VICI - REIT Income For Life

2023-08-23 07:00:00 ET

Summary

- We emphasize the value of reading and considering different perspectives, even if they don't align with one's own beliefs.

- This article highlights comments from readers expressing concerns about the state of the US economy and consumer debt.

- We recommend considering real estate investment trusts such as Realty Income, Mid-America Apartment Communities, Agree Realty, and VICI Properties for consistent dividend payments and potential long-term returns.

It’s always interesting reading article comments – both the ones you leave me here on Seeking Alpha as well as my private community.

It’s not just interesting because of the drama that often erupts. Though that can serve as its own form of fascination. But I’m much more talking about the insights I can glean from taking in other perspectives.

Agreements or disagreements, it doesn’t matter: It’s real people’s thoughts, feelings, and analysis on bold display. Which has immeasurable value.

For those of you who are used to rolling your eyes, gritting your teeth, or even turning red in the face as you yell at the screen while reading other people’s “thoughts, feelings, and analysis,” bear with me. Because I’m not saying they’re all right, polite, or intelligent.

Only that we weren’t created to thrive in bubbles.

When we’re surrounded by yes men (and women) who merely echo our own conclusions, there’s no room for growth. Or compassion. Or the truth – which, incidentally, is oftentimes somewhere between the extremes.

For instance, people who are financially comfortable could read all the articles about consumer spending, air travel trends, and stronger-than-expected GDP figures… and conclude that we’re never going to see a recession. And maybe we won’t see an official one any time soon.

Maybe it’s true that all that talk about “the most anticipated recession ever” was just plain wrong. But that doesn’t mean everything is economic rainbows and butterflies.

The comments prove as much.

A Personal Recession

Recently I read an article on Yahoo Finance as in the opening line as an off-the-cuff reference. But, truth be told, it’s one of the few major financial platforms that still invites comments.

So I’ll use one of its recent postings – “ The U.S. Consumer is Stronger Than Investors Think, Bank of America Says ” – to prove my point. It begins this way:

“The American consumer has surprised Wall Street throughout 2023, leading to unexpected levels of growth in the U.S. economy and forcing economists to push out their recession targets.

“Despite a ‘better-than-expected’ narrative, that resilience isn’t fully reflected in the market, Bank of America argued in a new note on Monday.”

This would have been from Tuesday, Aug. 15, for the record.

“After recently eliminating its call for a recession in 2024, BofA’s economics team expects consumer spending to rise 2.3% in 2023 (up from 2.1% previously) and 1.1% in 2024 (up from 0.1% previously).”

And, again, that may very well be. But there’s another perspective to consider, as evidenced by the following comments:

“Sure, that’s why credit card debt just hit $1 trillion. The U.S. consumer (is) just barely hanging on, and we are now paying 25% of net wages in taxes. The highest amount in U.S. history… The entire system is collapsing under the weight of debt.”

That response, from Richard, generated 35 likes, four dislikes, and four comments – at least three of them positive – at last check. (The fourth comment might have been sarcastic. It’s hard to tell.)

That’s a pretty indicative ratio right there. And it’s hardly isolated. All you need to do is keep scrolling down to see.

An Investment for Everyone

There was also this one from Dave, which generated 17 likes and two dislikes:

“When the price of everything we buy goes up by 10% to 50%, of course we are spending more. Getting less but spending more.”

And this one from Joe, with 23 likes and one dislike:

“(The) U.S. consumer is so broke and in enormous debt. If they lose their job for two weeks, the entire system is coming down again.”

I could go on, but I assume you get the point. I’d also say it’s safe to assume that some of you are in the same camp of thinking.

Others, I know, will ardently argue the opposite. And, again, that’s fine. Differing perspectives are welcome – even important.

Fortunately, what I’m about to write about applies to both sides of the aisle. It’s going to seem more appealing to the doom and gloom crowd at first glance, I know. But who can’t benefit from recurring income for life?

For those of you who feel as if the markets are headed higher, higher, and higher still from here, I’m ultimately in your camp – just in an “over time” kind of way. The markets always go ultimately up, after all…

Just with countless bumps, craters, and other consternations along the beaten path.

I’m also not suggesting you should put all your money in real estate investment trusts (REITs). In fact, please don’t put all your money in them. That lack of diversification would be foolish.

But so is ignoring REITs when they offer such consistent dividend payments throughout the year. You can consider them to be your insurance plan in case, for some reason, the stock market floor does fall through after all.

An insurance plan that pays you no matter what.

And for all of you doom and gloomers, who I’m hardly mocking, I see what you see too. There are plenty of disconcerting facts and figures out there. And inflation is still going up from already painful prices, just not as fast.

In which case, again, the following REITs look pretty reassuring.

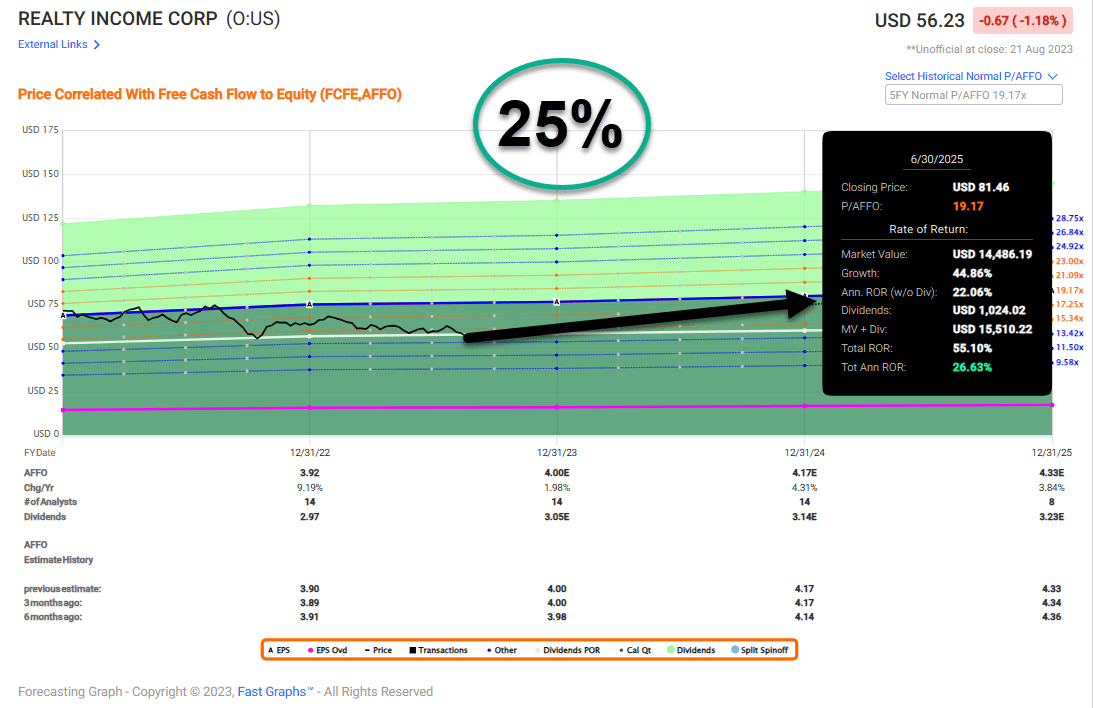

Realty Income (O)

