ROIC - REIT Matchmaker: Survival Of The Fittest

2023-06-04 08:00:00 ET

Summary

- While I hate to see the REIT sector shrinking, it is likely that many REITs will become suitors, which is a sign that the sector is healthy.

- I would never use M&A as a catalyst supporting a recommendation since investors should always focus on underlying fundamentals.

- Nonetheless, it's fun to play the REIT matchmaker game, and I look forward to your thoughts and comments below.

This article was published at iREIT™ on Alpha on Thursday June 1, 2023.

Welcome to June 2023, everyone! And what a ride it’s been.

I think we waved goodbye to “boring” when we rang in the new year on January 1, 2020, at 12:00 a.m.

There have been worldwide shutdowns. There have been massive wars. There have been massive earthquakes. There have been massive political upheavals and shakedowns. The British empire got a new monarch after a whopping 70 years…

And the list goes on.

Far be it from me to predict what other life-changing events will happen from here. Though I will resort to smaller speculations – such as which real estate investment trusts ("REITs") might participate in mergers and acquisitions ("M&A").

We’ve already had some really big movements the last 3+ years, starting with Simon Property Group, Inc. ( SPG ) in December 2020. That was when it acquired Taubman Centers for $3.4 billion, including an 80% stake in Taubman Realty Group Limited Partnership.

Of course, after that, society shut down, as did countless businesses. While corporate giants like Target Corporation ( TGT ), Walmart Inc. ( WMT ), Costco Wholesale Corporation ( COST ), The Home Depot, Inc. ( HD ) and Lowe's Companies, Inc. ( LOW ) were able to stay open, many REITs could not. And so nothing big happened M&A-wise in the sector for over a year and a half.

The doors seemed to reopen again in August 2021, though, when Kimco Realty Corporation ( KIM ) acquired Weingarten Realty Investors. That $3.87 billion turned out to be the tip of the giant popsicle.

It’s been ice, ice, baby ever since.

The Long List of REITs That M&A-ed This Decade

In case you don’t believe me – either because you weren’t aware at the time or you’ve forgotten – here’s all the REIT M&A agreements that have taken place since August 2021:

- September 2021 – Blackstone Inc. ( BX ) acquired QTS Realty Trust for approximately $10 billion.

- November 2021 – Realty Income Corporation ( O ) acquired VEREIT for about $11 billion.

- December 2021 – American Tower Corporation ( AMT ) acquired CoreSite Realty for around $10.1 billion.

- February 2022 – Industrial Logistics Properties Trust ( ILPT ) acquired Monmouth Real Estate for $4 billion.

- March 2022 – KKR & Co. Inc. ( KKR ) and Global Infrastructure Partners acquired CyrusOne for approximately $15 billion.

- June 2022 – Blackstone bit again, this time by buying up Preferred Apartment Communities for around $5.8 billion.

- July 2022 – Healthcare Realty Trust Incorporated ( HR ) acquired Healthcare Trust of America for $17.6 billion.

- August 2022 – Blackstone (yet again) acquired American Campus Communities for $12.8 billion.

- October 2022 – Prologis, Inc. ( PLD ) acquired Duke Realty for around $23 billion.

In February 2023, then, Ready Capital Corp. ( RC ) announced its intent to merge with Broadmark Realty Capital (BRMK) (TMCXU). Extra Space Storage ( EXR ) agreed to buy Life Storage ( LSI ) in April. And the next month, it was Regency Centers ’ ( REG ) turn to announce the acquisition of Urstadt Biddle Properties ( UBA , UBP ).

I don’t think this M&A phase is over yet, though I do think it’s safe to say it’s slowed down. That’s probably in part due to rising interest rates, which makes it more expensive to expand.

At the same time, that less-than-ideal business environment makes it disproportionally harder for small businesses to operate. It’s always a dog-eat-dog world out there, but the big dogs are definitely looking "badder" than ever right now.

For any grammar fanatics and vocabulary enthusiasts out there, yes. I know that “badder” is not a real word. But I’m leaving it in there anyway.

So moving right along…

Two Advantages M&A Can Bring

Big dogs tend to rule. This fact of life is something many of us take for granted, but let’s discuss two of the main reasons behind it anyway.

- Scale advantage: Big companies can produce more for less. Their advertising clicks with more people thanks to greater brand recognition. Whatever products they need to buy can be bought in bulk, which reduces their cost overheads. And the same thing tends to go with shipping and handling costs for when they send out products. Even when they offer services instead of products, their employee counts tend to outweigh their customer counts at much greater rates, which once again allows them to take more in than they spend.

- Cost of capital advantage: Big companies can borrow money for less. This, of course, depends on how well they’re managing their business. But if they’re playing their scale advantage card correctly – as they should be – then they should be able to walk into a bank with their heads held high. Basically, their reputations precede them, assuring lenders that they’re good to repay whatever loans they take out. The result is lower financing rates that then allow big companies to save or spend their money elsewhere.

Who wouldn’t want those kinds of advantages in any kind of business environment, much less one that’s so hard to navigate?

REITs are clearly keen on them, considering all the mergers and acquisitions I mentioned above. The smaller ones are more likely to consider takeover offers considering the pressures they’re under. And the larger ones know it, with many of them more than ready and willing to take advantage of the situation and grow their advantages even further.

So let’s discuss six M&A deals I could see happening sometime in the foreseeable future.

