasing spreads to average 30% for the year. STAG received an extra boost this week on word that the stock would be moving into the S&P MidCap 400 Index. EastGroup ( EGP ) also reported impressive results, raising its full-year FFO outlook by 210 basis points to 7.9% its same-store NOI outlook by 100 basis points to 7.0% at the midpoint. Industrial Logistics ( ILPT ) - an RMR-advised REIT that has plunged more than 80% over the past year - has rebounded a bit since reporting decent results, highlighted by strong leasing activity which generated rental rate spreads of 15.1%. ILPT commented that its "evaluating anything that can help with our deleveraging," but there are no active discussions with additional joint venture partners. Rexford ( REXR ) has also been a laggard over the past month despite reporting incredible 60% rental rate growth.

{kind=link}

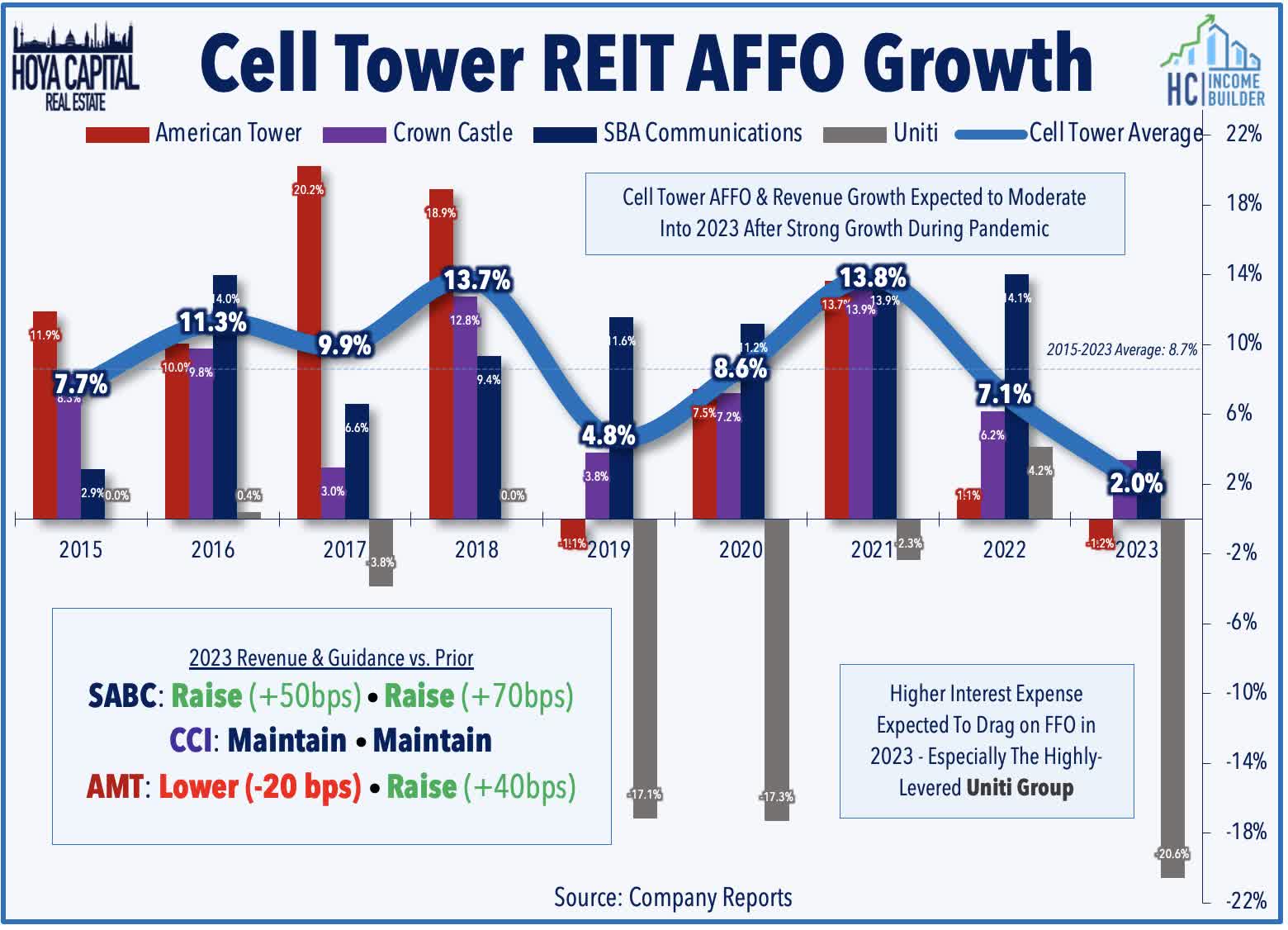

Cell Tower : (Halftime Grade: B+) We've seen results from all three major cell tower REITs. Results have been a bit better than expected, indicating continued strength in property-level fundamentals but offsetting headwinds from their relatively large variable rate debt exposures. Crown Castle ( CCI ) reported decent results but provided cautious commentary in which it noted that near-term impacts from higher interest rates will result in "minimal dividend growth in 2024 and 2025" after recently exceeding its target of 7-8% annual dividend growth in 2017. American Tower ( AMT ) boosted its full-year FFO outlook driven by an "acceleration in organic tenant billings growth." AMT lifted the midpoint of its FFO target by 40 basis points to -1.2% while revising lower its revenue target due to the sale of its Mexico Fiber portfolio last month for $252 million. AMT noted that its organic billings - the sector's comparable proxy for same-store NOI - rose 6.4% year-over-year, which was the strongest since 2017 and up from 4.7% in Q4 driven by "growth through colocations and amendments, as carriers continue to leverage our leading macro tower portfolio to aggressively roll out their networks to meet customer demand."

