VRAI - REIT Earnings Preview: The New Normal

Summary

- Real estate earnings season kicks into gear this week, and over the next month, we'll hear results from 175 equity REITs, 40 mortgage REITs, and dozens of housing industry companies.

- REITs enter earnings season with some momentum amid the recent moderation in interest rates and hopes of a 'softish' economic landing following a punishing year of stock price performance.

- How REITs are responding to this higher rate environment – both on the acquisitions and the financing side - will be closely watched. REITs hunkered down in 2022, but opportunities are becoming more plentiful.

- The non-traded REIT sector - headlined by Blackstone and KKR - may be an area "ripe for the picking" if investor redemptions continue. We foresee many of the recently-privatized portfolios eventually coming back into public markets.

- Full-year FFO guidance will be the metric most closely watched - especially in the residential, retail, and office sectors given the wide range of analyst expectations. We discuss the themes and metrics we're most focused on this earnings season across each property sector.

Real Estate Earnings Preview

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on January 29th.

{kind=link}

Real estate earnings season kicks off this week, and over the next month, we'll hear results from more than 175 equity REITs, 40 mortgage REITs, and dozens of housing industry companies which will provide key insights into how the real estate industry is adapting to the higher interest rate regime. This report discusses the major high-level themes and metrics we'll be watching across each of the real estate property sectors this earnings season. Below, we compiled the earnings calendar for equity REITs and homebuilders. (Note: Companies that have not yet confirmed an earnings date are in italics.)

{kind=link}

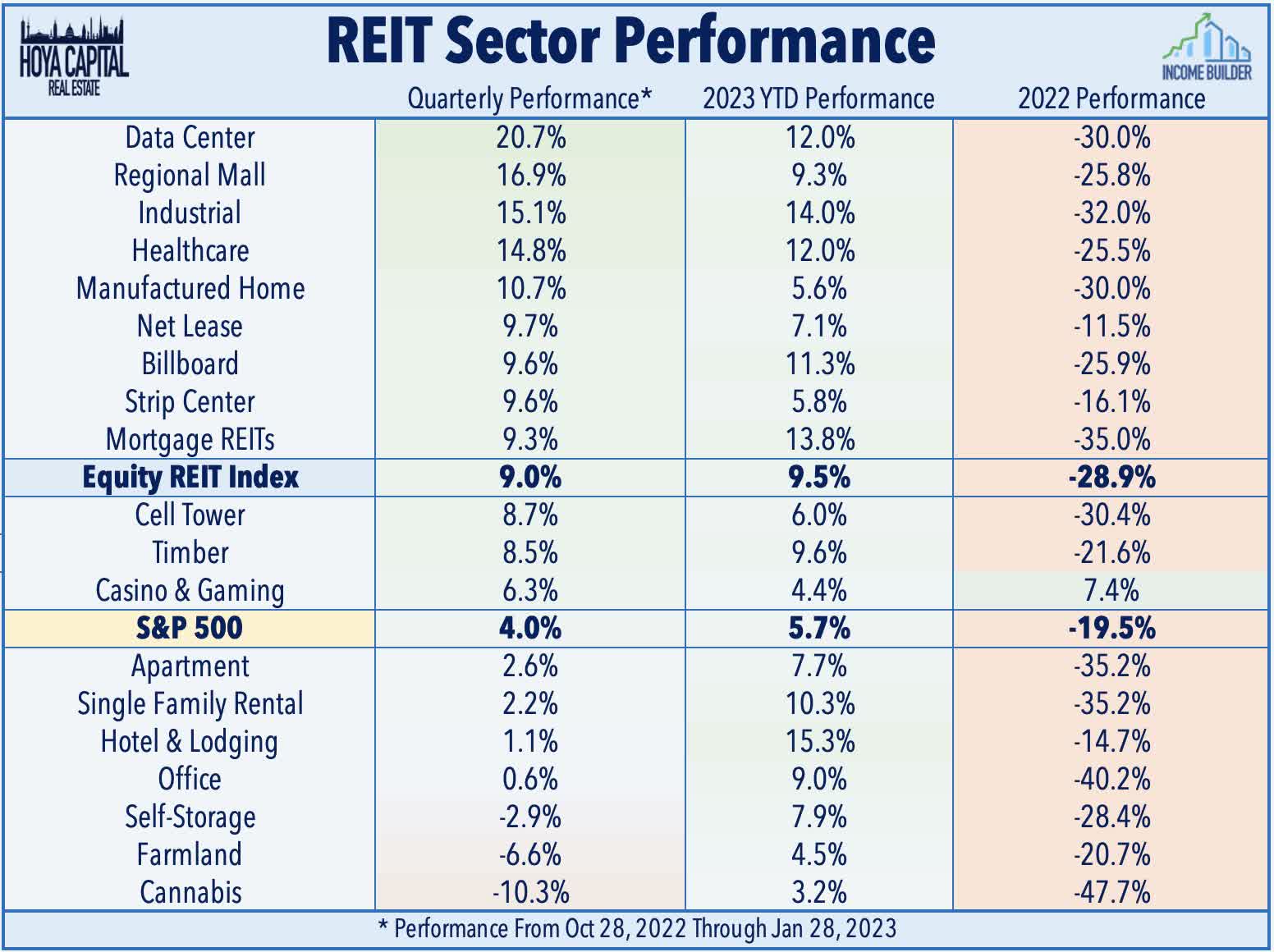

Real estate equities enter earnings season with some momentum following a punishing year in 2022 in which the Vanguard Real Estate ETF ( VNQ ) slid more than 25% on a total return basis - its second-worst year on record behind 2008 - and the worst returns among the ten major asset classes. A moderation in interest rates and hopes of a 'softish' economic landing has sparked a bid for yield-sensitive asset classes, in particular, with the Equity REIT Index higher by over 9% through the first four weeks of 2023. Since the start of the last earnings season in October, we've seen a notable rebound in performance from data center, industrial, retail, and healthcare REITs while office, hotel, and residential-focused sectors have been among the laggards during this period, entering earnings season with lowered expectations.

{kind=link}

Before diving into the specific sector-by-sector metrics we're focused on this earnings season, we discuss the three higher-level themes that we're focused on this earnings season:

- Cap Rates & Private Market Valuations

- Balance Sheets & Rate Expectations

- Full-Year 2023 FFO Guidance

1) Cap Rates & Private Market Valuations

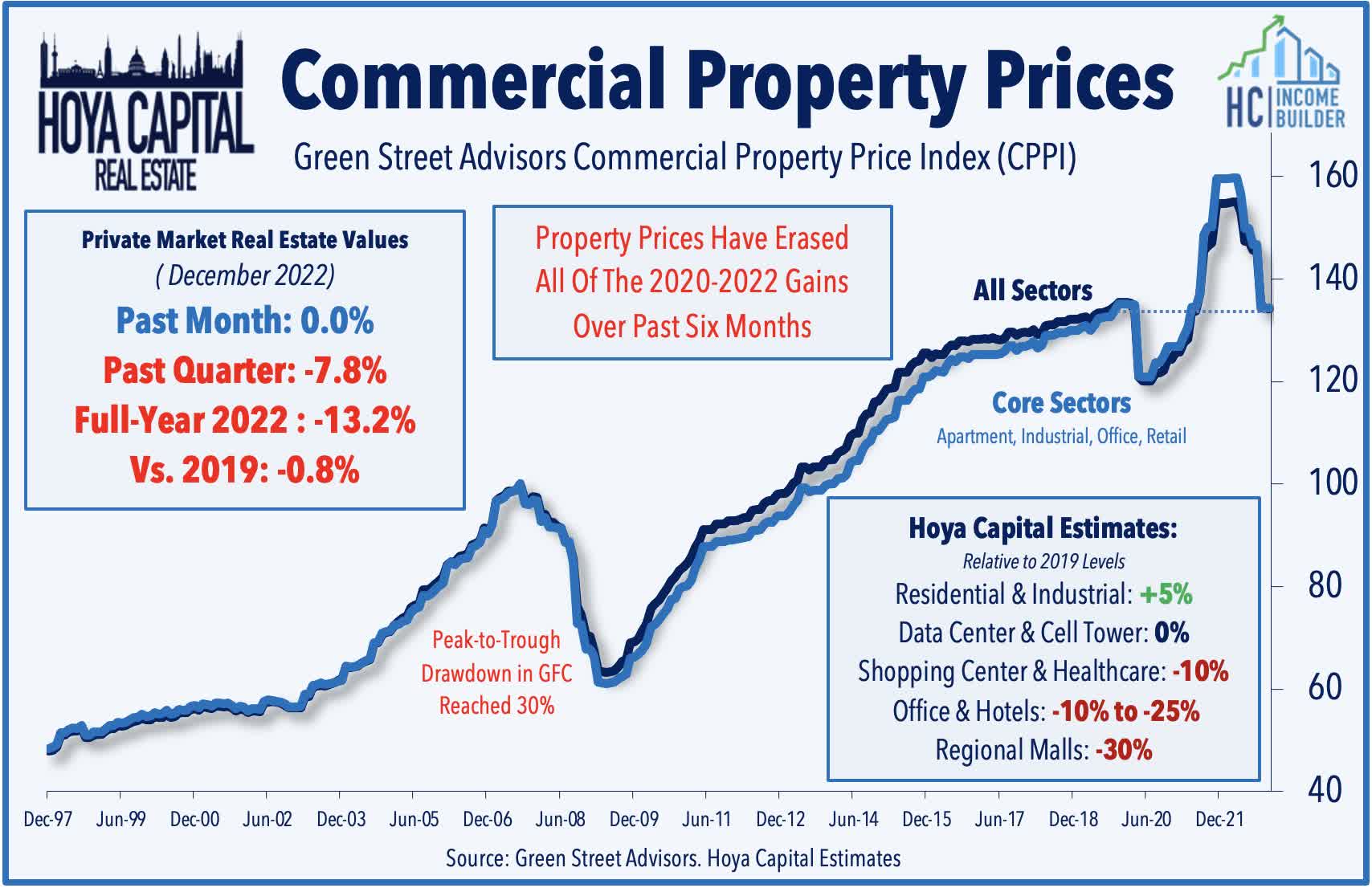

This active debate has been playing out across the U.S. real estate industry - a unique "dual market" structure with both an active public and private market. Private real estate markets are finally "catching up" to the reality of sharply higher interest rates - and expectations that rates may be "higher for longer" - which have been reflected in public real estate markets for several quarters. Recent Green Street Advisors data shows that private market real estate values declined 13% in 2022 and now sit about 1% below pre-pandemic levels. While transactions have been few and far between in recent months given the wide bid-ask spread in commercial real estate markets, commentary regarding estimated capitalization rates ("Cap Rates") - and by extension real estate valuations - will be closely watched across the sector.

