PEAK - REIT Earnings Preview: Here's What We're Watching

2023-07-19 09:00:00 ET

Summary

- Real estate earnings season kicks into gear this week, and over the next month, we'll hear results from 175 equity REITs, 40 mortgage REITs, and dozens of housing industry companies.

- Real estate equities - the sector with perhaps the most to gain from a moderation in inflation and normalization in Fed monetary policy - enter earnings season with wind in their sails.

- Obscured by macro headwinds, REITs delivered a solid first quarter of earnings results fueled by buoyant rent growth. This report discusses the major high-level themes we'll be watching across second quarter results.

- Expenses and margins will be a key focus amid broader disinflationary impacts on revenues. A reversal from last quarter, upside guidance revisions to Net Operating Income ("NOI") are more likely to be driven by lower expense expectations.

- Access to capital is also a focus amid expectations that capitulation from debt-burdened private portfolios will create consolidation opportunities for well-capitalized REITs. Public REITs' access to equity capital could become a major competitive advantage if debt markets remain tight.

Real Estate Earnings Preview

{kind=link}

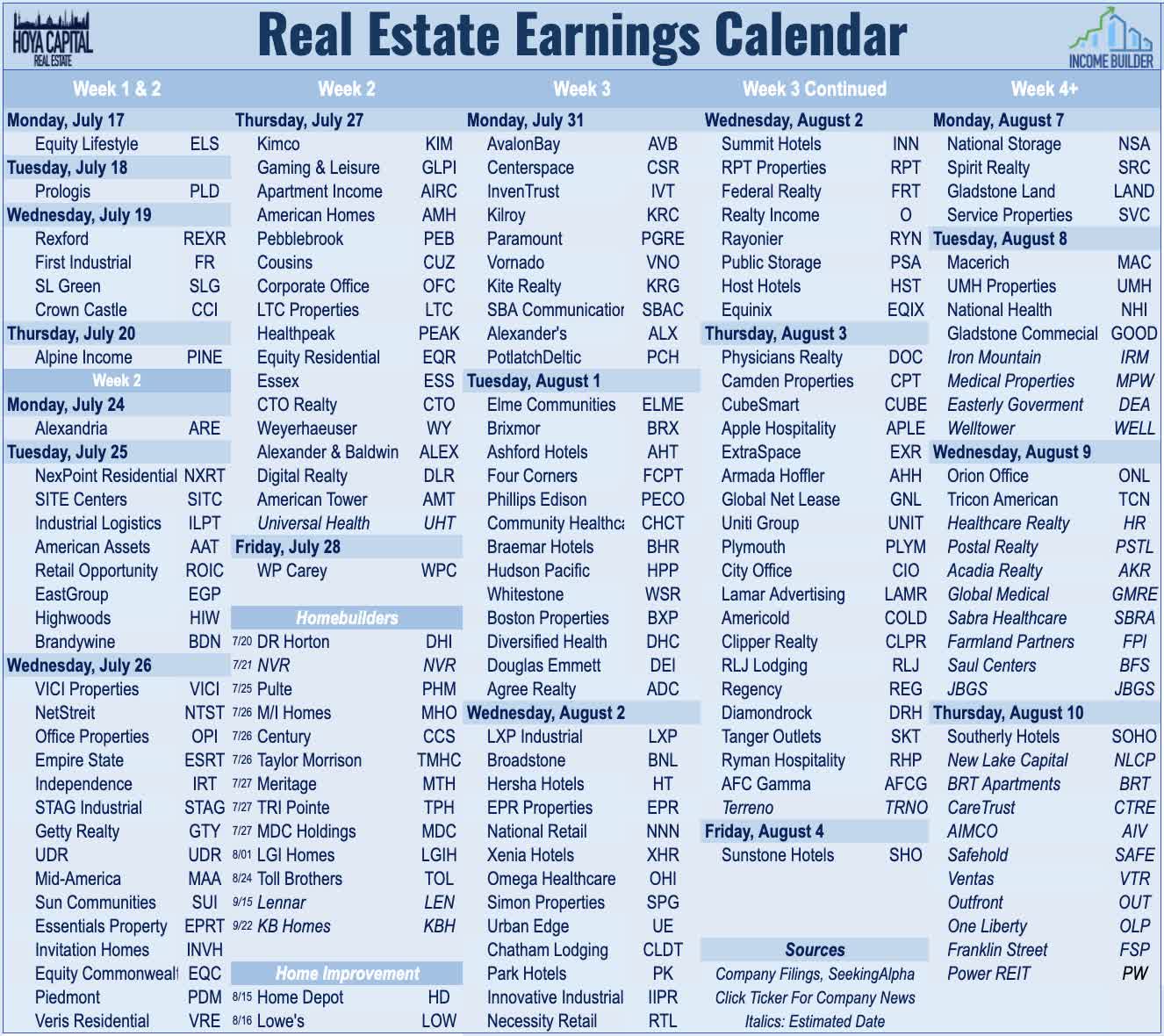

Real estate earnings season kicks off this week, and over the next month, we'll hear results from more than 175 equity REITs, 40 mortgage REITs, and dozens of housing industry companies which will provide key insights into how the real estate industry is adapting to the higher interest rate regime - and whether the outlook has shifted given the recent "soft landing" optimism fueled by several months of encouraging inflation data. This report discusses the major high-level themes and metrics we'll be watching across each of the real estate property sectors this earnings season. Below, we compiled the earnings calendar for equity REITs and homebuilders. (Note: Companies that have not yet confirmed an earnings date are in italics.)

{kind=link}

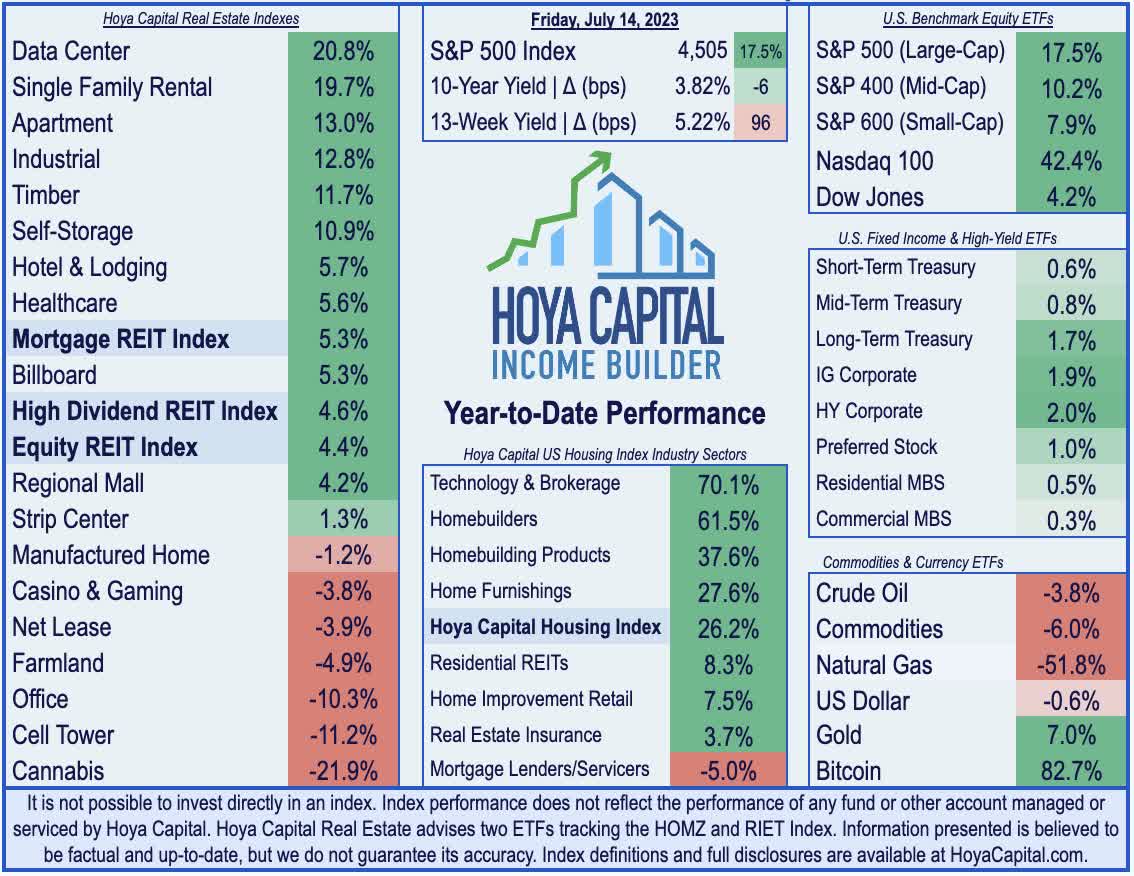

Real estate equities - the sector with perhaps the most to gain from a moderation in inflation and normalization in Fed monetary policy - enter earnings season with some wind in their sails after a rather dismal year-long stretch where any sense of forward headway seemed illusive. The Vanguard Real Estate ETF ( VNQ ) is higher by roughly 4% (6.5% total returns) on the year, having now almost pulled even with the Mid-Cap ( MDY ) and Small-Cap ( VIOO ) benchmarks. Within the real estate sector, 11-of-18 property sectors are in positive territory on the year, led by Data Center, Single-Family Rental, Apartment, Industrial, and Timber REITs, while Office and Cell Tower REITs have lagged on the downside. At 3.82%, the 10-Year Treasury Yield has declined by 6 basis points since the start of the year - up sharply from its 2023 intra-day lows of 3.26% - but still below its late-2022 closing highs of 4.30%.

{kind=link}

Before diving into the specific sector-by-sector metrics we're focused on this earnings season, we discuss the four higher-level themes that we're focused on this earnings season include:

- Full-Year Guidance & Expense Outlook

- Private-Market Valuations & Cap Rate Trends

- Acquisition & Consolidation Opportunities

- Dividend Policy & Commentary

1) Full-Year Guidance & Expense Outlook

Obscured by macro headwinds, REITs delivered a solid first-quarter earnings season fueled by buoyant rent growth - particularly across the residential, industrial, hospitality, technology, and retail sectors. Of the 83 equity REITs that provided full-year Funds from Operations ("FFO") guidance last quarter, 37 (44%) raised their full-year earnings outlook, while 5 (6%) lowered guidance - a FFO beat rate that exceeded the historical REIT average of 40% for the first quarter. We expect a slightly higher "beat rate" in the second quarter, but anticipate that the upside revisions to FFO and Net Operating Income ("NOI") are more likely to be driven by lowered property-level expense expectations amid broader disinflationary impacts. The more labor-intensive sectors - including hotels, residential, and senior housing - have the most potential upside from a moderation in inflationary expense pressures.