{kind=link}

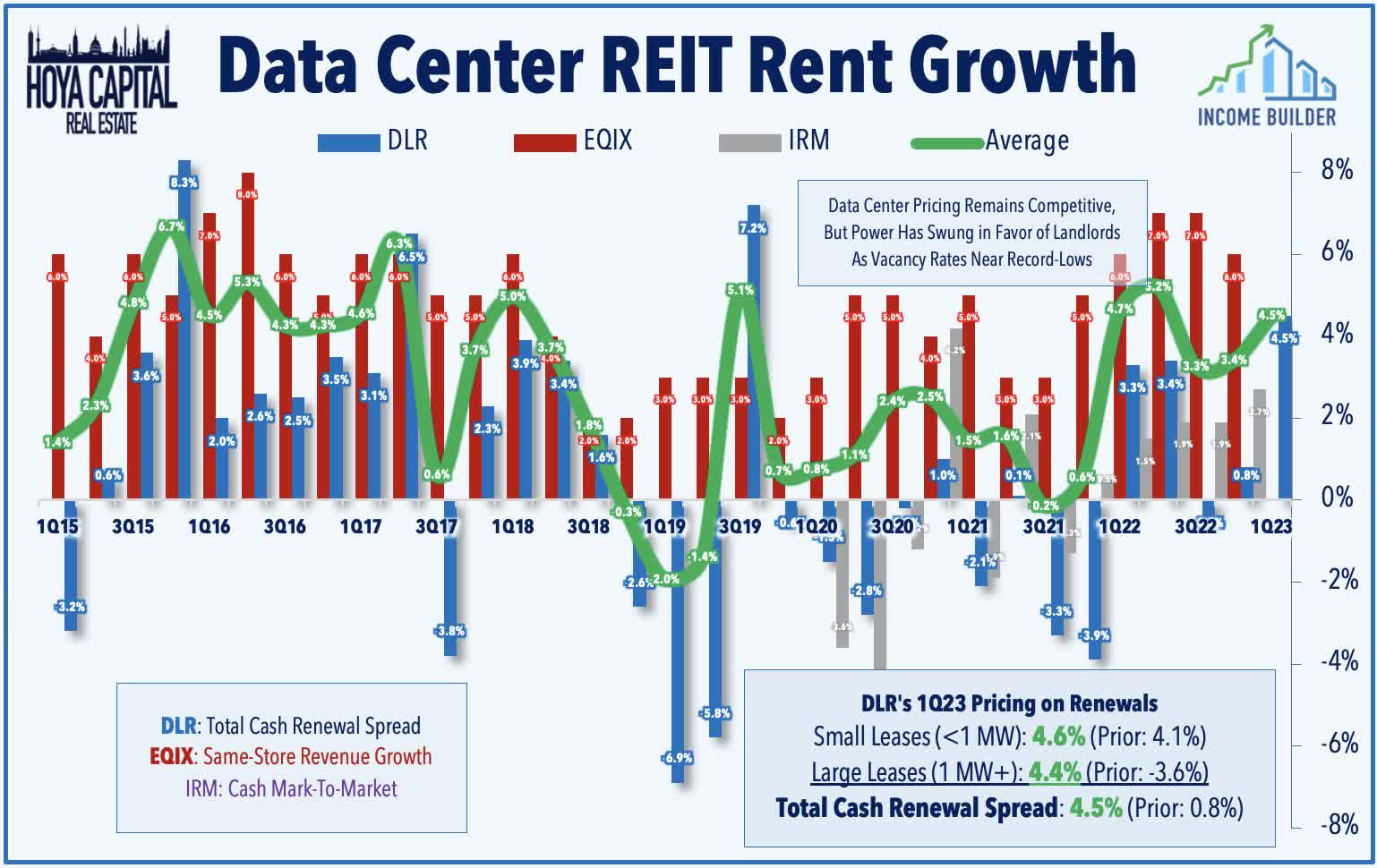

Data Center : (Halftime Grade: B) We've heard results from just one data center REIT - Digital Realty ( DLR ) - but have also had a full dose of cloud commentary from the big-tech "hyperscalers." DLR reported in-line results and maintained its full-year FFO outlook calling for flat growth in 2023. Positively, DLR reported strong pricing trends with renewal rent spreads rising 4.5% on a cash basis - the strongest quarter since 2019 - to which DLR commented, "we feel confident that this positive pricing environment is sustainable and here to stay." New leasing volume was light, however, with DLR signing $83M of incremental annualized GAAP rental revenues - the lowest since Q1 of 2020 - to which DLR commented, was "probably just a one-quarter timing issue." DLR reiterated its guidance calling for "same-capital" NOI growth of 3.4% for full-year 2023, which would be the first year of positive organic growth since 2017. Providing more color on these supply/demand conditions, DLR commented, "as inventory in various markets becomes more and more precious, we’ve seen that pricing pendulum move in our favor."