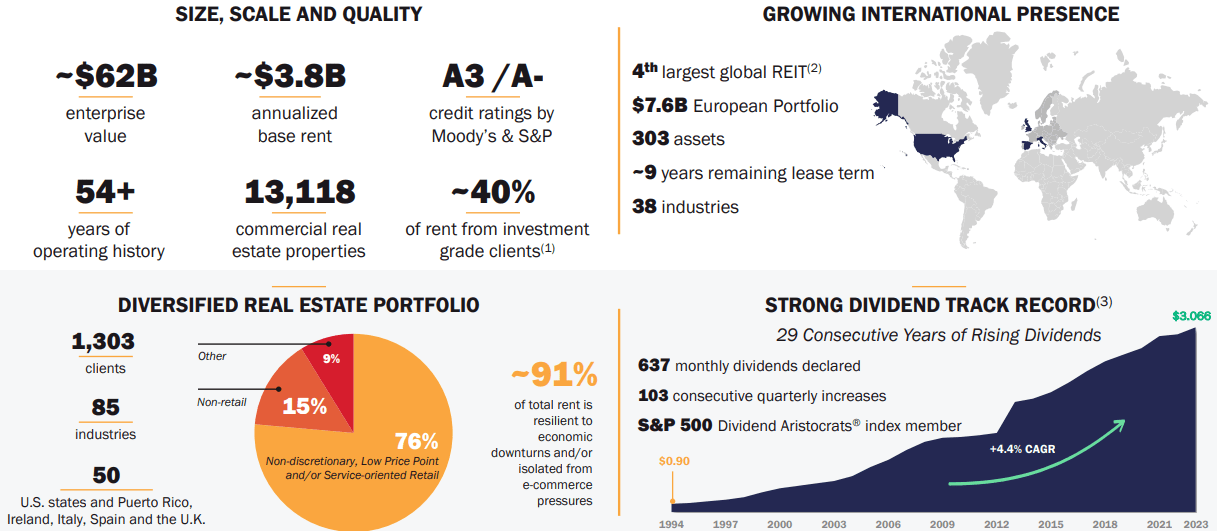

Realty Income is a real estate investment trust (“REIT”) that has been operating for over 54 years and has been publicly listed since 1994.

They have been one of the most consistent and dependable dividend payers with 638 consecutive monthly dividends declared since their formation and 121 dividend increases since 1994.

They're a member of the S&P 500 Dividend Aristocrats with a track record of 29 consecutive years of dividend increases, which is supported by the cash flow they receive from a portfolio of over 13,000 commercial properties that are leased on a triple-net basis.

Realty Income has properties located in 50 states within the U.S. and international properties located in the United Kingdom, Spain, Italy, and Ireland. In total, their properties are leased to 1,303 tenants operating in 85 industries with a weighted average remaining lease term of 9.6 years and a portfolio occupancy of 99.0%.

{kind=link}

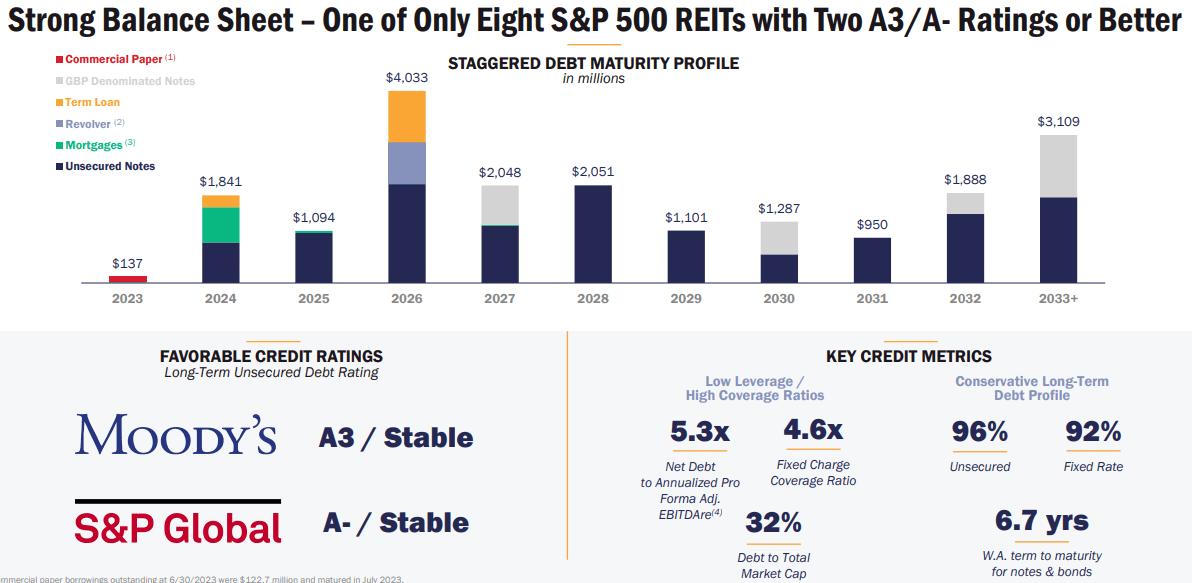

Realty Income is one of the few REITs that has an A- or better credit rating from S&P Global and is well positioned with approximately $3.5 billion of liquidity and minimal debt maturities in 2023.

They have a strong balance sheet with a net debt to pro forma adjusted EBITDA of 5.3x and a fixed charge coverage ratio of 4.6x. Their debt is 96% unsecured, 92% fixed rate, and their notes and bonds have a weighted average term to maturity of 6.7 years.