{kind=link}

Relevant for these REITs, producer price pressures have cooled even sharper than consumer inflation. The headline PPI rose just 0.2% year-over-year in June, its lowest reading since August 2020. While services-related inflation has appeared stickier - partially a function of the lagged measurement methodology - goods costs fell 4.4% from a year ago, the biggest decline in over three years. Excluding the volatile food and energy components, Core PPI also barely rose from May and was up 2.4% from a year ago, which was the smallest annual gain since January 2021. Forward-looking indices in the PPI report showed even more significant deflation coming through the supply chains. The PPI Index for Unprocessed Goods for Intermediate Demand is lower by 32.2% in June, the most significant deflationary one-year period on record for that index. Services-related inflation for intermediate demand, meanwhile, has increased by less than 1% in the six months of 2023.

{kind=link}

2) Private Market Valuations & Cap Rates

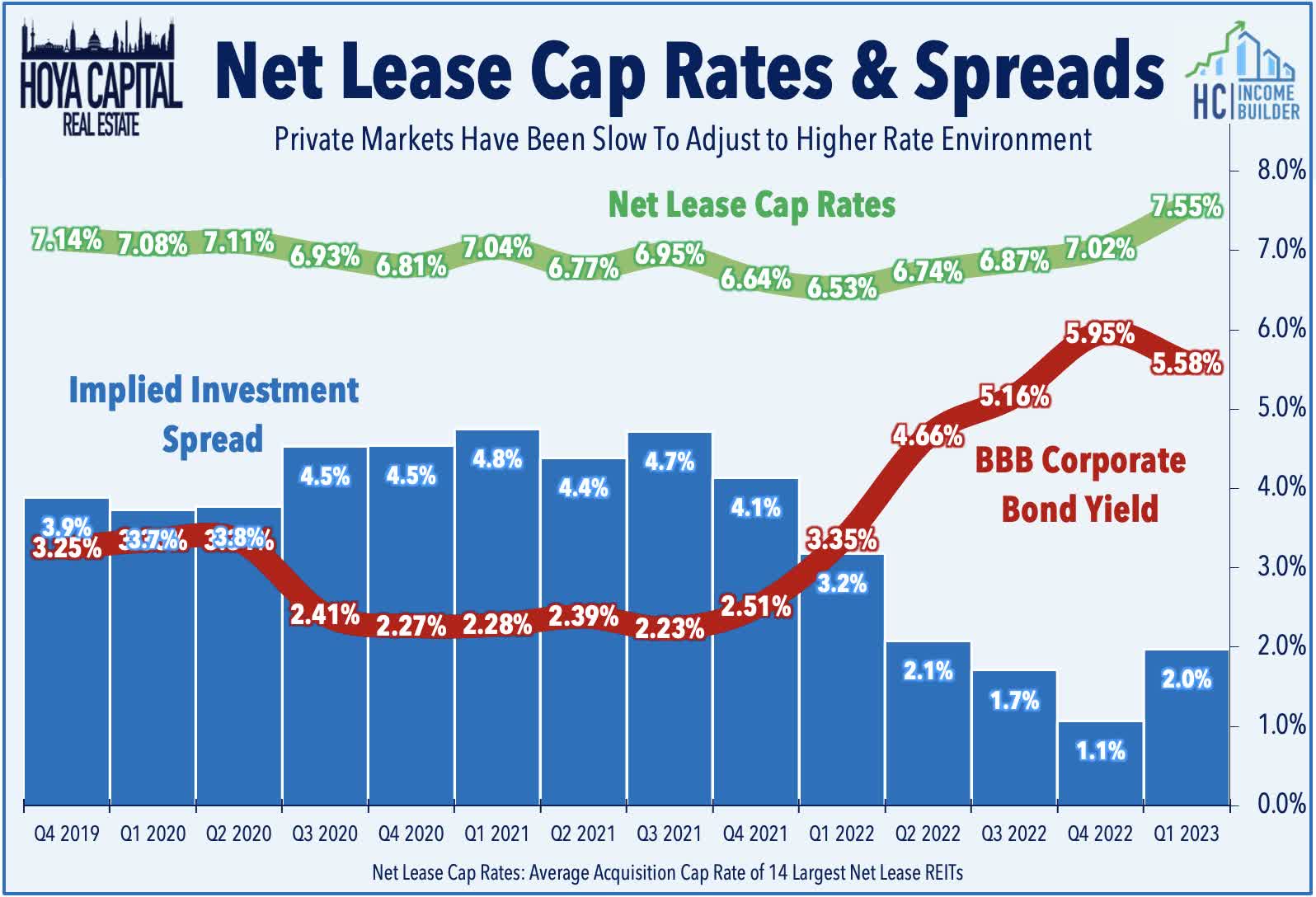

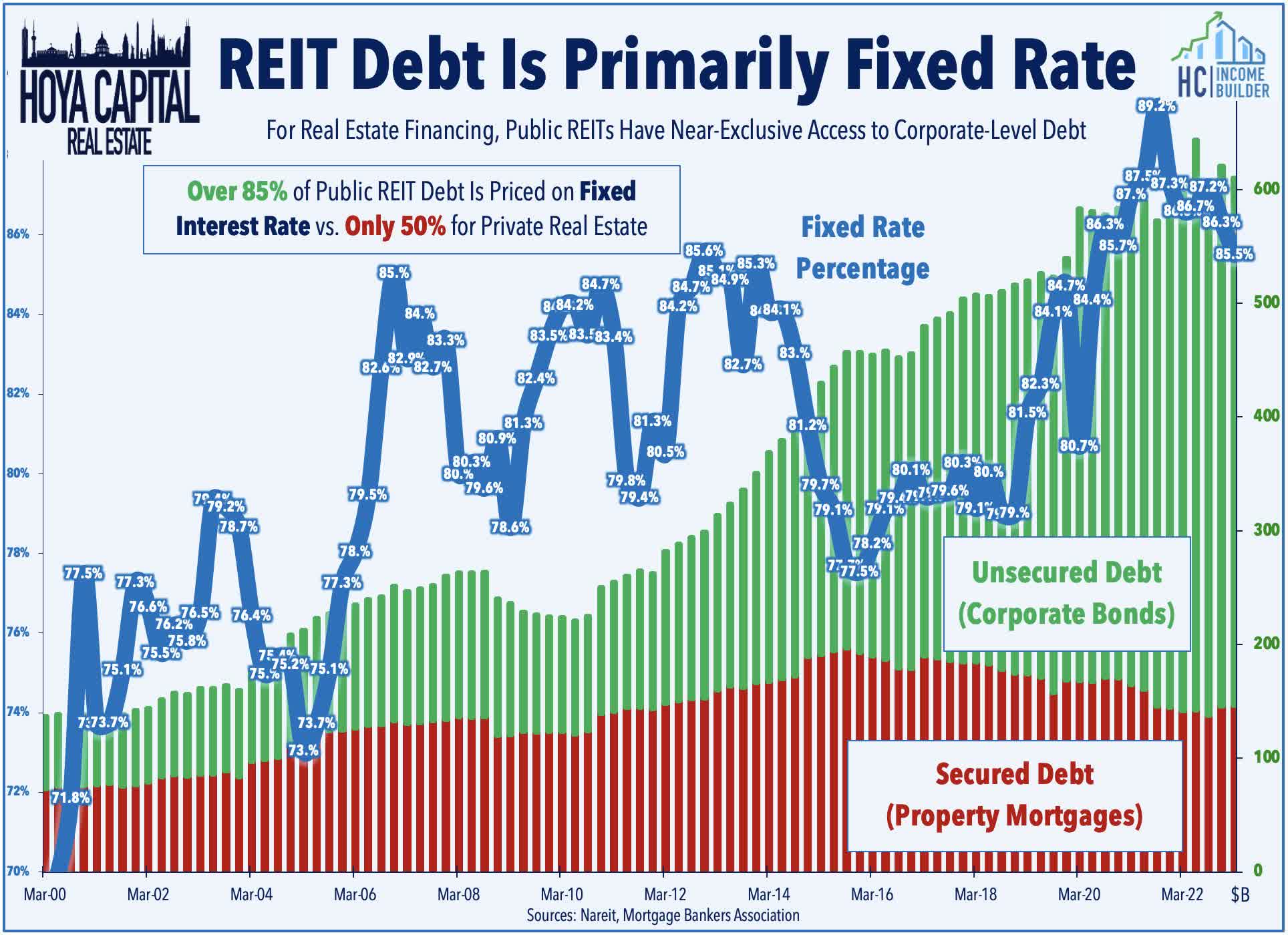

Private real estate markets remain slow to "catch up" to the reality of higher interest rates - conditions have been reflected in public real estate markets since early 2022. Transaction activity has been historically muted over the past year - a result of this ultra-wide bid-ask spread across commercial real estate markets - making it difficult to precisely track these trends, but the secular themes are captured by the trends observed via net lease REITs, which provide the most comprehensive disclosure of any property sector on cap rates. Acquisition cap rates for these REITs increased by about 100 basis points in Q1 over the prior year, during which time the benchmark interest rate increased by roughly 200 basis points, but this benchmark BBB Corporate Bond Yield was roughly unchanged during the second quarter.