{kind=link}

Office & Healthcare Halftime Report

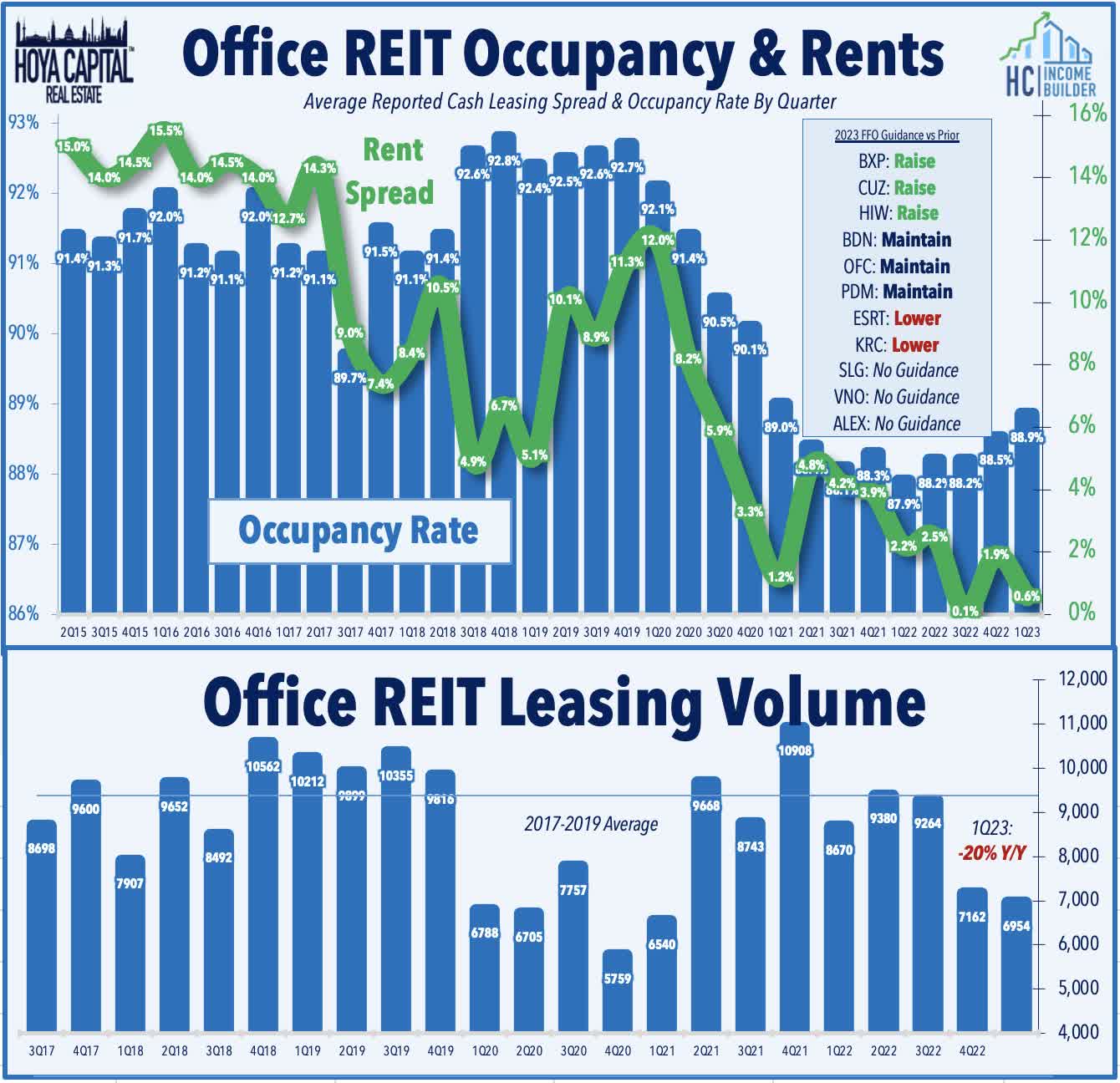

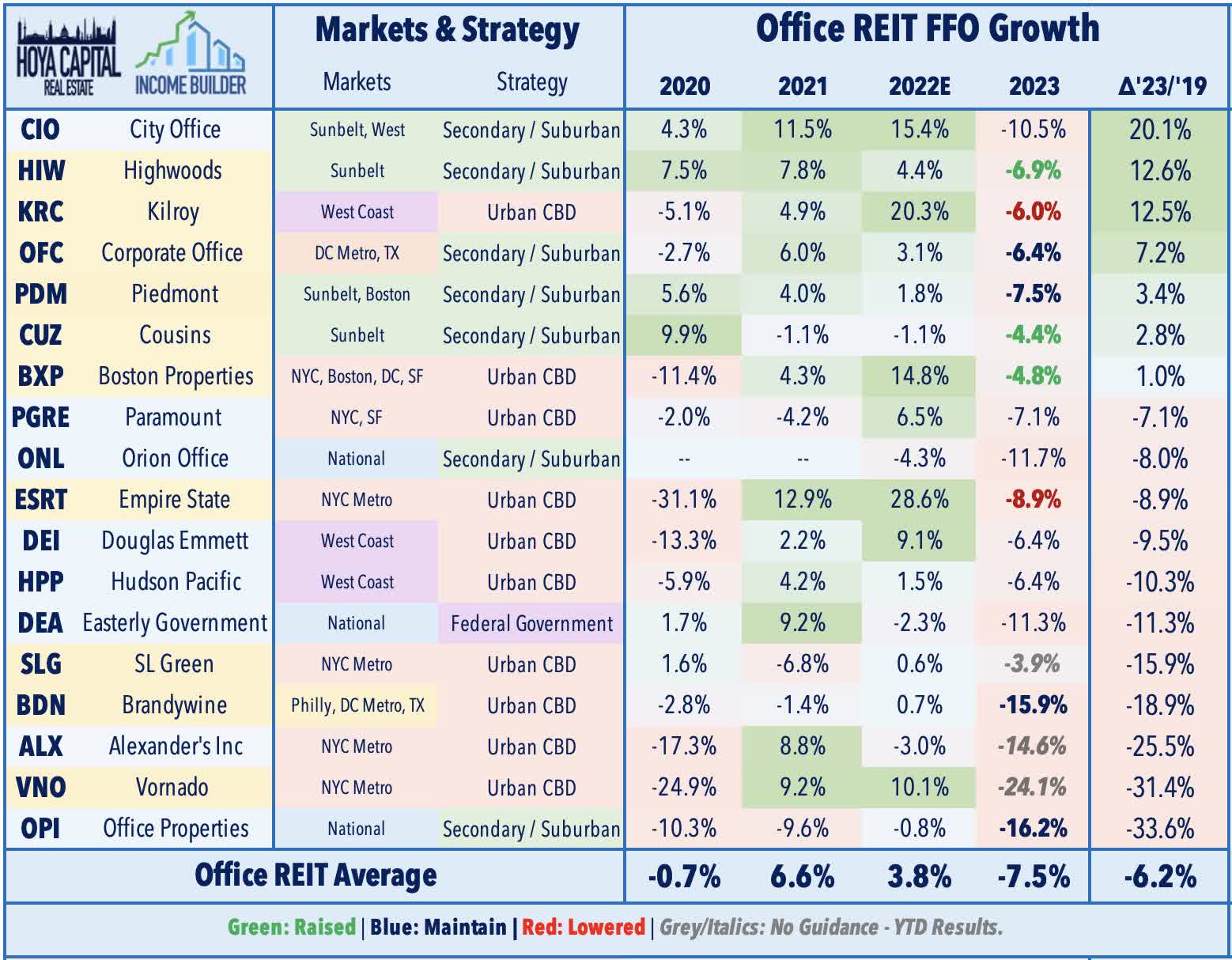

Office : (Halftime Grade: C) We've seen results from 11 of the 22 office REITs - reports that provided both reasons for optimism and for pessimism. Reports from coastal-focused REITs have done little to change the downbeat narrative. Vornado ( VNO ) has been in the spotlight after announcing that it will suspend its common stock dividends until the end of 2023. VNO noted that it would instead use the cash to reduce debt and/or fund its newly-launched $200M stock buyback program. Boston Properties ( BXP ) raised its full-year FFO outlook by 40 basis points to -4.8%, but leasing volume was very light at 660k SF, which was down 59% from Q1 of last year and the lowest in more than five years. NYC-focused Empire State Realty ( ESRT ) lowered its FFO outlook by about 2% to -8.9% on impacts from its lease to Signature Bank. West Coast-focused Kilroy ( KRC ) also lowered its FFO outlook and recorded a surprisingly weak cash rent decrease of 4.4% on new and renewed leases.

{kind=link}

Importantly, the magnitude of the weakness in Sunbelt markets remains far more muted than coastal urban markets, underscored by the guidance increases from the pair of leading Sunbelt office REITs - Cousins ( CUZ ) and Highwoods ( HIW ) - which reported leasing volumes that were only about 20% below pre-pandemic levels while occupancy rates. Results from Cousins were particularly solid, with a sequential increase in occupancy and sector-leading cash spreads of 6.1%. Highwoods reported GAAP rent growth of +15.9% and cash rent growth of +2.0% and maintained its full-year occupancy outlook at 90% at the midpoint. Corporate Office ( OFC ) has also been an upside performing after raising its same-store NOI guidance to 4% - up 100 basis points from last quarter.