{kind=link}

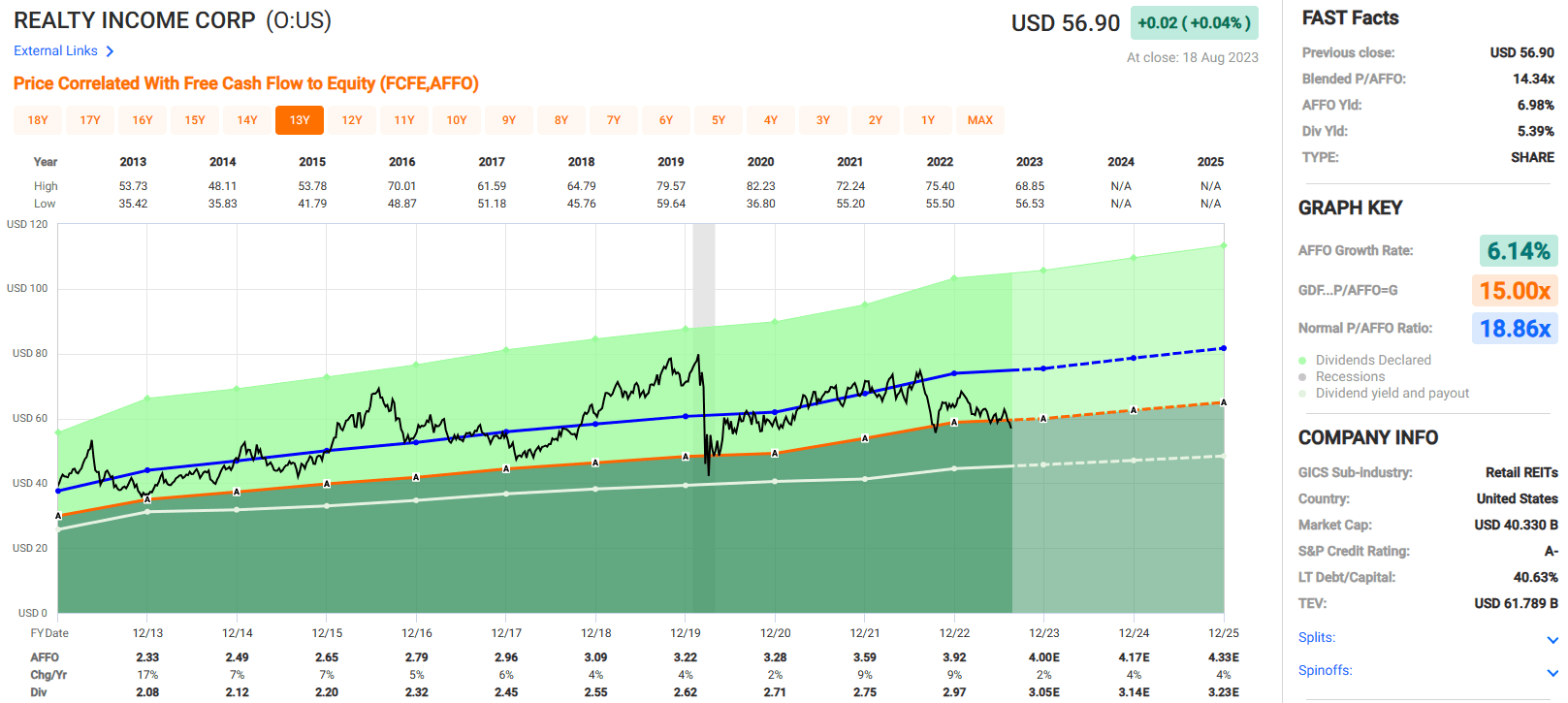

Realty Income has had positive adjusted funds from operations (“AFFO”) growth in 26 out of the last 27 years with a median AFFO per share growth rate of 5% since 1996.

Over the last 10 years they delivered an average AFFO growth rate of 6.14% and an average dividend growth rate of 5.76% and just recently announced their 103rd consecutive quarterly dividend increase in June.

They pay a 5.39% dividend yield that is well covered with an AFFO payout ratio of 75.69% and are trading at a P/AFFO of 14.34x which is a large discount to their normal AFFO multiple of 18.86x.

We rate Realty Income a Buy.

{kind=link}

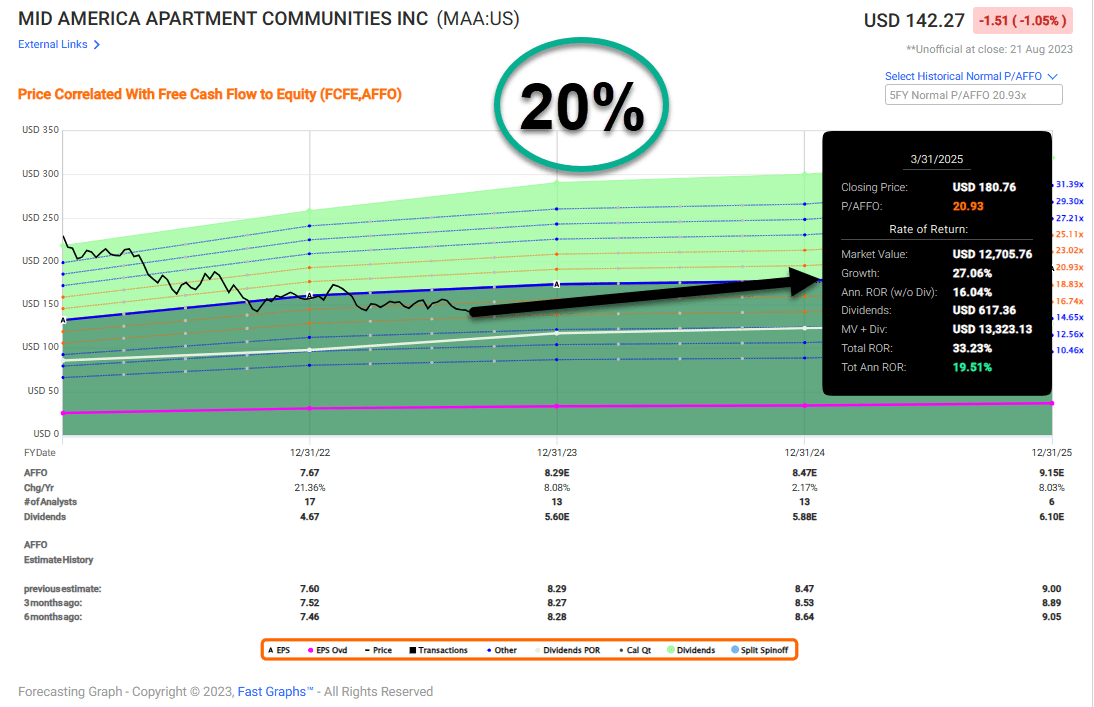

Mid-America Apartment Communities (MAA)