{kind=link}

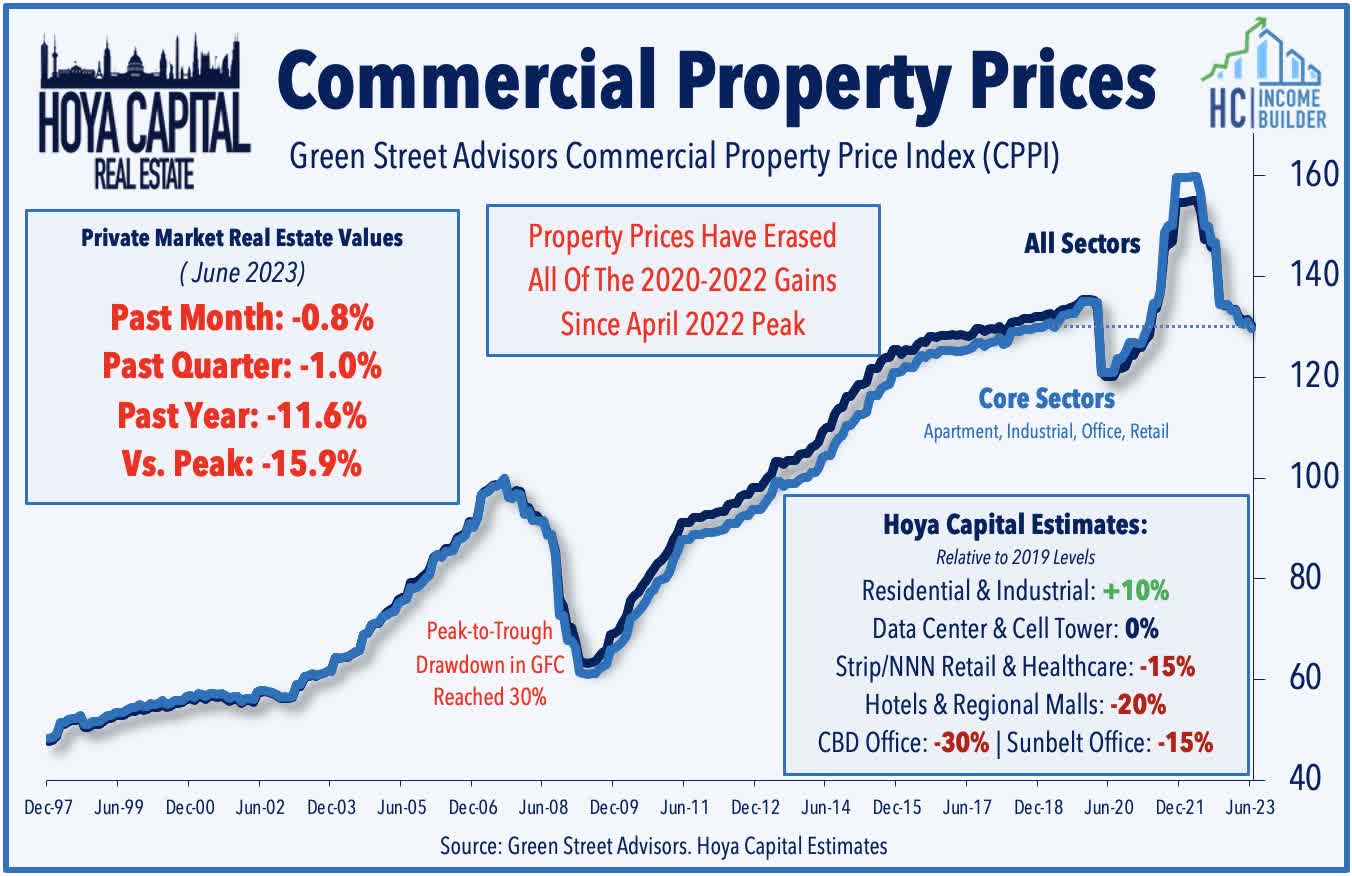

We'll be closely watching these cap rate metrics, expecting to see private market cap rates drift higher as previously low-rate debt maturities come due. Green Street Advisors' data shows that private-market values of commercial real estate properties have dipped over 15% over the past year and have now given back all of their pandemic-era gains, but the pace of the declines has started to flatten out over the past several months. Far more than the prior crisis, however, we've seen a greater divergence between property sectors over the past several quarters, with office valuations now about 30% below 2019-levels while residential and industrial property valuations have remained more buoyant. Importantly, the downward pressure on valuations has been driven almost entirely by the increase in benchmark interest rates, as REIT property-level NOI is about 10% above 2019-levels.

{kind=link}

3) Acquisition & Consolidation Opportunities

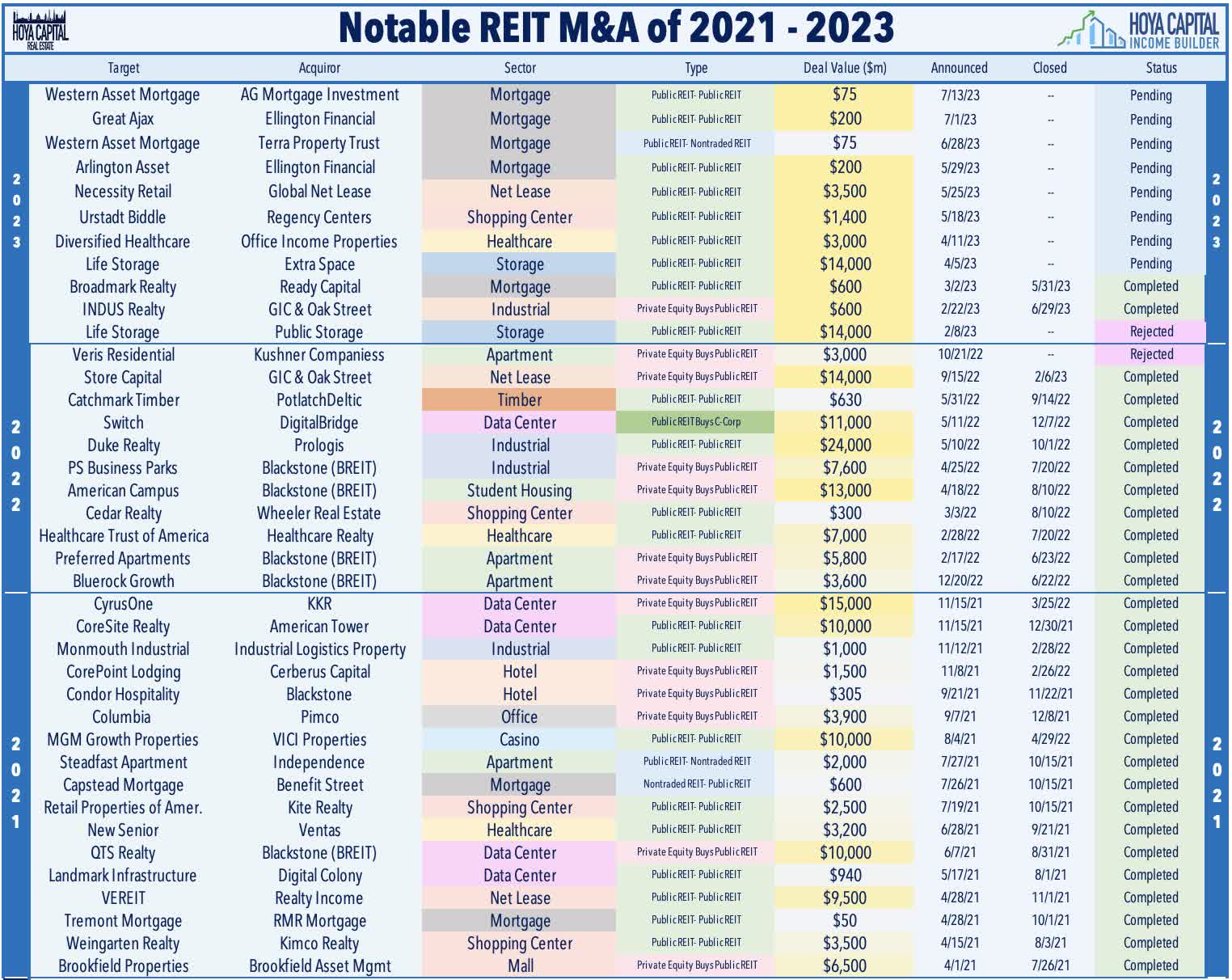

Access to capital is also a focus amid expectations that capitulation from debt-burdened private portfolios will create consolidation opportunities for well-capitalized REITs and public REITs' access to equity capital could become a major competitive advantage if debt markets remain tight. This commentary is particularly pertinent given the recent exodus from several major non-traded REIT ("NTR") platforms - including those offered by Blackstone ( BX ) - which offloaded a handful of major portfolio holdings to public REITs over the past two quarters and we expect to see more of these private-held assets return to public markets throughout the year. As noted in our State of the REIT Nation report, unlike their role during the GFC, many well-capitalized REITs are equipped to "play offense" and take advantage of acquisition opportunities from these private players - but whether or not these typically-defensive REITs are ready to take a more aggressive tact remains a key focus.

{kind=link}

Still-lofty valuations in the private markets have prompted these public REITs with the balance sheet firepower to look within the public markets for growth opportunities, fueling a notable surge in public REIT-to-REIT consolidations this year - and conditions are ripe for this type of activity to continue. Activity this year has been headlined by the merger between two of the four largest self-storage REITs Extra Space ( EXR ) and Life Storage ( LSI ), and by Regency Centers ( REG ) acquisition of fellow strip center REIT Urstadt Biddle ( UBP ). Markets have generally been receptive to these moves, and we expect several additional small and mid-cap REITs that trade at size-related discounts to be picked-up by larger peers. We've also observed a surge in mortgage REIT mergers in recent weeks as well - activity that has also been well-received given the steep Book Value discounts of these acquisition targets.