{kind=link}

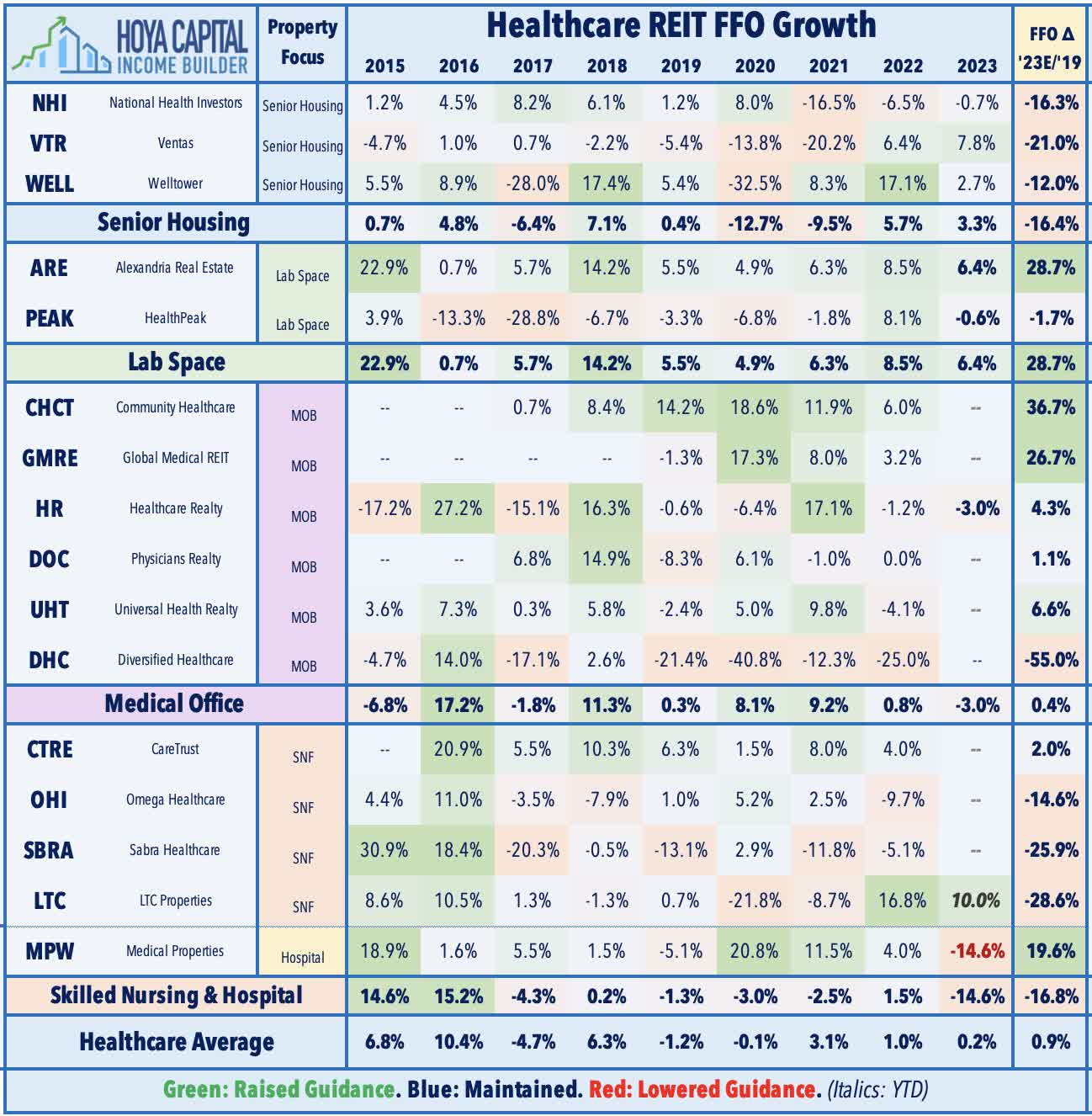

Healthcare : (Halftime Grade: C) Tenant operator struggles have remained the major focus of healthcare REIT reports as pandemic-related government support has waned in recent quarters. Embattled hospital owner Medical Properties ( MPW ) - which has been in the cross-hairs of short-sellers for the past year - has been an upside standout this earnings season after reporting better-than-feared results and maintaining its dividend. Under pressure from tenant rent collection issues, MPW lowered the midpoint of its FFO guidance, citing recent asset sales and debt reduction costs, and now expects a 14.6% decline in FFO for full-year 2023. "No news" was seen as "good news" regarding tenant issues, however, after the company reported earlier this year that Prospect Medical - its third-largest tenant at roughly 12% of revenues - had stopped paying rent.

{kind=link}

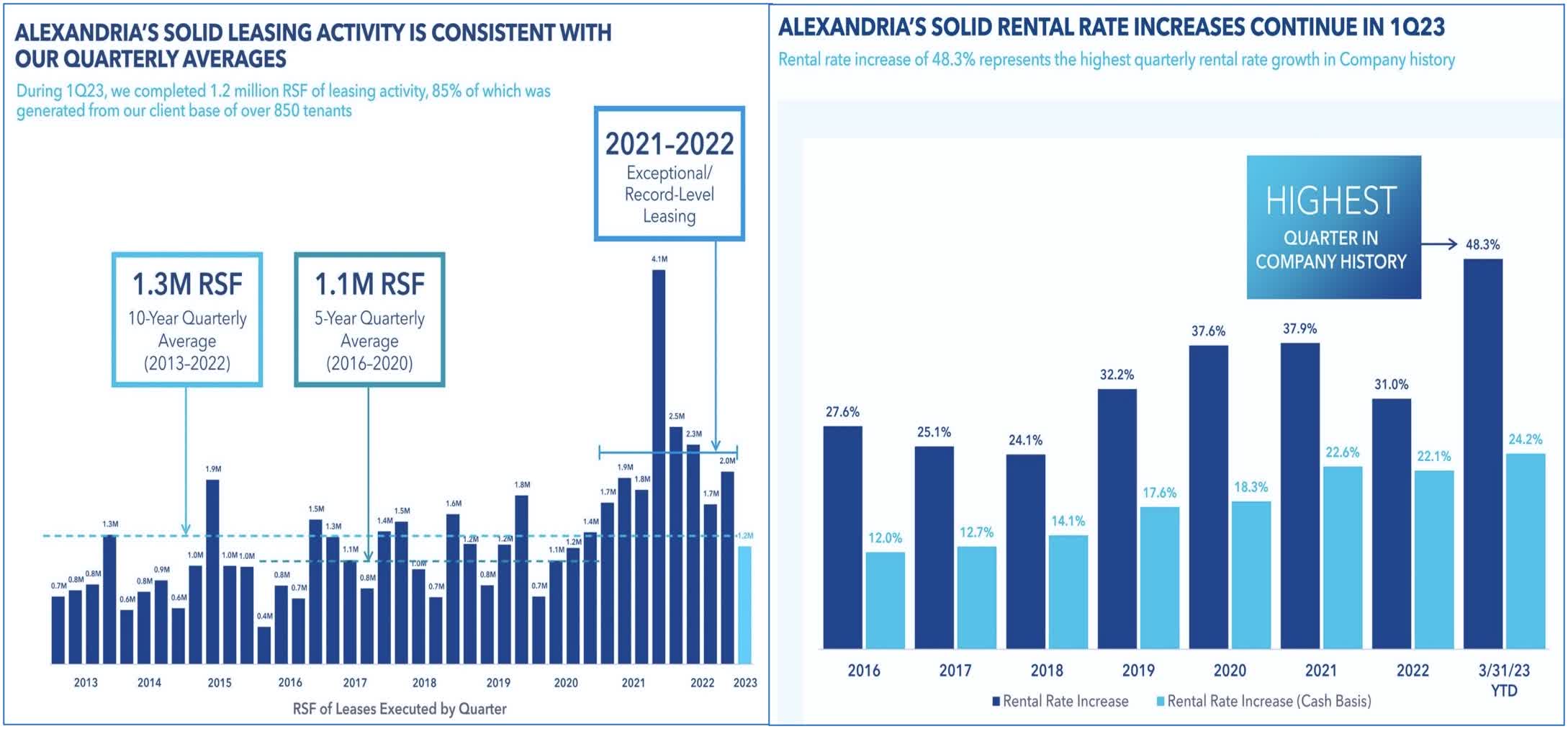

Lab space owner Alexandria Real Estate ( ARE ) reiterated its full-year FFO outlook calling for FFO growth of 6.4% while noting that it collected 99.9% of rents in Q1 and 99.7% thus far in April - pushing back on concerns over its tenants' exposure to Silicon Valley Bank - while achieving record-high rental rate increases of 48.3% GAAP/ 24.2% cash. ARE revised lower its full-year occupancy outlook from 95.3% to 95.1%, however, and recognized a $139M impairment on an office campus that it acquired in January 2020 - its only traditional office assets in the Boston market, noting that the "demand for [traditional] office space has deteriorated considerably" since its purchase. Healthpeak ( PEAK ) maintained its FFO outlook but raised its same-store NOI outlook to 3.75% at the midpoint - up 25 basis points from last quarter. First quarter life science leasing totaled 311k SF with an impressive 55% spreads on renewals. Its senior housing portfolio delivered the strongest NOI growth at 9.5% - a positive read-through for Welltower ( WELL ) and Ventas ( VTR ).