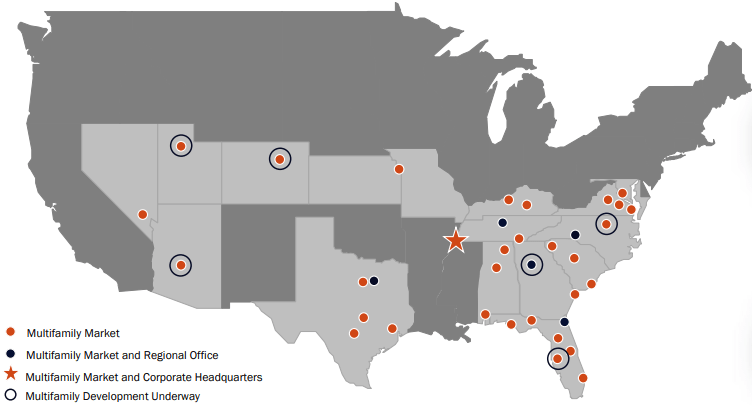

Mid-America Apartment Communities is a sunbelt focused multifamily REIT that owns, acquires, develops, and manages apartment communities with a large presence in the Southeast, Southwest, and Mid-Atlantic regions of the U.S.

As a percentage of their net operating income (“NOI”), the top five markets are Atlanta at 12.6%, Dallas at 9.7%, Tampa at 6.9%, Orlando at 6.5%, and Austin at 6.4%.

Their properties are well diversified by asset class with 40% of their portfolio rated class A or A+, 52% rated class B+ or A-, and 8% rated class B- or B.

Similarly, they're well diversified by apartment style with 63% of their portfolio consisting of garden style apartments (three stories or less), 33% consisting of mid-rise apartments (four to nine stories) and 4% consisting of high-rise apartments (over 10 stories).

MAA owns or has an ownership interest in 101,986 apartment units that are located across 16 states and Washington, D.C., and reported average same-store physical occupancy of 95.5% during the second quarter of 2023.

{kind=link}

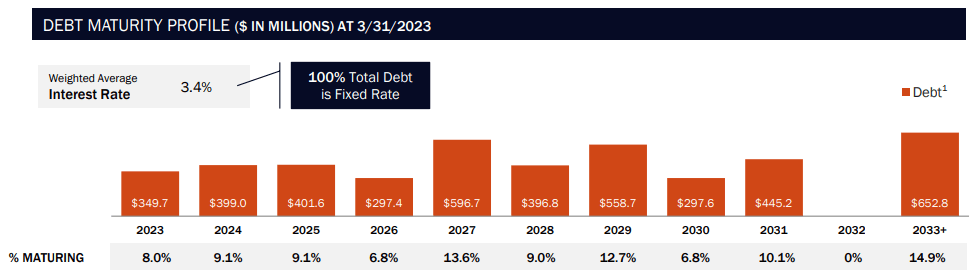

MAA is investment-grade with an A- credit rating and has excellent debt metrics including a net debt to adjusted EBITDAre ratio of 3.41x and an EBITDA to interest expense ratio of 8.23x.

Their debt is 100% fixed rate with a weighted average interest rate of 3.4% and a weighted average maturity of 7.5 years. MAA has a well staggered maturity schedule and manageable near-term maturities with $349.7 million of debt maturities in 2023 and $1.4 billion of combined cash and availability under their revolving credit facility as of the end of the second quarter.

{kind=link}

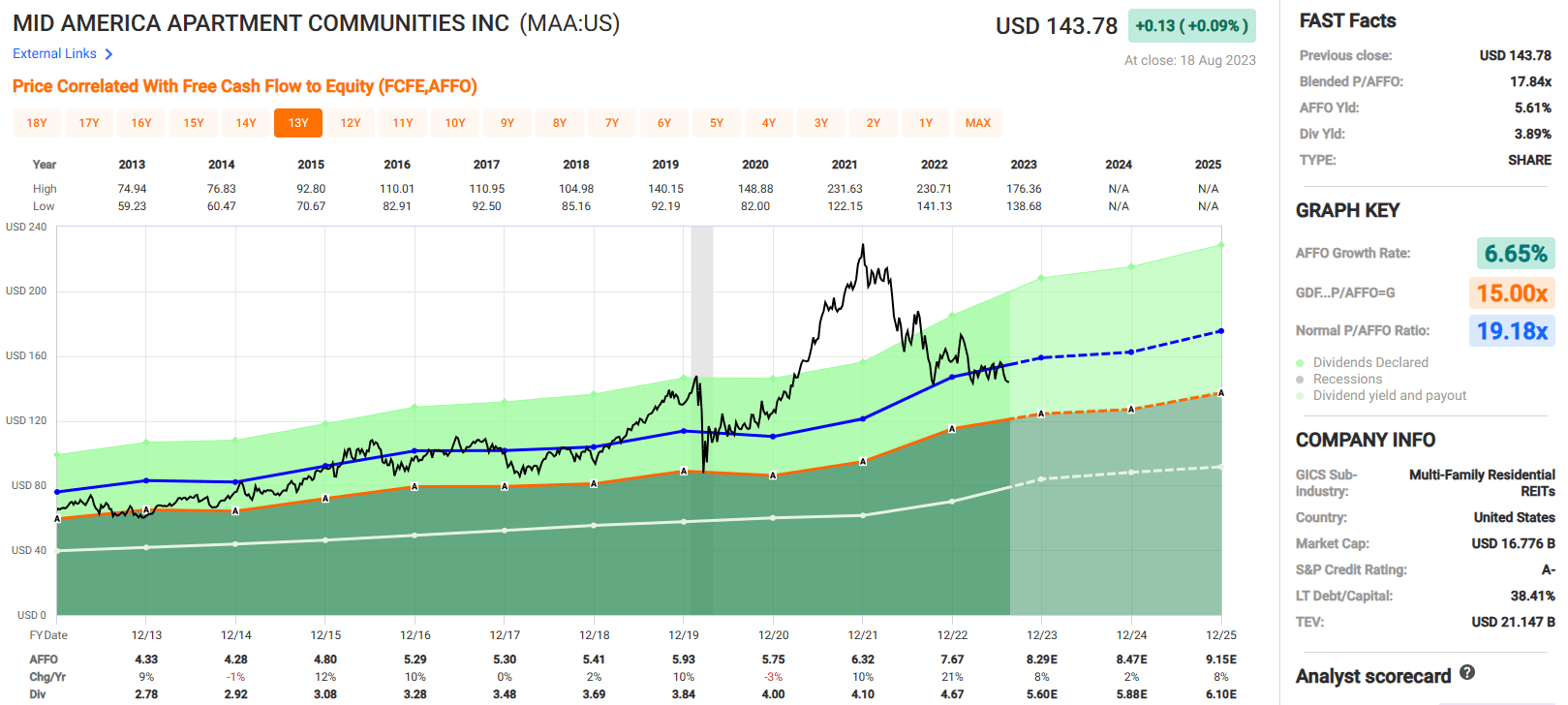

MAA has been a publicly traded company for 29 years and has paid 118 consecutive quarterly dividends over that time with no cuts or suspensions.