BT's Possible Mergers & Acquisitions Picks

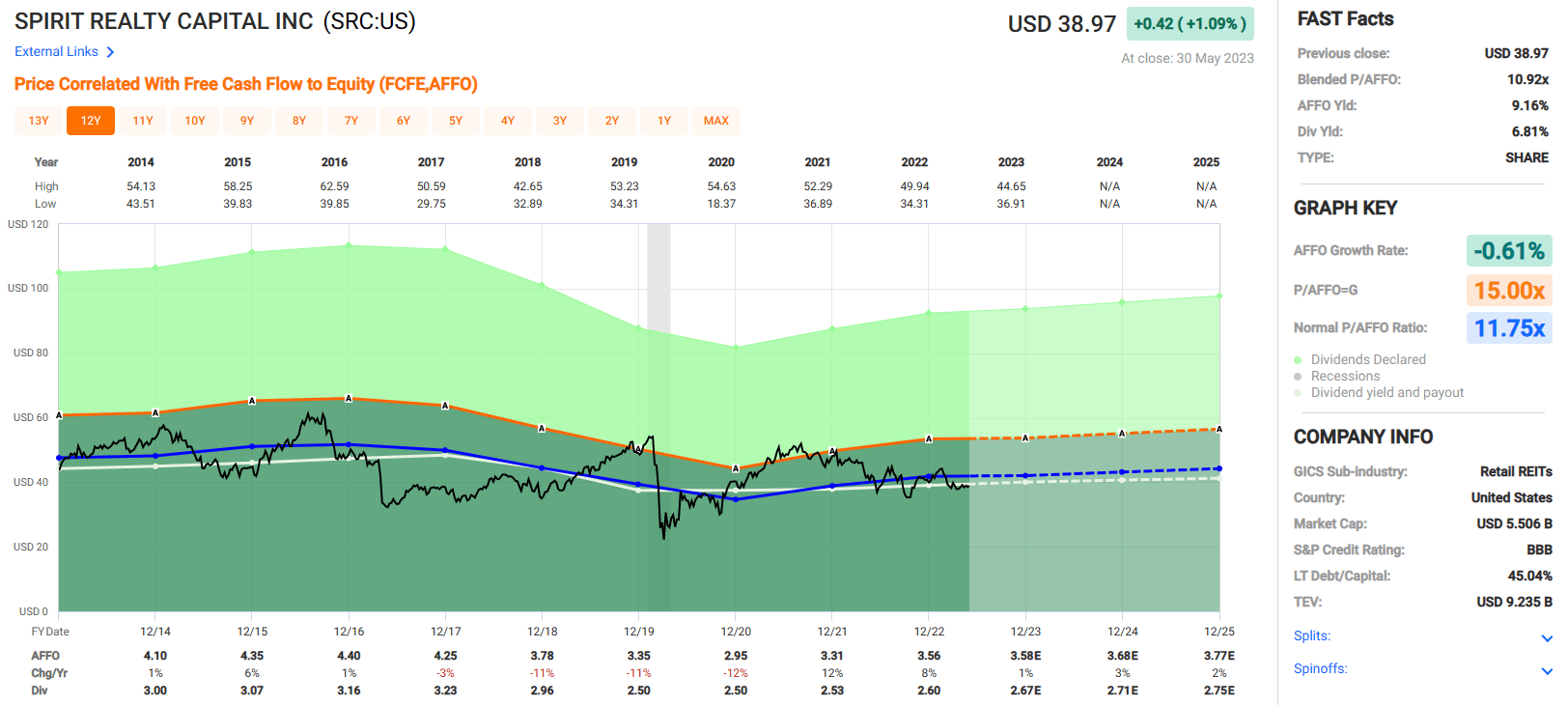

Spirit Realty Capital, Inc. ( SRC )

SRC is a net-lease real estate investment trust that owns 2,083 properties located in 49 States. They lease their properties to 347 tenants doing business in 37 industries and have a 99.8% occupancy rate with a weighted average lease term (“WALT”) of 10.4 years.

They're investment grade with a BBB credit rating from S&P Global and have solid debt metrics including an adjusted debt to adjusted EBITDAre of 5.3x and a long-term debt to capital ratio of 45.04%.

We look at SRC as a possible acquisition target with a likely suitor of Realty Income for a couple of reasons. Realty Income has a total market capitalization of $39.88 billion vs Spirit Realty’s market capitalization of $5.52 billion.

In 2021, Realty Income’s acquisition volume totaled $6.4 billion and in 2022, it totaled $9.0 billion. Due to Realty Income’s size and scale they need to make large acquisitions in order to move the needle, and this usually means that they acquire a portfolio of properties rather than purchasing individual properties.

A recent example of this is their announced acquisition of 185 single-tenant retail and industrial properties from CIM Real Estate late last year for approximately $894 million.

In their first quarter earnings release , Realty Income increased their initial acquisition guidance to over $6 billion, so acquiring Spirit Realty would be within the range of their 2023 full-year acquisition guidance.

{kind=link}

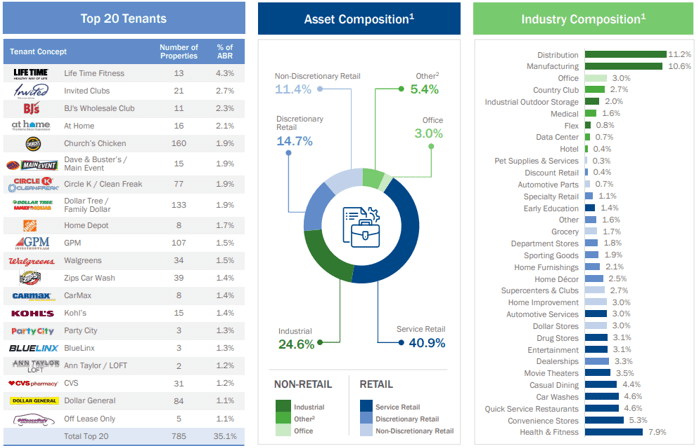

Both Spirit Realty and Realty Income are net-lease REITs that primarily own retail properties, but also own industrial real estate. They have in common several of the same tenants listed in their top-20 including Life Time Fitness, Dollar General, Walgreens, and CVS Pharmacy.