{kind=link}

Retail REIT Halftime Report

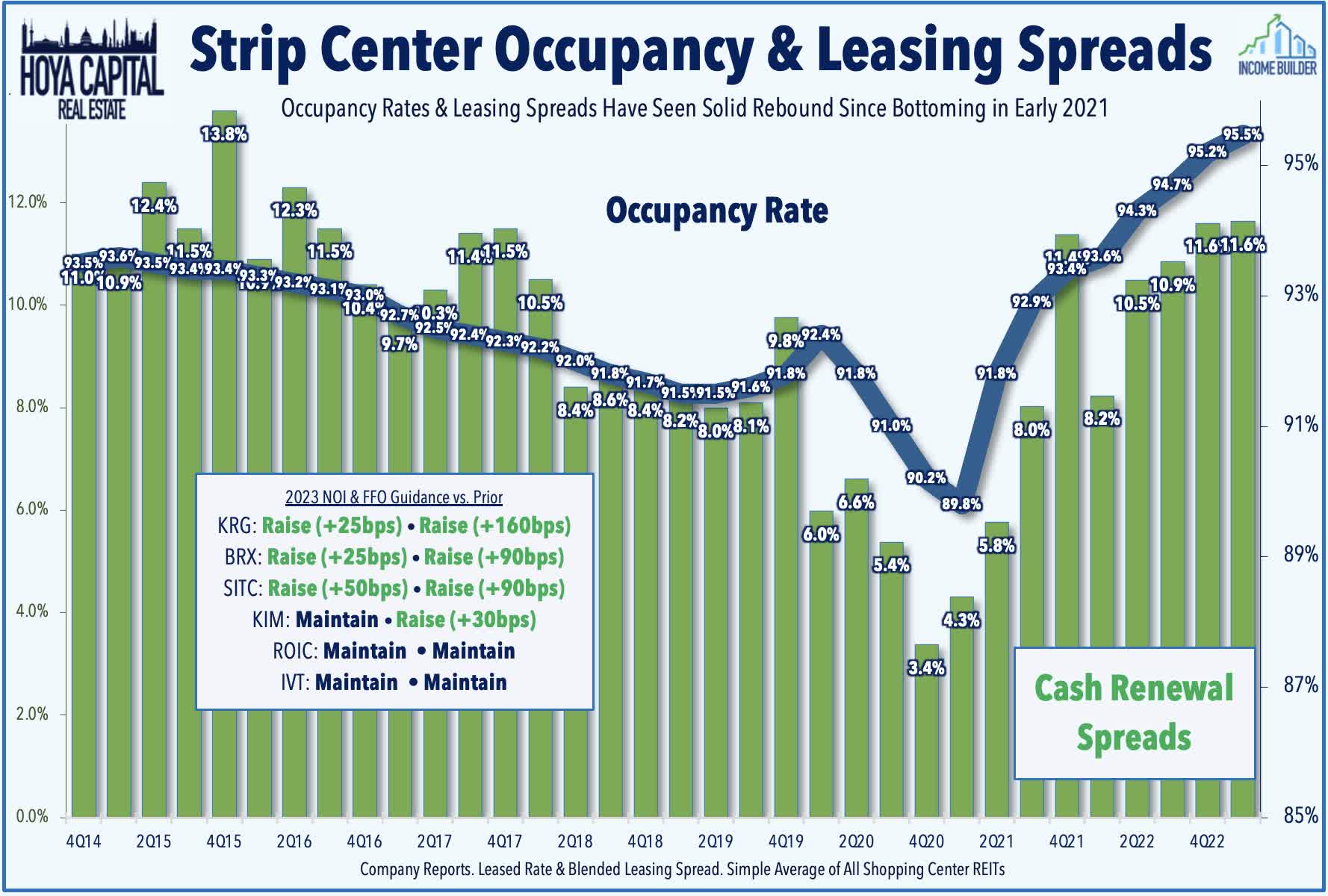

Strip Centers : (Halftime Grade: B+) Earnings season is still young for the retail sector, but results thus far have been quite solid - continuing a trend of better-than-expected results stretching back to late 2021 as demand for "big box" space has significantly exceeded the available supply. We've heard results from six of the 16 shopping center REITs - four of which have raised their full-year FFO outlook. Kite Realty ( KRG ) reported the strongest results thus far, raising both its full-year FFO and NOI growth outlook. Leasing activity was impressive with cash leasing spreads of 38.0% on 17 new leases, 10.0% on 77 renewals for a 13.0% blended increase. Brixmor ( BRX ) reported similarly strong "beat and raise" results, with rent spreads accelerating to 19.2% - its strongest in a half-decade. SITE Centers ( SITC ) also reported impressive cash leasing spreads of 20.3% on new leases and 8.7% on renewals while noting that its occupancy rate increased to 95.9% - up 50 basis points from last quarter and 270 bps from last year. Lifted by this strong leasing momentum, SITC raised its full-year NOI growth outlook by 50 basis points to 2.25% at the midpoint and its full-year FFO growth outlook by 90 basis points to 2.6%. Kimco ( KIM ) also raised its full-year FFO outlook while recording cash rent spreads of 44% on new leases in Q1 - its strongest in five years - which drove its blended rent spread to 10.3%, which was its best since early 2020.