Over the last 10 years MAA has had an average AFFO growth rate of 6.65% and an average dividend growth rate of 5.92%. Analysts expect AFFO per share to increase by 8% in 2023, by 2% in 2024, and by 8% in 2025.

Currently MAA pays a 3.89% dividend yield that is very secure with an AFFO payout ratio of 60.95% and trades at a P/AFFO of 17.84x, which is a discount compared to their normal AFFO multiple of 19.18x.

We rate Mid-America Apartment Communities a Buy.

{kind=link}

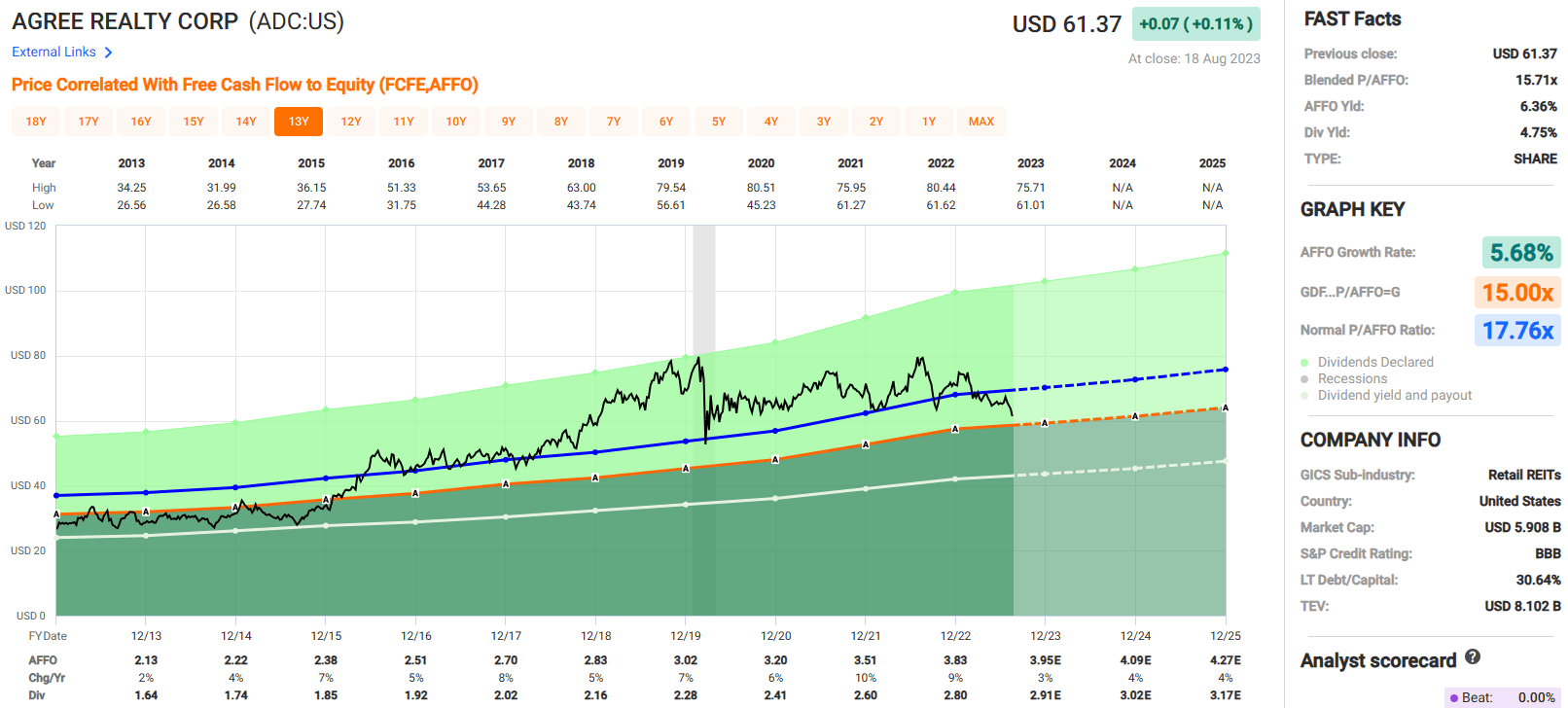

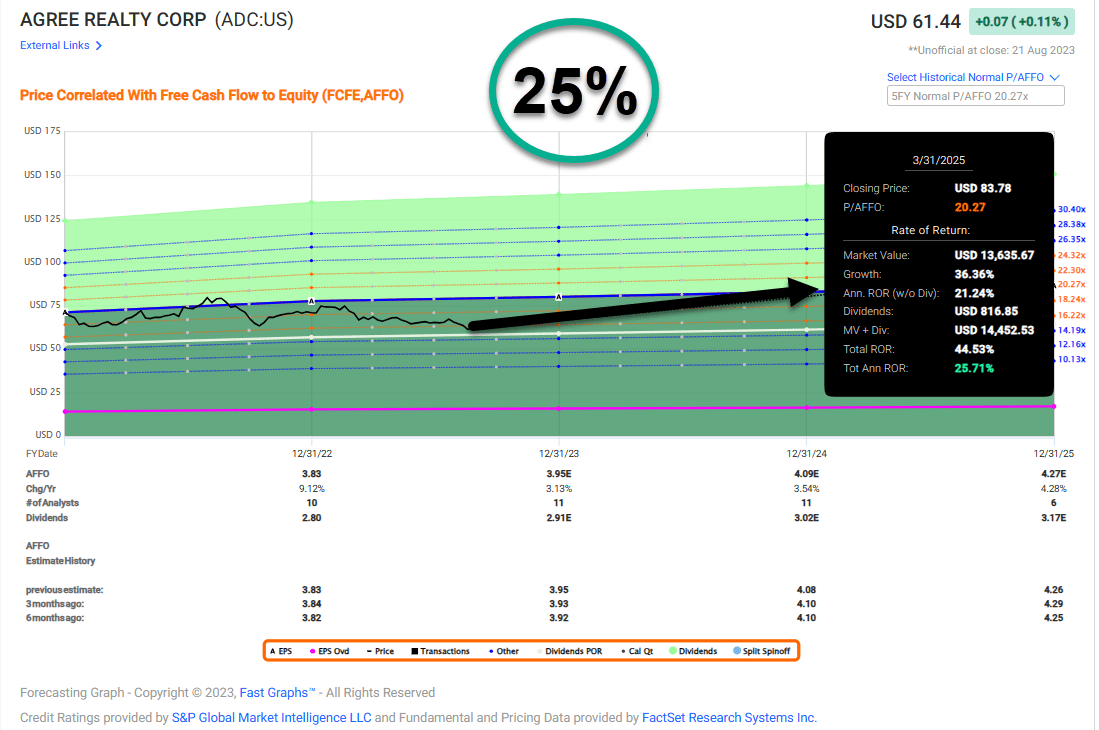

Agree Realty (ADC)