{kind=link}

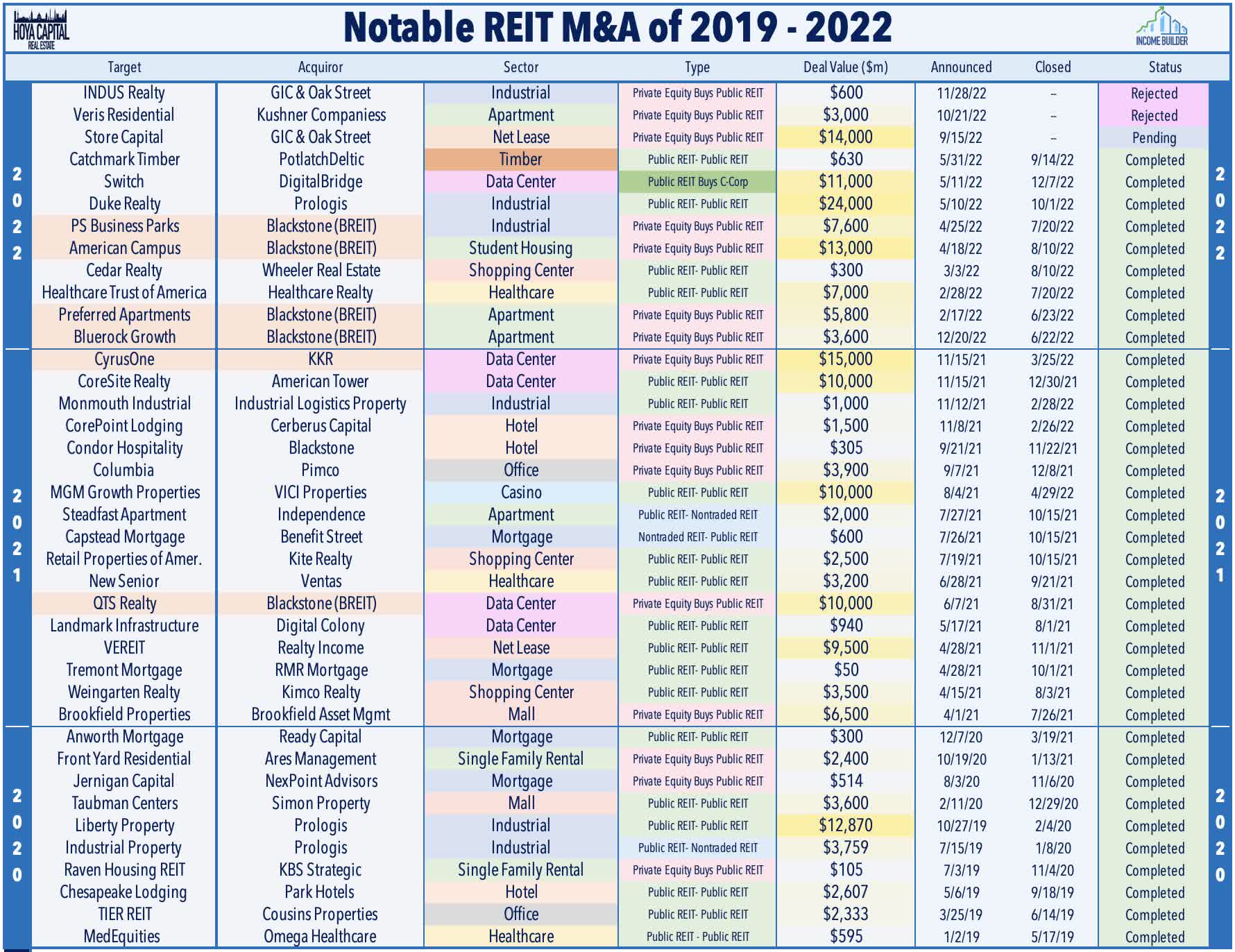

This commentary is particularly pertinent given the recent focus on the non-traded REIT ("NTR") platforms - including those offered by Blackstone ( BX ), Starwood , and KKR ( KKR ) - which have come under scrutiny in recent months after limiting investor redemptions at valuations that were seemingly still based on 2021 market conditions. Blackstone's non-traded real estate platform - BREIT - estimated that its Net Asset Value increased about 30% during that same three-year period in which public REITs ( VNQ ) and private real estate valuations were lower by 1%. Publicly-traded REITs, by contrast, trade at an estimated 10-15% discount to consensus Net Asset Value ("NAV") estimates. This discount has narrowed a bit in recent weeks amid a broader rebound in public REIT valuations, and we're interested to hear if public REITs are looking to become more opportunistic on the acquisitions-front.

{kind=link}

What goes around comes around? These non-traded REIT platforms were on a "buying spree" from late 2020 into mid-2022 - paying "top dollar" for many of these large portfolio transactions - including the acquisition of more than a half-dozen public REITs. Foreshadowed by Blackstone's deal with VICI Properties ( VICI ) to sell its $5.5B stake in the MGM Grand Las Vegas and the Mandalay Bay Resort to VICI , we see these NTR platforms as "ripe for the picking" for opportunistic public REITs if redemption requests remain elevated. Even without "forced selling" in the near-term, we believe that the recent redemption limits exposed a key deficiency in the NTR structure compared with the far more investor-friendly and efficient publicly-traded REITs and foresee many of these assets eventually returning to the public markets.

{kind=link}

2) Balance Sheets & Rate Expectations

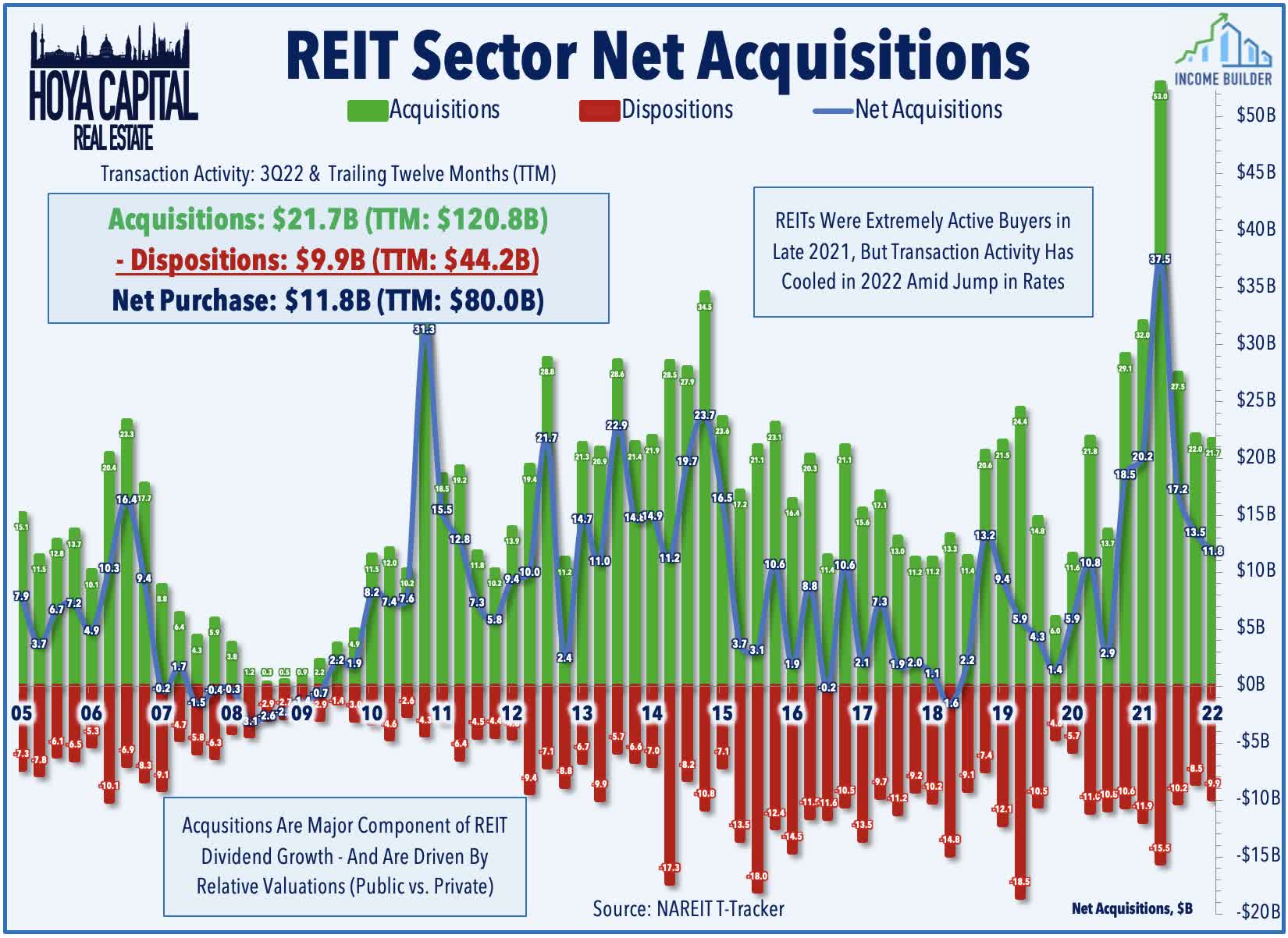

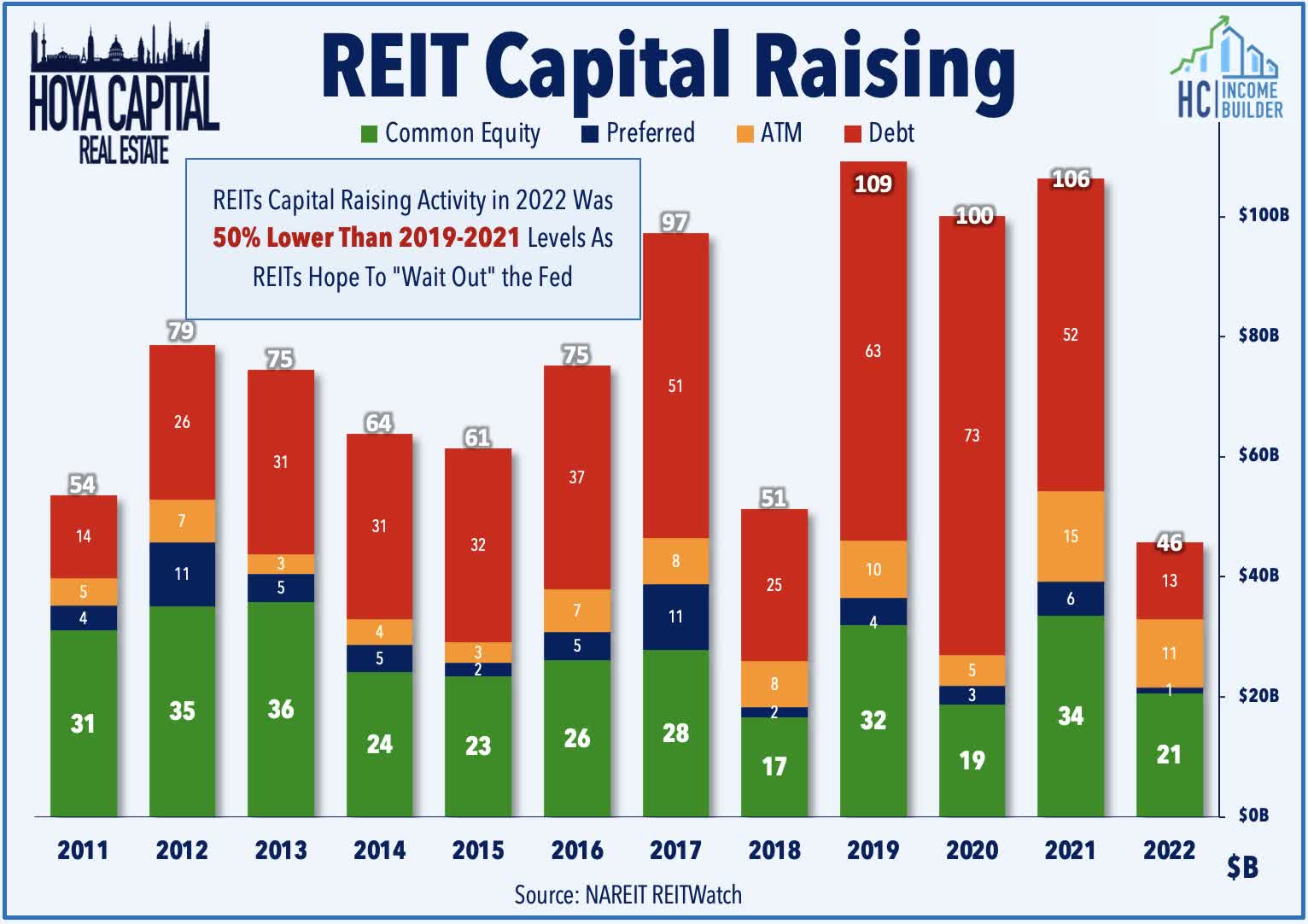

Given the historic surge in interest rates in 2022, REITs have largely "hunkered down" over the last year - a benefit that was “earned” through their cautious balance sheet management over the past decade. As noted in our State of the REIT Nation report, following several years of robust capital-raising activity and balance sheet deleveraging, REITs raised less capital in 2022 than in any year of the prior decade and leaned more heavily into shorter-term credit facilities for funding needs, hoping to "wait out" the Fed and avoid locking in these higher rates on longer-term capital. We're interested in hearing which REITs are seeking to take advantage of the recent pull-back in benchmark lending rates and rebound in equity market valuations - and how the overall balance sheet strategy has evolved in the "new normal."

{kind=link}

Unlike the post-GFC period, there is no looming "wall of maturity" this time around as public REITs' access to long-term bond markets has allowed them to push their average maturity to nearly 7 years - but incremental external growth would almost surely require additional long-term capital. While most REITs remain on very solid footing with no immediate capital needs, the same can't necessarily be said about many private market players that rely on more short-term borrowing and continuous equity inflows to keep the wheels spinning. Much the opposite of their role during the GFC, many well-capitalized REITs are equipped to "play offense" and take advantage of acquisition opportunities from these private players - but whether or not these typically-defensive REITs are ready to take a more aggressive tact remains a key focus.