Additionally, many of their tenants operate in the same industry such as convenience stores, quick service restaurants, and drug stores, so the possible combination would be relatively seamless.

In my opinion, one of the largest driving factors that would entice Realty Income to acquire Spirit Realty is the amount of industrial properties they would gain in doing so. 24.6% of Spirit’s portfolio is made up of industrial properties, and their largest two industries are Distribution centers and Manufacturing warehouses.

Industrial properties make up 13.3% of Realty Income’s portfolio so the acquisition would increase their exposure to this growing sector and further increase the diversity of their asset mix.

Another catalyst for the possible acquisition is the discount Spirit Realty is currently trading at when compared to Realty Income. Realty Income trades at a P/AFFO of 14.91x vs Spirit Realty that trades at a P/AFFO of 10.92x.

Additionally, Realty Income is currently trading at a slight premium to their net asset value (“NAV”) whereas Spirit is trading at a slight discount to their NAV. Realty Income would receive more cash flow and real estate for each dollar invested than if it were to buy back its own shares or acquire a company with similar valuation metrics to its own.

At iREIT, we rate Spirit Realty a STRONG BUY.

{kind=link}

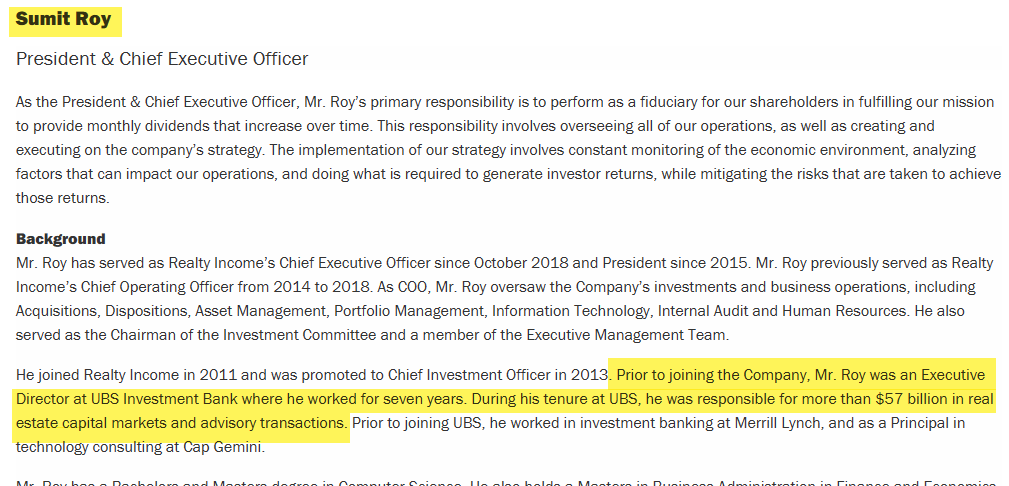

One other footnote: Realty Income's CEO once worked at UBS Investment Bank:

{kind=link}

While Spirit Realty's CEO, Jackson Hsieh, worked at UBS, too:

Spirit Realty website

Not sure how relevant this is to possible M&A but interesting footnote, nonetheless.