{kind=link}

4) Dividend Policy & Commentary

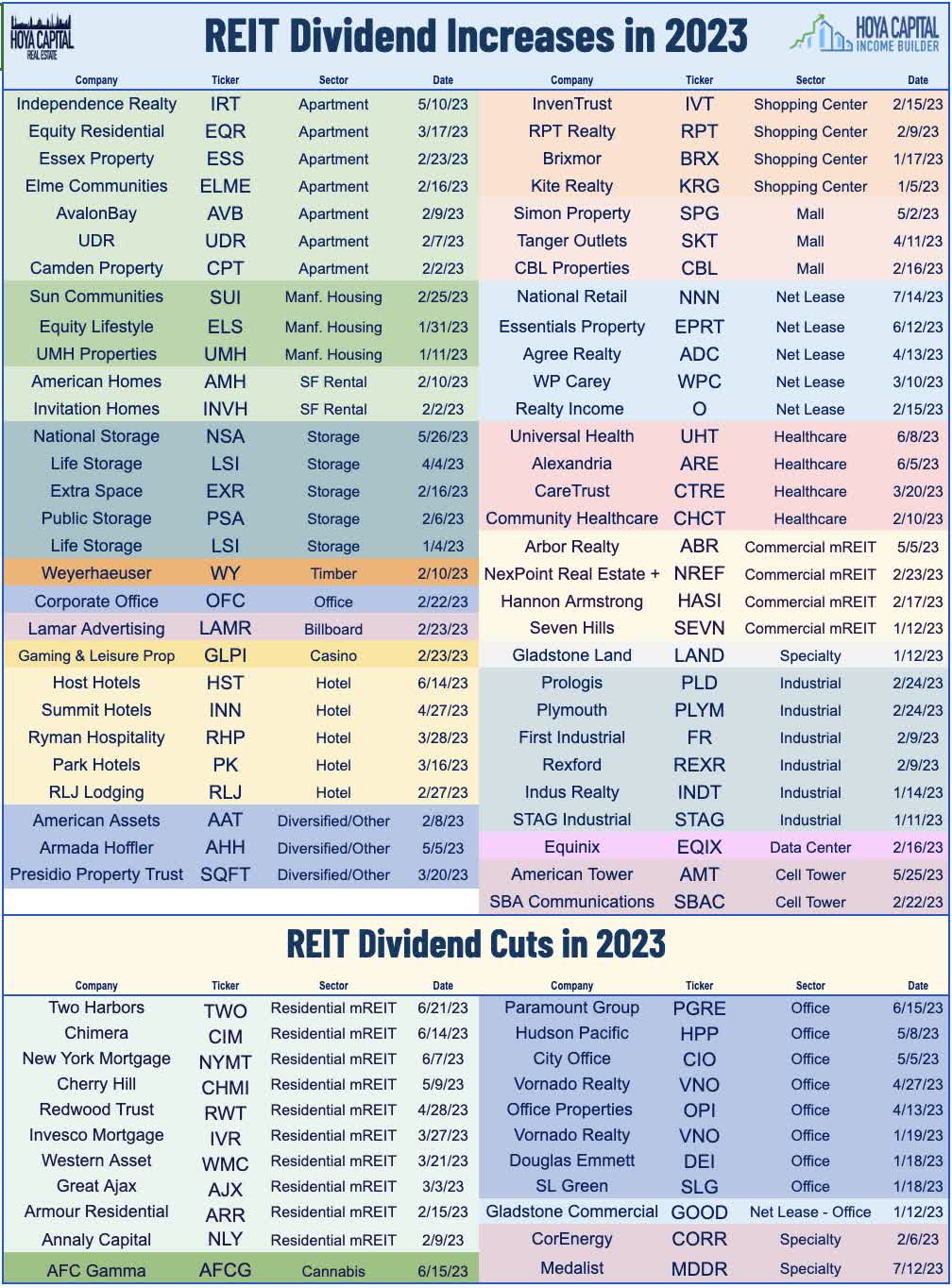

Despite more than 120 REIT dividend hikes in both 2021 and 2022 - and another 59 dividend hikes so far in 2023 - total REIT dividend payouts remain roughly 5% below pre-pandemic levels, as many REITs have been conservative in their dividend distribution policy. While sector-level dividend coverage ratios remain quite healthy with an average payout ratio of around 70% - slightly below the long-term historical average - dividend commentary will be a major focus for office and mortgage REITs - the sectors that have been responsible for essentially all of the 20 dividend reductions so far this year across the REIT sector. We believe that the "bleeding" in these sectors from a dividend cut perspective is largely contained at this point, and anticipate that dividend increases will outpace dividend cuts in the back half of 2023 driven primarily by the hotel and retail sectors - segments that have been especially conservative in recent quarters amid lingering recession worries.

{kind=link}

Residential Real Estate Earnings Preview

Apartments : The state of the U.S. housing market will be a critical focus throughout earnings season - the industry that felt the most direct effects from the historically swift monetary tightening cycle that began in mid-2022. Consensus sentiment around apartment REITs has improved in recent months as recent industry data has shown a stabilization in rental rate and occupancy trends since bottoming in January, with rent growth appearing to stabilize in its typical "inflation-plus" range between 4-5%. Supply concerns have been the unabating refrain from 'bears' over the past decade of outperformance. While the multifamily pipeline is historically large, overall housing development remains below equilibrium levels, and tighter financing conditions have curbed groundbreakings. We'll be closely-watching rent growth metrics on new and renewed leases and anticipate upside NOI revisions will be driven by an improved expense outlook, driven in the near-term by lower utilities expense.

{kind=link}

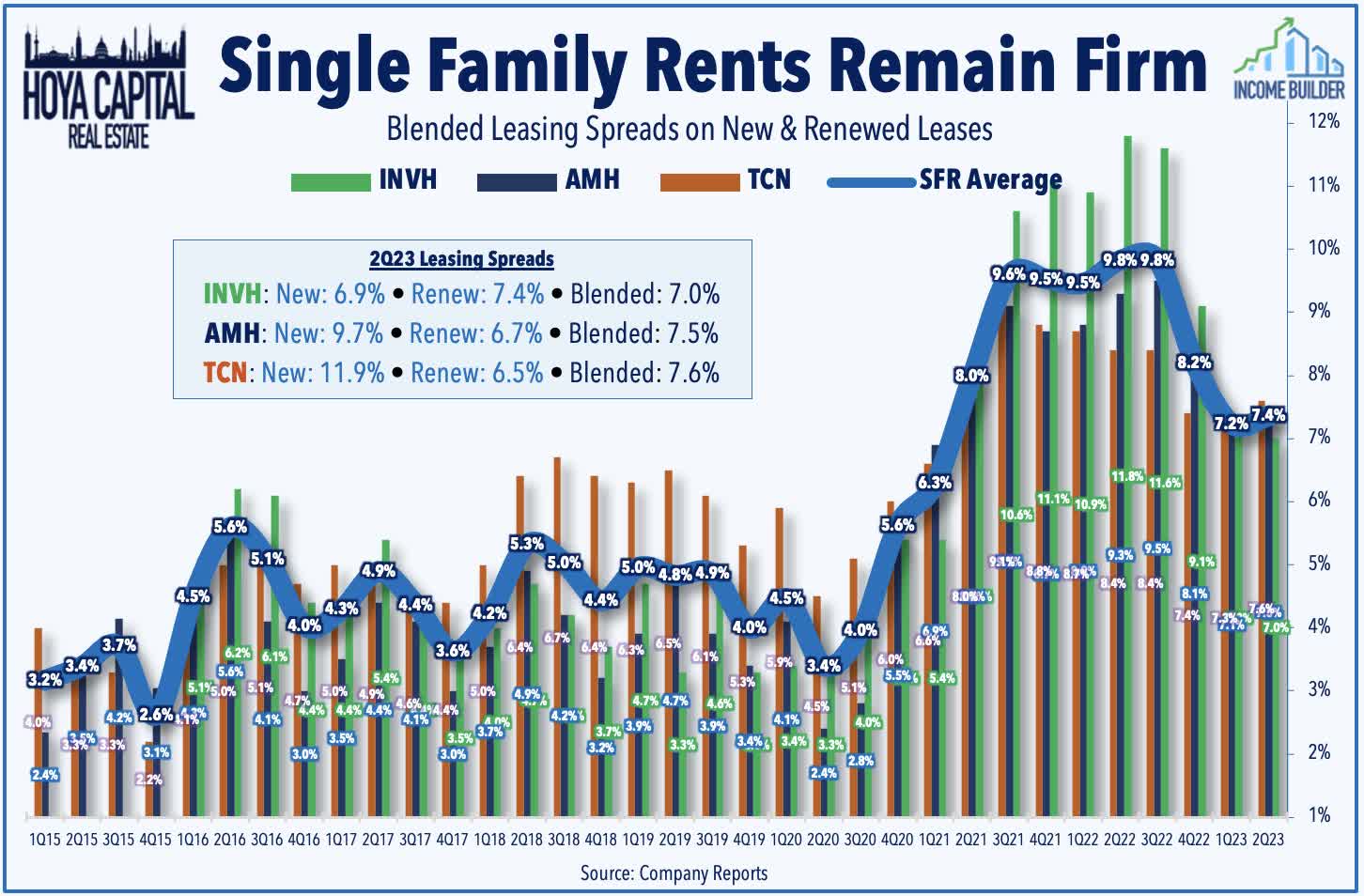

Single-Family Rentals : Buoyant rent growth has been particularly apparent across the single-family rental sector, which is not facing the same supply headwinds as the multifamily side. We're expecting a strong quarter for property-level fundamentals, aided by a cooling of expense headwinds. Negative home price appreciation and tighter credit conditions quickly neutralized the pockets of speculative housing market activity - including the "fix-and-flips" and highly-levered short-term rental ("STR") startups that were beginning to fizzle in 2021 and 2022, an environment that made it difficult for SFR REITs - or any large-scale institution - to accretively add to their portfolios. As a result, the institutional SFR industry has been especially quiet in recent quarters following a frenzy of activity in prior years. In addition to rent growth metrics, we're interested in commentary about these external growth prospects - specifically, whether these REITs are beginning to see any pockets of private-market distress that could be ripe for the picking.

{kind=link}

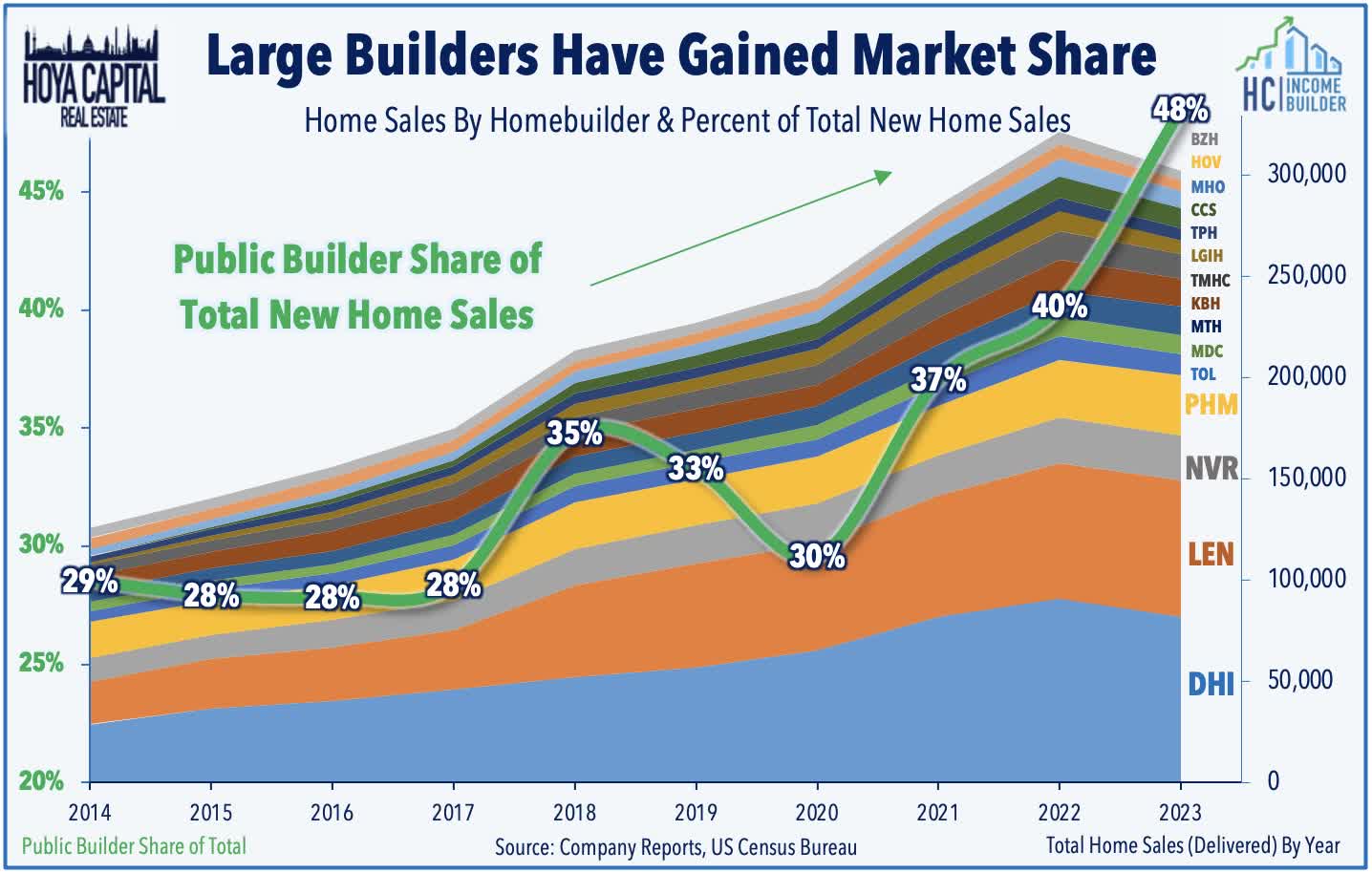

Homebuilders : To the surprise of countless pundits, the U.S. housing industry has quietly started to emerge from its year-long recession, thawing from a deep freeze induced by historically aggressive monetary tightening. Rebounding from punishing declines of nearly 30% last year that sent valuations to housing-crisis-era lows, homebuilders have surged 50% through the first half of 2023 as "crash" concerns proved misguided. Higher mortgage rates have delayed - but not permanently altered- the existing secular fundamentals supporting the single-family market: a "lost decade" of single-family construction ahead of a wave of demographic-driven demand. The sharp slowdown in housing activity and home prices was necessary to avoid a painful correction, but don't expect a return to the "boom times" either. With builders no longer trading the incredible discounts seen last year, further upside will require operational execution. We're focused on net orders - expecting a modest positive inflection this quarter after roughly six quarters of year-over-year declines - along with cancellation rates, and gross margins.