{kind=link}

3) Full-Year 2023 Guidance

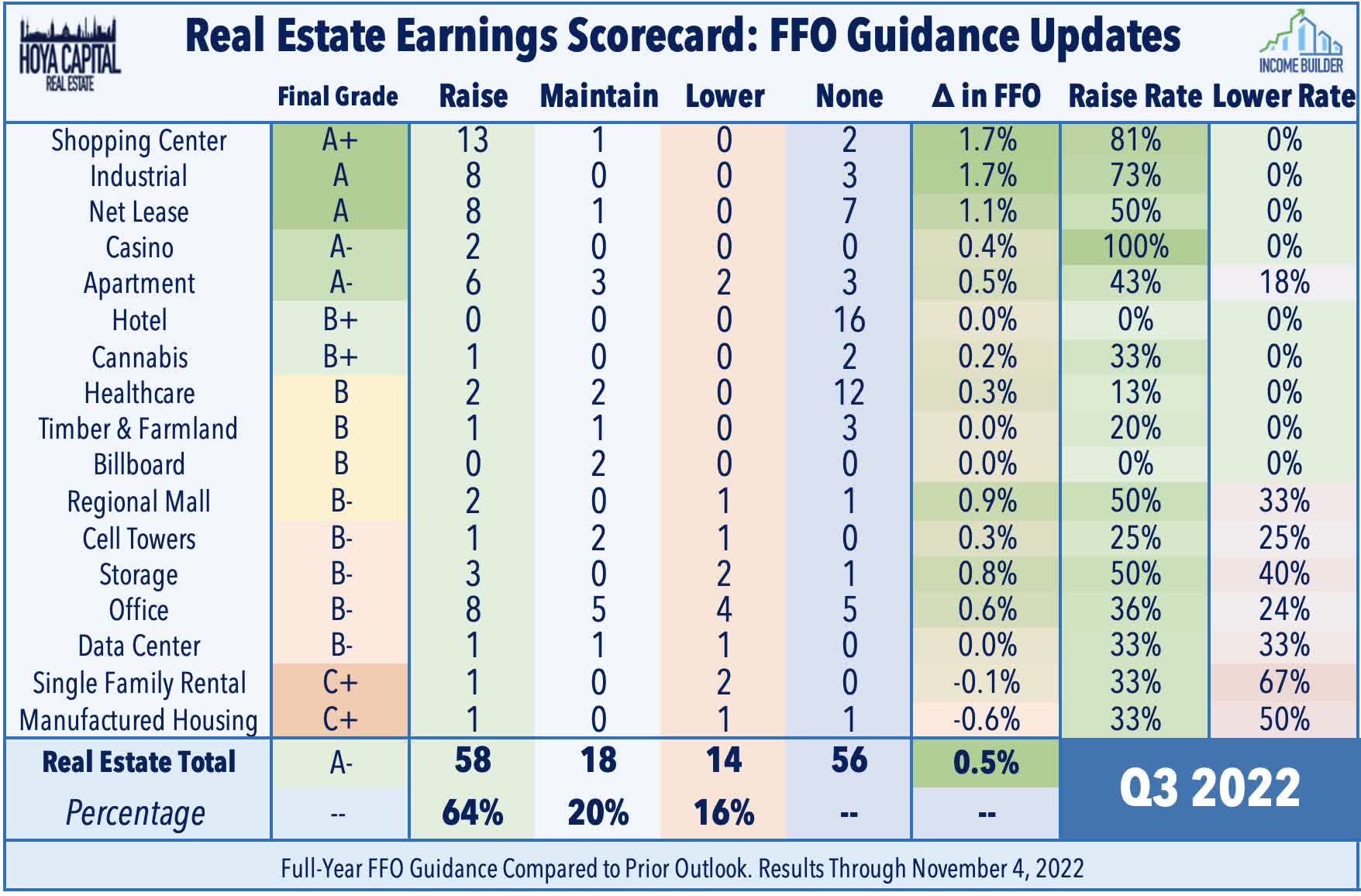

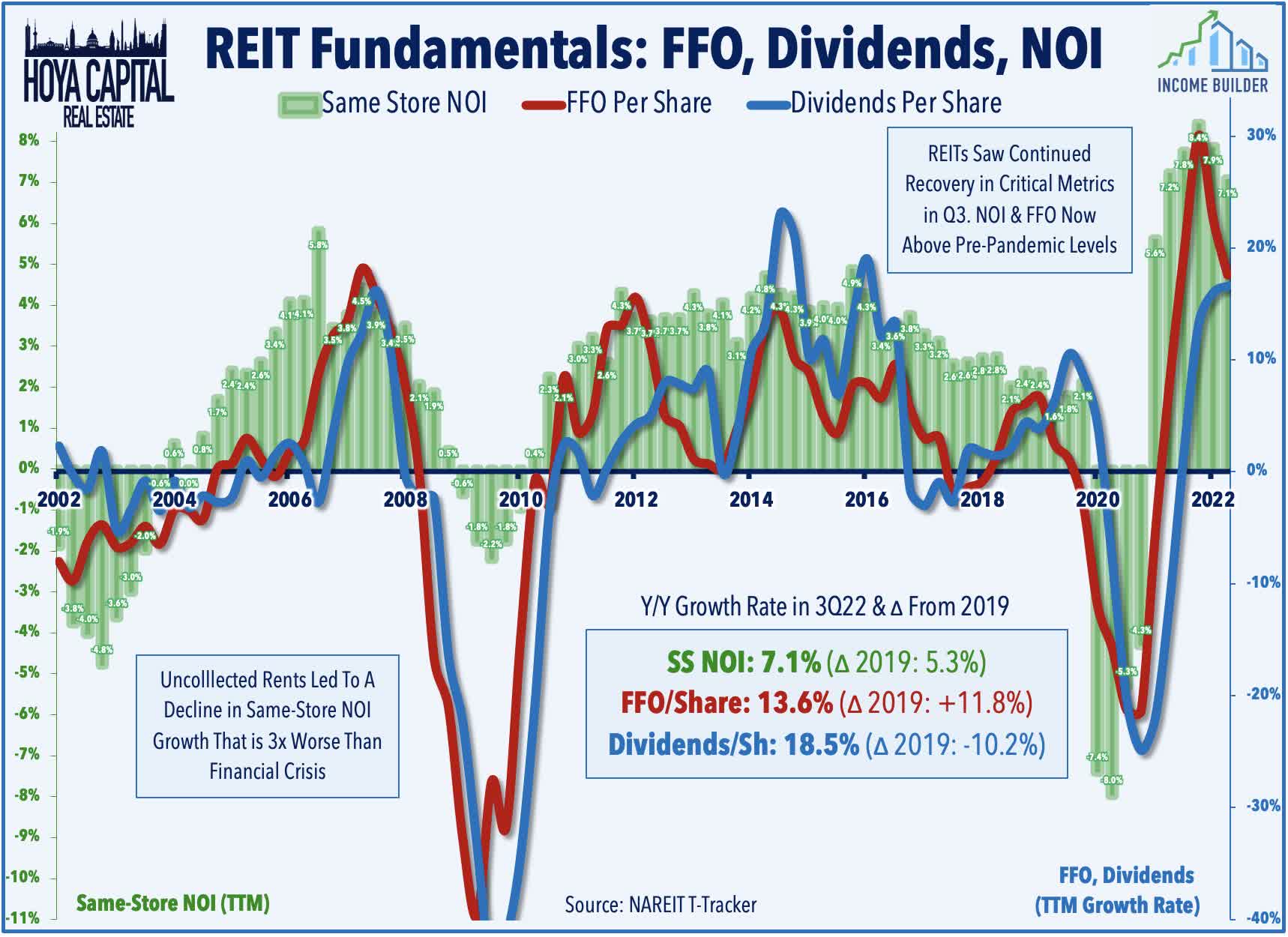

All eyes will be on these REITs' full-year outlook for 2023 with nearly 100 REITs expected to provide their initial FFO and/or NOI guidance for the year. Obscured by the macro narrative, company-level REIT fundamentals have been quite strong - and strengthening - for most property sectors in recent quarters. Third-quarter REIT earnings season was surprisingly strong with nearly two-thirds of REITs raising their full-year 2022 FFO outlook, which came alongside an otherwise disappointing earnings season for the broader equity market in which less than half of S&P 500 companies boosted their outlook.

{kind=link}

REIT FFO/share ("Funds From Operations") is projected to end 2022 at levels that are about 15% above pre-pandemic levels - led by relative outperformance from residential, industrial, and technology REITs. Consensus expectations call for 6-8% FFO growth in 2023 for the sector average, but REITs typically provide a relatively conservative initial outlook with room to raise in subsequent quarters, so a mid-single-digit initial FFO growth target will be seen as a "beat" across most sectors. Dividend commentary will also be in focus following a record pace of hikes in 2021 and 2022. With a historically low dividend payout ratio, most equity REITs still have a healthy buffer to protect current payout levels if macroeconomic conditions take a turn for the worse. Below, we discuss the specific metrics we're watching across each sector.