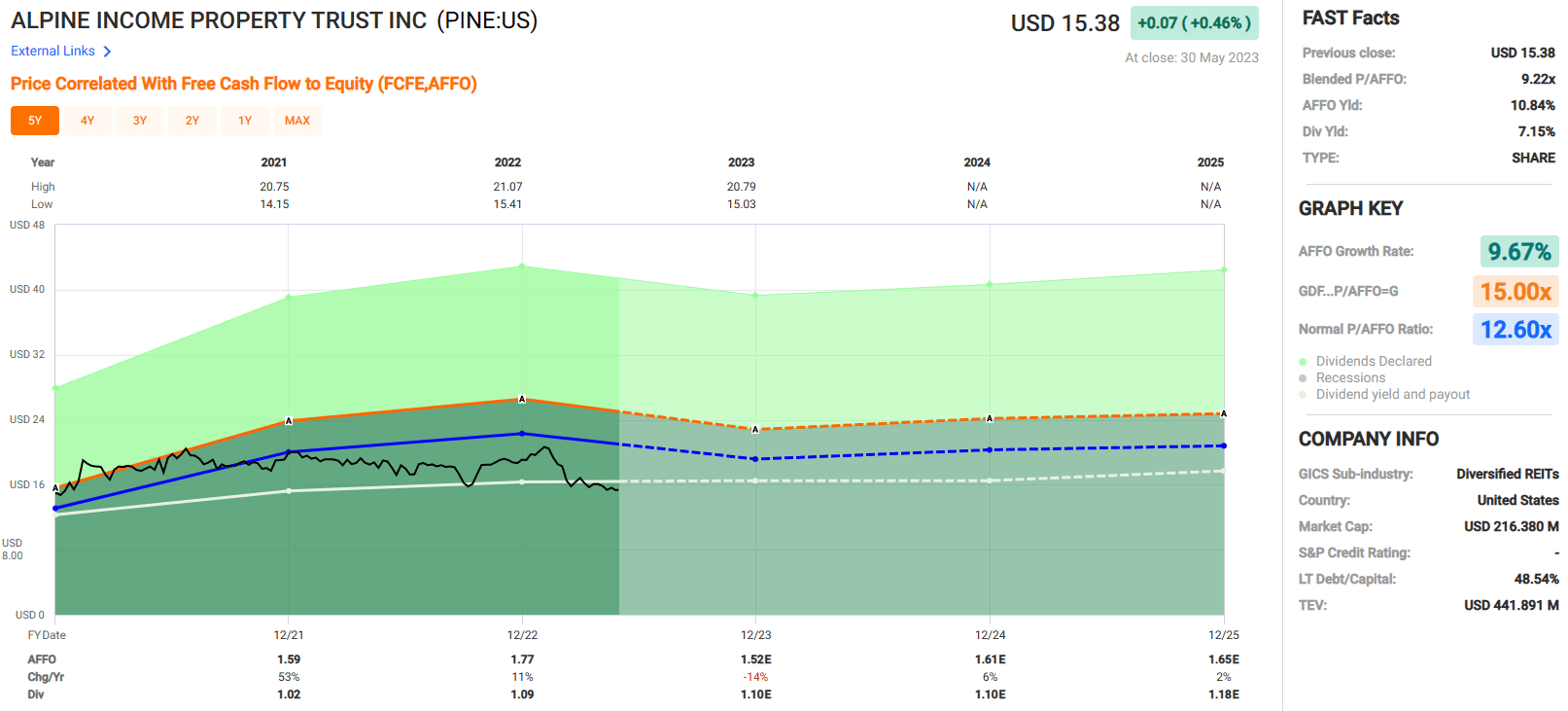

Alpine Income Property Trust, Inc. ( PINE )

Alpine Income Property Trust is an externally managed net-lease REIT. Their portfolio consists of 148 properties that are primarily leased on a triple-net basis and have an occupancy rate of 99.4%.

Their properties are located in 34 States and cover 3.5 million square feet of gross rentable space and has a weighted average lease term of 7.6 years. PINE has solid debt metrics including a net debt to pro forma EBITDA of 6.4x and a long-term debt to capital ratio of 48.54%. Additionally they have $260 million in liquidity and no debt maturities until 2026.

We view PINE as a possible acquisition suitor for Agree Realty Corporation ( ADC ).

Both companies are net-lease REITs that specialize in retail properties and both have a portfolio of ground leases. ADC has a ground lease portfolio that makes up 12.1% of their annualized base rents (“ABR”), while PINE’s ground leases make up 3% of their ABR.

In addition to having a very similar asset-mix, both REITs lease tenants that operate in many of the same retail sectors such as grocery stores, home improvement, dollar stores, and convenience stores. Furthermore, both companies share several of the same top tenants such as Walmart, Dollar General, and Lowes.

ADC / PINE - IR

As shown above, both REITs have high-quality tenants, many of which are investment-grade rated. 68% of the tenants that ADC leases to are investment-grade while 58% of PINE’s tenants have investment-grade credit ratings.

I see this as one of the biggest reasons why ADC might target PINE for an acquisition . They share many of the same tenants that operate in many of the same retail sectors and both have a high percentage of investment-grade tenants. If ADC were to acquire PINE it would not significantly reduce the credit quality of their tenant base.

ADC is a much larger company with an equity market capitalization of approximately $6.0 billion, while PINE’s equity market capitalization is $218.49 million. ADC invested $314 million in net lease properties during the first quarter and increased acquisition guidance for the full year to $1.2 billion.

PINE’s total market capitalization is less than ADC’s investments in the first quarter alone so it is very feasible to see them acquire PINE’s portfolio of net-lease holdings over the course of 2023.

Valuation is another reason why ADC might decide to acquire PINE . Currently ADC trades at a P/AFFO multiple of 16.59x while PINE trades for a P/AFFO of 9.22x. Similarly, ADC trades at a slight premium to their NAV while PINE trades at 70% of its NAV.

ADC could take advantage of the dislocation between PINEs properties’ market value and its stock’s market value and acquire their real estate for $0.70 cents on the dollar.

At iREIT, we rate PINE a Spec BUY.