{kind=link}

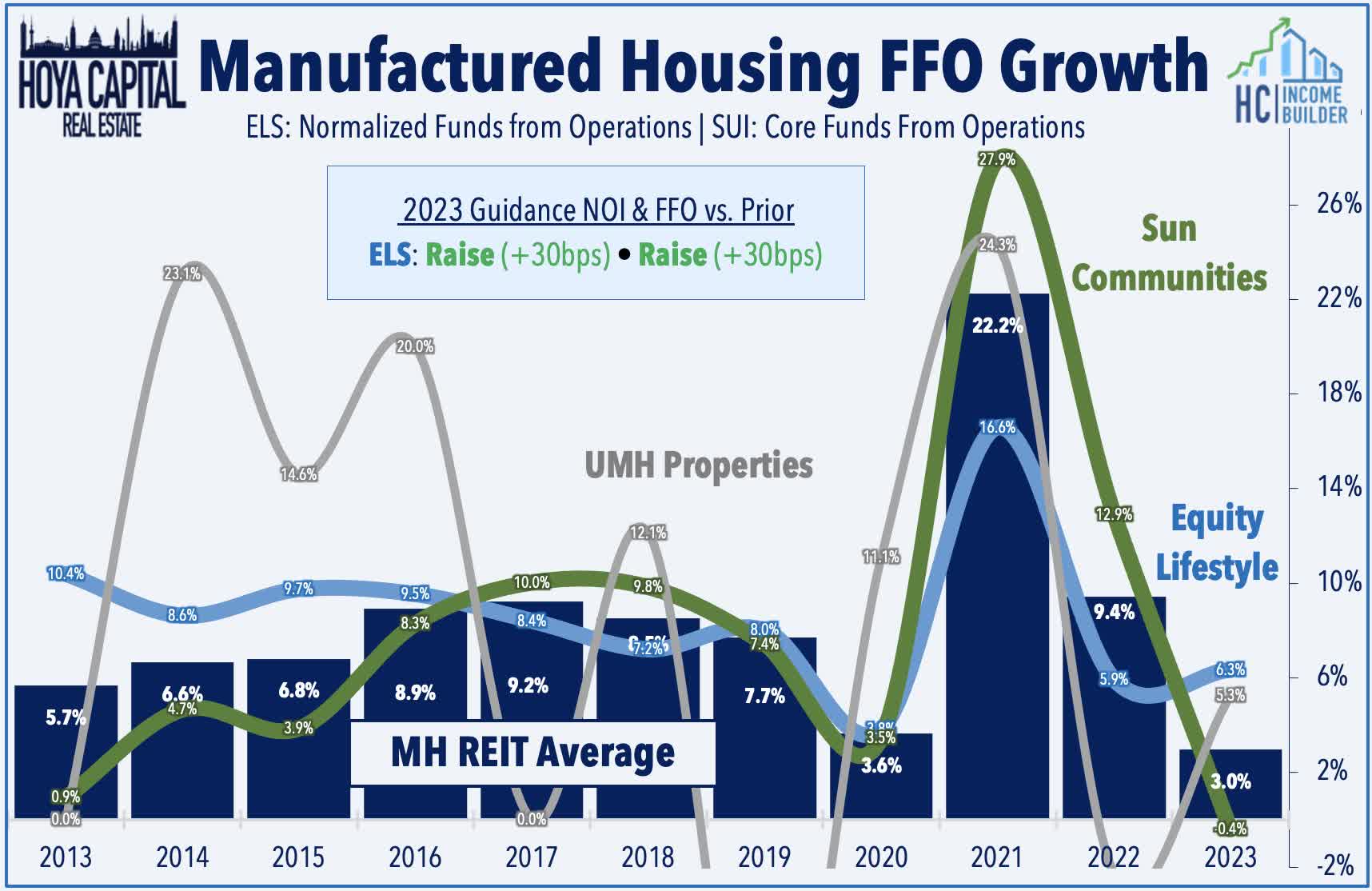

Manufactured Housing : Equity LifeStyle ( ELS ) kicked-off earnings season on Monday with solid results in which it raised its full-year FFO and NOI guidance, "driven by continued strength in annual revenue and reduced expenses throughout our portfolio." ELS increased its full-year 2023 FFO growth outlook to 6.3% - up from 6.0% last quarter - which would be an acceleration from the 5.9% growth reported in full-year 2022. ELS also raised its full-year NOI guidance driven by lower expense projections driven primarily by lower utilities rates. ELS maintained its outlook for full-year revenue growth in its core manufactured housing with a midpoint at 6.8%, but revised lower its revenue outlook in its RV & marina segment by about a percentage point to 4.6% on continued softness in its transient RV segment - an area that has been impacted by a post-COVID normalization and by "unfavorable weather patterns" including delayed openings at several of its Northern resorts.

{kind=link}

Self-Storage : Delivering the strongest earnings growth of any property sector during the pandemic, Storage REITs are among the best-performing sectors this year after lagging in late 2022, lifted by the thawing of the previously icy-cold housing market. Storage demand is driven largely by housing activity – specifically, home sales and rental market turnover - each of which have bounced from their early 2023 lows just in time for peak leasing season. REITweek updates last month showed a rebound in demand through May following a notable slowdown in late 2022 and into early 2023. PSA reported that its comparable occupancy increased 30 basis points since the of Q1 while its average rent per square foot rose 7.8% from a year earlier at the end of May. EXR reported that its comparable occupancy increased 80 basis points since the end of Q1 while CUBE posted occupancy gains of 110 basis points and NSA posted a 20 basis point increase. In REITweek commentary, PSA noted that the rebound goes beyond typical seasonality, citing a recent moderation in new supply growth and development activity.

{kind=link}

Tech and Industrial REITs Earnings Preview

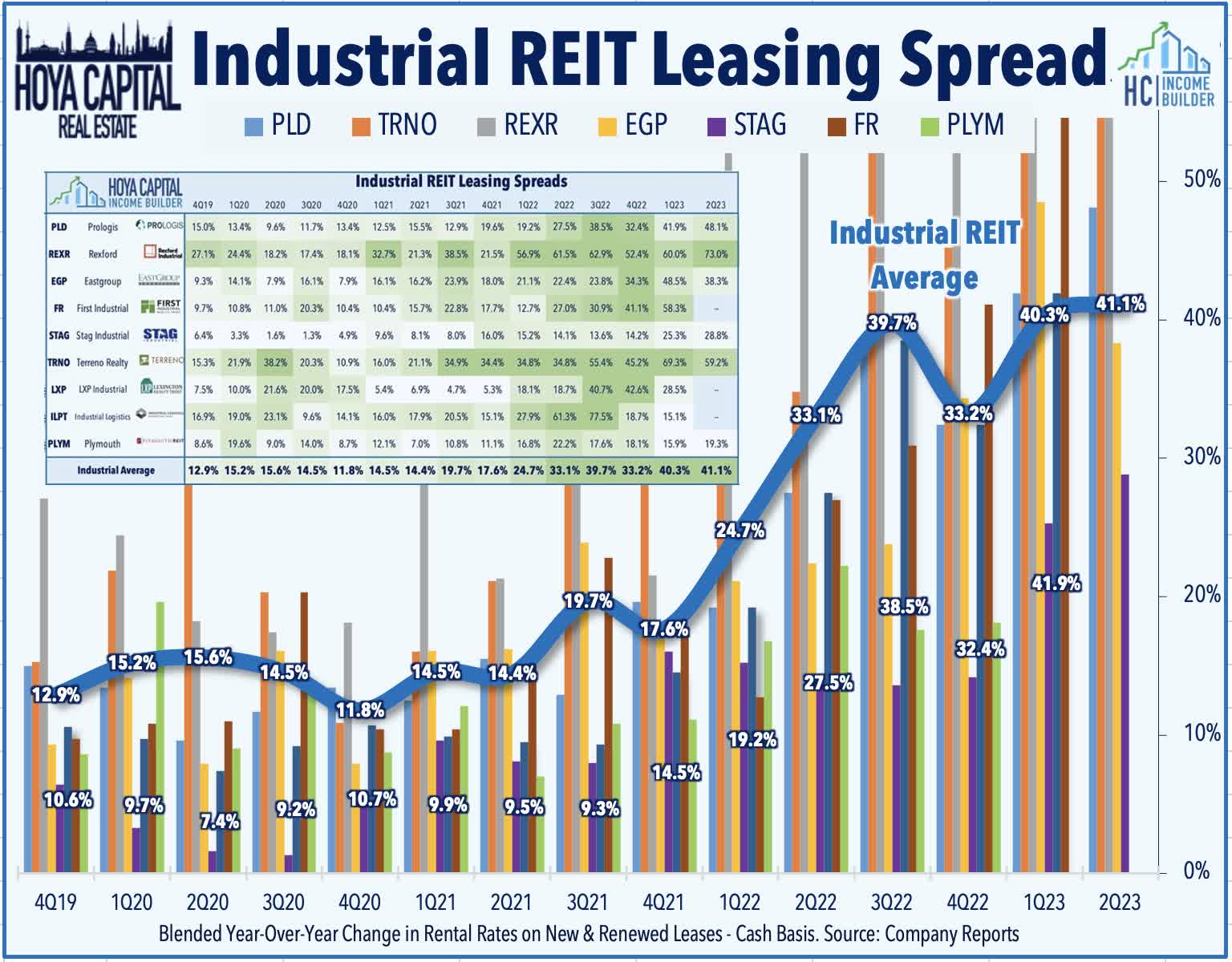

Industrial : Following their worst year of performance on record in 2022, industrial REITs have rebounded this year after first-quarter earnings results and recent interim updates showed a surprising re-strengthening of property-level fundamentals. Prologis ( PLD ) kicked-off earnings season on Tuesday with another "beat and raise" quarter, lifting its full-year FFO and NOI outlook by another 40 basis points driven by a record-high cash rent spread of 48.1% in Q2 - up from the 41.9% reported in Q1. PLD did note that overall market vacancies have trended slightly higher in recent quarters after hitting record-low levels in 2022 amid a "normalization" in demand trends combined with peaking supply growth, but reiterated its expectation that demand will begin to outpace supply again by 2024 given the sharp decline in new development starts in recent quarters. PLD also flagged Southern California as a region of concern and lowered its rent growth forecast on these properties, noting that "customers are re-evaluating expansion" amid persistent political and labor union issues. We're interested in hearing whether other industrial REITs are seeing these regional bifurcations and whether they share Prologis' upbeat outlook on medium and longer-term supply-demand fundamentals.