{kind=link}

Residential REITs Earnings Preview

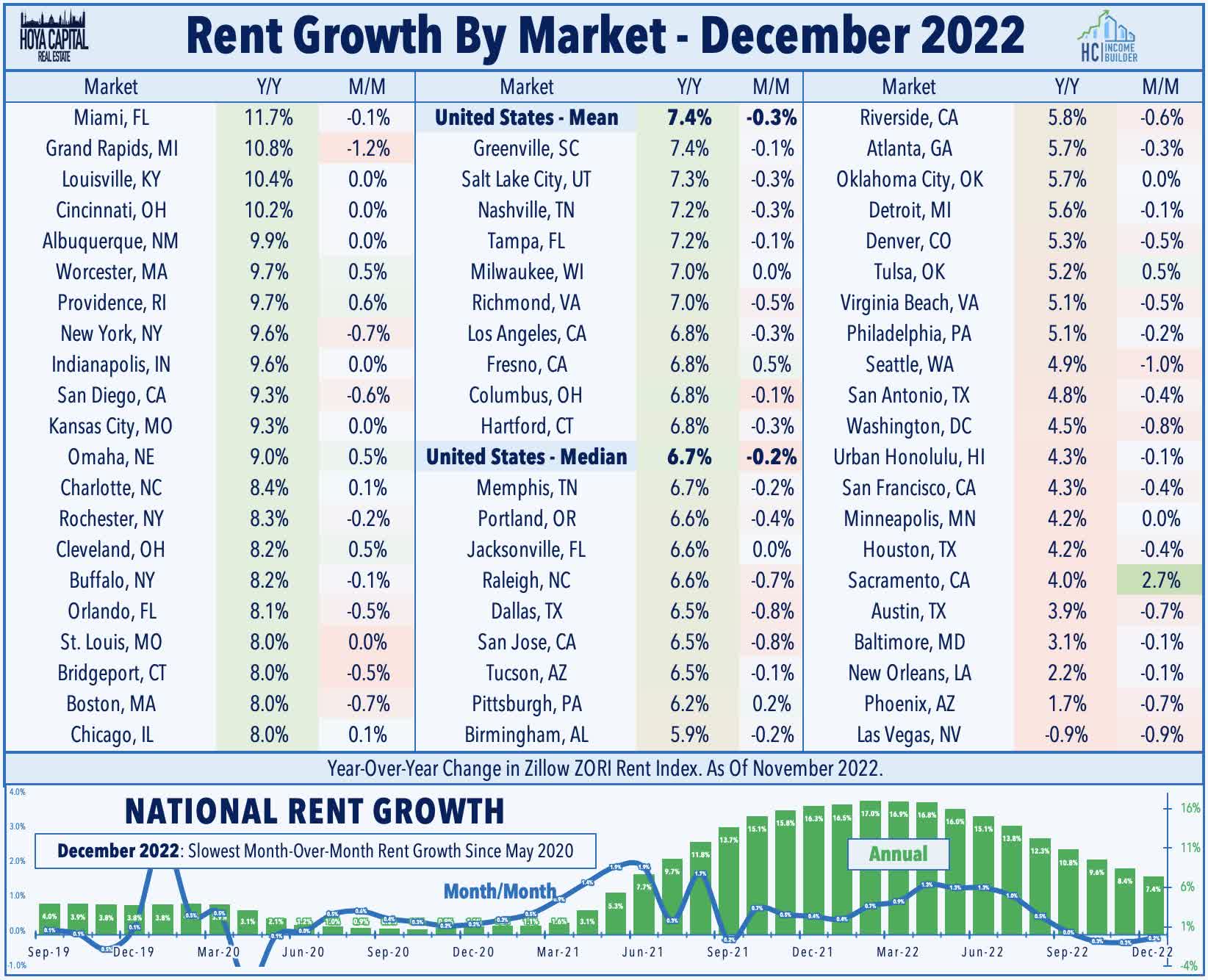

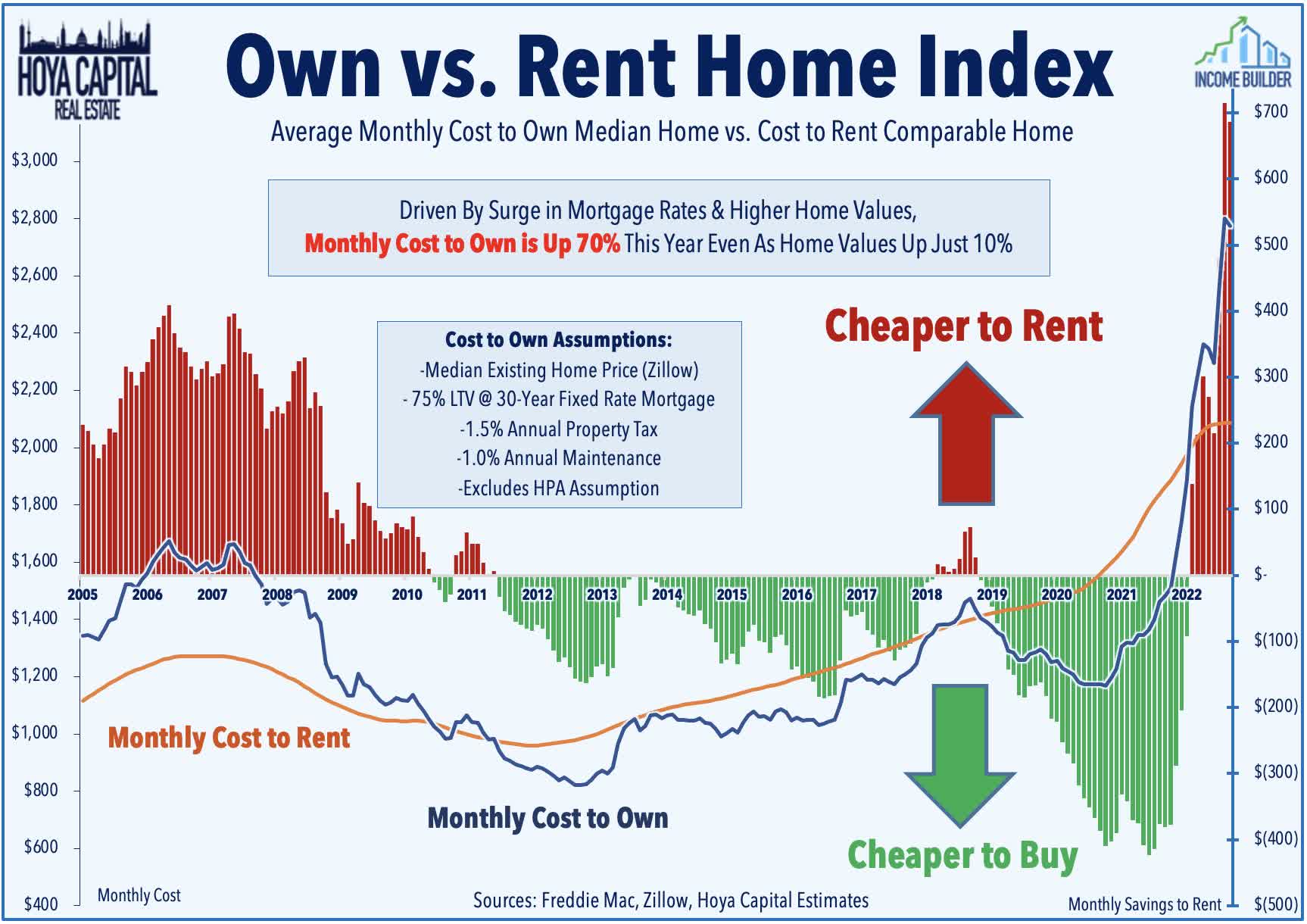

Apartments : The state of the U.S. housing market will be a critical focus throughout earnings season - the industry feeling the most direct effects from historic monetary tightening since mid-2022. Consensus sentiment around apartment REITs has remained distinctly negative despite recent "green shoots" in forward-looking housing metrics. Recent data from Apartment List and Zillow shows that rent growth cooled considerably in the back-half of 2022 and investors are split on whether we're seeing the start of a sustained downtrend with negative annual rent growth or whether the recent softness is more symptomatic of a normalization back towards "trend levels." We'll be closely-watching rent growth metrics on new and renewed leases and remain focused on the regional disparities between Sunbelt and Coastal markets.

{kind=link}

Single-Family Rentals : Cooling home price appreciation and tightening credit conditions is indeed bad news for many new “start-up” entrants into the single-family rental ("SFR") scene that are learning the hard way that the SFR game is a capital-intensive business that requires significant scale to operate profitably. While residential rent growth has moderated over the past six months, the recent gloomy narrative on SFR REITs appear particularly unwarranted given the still-strong labor markets, lack of new single-family housing supply, and affordability conditions that remain heavily skewed towards renting over owning. In addition to SFR rent growth metrics, we're interested in commentary about external growth prospects - specifically whether these REITs are seeing signs of distress in private markets that could create discounted buying opportunities in the quarters ahead.