{kind=link}

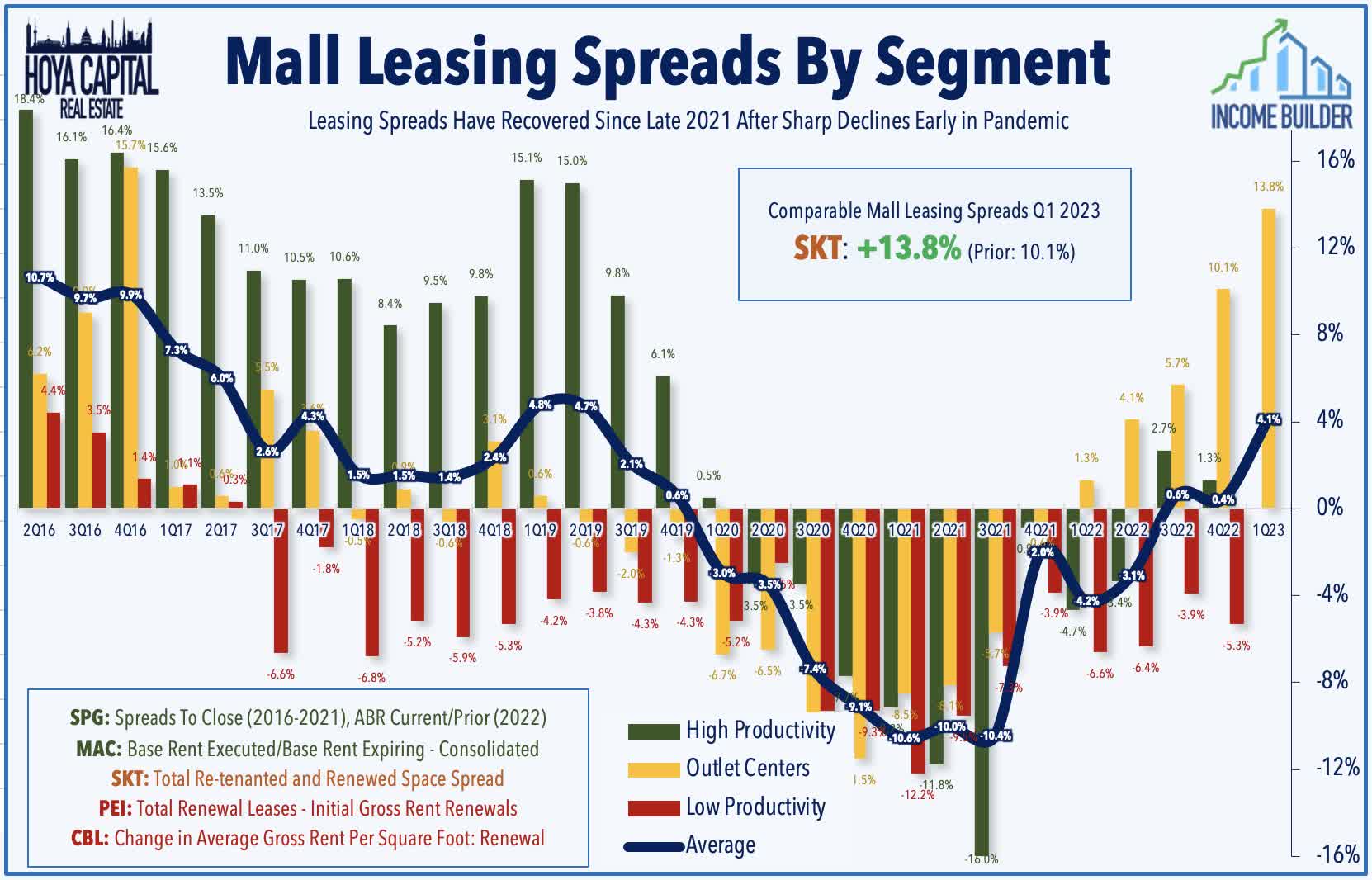

Mall : (Halftime Grade: B+) Tanger Factory Outlet ( SKT ) rallied after reporting strong leasing momentum and raising its full-year outlook. SKT now sees full-year FFO growth of 1.6% - up 110 basis points from last quarter - which would bring its FFO level to within 20% of its pre-pandemic level from full-year 2019. Encouragingly, SKT reported that blended rent spreads rose 13.8% on a trailing-twelve-month basis in Q1, which was the eighth-straight quarter of positive spreads following a period of eight-straight negative quarters, consistent with the recent buoyance in rental rates observed across the retail real estate space. Occupancy rates ticked down to 96.5% sequentially - consistent with seasonal patterns - but this was 220 basis points above Q1 of 2022 and was the strongest Q1 occupancy rate for the company since 2016. SKT commented, "we are seeing robust leasing activity with accelerating double-digit rent spreads as our retailers demonstrate their commitment to the outlet channel and Tanger's open-air portfolio."

{kind=link}

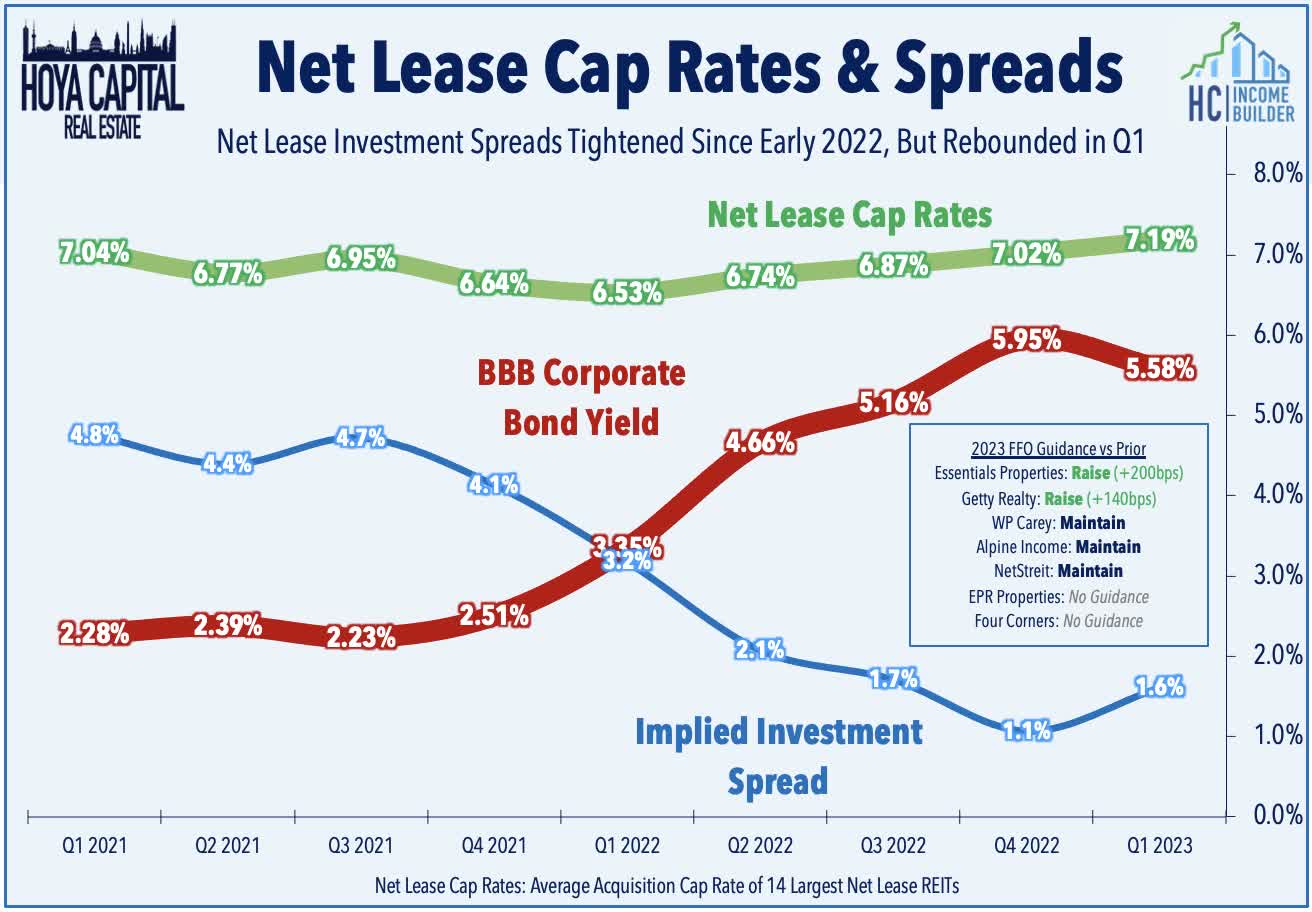

Net Lease : (Halftime Grade: B) We've heard results from 7 of the 16 net lease REITs, two of which have raised their full-year FFO outlook. EPR Properties ( EPR ) has been an outperformer after reporting that it collected 100% of rents and deferred payments through April from Regal despite the bankruptcy filing from its parent firm Cinemark. Essential Properties ( EPRT ) raised its full-year FFO growth outlook to 5.9% - up 200 basis points from last quarter. EPRT acquired roughly $200M in assets in Q1 at a 7.6% cap rate - up from recent lows in late 2021 of 6.9% - and sold $37M of assets at a 6.1% cap rate. Getty ( GTY ) boosted the midpoint of its FFO outlook to 4.2% - up 140 basis points from last quarter - driven by recent acquisition activity. NETSTREIT ( NTST ) and W.P. Carey ( WPC ) each maintained their full-year outlooks, which call for FFO growth of 3.4% and 1.1%, respectively. Among these seven REITs, we note that average cap rates have increased about 20 basis points sequentially - which combined with the retreat in interest rates - has resulted in a 50 basis point improvement in implied investment spreads.