{kind=link}

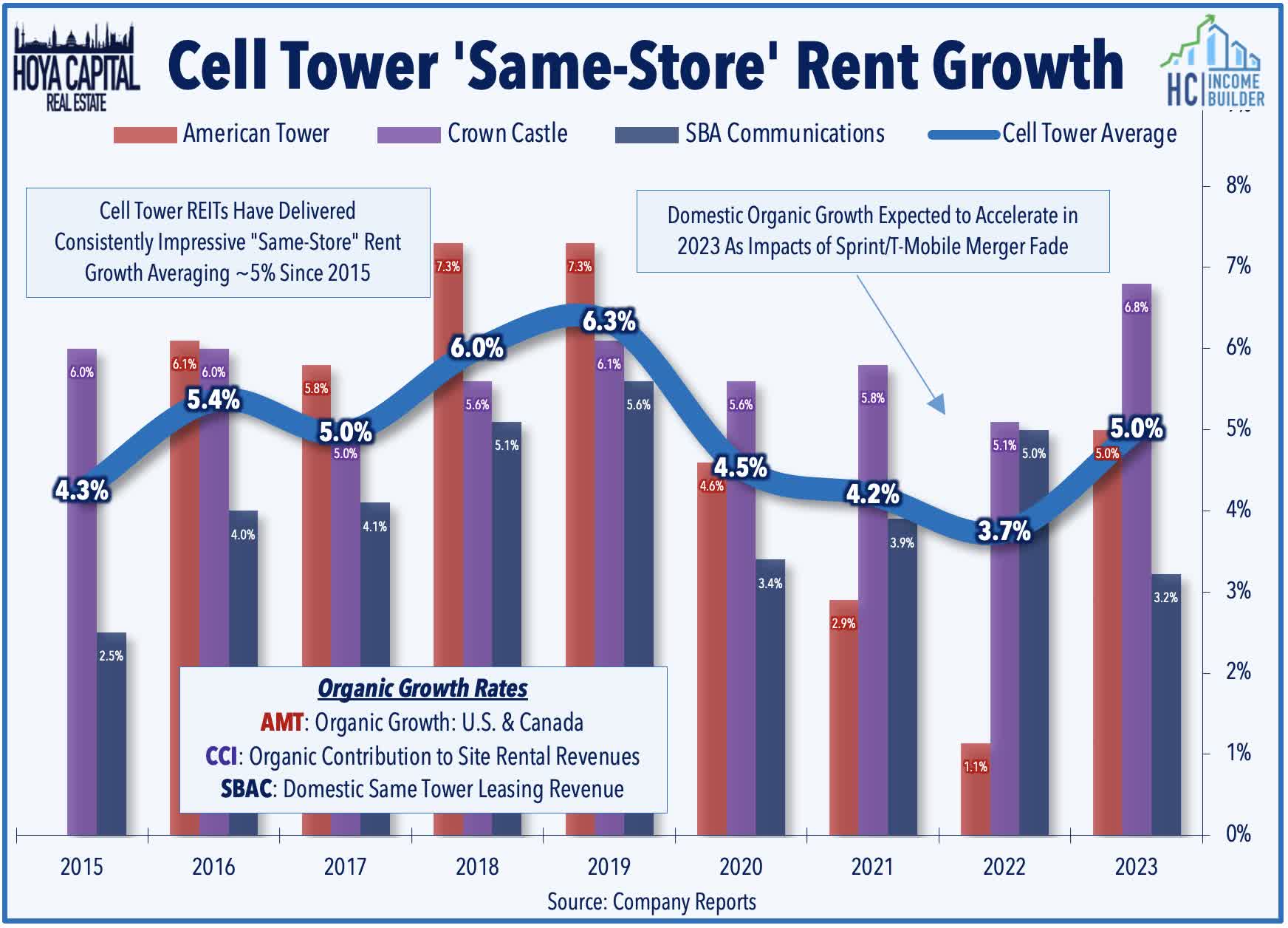

Cell Towers : The perennially-outperforming cell tower REIT sector has uncharacteristically stumbled this year, mirroring the downward pressure on their primary cell carrier tenants. The recent selling pressure on the carriers - and these REITs - has been compounded by a recent Wall Street Journal report that named AT&T ( T ) and Verizon ( VZ ) among several telecom companies that abandoned underground toxic lead cables, which are possibly causing environmental damage that likely require costly remediation. While cell tower REITs' direct exposure to these claims is appears to be very limited, network expansion could be impacted as carriers redirect time and funding away from 5G rollouts. The two major carriers have also been impacted by mounting competition both from within the industry via T-Mobile ( TMUS ) and DISH ( DISH ) and from the periphery via Amazon's ( AMZN ) rumored plans to enter the carrier business. More competition is certainly good news for these tower REITs, which appear to be unjustly caught up in the selling pressure. We're focused on commentary regarding any impacts of the WSJ report and on the viability and impact of Amazon's potential entrance into the space.

{kind=link}

Data Center : Among the top-performing property sectors this year, the Data Center REIT rebound has been augmented by reports of "booming" demand for artificial intelligence ("AI") focused data center chips. Ironically, this AI-wave comes just as Data Center REITs became a trendy “short” idea centered on a thesis of weak pricing power and competition from the "hyperscalers"- Amazon, Google, and Microsoft. A confluence of development bottlenecks - power shortages, higher cost of capital, supply chain constraints, ecopolitics, and NIMBYism - have created a more favorable dynamic and swung the pendulum of pricing power towards existing property owners. Barriers to supply growth combined with AI-accelerated demand should bring some sustained pricing power to a sector long-burdened by near-unlimited supply. With negotiating power tilting back towards landlords, there appears to be enough economic value to be shared. We'll again watch renewal pricing trends and leasing volumes closely this quarter.

{kind=link}

Retail REITs Earnings Preview

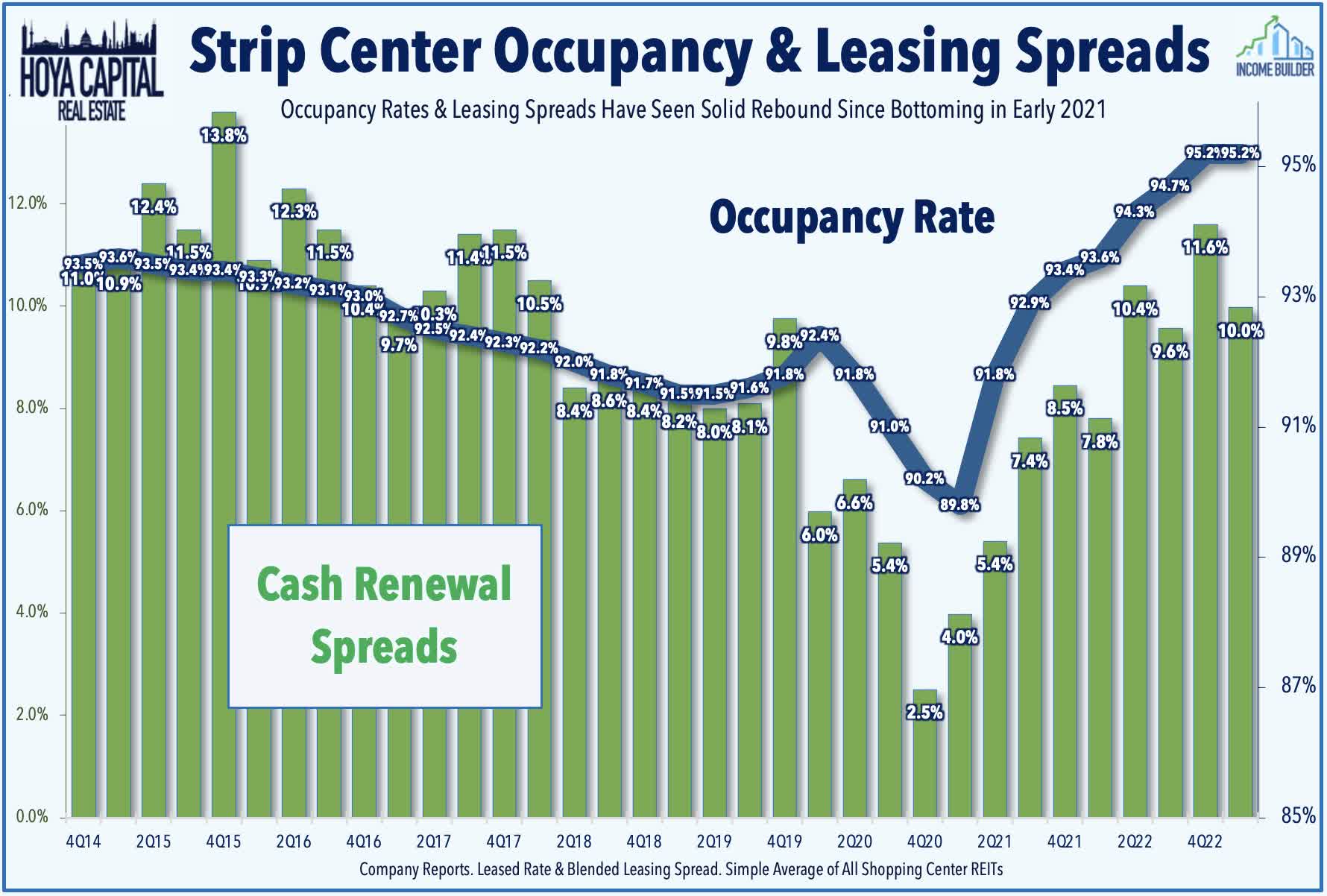

Strip Centers : Strip Center REIT fundamentals have improved materially over the past year and continue to be underappreciated in the market as a decade-long “retail apocalypse” narrative has been tough to shake. The combination of near-zero new development and positive net store openings since 2021 has driven occupancy rates to record-highs and allowed Strip Center REITs to enjoy some long-awaited pricing power. These favorable property-level supply/demand fundamentals have translated into impressive double-digit rent growth spreads since mid-2022 and the best earnings “beat rate” of any property sector during that time. Despite several high-profile retail bankruptcies - including Bed Bath & Beyond and Party City - store openings have continued to outpace store closings by about 50% so far in 2023, led by demand for space in large-format open-air strip centers. We'll again be focused on leasing spreads and occupancy rate trends - which have been impressive of late - and on updates on re-lease progress at these vacated Bed Bath and Party City locations, in particular. We also expect strip center REITs to be among the leaders in dividend growth in the back-half of the year.