{kind=link}

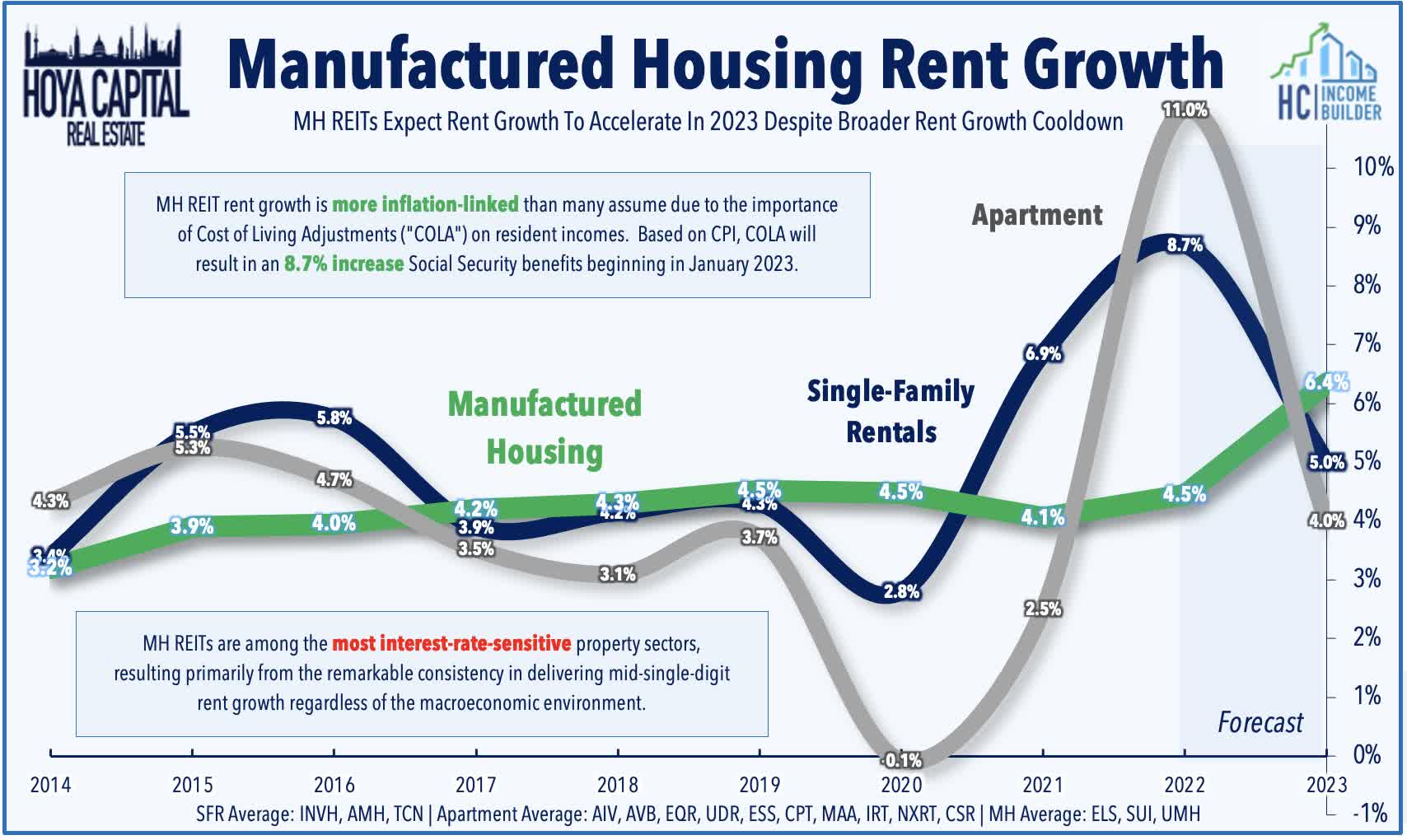

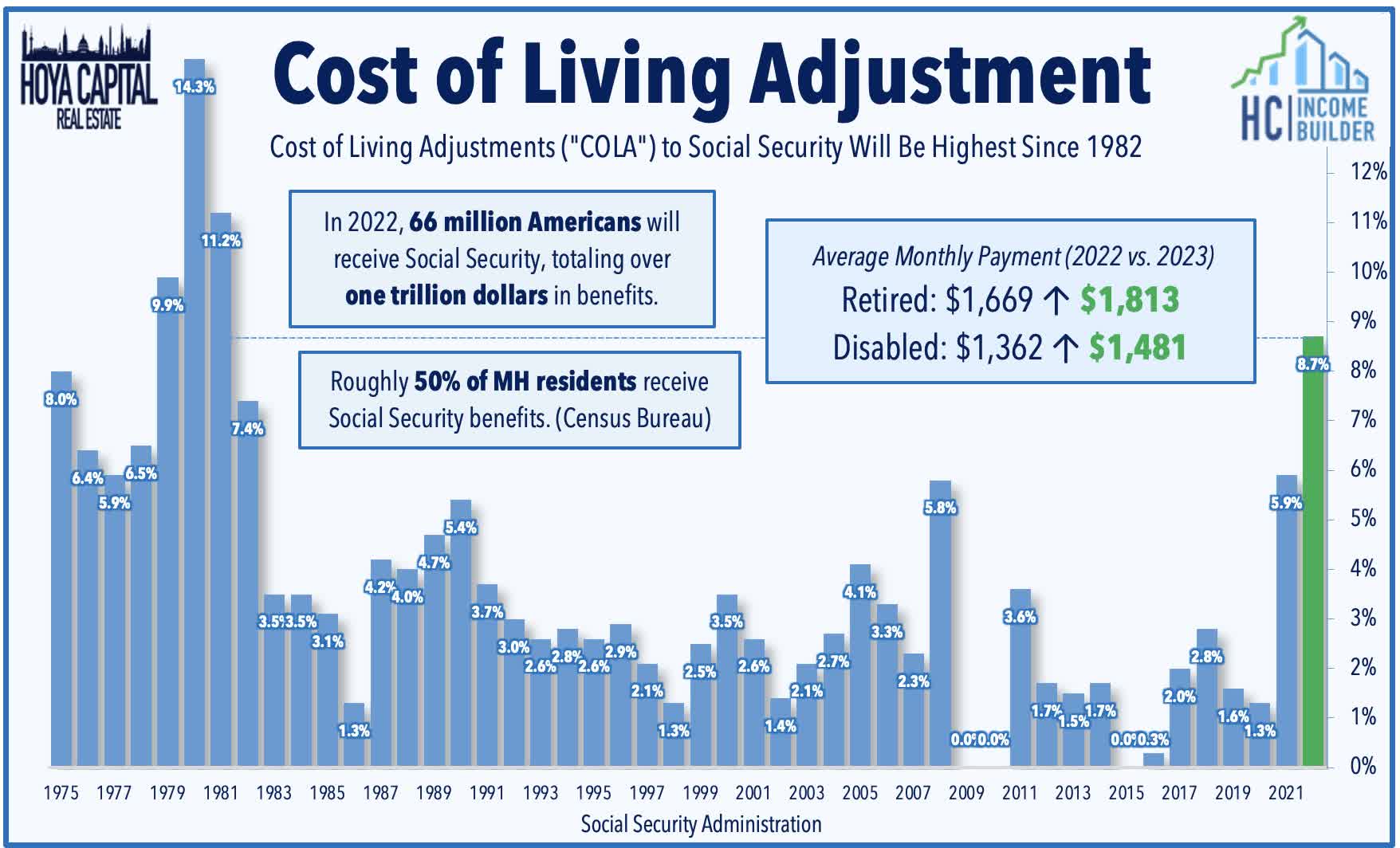

Manufactured Housing : There's less uncertainty around the MH REIT outlook after both Equity LifeStyle ( ELS ) and Sun Communities ( SUI ) provided a preliminary 2023 outlook last quarter. These REITs expect to send out record-high rent increases for the 2023 renewal season in the range of 6-8%, consistent with our expectation that MH REITs will leverage the record-setting cost-of-living adjustment ((COLA)), which resulted in a nearly 9% increase in benefits to a significant percentage of MH REIT residents. ELS reported strong results on Monday afternoon with full-year guidance calling for FFO growth of 6.0% - an acceleration from the 5.9% growth it achieved in 2022 - while boosting its dividend by 9.1% to $0.15/share. Notably, ELS upwardly revised its guidance for MH revenue growth which is now expected to rise 6.5% this year, up from the prior outlook of 6.4%. We'll be focused on the FFO outlook for SUI and UMH and think that another high-single-digit growth rate in 2023 is achievable.

{kind=link}

Tech and Industrial REITs Earnings Preview

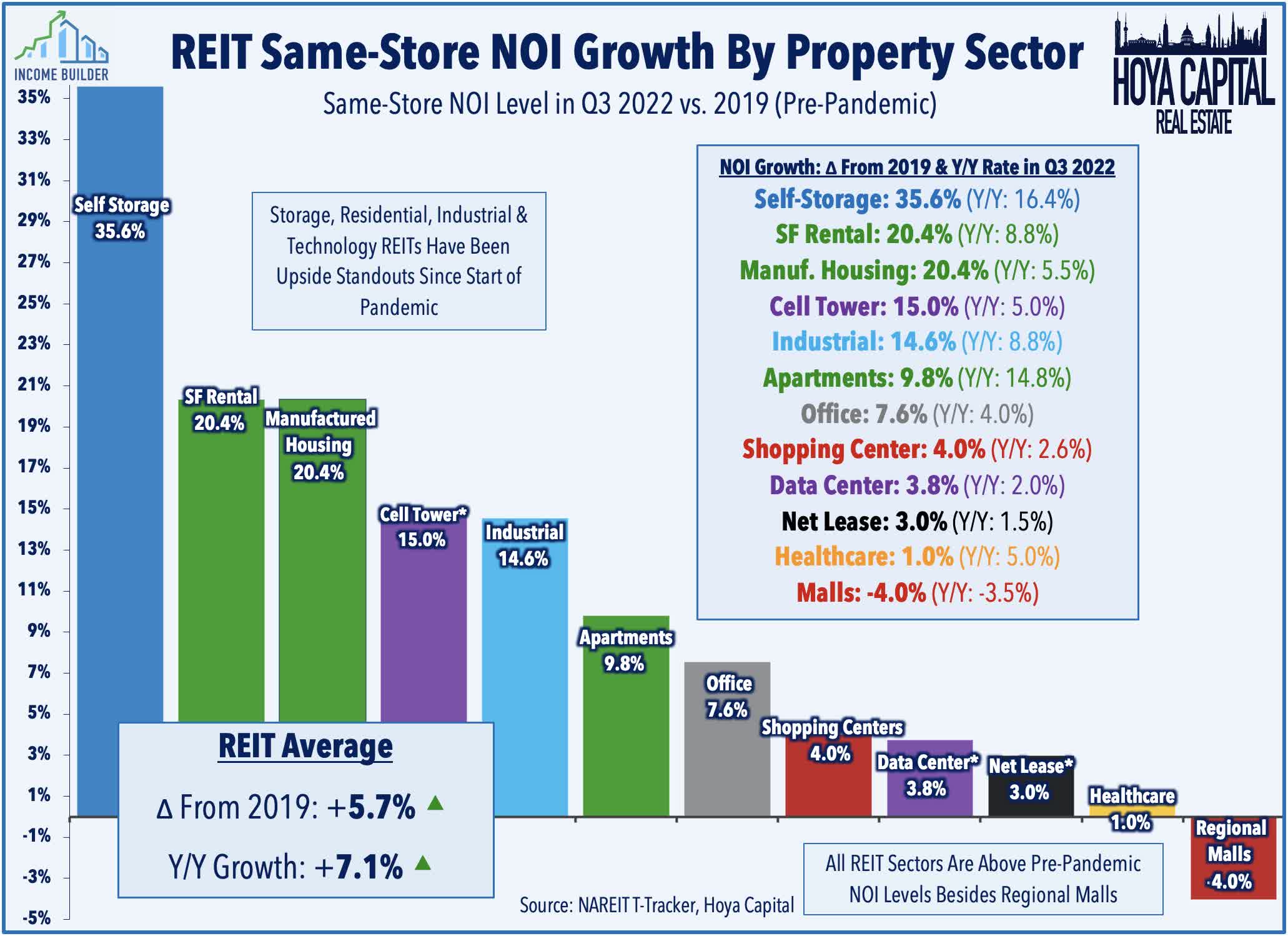

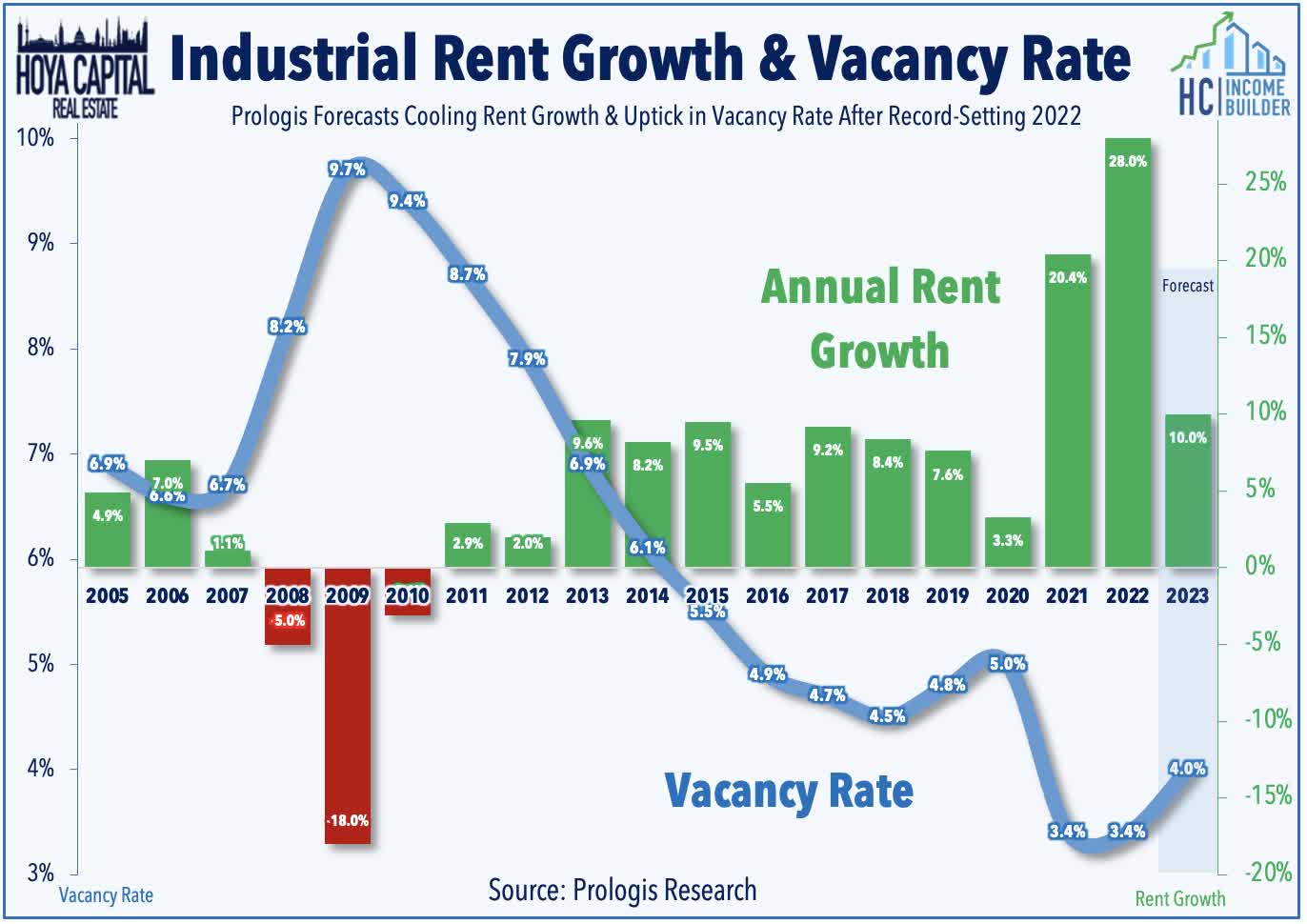

Industrial : Industrial REITs - which were in the basement of the REIT sector for much last year - have regained some ground over the past several months as these REITs continue to push back on concerns over logistics softening demand. Prologis ( PLD ) kicked off REIT earnings season last week with very strong results, reporting that its full-year Core FFO rose 11.1% in 2022 and provided initial 2023 guidance calling for Core FFO growth of 9.5%. Prologis recorded net effective rent growth of 50.6% in Q4 (down slightly from record-highs of 59.7% in Q3) and cash rent growth of 32.4% (also down from record-highs of 38.5% in Q3). Industrial REITs aren't entirely immune from post-pandemic demand normalization, but supply remained inherently capped by land constraints. Rent growth will naturally moderate toward "trend" levels, but fundamentals are forecast to remain healthy absent a demand shock.