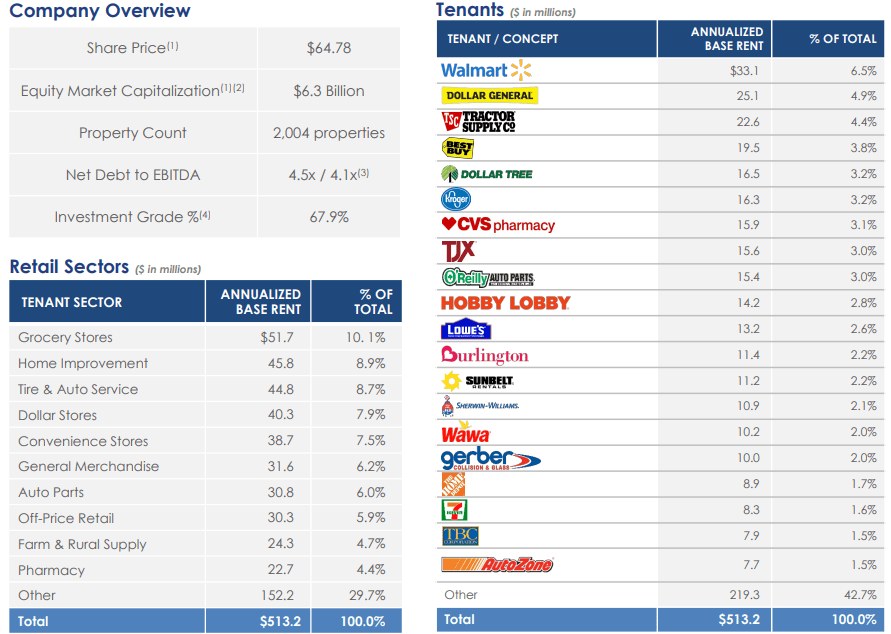

Agree Realty is a REIT that specializes in acquiring and developing commercial properties that are net leased to retail tenants. ADC owns and manages a portfolio of 2,004 properties that are located across 49 states.

Their portfolio is 99.7% leased with a weighted average remaining lease term of roughly 8.6 years and in total their properties contain roughly 41.7 million gross leasable square feet.

One thing that distinguishes ADC from many of its net lease peers is the quality of their tenants. Walmart, Dollar General, Tractor Supply, Best Buy, and Dollar Tree make up their top five tenants and approximately 67.9% of their annualized base rent (“ABR”) was derived from investment-grade retail tenants.

Agree Realty targets national and super regional retailers that operate in industries that are resistant to e-commerce.

As percentage of their ABR their top retail sectors include grocery stores at 10.1%, home improvement at 8.9%, auto service at 8.7%, dollar stores at 7.9%, and convenience stores at 7.5%.

{kind=link}

ADC has an investment-grade BBB credit rating and a strong balance sheet with a net debt to EBITDA of 4.5x, a long-term debt to capital ratio of 30.64%, and a fixed charge coverage ratio of 5.1x.

Additionally, 100% of their debt is fixed rate and they have approximately $1.3 billion of total liquidity with minimal maturities in 2023 and no significant maturities until 2028.

{kind=link}

Agree Realty has consistently paid dividends to their shareholders since 1994. They paid quarterly dividends for 107 consecutive quarters from 1994 to 2020 before moving to a monthly dividend schedule in 2021 and have paid 30 consecutive monthly dividends since the change.

Since 2013 they have delivered an average AFFO growth rate of 5.68% and an average dividend growth rate of 5.79%. ADC currently pays a 4.75% dividend yield that is well covered with an AFFO payout ratio of 73.24% and trades at a P/AFFO of 15.71x, which compares favorably to their normal AFFO multiple of 17.76x.

We rate Agree Realty a Buy.