{kind=link}

Hotel & Casino REIT Halftime Report

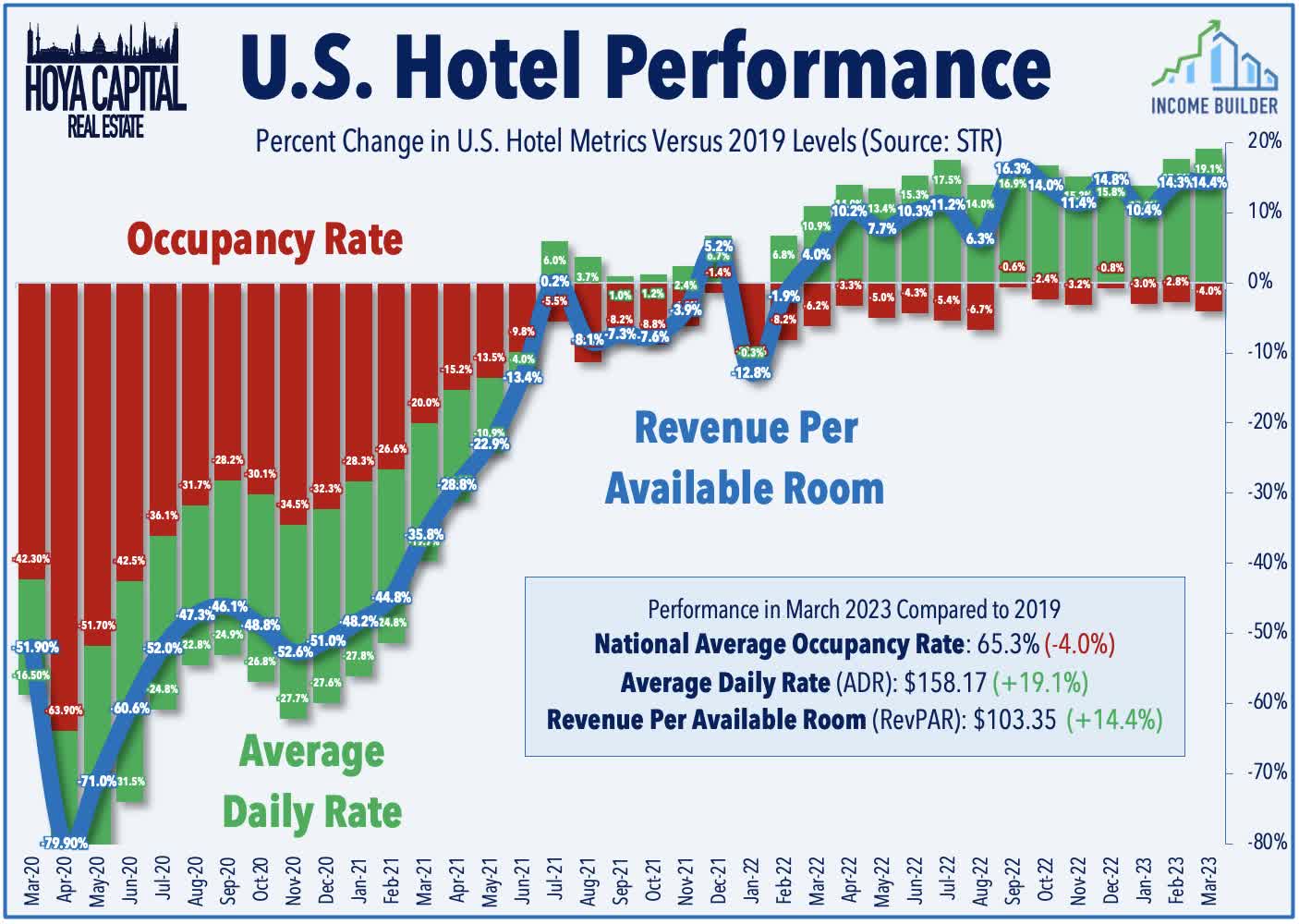

Hotels : (Halftime Grade: B+) We've heard results from just three of the 16 hotel REITs thus far. Park Hotels ( PK ) reported strong results and significantly raised its full-year FFO outlook, now projecting FFO growth of 26.0%, up from 16.6% last quarter. PK noted that its Revenue Per Available Room ("RevPAR") was 9.6% below 2019-levels as a 12.3 percentage point occupancy drag was partially offset by a 7.5% increase in Average Daily Rates ("ADR") compared to Q1 2019. Trends improved throughout the quarter and into early Q2, however, with PK noting that its preliminary April RevPAR was just 2.5% below 2019-levels. PK commented that "results were driven by ongoing improvements at our urban hotels and sustained strength in our resort markets, while an acceleration in group trends helped to drive healthy margin gains during the quarter." Pebblebrook ( PEB ) reported mixed results, noting that its Revenue Per Available Room ("RevPAR") was about 10% below 2019-levels as an 18 percentage point occupancy drag was partially offset by a 44% increase in Average Daily Rates ("ADR") compared to Q1 2019. Summit Hotel ( INN ) hiked its dividend by 50% to $0.06/share (3.9% dividend yield), becoming the 46th REIT to raise its dividend this year.