{kind=link}

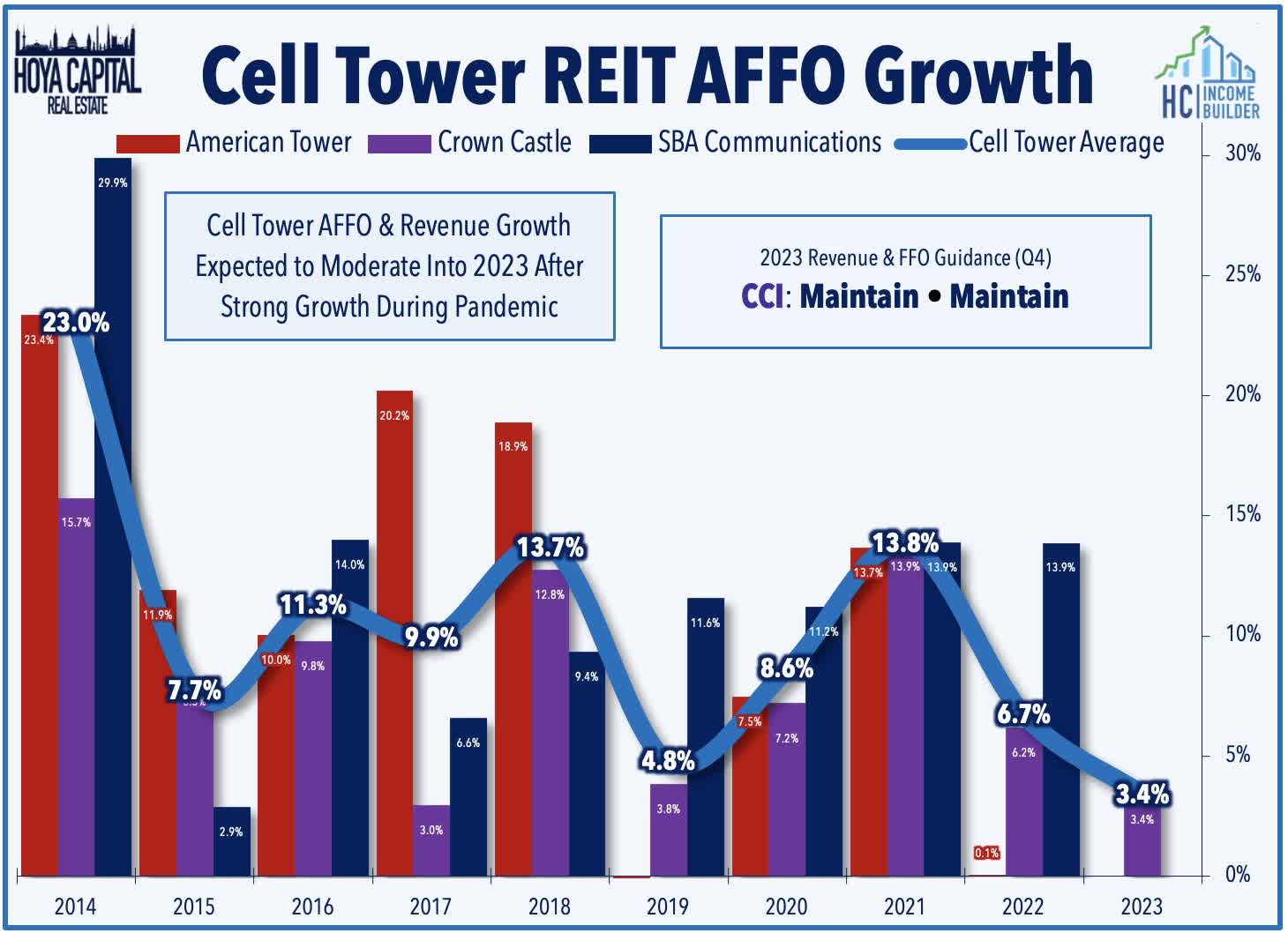

Cell Towers : Similar to their industrial REIT peers, Cell Tower REITs uncharacteristically lagged in 2022, weighed down by tech-related weakness and concerns of disruptive threats to the long-term competitive positioning. Crown Castle ( CCI ) reported decent fourth-quarter results last week, recording full-year revenue growth of 10% and FFO growth of 6.2% - each slightly above the midpoint of its most recent guidance while maintaining its outlook for full-year 2023 which calls for revenue growth of 3.0% and FFO growth of 3.4% as near-term headwinds from higher interest rates and the effects of the Sprint churn offset projected organic revenue growth of 6.8% (4.2% excluding Sprint). CCI noted that this 4.2% organic growth consists of 5% growth in towers, 8% growth in small cells, and flat revenue in fiber solutions. We're focused on the initial full-year guidance from American Tower ( AMT ) and SBA Communications ( SBAC ) and on commentary about potential M&A given recent speculation regarding Spanish telecom operator Cellnex.

{kind=link}

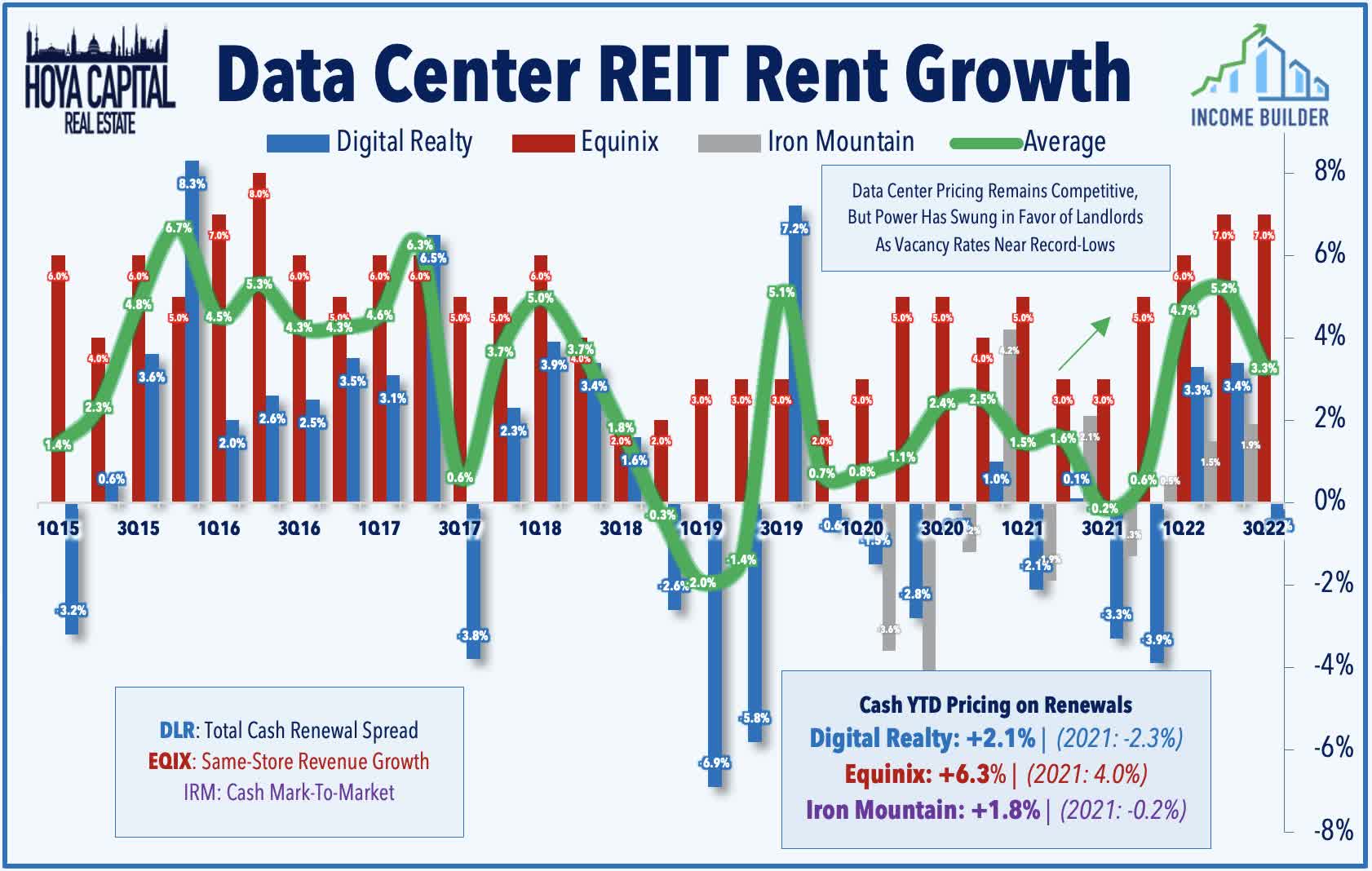

Data Center : Data Center REITs have been one of the best-performing property sectors over the past quarter as property-level fundamentals have strengthened despite an expected downshift in cloud-related spending. Ironically, just as Data Center REITs became a trendy “short” idea centered on a thesis of weak pricing power and competition from hyperscalers, rental rate meaningfully improved in the back-half of 2022. While property-level fundamentals are not as compelling as the cell tower space where REITs have effectively corned the market, the concentration of data center REITs shouldn’t be discounted either as Equinix ( EQIX ) and Digital Realty ( DLR ) have built relatively dominant platforms. We'll again be watching renewal pricing trends and leasing volumes closely this quarter.

{kind=link}

Retail REITs Earnings Preview

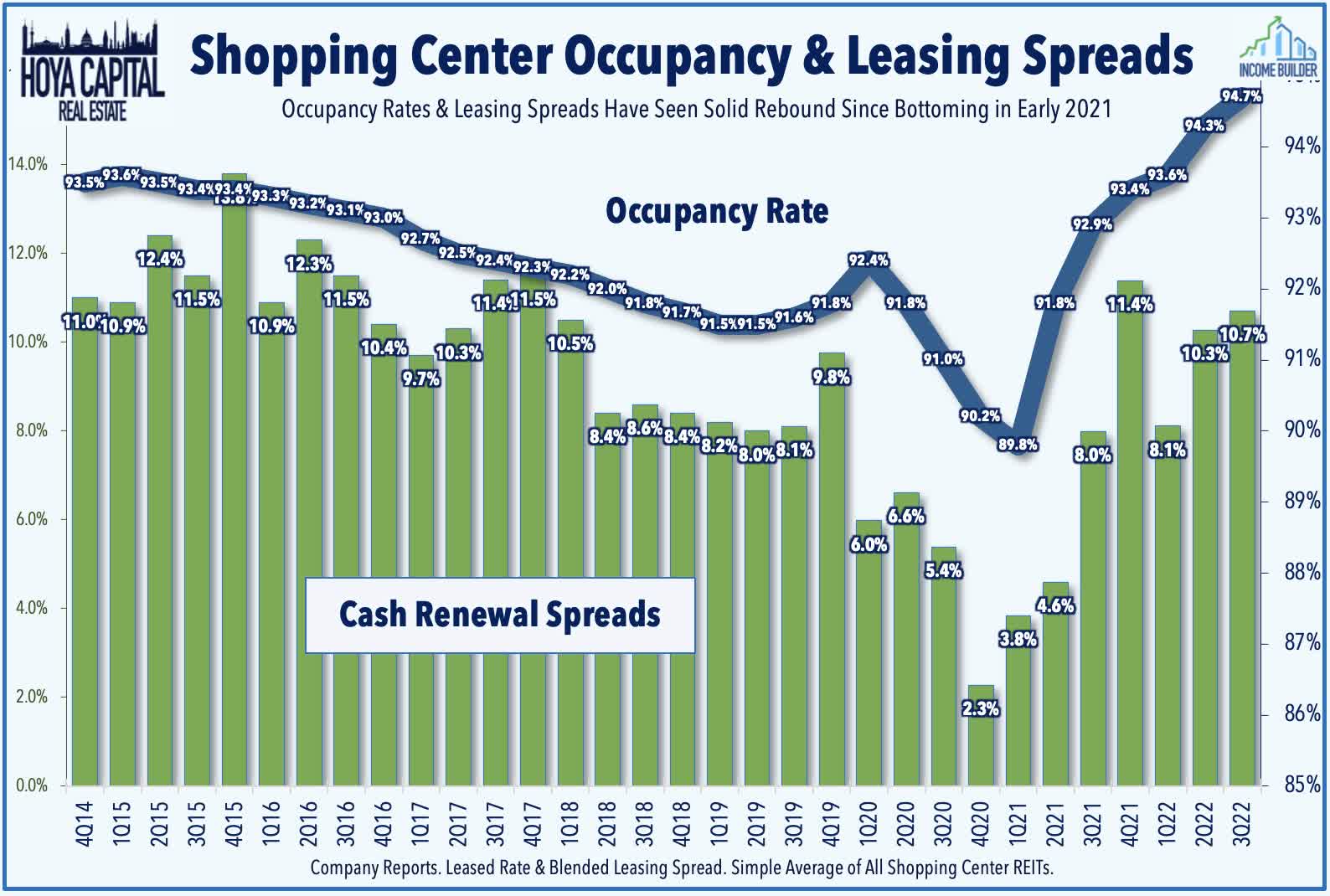

Strip Centers : Flying under-the-radar amid recession concerns and the looming shadow cast by their persistently-troubled mall peers, the outlook for Strip Center REITs has improved considerably over the past year. The combination of near-zero new development and positive net absorption since early 2021 has driven occupancy rates to record-highs and allowed Strip Center REITs to enjoy some long-awaited pricing power. Favorable supply/demand fundamentals have translated into impressive double-digit rent growth spreads throughout 2022 and the best earnings “beat rate” of any property sector during the year. We’ve been buyers this year and currently see strip center REITs as some of our favorite names in the "sweet spot" of value and growth with 4-6% dividend yields - while also being fundamentally well-positioned for a variety of potential economic scenarios. We'll be focused again on leasing spreads and occupancy rates which have been impressive of late.

{kind=link}

Malls : The troubled mall REIT sector benefited from similar favorable store opening trends in 2022, but the recent bankruptcy concerns for Bed Bath & Beyond ( BBBY ) renewed concerns that the tighter monetary environment may push other troubled retailers over the edge. A microcosm of broader retail trends, mall sector dynamics remain a story of "haves and have-not" and while lower-tier mall REITs remain in a seemingly endless loop of delistings and bankruptcies, the upper-tier malls are no longer teetering dangerously on the edge. We're focused on same-store occupancy rates this earnings season - which remained relatively soft last quarter despite improving NOI and FFO trends - and we want to see rental rates stabilize before we can officially call the bottom to the decade-long downward pressure on FFO.