{kind=link}

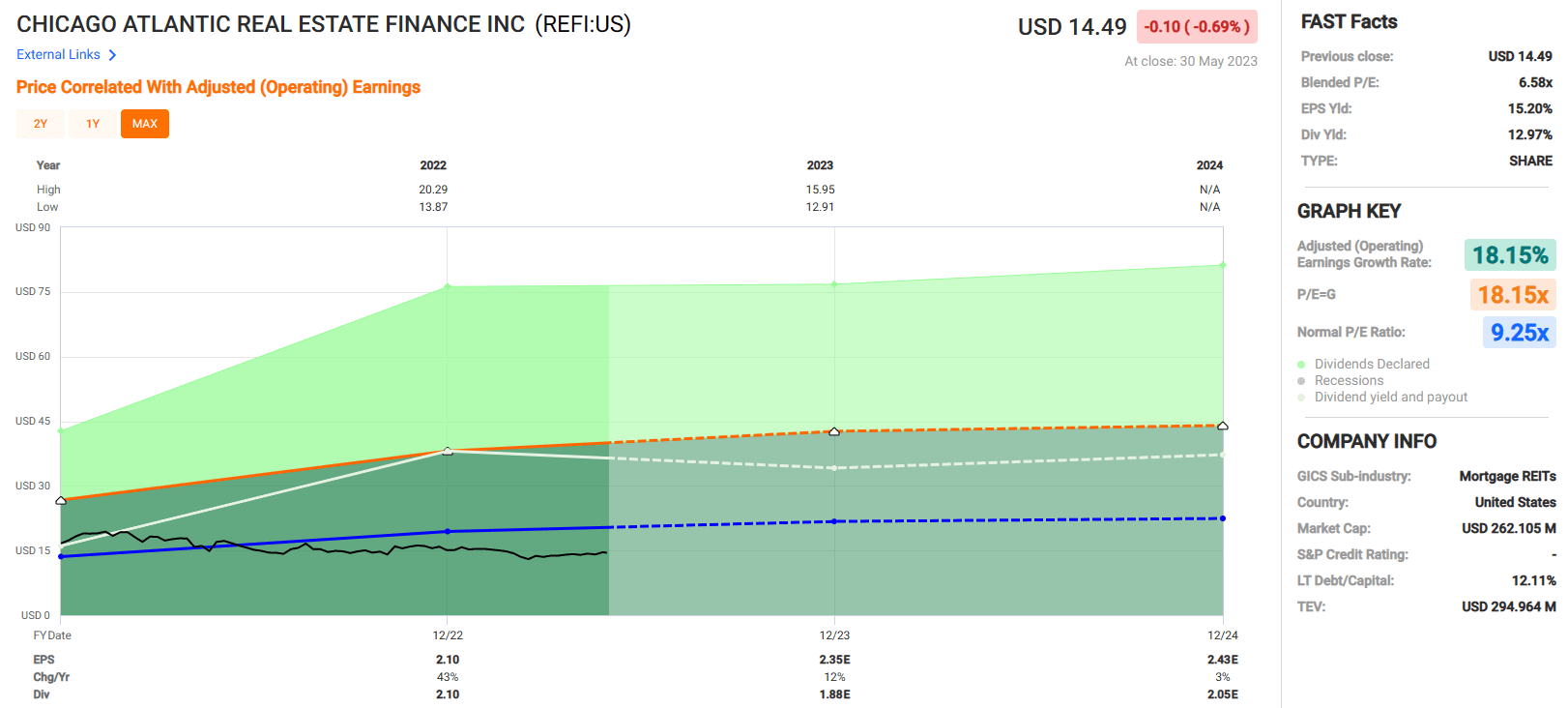

Chicago Atlantic Real Estate Finance, Inc. ( REFI )

REFI is a mortgage REIT that originates and invests in first mortgage loans that are secured by commercial real estate. Currently their portfolio is primarily made up of senior secured loans issued to state licensed cannabis operators.

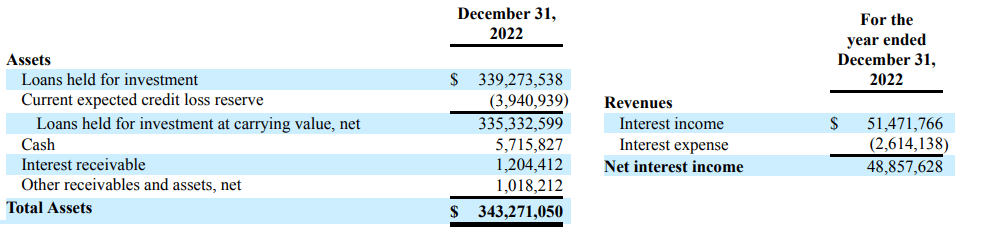

As of their latest annual filing, REFI’s assets primarily consisted of loans held for investment and all of their revenues were derived from interest income.

{kind=link}

We feel REFI could be a potential merger partner with NewLake Capital Partners, Inc. (NLCP).

NewLake Capital is an equity REIT (traded OTC) that specializes in the cannabis industry and derives the majority of its revenue through rental income but also receives interest income from loans.

Both companies are in the cannabis industry, but REFI generates its revenue from interest income while NLCP generates the majority of its revenues from rental income.

Both REFI and NLCP have a market cap totaling approximately $263 million, so if NLCP acquired REFI it would double their total equity market capitalization. REFI would complement NLCP well as it would further diversify their revenue stream with the loans they would own as a result of the acquisition.

REFI’s net interest income was reported at $48,857,628 at the end of 2022. If NLCP acquired REFI their rental income of 42,365,000 would be matched by the interest income they would receive from acquisition.

NLCP - Form 10-K (in thousands)

The acquisition would make NLCP a more diversified REIT, receiving approximately half of its revenue through rental income and about half of its revenue from interest income.

We believe there would be synergies in place between the two companies as they both operate in the cannabis space and both know how to navigate around the regulations involved in the cannabis industry.

The combination of the two companies would allow NLCP to become a one stop destination for cannabis operators to either finance their operations through sale-leaseback transactions or receive financing from senior mortgage loans.

Most importantly, NLCP could move from OTC to NASDAQ, which solves the overhang associated with the shares that are now thinly traded.

At iREIT we rate REFI a Spec BUY.