{kind=link}

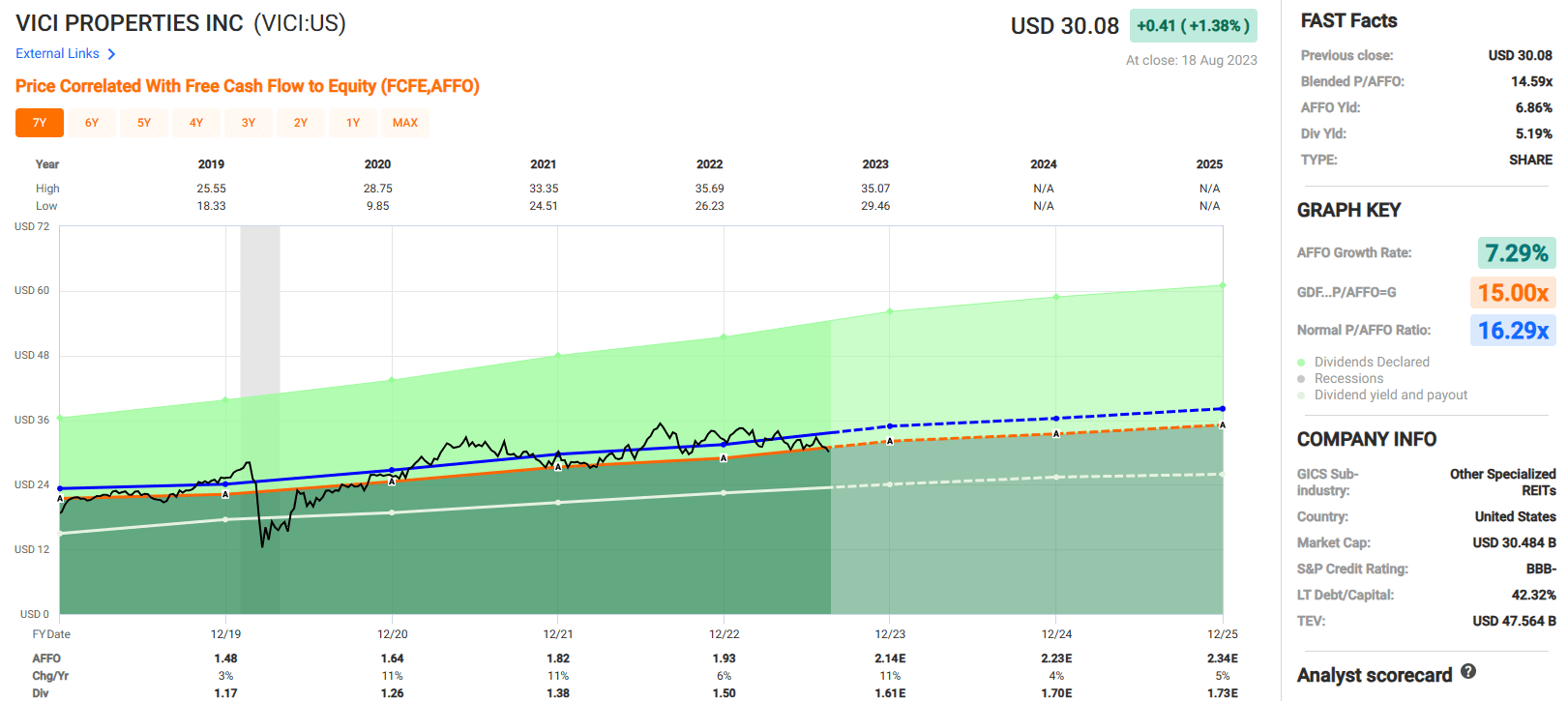

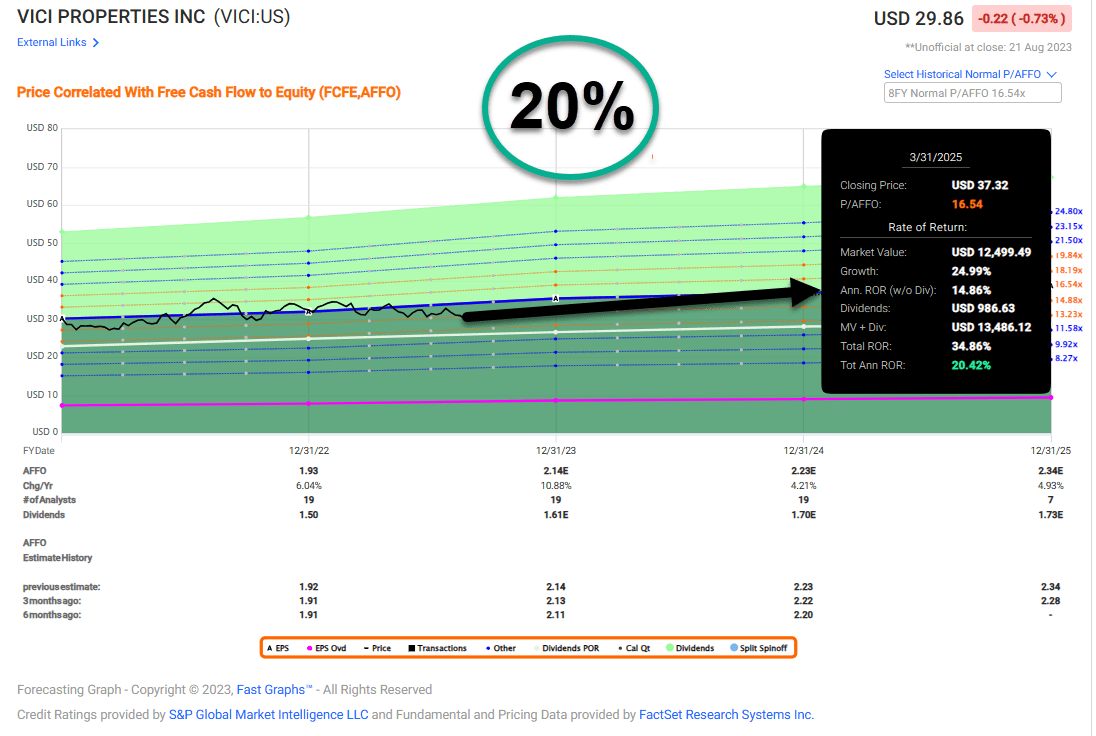

VICI Properties (VICI)

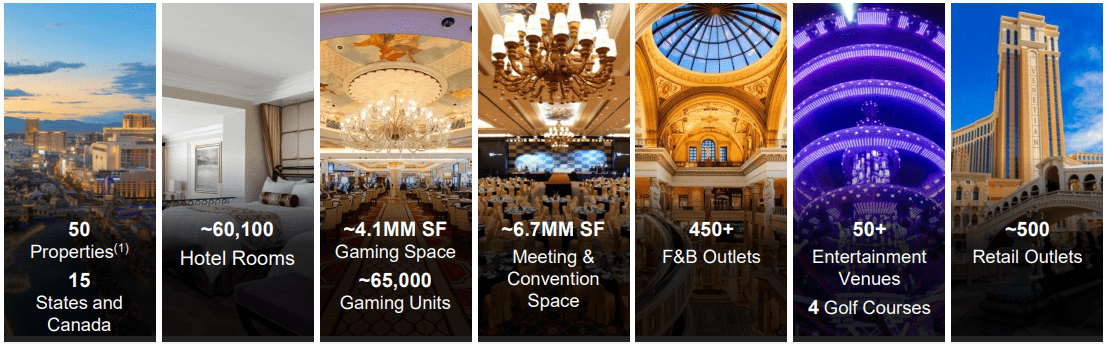

VICI Properties is an experiential REIT that invests in gaming properties along with hospitality and entertainment destinations which include iconic trophy properties such as MGM Grand, the Venetian Resort Las Vegas, and Caesars Palace Las Vegas.

Their portfolio consists of 50 gaming properties located in the U.S. and Canada that cover roughly 124 million square feet and includes over 60,000 hotel rooms, approximately 500 retail outlets, and more than 450 restaurants, nightclubs, and bars. In addition to their gaming properties, VICI also owns four championship golf courses and 34 acres of undeveloped land located next to the Las Vegas Strip.

VICI leases its properties to top gaming and hospitality operators on a long-term, triple-net basis and has inflation protected leases with 50% of their leases containing CPI-linked escalations in 2023.

VICI has 11 tenants but the majority of their rent comes from their top two operators, Caesars and MGM Resorts.

Caesars operates 18 properties which makes up 40% of VICI’s annual rent and has a weighted average lease term (“WALT”) of 32.4 years, while MGM Resorts operates 13 properties which contributes 36% to VICI’s annual rent and has a WALT of 52.0 years. The WALT for both operators is inclusive of all tenant renewal options.