{kind=link}

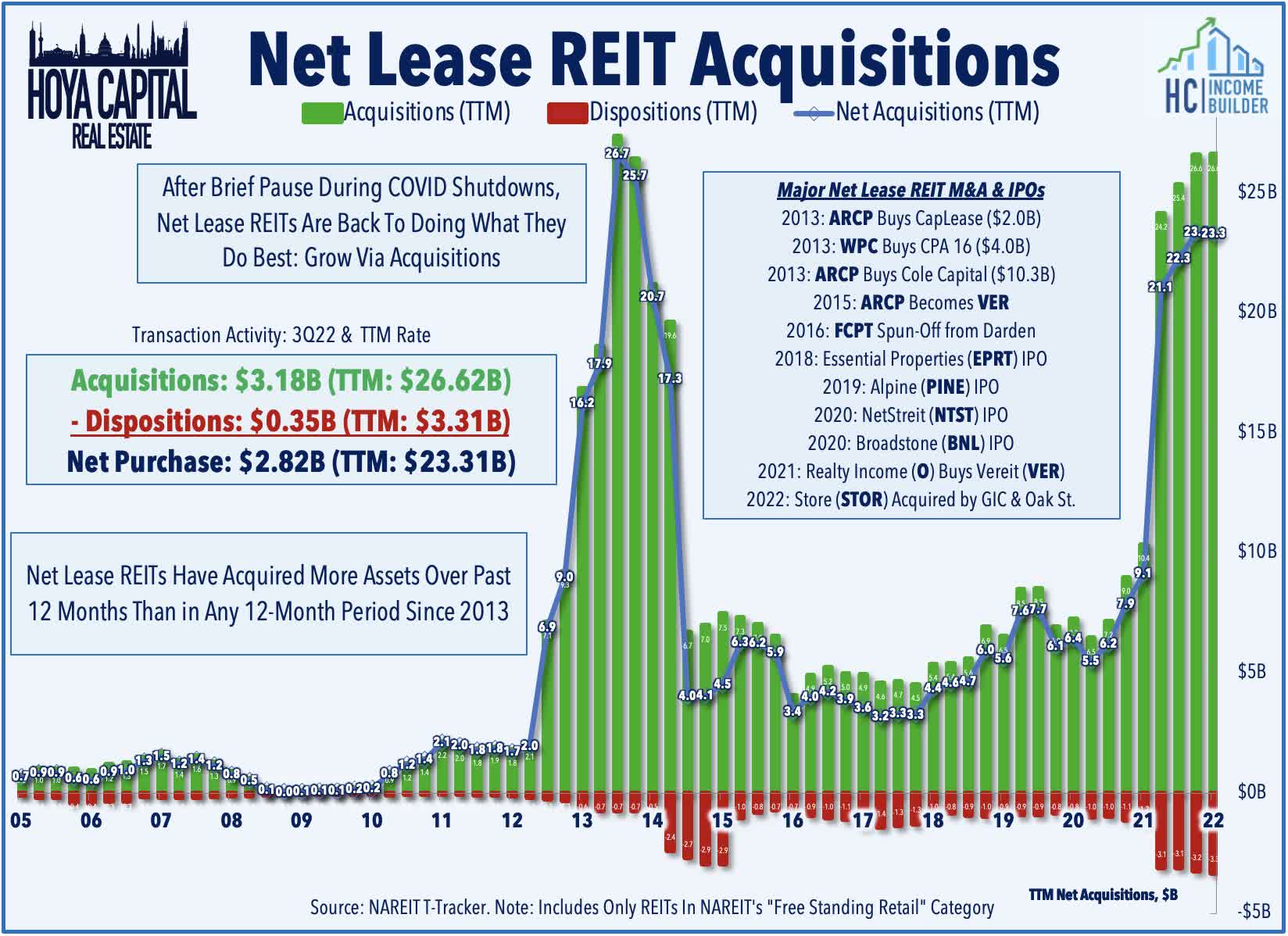

Net Lease : Curiously, net lease executives, investors, and asset owners have seemingly never bought into the idea of a "new normal" of sustained higher interest rates and have plowed ahead with acquisitions. Last quarter, net lease REITs reported that acquisition cap rates expanded only modestly - roughly 50-100 basis points - during which time we’ve seen benchmark rates climb by 250-300 basis points, so we're listening carefully for updates on how this dynamic has changed in the final months of the year and how these REITs see their cost of capital in relation to acquisition cap rates. We see the best value in REITs that focus on “middle-market” tenants and the middle-tier of cap rates where you'll typically see more inflation-hedging lease structures and initial yields that grant more breathing room for higher financing costs.

{kind=link}

Hotel & Casino REIT Earnings Preview

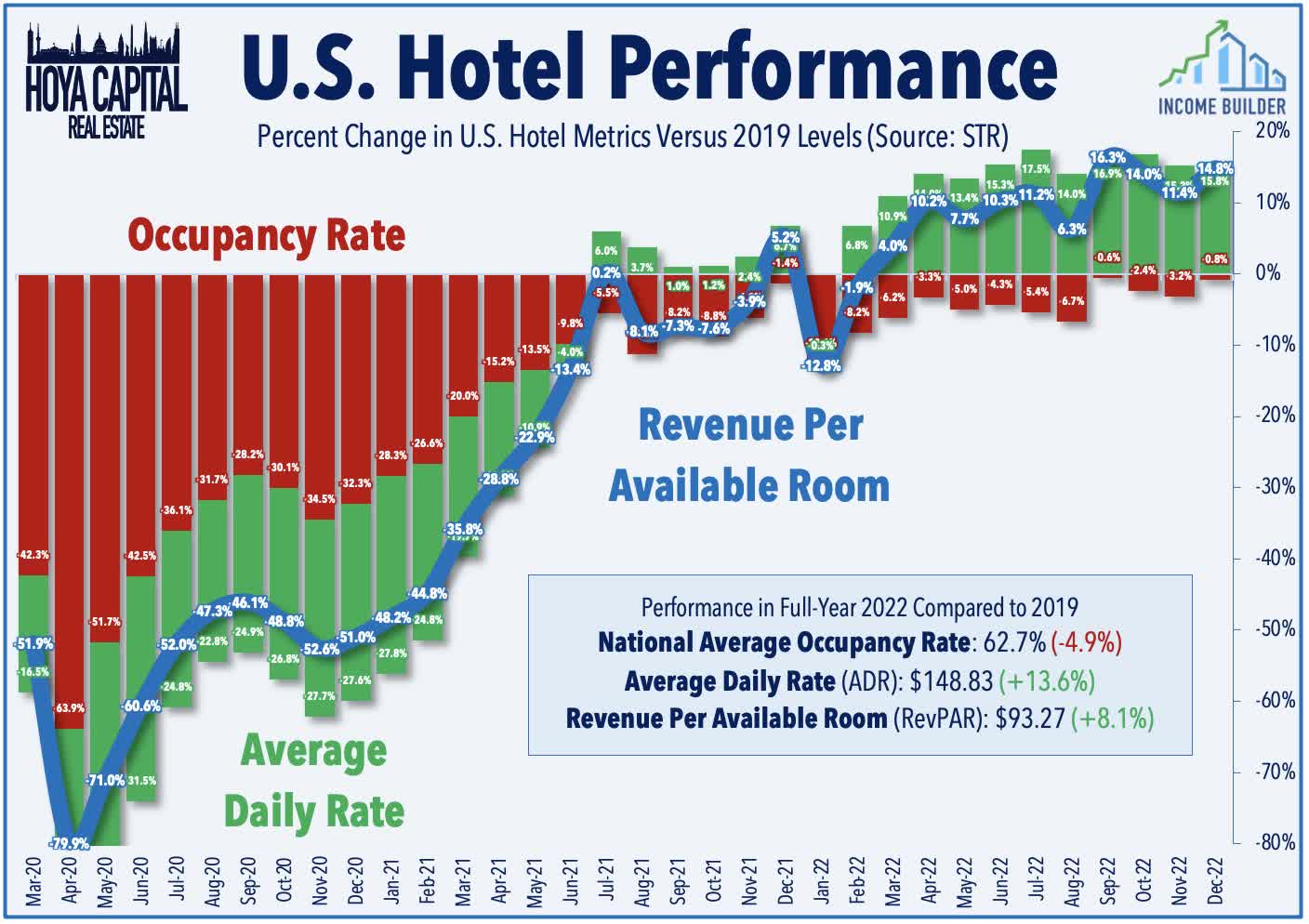

Hotels : Despite lingering recession concerns and recent travel disruptions, Hotel REITs have been among the better-performing sectors over the past year, buoyed by steady post-pandemic operating improvement and a much-anticipated return of dividends. Several years of pent-up leisure demand helped to offset a sluggish business and group travel recovery - but we foresee a pickup in business travel even without a corresponding recovery in office utilization rates. The final months of 2022 saw a mild softening in demand - worsened by holiday travel nightmares - but recent high-frequency data and REIT updates show surprisingly solid momentum in early 2023. With pent-up leisure demand carrying the recovery over the past year, further progress rests largely with the other two major demand segments - group and business travel, so we're focused on commentary on recent demand trends. We're also hoping to see additional hotel REITs provide full-year guidance after several years of limited disclosures amid COVID-related uncertainty.

{kind=link}

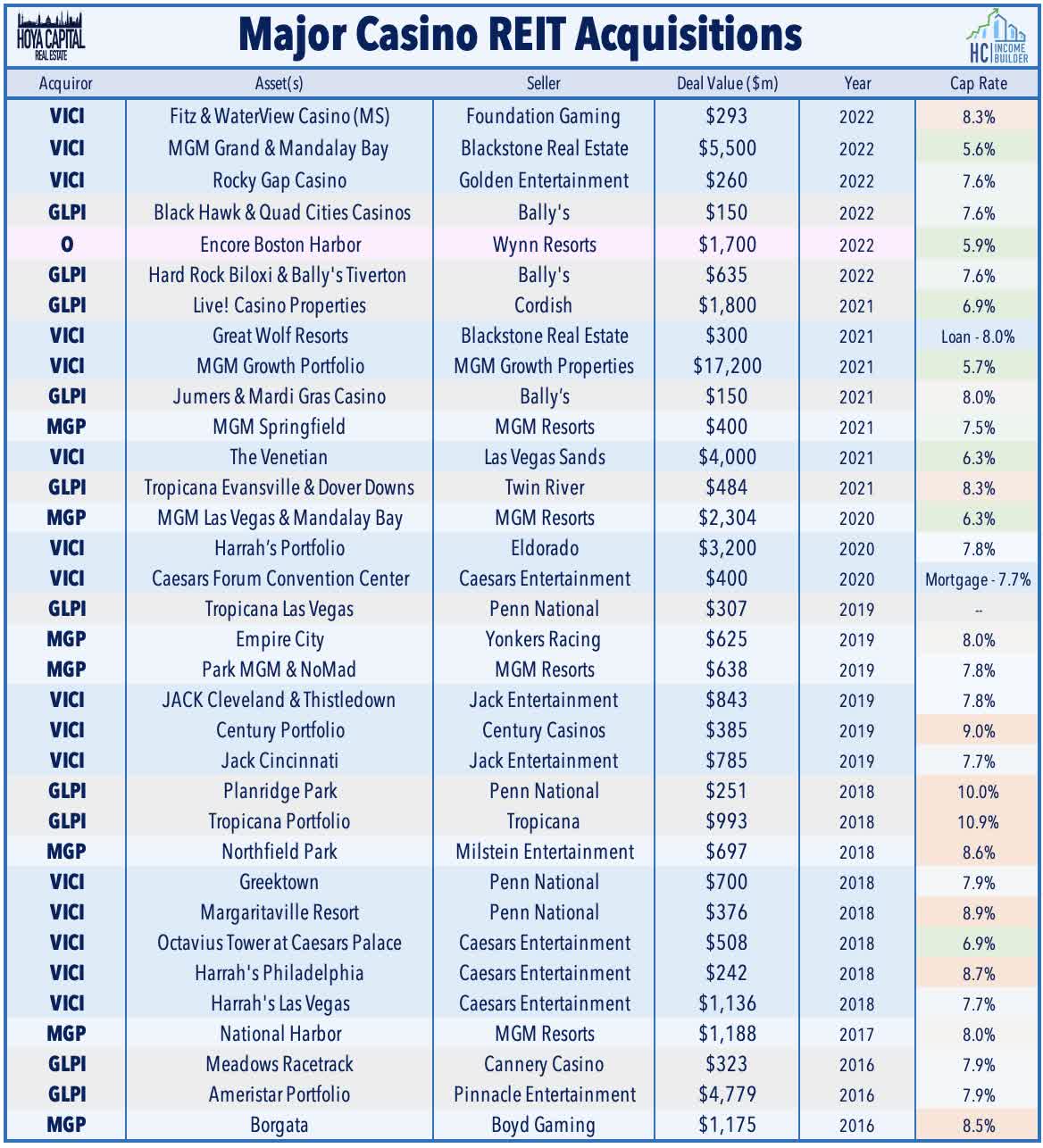

Casinos : Las Vegas is one of the hotel markets that continue to see relatively strong demand and has been one of the first markets to see a meaningful uptick in group and convention demand. Casino REITs were the lone property sector in positive-territory this year, benefiting from this notable strength in Las Vegas travel demand along with their attractive “inflation-hedging” lease structure and broader institutional investor acceptance. M&A will be the focus of earnings season given that Casino REITs have been as active as any REIT sector in recent months including VICI Properties' ( VICI ) recent $201M deal to acquire four casinos in Canada from PURE Canadian Gaming, which followed a $350M deal to finance the construction of Fontainebleau Las Vegas, a $300M deal to acquire two hotel-and-casino properties in Mississippi, and its $5.5B deal to acquire the MGM Grand and Mandalay Bay from Blackstone.