{kind=link}

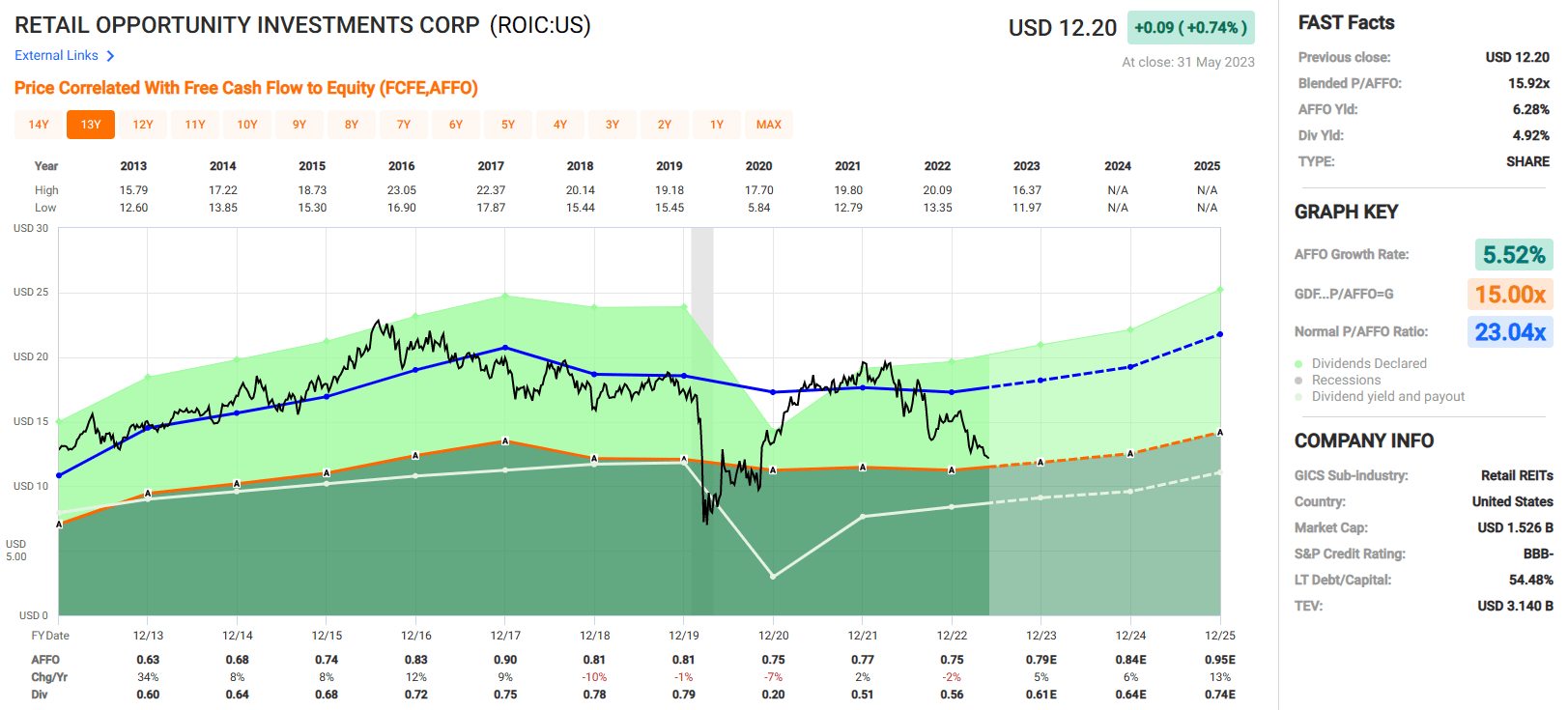

Retail Opportunity Investments Corp. ( ROIC )

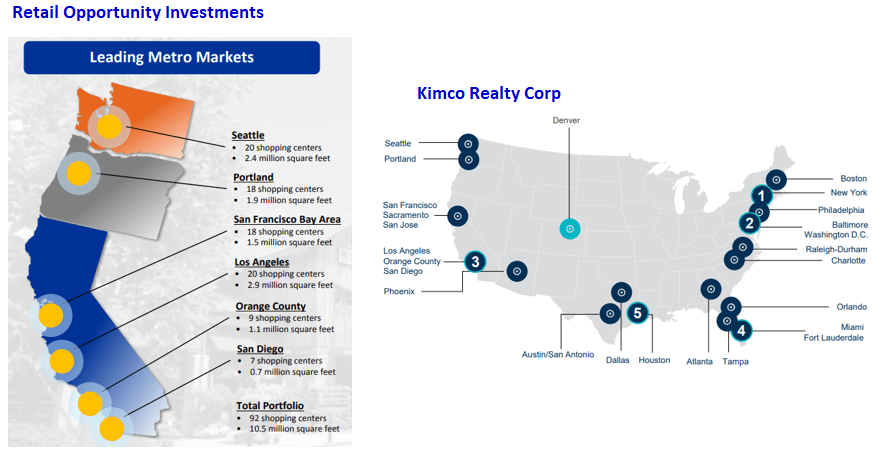

Retail Opportunity Investments is an internally managed REIT that specializes in shopping centers that are anchored by grocery stores and drugstores.

As of year-end 2022, ROIC’s portfolio consisted of 93 shopping centers and 1 office property that cover approximately 10.6 million square feet and are exclusively located on the west coast.

ROIC is investment-grade with a BBB- credit rating from S&P Global and has reasonable debt metrics including a net debt to annualized EBITDA of 6.7x, a long-term debt to capital ratio of 54.48%, and an interest coverage ratio of 3.0x

We see ROIC as a possible acquisition target for Kimco Realty Corporation ( KIM ). Kimco also specializes in grocery-anchored shopping centers and has properties located primarily in coastal and sunbelt markets.

Kimco is a much larger company with a total market capitalization of $11.22 billion vs ROIC which has a total market capitalization of $1.54 billion. KIM has much more regional diversity but operates in many of the same markets as ROIC including Seattle, Portland, San Francisco, and Los Angeles.

By acquiring ROIC, Kimco Realty would expand its West Coast presence and further diversify its regional exposure. During the first quarter Kimco acquired the remaining 85% interest in 3 grocery-anchored shopping centers located in California, which leads me to believe they have a desire to expand further into the west coast markets and by acquiring ROIC they would do just that.

{kind=link}

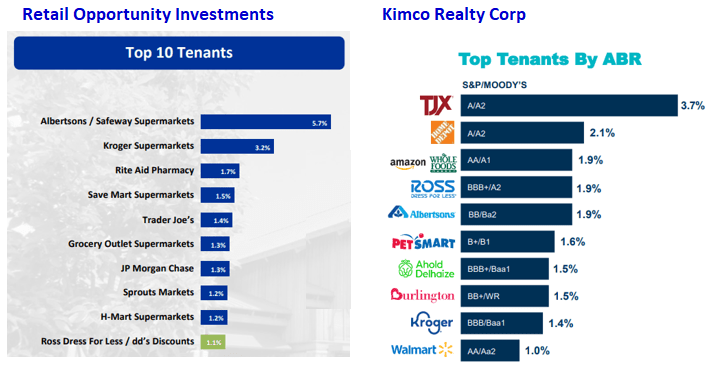

Kimco and ROIC share many of the same top tenants including Albertsons, Kroger, and Ross Dress for Less. I believe the driving catalyst for the possible acquisition is ROIC’s top two tenants: Albertsons and Kroger Supermarkets.