{kind=link}

Malls : With recent distress across office markets seizing the headlines, Mall REITs are no longer the "Problem Child" of the REIT sector, particularly after weaker players and lower-tier malls closed shop. Following three years of rental rate and occupancy declines, the supply-demand dynamic has recently favored retail landlords, which has helped these stumbling mall REITs regain some footing and repair balance sheets in anticipation of tougher times ahead. Traffic and sales levels at higher-end mall properties were back to pre-pandemic levels during the holiday season, but we're interested to see if this momentum continued into the second quarter, given the relatively softer trends seen in the Commerce Department's retail sales reports. We're focused on same-store occupancy rates this earnings season - which remained relatively soft last quarter despite improving NOI and FFO trends - and we want to see rental rates stabilize before we can officially call the bottom to the decade-long downward pressure on FFO.

{kind=link}

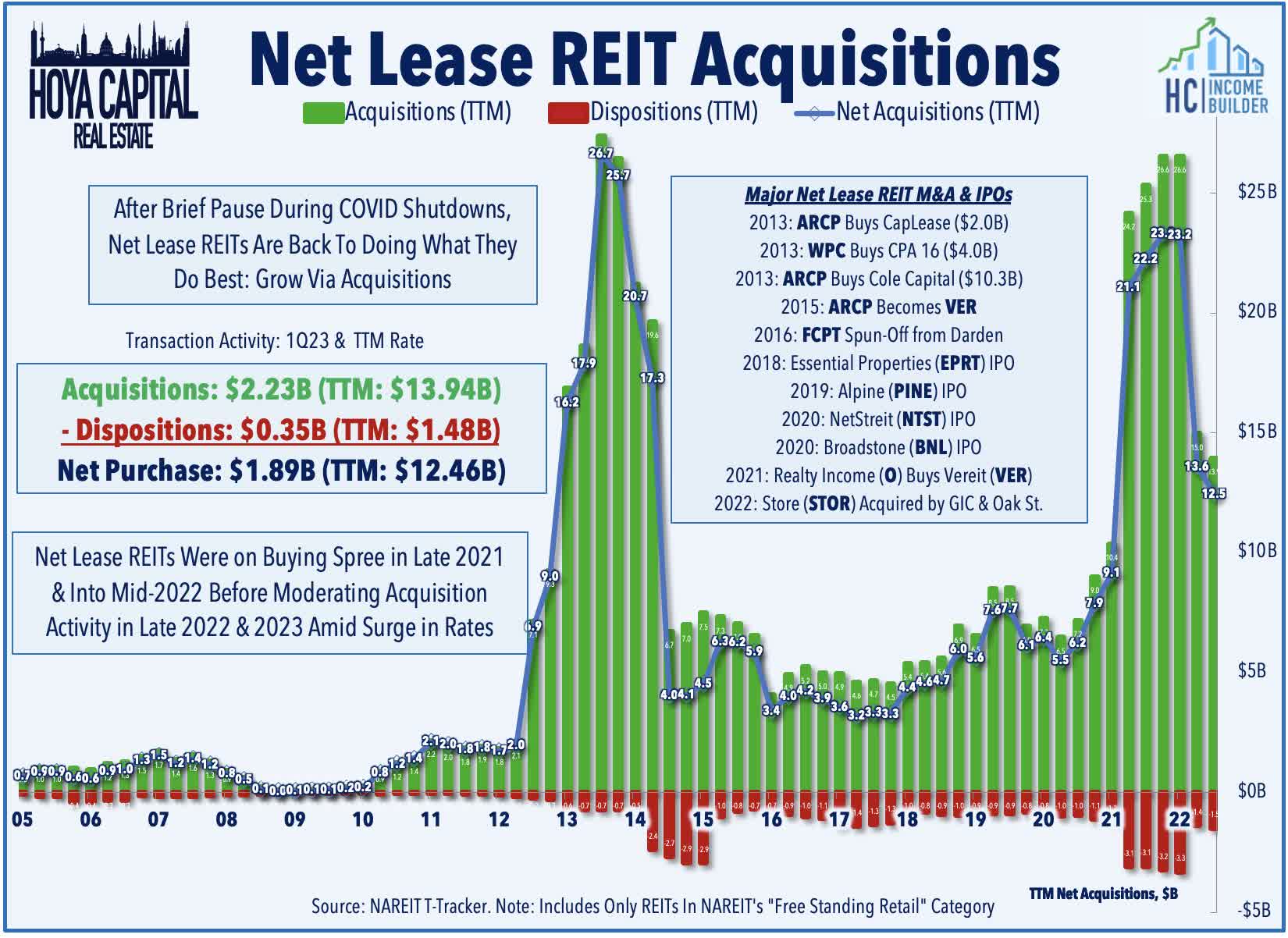

Net Lease : Historically one of the most "rate-sensitive" property sectors, net lease REITs have surprisingly been among the best-performing major property sector since early 2021 despite the significant rise in interest rates. Private market values remained far "stickier" than comparable public market assets through much of 2022, but despite the tighter investment spreads, the pace of acquisition activity for some REITs slowed only modestly in late 2022, a strategy that could prove costly if rates remain persistently elevated. Strong balance sheets and lack of variable rate debt exposure have positioned net lease REITs to be aggressors as over-levered private players seek an exit, but these REITs can afford to wait until the price is right. We're keyed-in on commentary regarding cap rate movements in early 2023 for a read on whether private market asset owners are holding tight or ready to adjust price expectations to the reality of higher benchmark rates.

{kind=link}

Hotel & Casino REIT Earnings Preview

Hotels : Despite lingering recession concerns, Hotel REITs are pacing for a second-straight year of outperformance after punishing early-pandemic declines, buoyed by steady post-pandemic operating improvement and the long-awaited return of dividends. Domestic travel recovered to 100% of pre-pandemic levels in early 2023 and has held-up around record-high levels throughout the year. Business and group demand has marginally improved, offsetting some moderation in leisure demand. International travel demand has started to provide a healthy tailwind as the final pandemic-era travel restrictions were lifted in May. Squaring with data from STR showing that hotel occupancy rates are hovering around the prior record-highs set in 2019, TSA reported last week that it processed record-high throughput at its checkpoints during the Independence Day week, peaking at nearly 3 million travelers for the first time ever. We're hoping to see additional hotel REITs provide full-year guidance after several years of limited disclosures amid COVID-related uncertainty and expect the sector to be among the leaders in dividend increases in the back-half of 2023.

{kind=link}

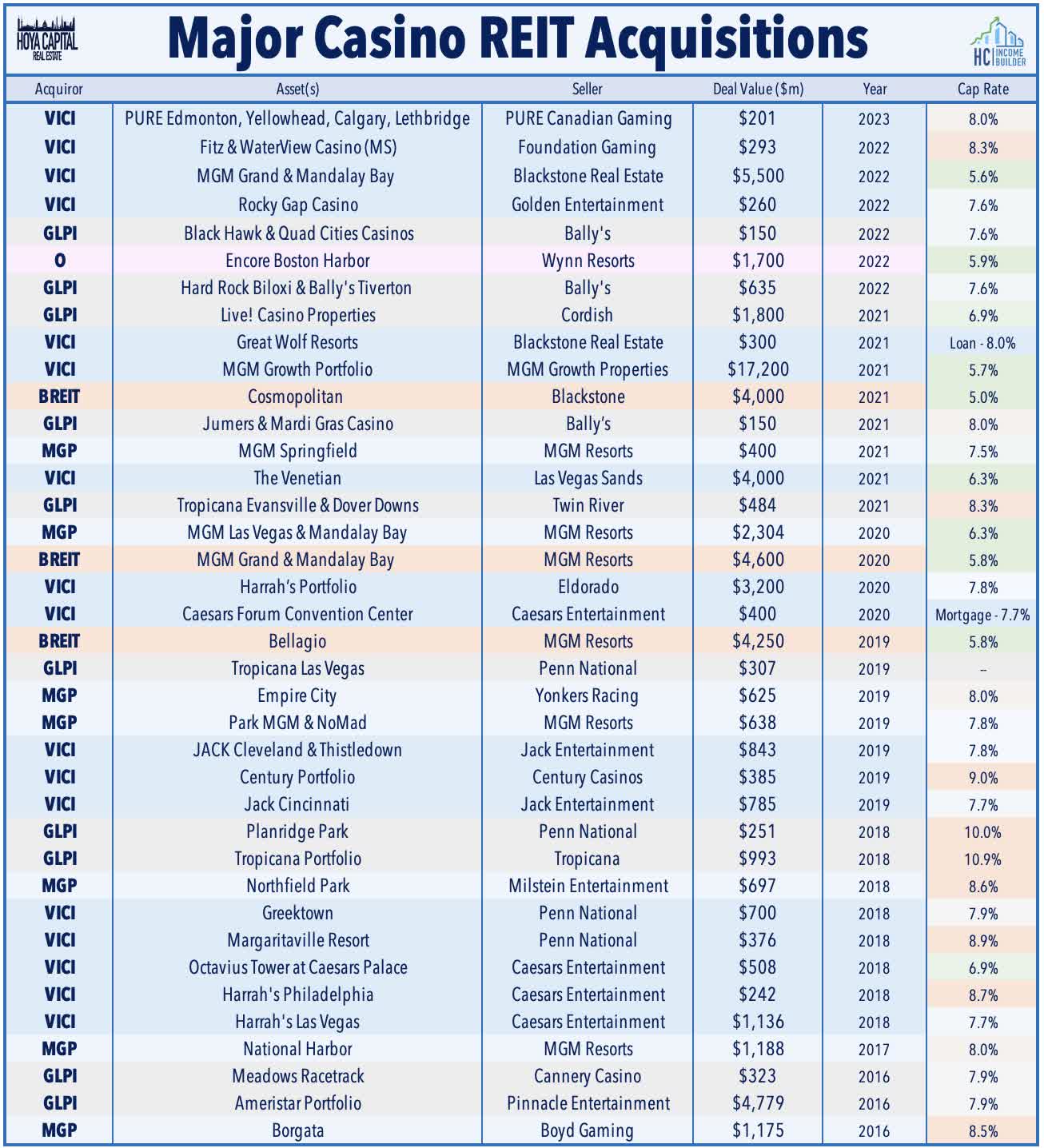

Casinos : Casino REITs were the lone property sector to finish in positive territory in 2022, benefiting from their attractive “inflation-hedging” lease structure, strength in Las Vegas travel demand, and broader institutional investor acceptance. A success story of the "Modern REIT Era," Casino REITs have been the best-performing property sector since their emergence in the mid-2010s, honing the competitive advantages of the public REIT model. Fittingly, Casino REITs - exemplars in shareholder-friendly governance - have been beneficiaries of distress felt across the darker underbelly of the real estate industry, including Blackstone’s non-traded REIT ("NTR") platform. M&A will again be the focus of earnings season, and we're focused specifically on whether any REITs have had discussions about acquiring BREIT's interest in the Bellagio and Cosmopolitan.