{kind=link}

Office & Healthcare REIT Earnings Preview

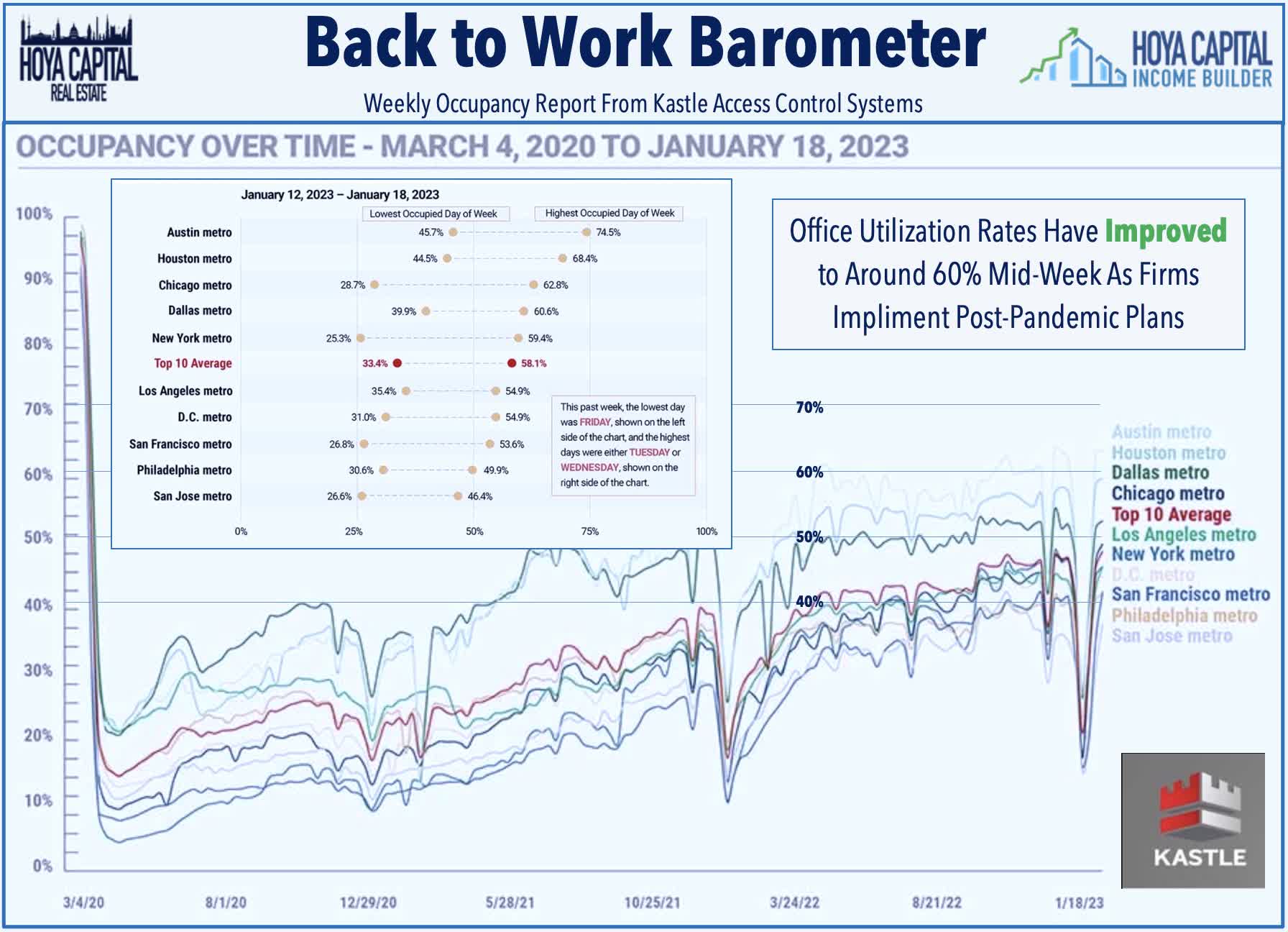

Office : The "Return to the Office" has been slow, to say the least. Nearly three years into the pandemic, data from Kastle Systems still shows that office utilization rates remain 40-60% below pre-pandemic levels and have trended more-or-less sideways since late 2021. Office leasing demand - and earnings results from these office REITs - were surprisingly resilient for much of 2022, however, particularly for REITs focused on business-friendly Sunbelt regions and specialty lab space. Investors remain skeptical over how long companies will continue to pay full price for half-empty office space. Utilization rates remain far higher in Sunbelt markets with shorter commutes, and so long as labor markets remain tight and employees have the negotiating power, it'll be tough to pull reluctant workers back into the office in coastal markets. Leasing velocity will be closely watched this quarter and we're interested in updated expectations of what exactly "normalization" looks like for each REIT.

{kind=link}

Healthcare : The recovery for many healthcare REITs - notably senior housing, skilled nursing, and hospital owners - has been similarly sluggish following their pandemic plunge. Many of the pre-pandemic operator-related issues that weighed on these REITs in the late 2010s have returned as COVID relief funds have waned. Senior Housing REITs Welltower ( WELL ) and Ventas ( VTR ) have been among the better performers over the past quarter, however, lifted by NIC data showing that senior housing occupancy increased for a sixth-straight quarter to 83% - up 5.2% from the pandemic occupancy low of 77.8% in 2Q21 - but still below the pre-pandemic levels of roughly 90%. Despite the reduced occupancy levels, SH operators have exhibited strong pricing power with annual rent growth climbing to 4.9% in Q4 - the largest increase on record - and we expect the nearly 9% cost-of-living adjustment (COLA) to Social Security benefits to further support SH rent growth in 2023.

{kind=link}

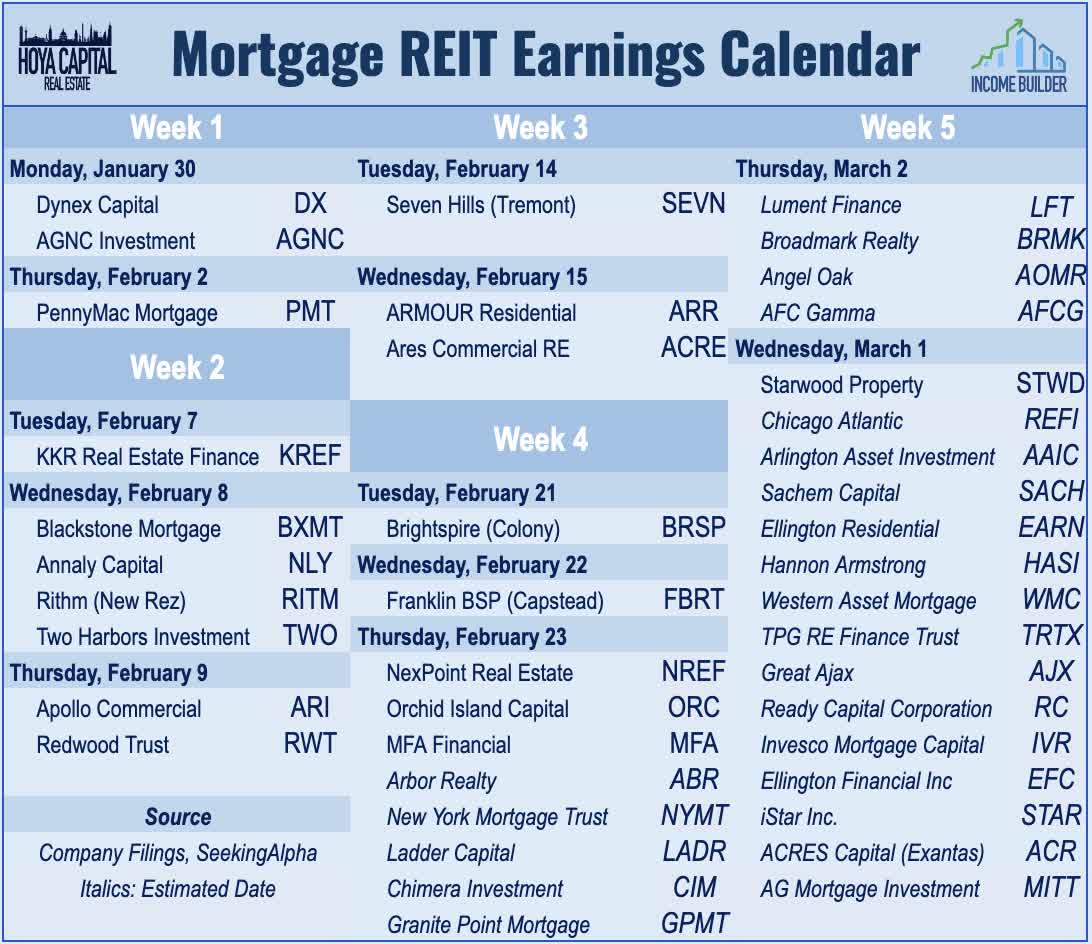

Mortgage REITs Earnings Preview

Mortgage REITs have posted an impressive rebound from their lows in mid-October with the iShares Mortgage Real Estate Capped ETF ( REM ) gaining nearly 25% during this period. Residential mREITs have led the rebound, buoyed by a revived bid for residential mortgage-backed bonds as the iShares MBS ETF ( MBB ) - an unlevered index of residential mortgage-backed bonds - has gained over 6% since the start of October. Investors expect mREITs to report a mid-single-digit rebound in Book Value Per Share ("BVPS"), on average, following several quarters of punishing declines. Through Monday afternoon, we've seen two mREITs report results: AGNC Investment ( AGNC ) reported that its BVPS jumped 8.4% in Q4 to $9.84/share while Dynex Capital ( DX ) reported a 4% increase in its BVPS to $14.73. In Mortgage REITs: High Yields Are Fine, For Now , we noted that despite paying average dividend yields in the mid-teens, the majority of mREITs have been able to cover their dividends, but we flagged a handful of mREITs with payout ratios above 100% of EPS.

{kind=link}

Key Takeaways: Real Estate Earnings Preview

Real estate earnings season kicks into gear this week. REITs enter earnings season with some positive momentum amid the recent moderation in interest rates and hopes of a 'softish' economic landing following a punishing year of stock price performance. How REITs are responding to this higher rate environment– both on the acquisitions and the financing side- will be closely watched. REITs hunkered down in 2022, but opportunities are becoming more plentiful. The non-traded REIT sector may be an area "ripe for the picking" if investor redemptions continue and we foresee many of the recently-privatized portfolios eventually coming back into public markets. Full-year FFO guidance will be the metric most closely-watched - especially in the residential, retail, and office sectors given the wide range of analyst expectations.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

REIT Earnings Preview: The New Normal