In late 2022, The Kroger Co. (KR) and Albertsons Companies, Inc. (ACI) announced a merger agreement where Kroger will acquire all of Albertsons outstanding shares and will combine to increase efficiencies and improve profitability.

Kimco has a vested interest in Albertsons as they own 14.2 million shares or approximately $300 million so they are very familiar with this tenant. By acquiring ROIC, Kimco would increase its exposure to Albertsons and Kroger Supermarkets in addition to increasing its west coast presence.

{kind=link}

Retail Opportunity Investments Corp is trading at a significant discount to their normal valuation. Currently ROIC is priced at a P/AFFO of 15.92x compared to their normal AFFO multiple of 23.04x.

Additionally, ROIC is trading well below their net asset value with a P/NAV ratio of 0.69. As of the end of the first quarter, Kimco had more than $2.3 billion in total liquidity so they have plenty of resources to make the acquisition if they find it advantageous.

In our opinion, this is a very possible scenario since they could purchase ROIC at a significant discount to its normal valuation and would expand their west coast presence and their exposure to Albertsons and Kroger.

At iREIT, we rate ROIC a STRONG BUY.

{kind=link}

Interesting footnote: ROIC's CEO, Stuart Tanz has a proven track record for M&A. In 1997 he led Pan Pacific Retail Properties in its IPO and in a decade expanded the portfolio from $447 million to $4 billion (600% total return) before selling to Kimco...

History doesn't repeat itself; it usually rhymes...

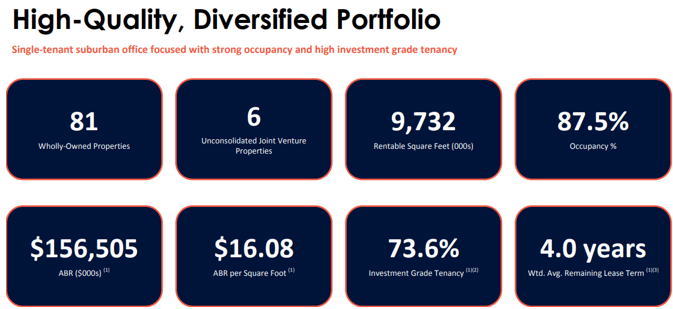

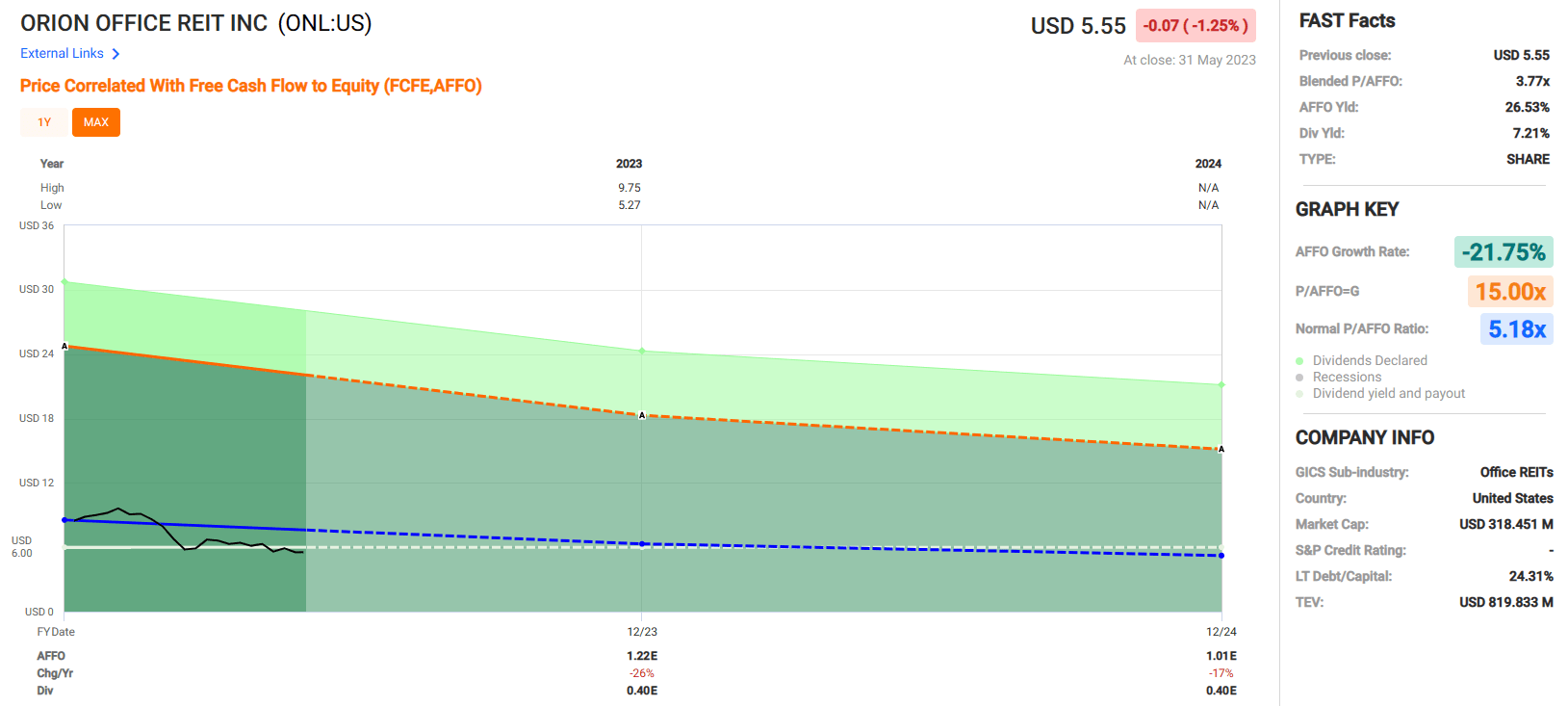

Orion Office REIT Inc. ( ONL )

Orion Office REIT was formed as a spinoff from Realty Income as part of the VEREIT merger in late 2021. ONL is an internally managed REIT that specializes in single-tenant suburban office properties that are primarily leased on a net-lease basis.