{kind=link}

Mortgage REITs Halftime Report

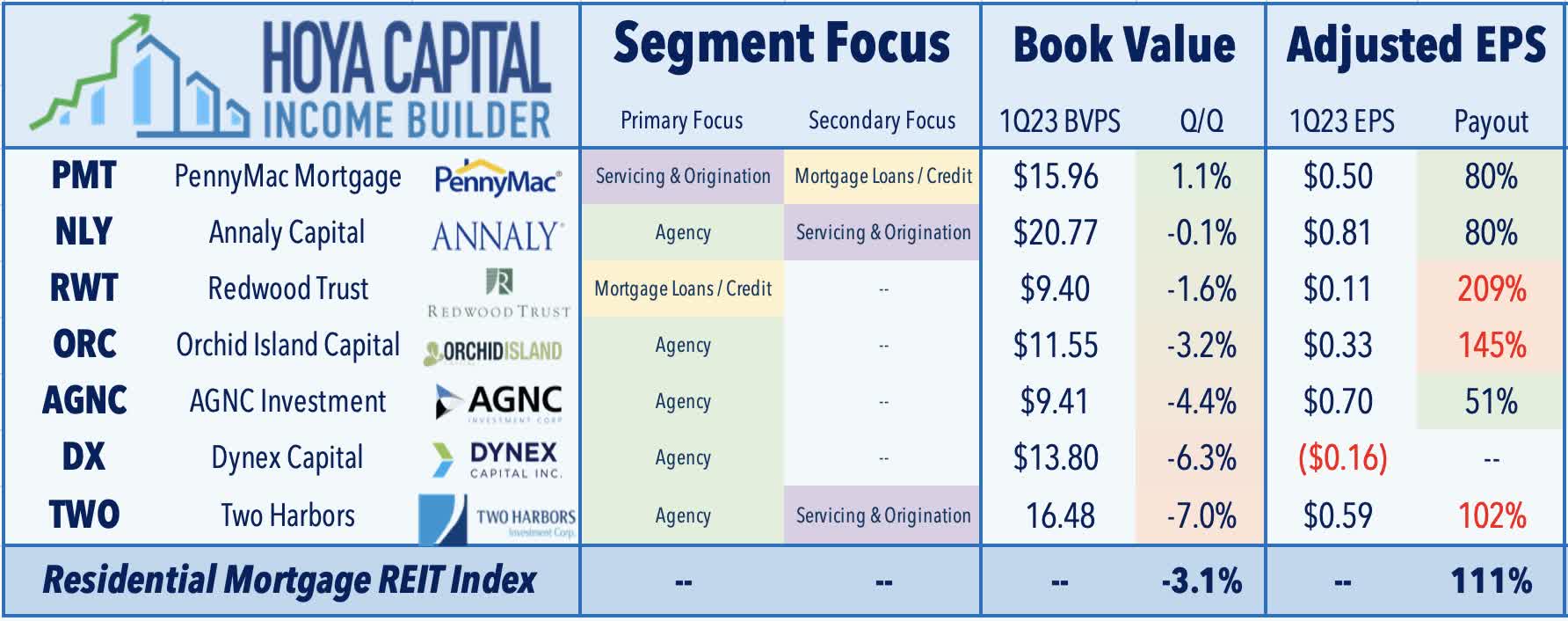

Residential mREITs : (Halftime Grade: B-) We've seen results from 7 of the 21 residential mREITs. As expected, results have been hit-and-miss given the volatile interest rate environment in Q1 combined with these REITs' typically high leverage and uncertain hedge exposure. PennyMac ( PMT ) is the leader in the clubhouse, reporting a 1% increase in its Book Value Per Share ("BVPS") driven by strong performance in its credit-sensitive strategies. Annaly Capital ( NLY ) has also been an upside standout, noting that its BVPS was flat in Q1, commenting that it "was prepared for market turmoil." Four mREITs reported EPS that failed to cover its Q1 dividend. Dynex Capital ( DX ) reiterated confidence in its dividend, but Redwood Trust ( RWT ) noted that it "expects to lower our quarterly dividends in the second quarter." Orchid Island ( ORC ) reported in-line results and commented, "We’re going to keep the dividend where it is, and we’ll see."

{kind=link}

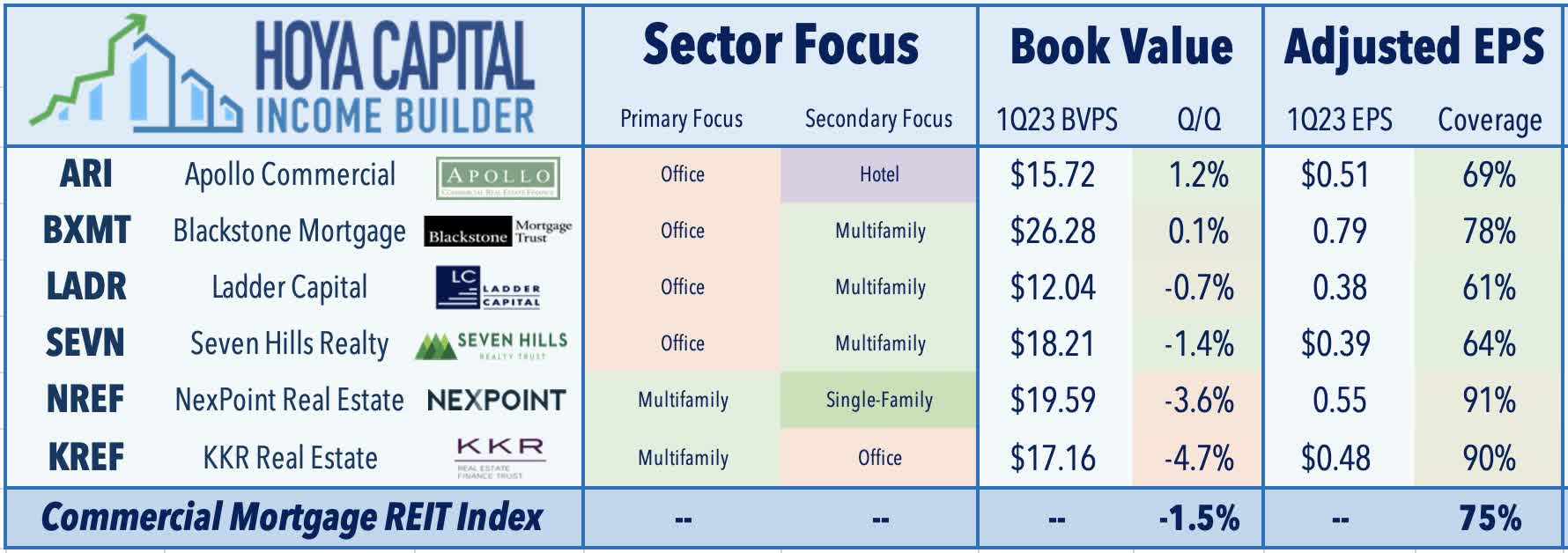

Commercial mREITs : (Halftime Grade: B+) We've seen results from 6 of the 20 commercial mREITs - including four of the mREITs with the highest exposure to office loans. Apollo Real Estate ( ARI ) rallied after reporting adjusted EPS of $0.51 - easily covering its $0.35/share dividend - while noting that BVPS increased 5% in Q1 to $15.72. NexPoint Real Estate ( NREF ) also rallied after reporting adjusted EPS of $0.55/share - covering its $0.50/share dividend. The prior day, NREF maintained its dividend at $0.50/share (15.8% dividend yield) while also declaring a special dividend. Blackstone Mortgage ( BXMT ) reported adjusted EPS of $0.79/share - covering its $0.62/share dividend - and noting that its book value per share ("BVPS") increased 0.1% to $26.28. BXMT noted that it collected 100% of interest payments in Q1 with no defaults despite its office-heavy loan portfolio. KKR Real Estate ( KREF ) has been under pressure, however, despite reporting adjusted EPS of $0.48/share - easily covering its $0.43/share dividend - but noted that its BVPS declined 4.7% to $17.16, resulting from an $0.88/share increase in its CECL allowance due to additional reserves for two office loans.

{kind=link}

Previewing The Second-Half of Earnings

Results at the halfway point of REIT earnings season have been better than the distinctly bearish prevailing narrative would suggest. Office and commercial mortgage REITs have been in focus given the stiff work-from-home headwinds and shaky dividend outlook. Apartment and Industrial REITs have accounted for nearly half of the guidance boosts thus far. Residential rent growth appears to have firmed in recent months after a rather sharp cooldown in late 2022 amid a broader Spring revival across the housing sector. While still early in earnings season for other sectors, retail REITs have reported impressive leasing momentum thus far. Healthcare REITs' operator issues have remained status-quo. More broadly, REITs appear content in remaining hunkered-down with muted appetite for aggressive external growth. We'll continue to provide real-time coverage and follow-up analysis articles for Hoya Capital Income Builder members throughout earnings season.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

REIT Earnings Halftime Report