{kind=link}

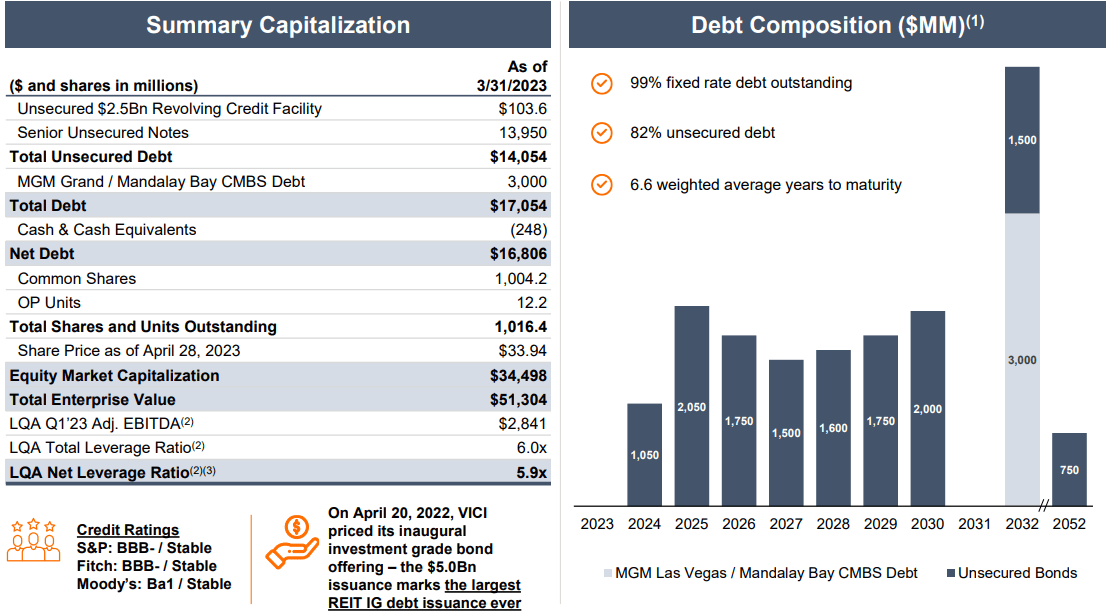

VICI completed its initial public offering (“IPO”) in 2018 and was included in the S&P 500 just several years later in 2022. That same year VICI achieved an investment-grade rating and currently has a BBB- credit rating from S&P Global.

VICI’s balance sheet is in good shape with a net debt to adjusted EBITDA of 5.9x, a long-term debt to capital ratio of 42.32%, and an EBITDA to interest expense ratio of 3.92x.

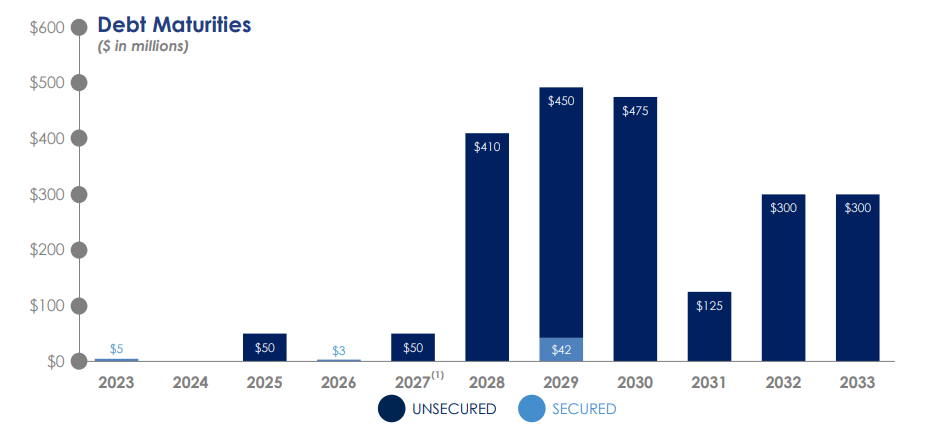

Their debt is 82% unsecured and 99% fixed rate with a weighted average term to maturity of 6.6 years, plus they have no debt maturities in 2023 and have approximately $4.0 billion in liquidity as of the end of the second quarter.

{kind=link}

Since its formation VICI has raised its dividend each year while maintaining a conservative payout ratio. Over the last four years they have delivered an average dividend growth rate of 10.80% and ended 2022 with an AFFO payout ratio of 77.72%.

VICI’s earnings have supported their growing dividend with an average AFFO growth rate of 7.29% and analysts expect that trend to continue with AFFO per share growth projected at 11% in 2023. VICI currently pays a 5.19% dividend yield and trades at a P/AFFO of 14.59x, which is below their normal AFFO multiple of 16.29x.

We rate VICI Properties a Buy.

{kind=link}

In Conclusion…

We have carefully vetted these four REITs and now let’s consider our most likely total return targets (forecast).

Realty Income: 25% Annual Total Return Forecast:

{kind=link}

MidAmerica: 20% Annual Total Return Forecast

{kind=link}

Agree Realty: 25% Annual Total Return Forecast

{kind=link}

VICI Properties: 20% Annual Total Return Forecast

{kind=link}

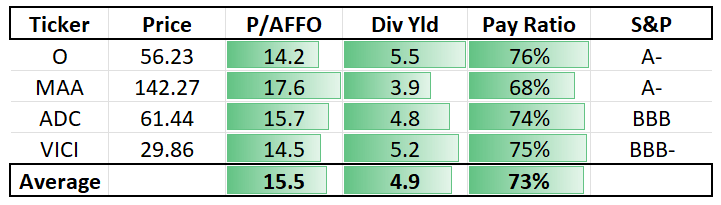

As viewed below, the average dividend yield for these four REITs is 4.9%.

{kind=link}

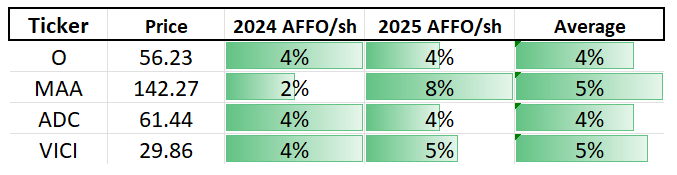

As viewed above, all four REITs have well-protected dividends supported by low payout ratios (we use AFFO per share). This means that there’s an excellent chance that these REITs will continue to increase their dividends, as evidenced by the analyst growth estimates below.

{kind=link}

While nobody knows exactly when rates will eventually pause, these four REITs are poised to deliver above average total returns and REIT Income for Life.

As always, thank you for reading and commenting.

Happy SWAN investing!

PS: Stay tuned: BDC Income For Life.

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

REIT Income For Life