{kind=link}

Office & Healthcare REIT Earnings Preview

Office : Brokerage firm JLL ( JLL ) reported last week that office leasing activity rebounded 7.7% in Q2 compared to Q1, an encouraging sign that office demand may be showing early signs of stabilization. The 40.4 million square feet of space leased in the second quarter was still roughly 14% below the same period a year ago and still about 25% below the pre-pandemic average from 2016-2019. Debt service expenses have been the primary culprit behind the wave of recent loan defaults on coastal office properties from private equity firms Brookfield, Blackstone, and Pimco, but the question remains whether there's any value in being the best house in a bad neighborhood or whether the downward inertia and spiraling effect on prices eventually drags even the better-capitalized players into the sinkhole. Nationally, property-level cash flows and occupancy rates remain within 5% of pre-pandemic levels, but actual utilization rates continue to exhibit a wide regional variance. Coastal tech-heavy markets remain at sub-50% daily utilization rates compared to pre-pandemic levels, but Sunbelt and secondary markets - most with less costly commutes - have recovered to over 75%.

{kind=link}

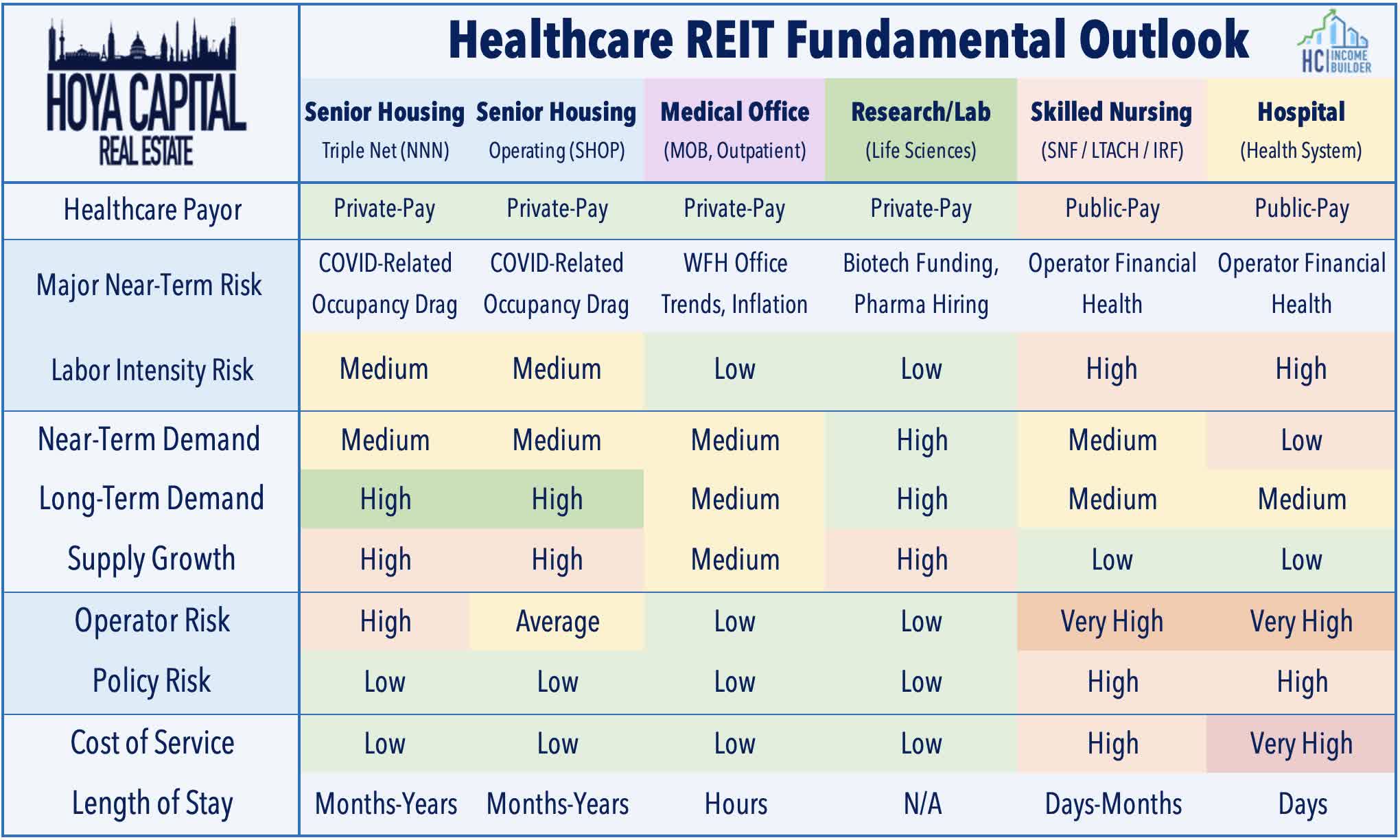

Public-Pay Healthcare : We segment the healthcare space along the private/public pay divide given the divergent fundamentals between the public-pay sub-sectors - hospitals and skilled nursing - and the private-pay sub-sectors - senior housing, medical office, and lab space. On the public-pay side, we've seen an intensification of tenant rent collection from struggling tenant operators. Gibbins Advisors reported early this year that bankruptcy filings for healthcare companies nearly doubled in 2022 compared to the prior year, which it attributes to this “COVID hangover” resulting from waning government support and higher labor costs. Medical Properties Trust ( MPW ) - which remains in the cross-hairs of short-sellers - has been a laggard this year, with tenant concerns still in focus. Skilled nursing REITs have also reported lingering rent collection difficulties from a handful of struggling operators, but also highlighted some progress last quarter in restructurings. Tenant health - and resulting dividend sustainability is the primary focus of earnings season for these public-pay healthcare REITs.

{kind=link}

Private-Pay Healthcare : Conditions are far more stable on the private-pay side. Senior Housing ("SH") REITs Welltower ( WELL ) and Ventas ( VTR ) have been among the better performers this year, lifted by NIC data showing that the senior housing occupancy rate increased to 83.7% in the second quarter, continuing a slow-but-steady rebound from its pandemic lows of 77.8%. While occupancy rates remain below the pre-pandemic levels of around 90%, rent growth set another record-high in Q2 at 5.7%, strength that has been fueled, in large-part, by the nearly-9% increase in social security benefits, which has allowed SH owners to push rent increases. Positively for senior housing REITs, supply growth has finally cooled following a decade of elevated inventory growth, as NIC reported that units under construction amounted to 4.9% of total inventory, which is the lowest seen since 2014. Results from lab space owners Alexandria ( ARE ) and Healthpeak ( PEAK ) will be closely watched for updates on tenant health and leasing volume.

{kind=link}

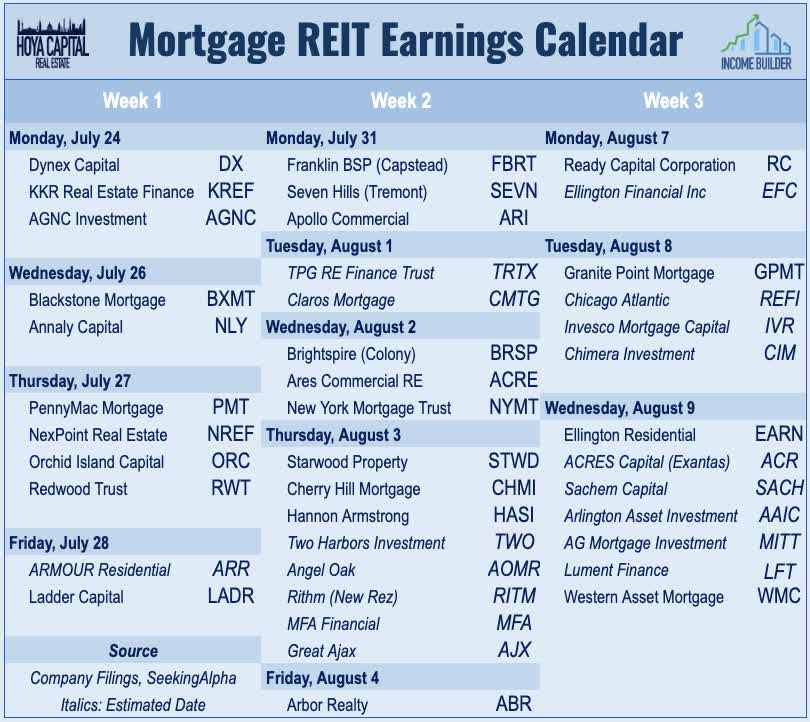

Mortgage REITs Earnings Preview

"Here we go again" was the attitude for a brief period last month in the wake of the Silicon Valley Bank collapse, as sharp changes in benchmark rates and/or spreads in either direction can wreak havoc on mortgage REITs that are caught over-levered or improperly hedged. Conditions have stabilized since April, however, which has lifted the iShares Mortgage REIT ETF ( REM ) higher by nearly 25% from its March 23rd lows. The RMBS and CMBS benchmarks were about flat in Q2 as a decline in spreads was offset by a modest increase in benchmark rates. For residential mREITs, book values and dividend commentary will be the major focus. For commercial mREITs, we're more closely-focused on loan performance and changes in Current Expected Credit Loss ("CECL") allowance - particularly for mREITs with significant office exposure. We note that despite paying average dividend yields in the mid-teens, the majority of mREITs have been able to cover their dividends, but there remains a handful of mREITs with payout ratios above 100% of EPS.

Buy Ratings : Blackstone ( BX ), Rithm ( RITM ), KKR Real Estate ( KREF )

{kind=link}

Key Takeaways: Real Estate Earnings Preview

Real estate earnings season kicks into gear this week, and over the next month, we'll hear results from 175 equity REITs, 40 mortgage REITs, and dozens of housing industry companies. Real estate equities - the sector with perhaps the most to gain from a moderation in inflation and normalization in Fed monetary policy - enter earnings season with wind in their sails. Expenses and margins will be a key focus amid broader disinflationary impacts on revenues and upside guidance revisions to Net Operating Income ("NOI") are likely to be driven by lower expense expectations. Access to capital is also a focus amid expectations that capitulation from debt-burdened private portfolios will create consolidation opportunities for well-capitalized REITs, and public REITs' access to equity capital could become a major competitive advantage if debt markets remain tight. As always. we'll provide real-time commentary throughout earnings season for Income Builder members.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

REIT Earnings Preview: Here's What We're Watching