ONL’s portfolio consists of 81 office properties that encompass a total of 9.7 million square feet and are located in 29 States with an occupancy rate of 87.5% and a weighted average lease term (“WALT”) of 4.0 years. ONL has solid debt metrics, including a net debt to EBITDA of 3.97x, a long-term debt to capital ratio of 24.31%, and an interest coverage ratio of 4.25x.

{kind=link}

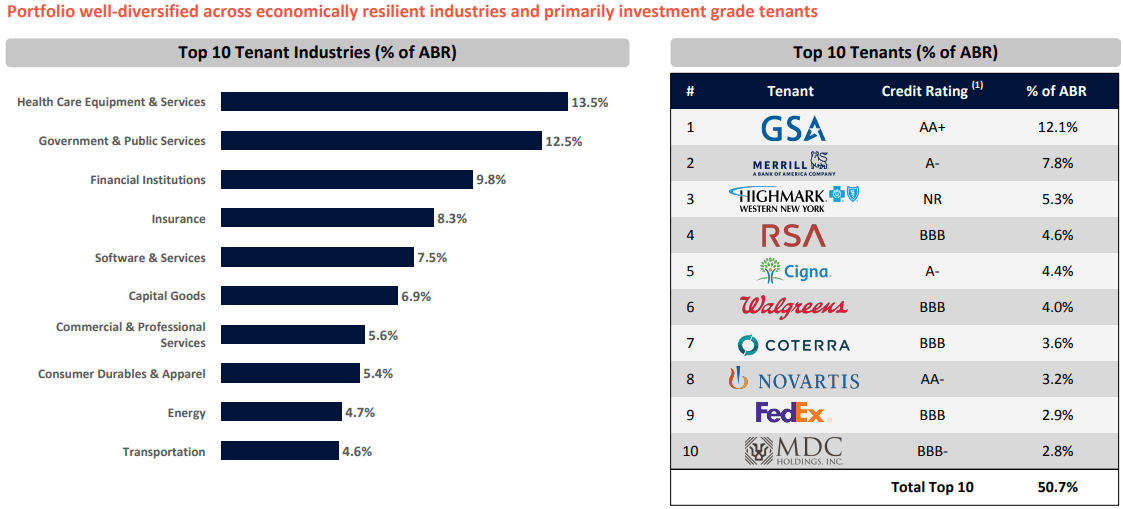

Orion’s office properties are used by tenants in multiple industries including health care and equipment, government services, financial institutions, and the insurance industry to name a few.

They have high quality tenants that mostly have an investment grade rating. In their top 10 tenants when measured by annualized base rent, only one does not have an investment-grade credit rating.

{kind=link}

As previously mentioned, Blackstone has been very active recently in acquiring real estate. In 2021, they acquired QTS Realty, in 2022 they acquired Preferred Apartment Communities, and in 2022 they acquired American Campus Communities.

Blackstone is the largest owner of commercial real estate and owns logistics properties, housing properties, life science office, and hospitality properties. BX has taken advantage of the sharp selloff in real estate to buy properties at attractive valuations and we feel Orion Office REIT could be a good candidate for a future acquisition by Blackstone.

ONL’s portfolio of properties would add extra diversification to BX’s real estate portfolio and they could easily be acquired by BX since ONL only has a total market capitalization of $322.42 million.

The biggest reason why I can see BX acquiring ONL is how cheap the stock is currently trading. We don’t have much in the way of historical comps since ONL was just recently formed, but they are currently trading at a P/AFFO of only 3.77x.

Additionally they are only trading at 37% of their net asset value with a P/NAV of 0.37. Given how cheap the stock is trading at, BX could very well scope up this company and their real estate at a significant discount.

At iREIT, we rate ONL a Hold.

(Although I personally bought a large tranche for my family office).

{kind=link}

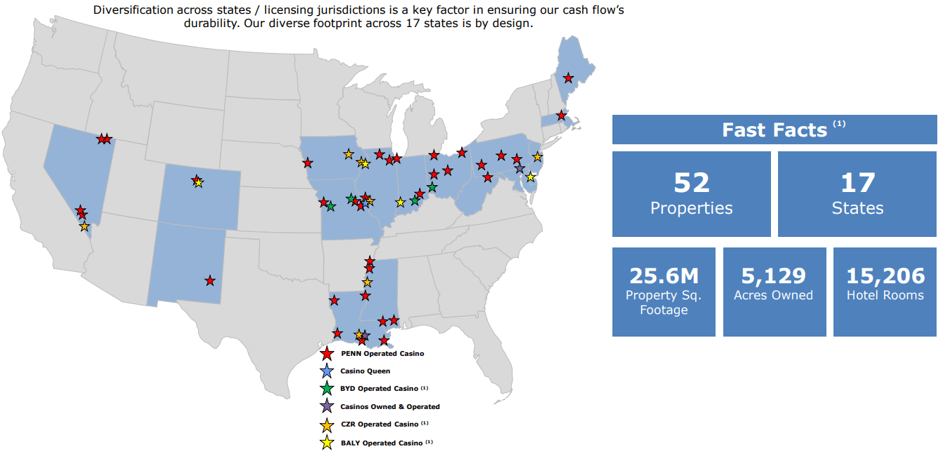

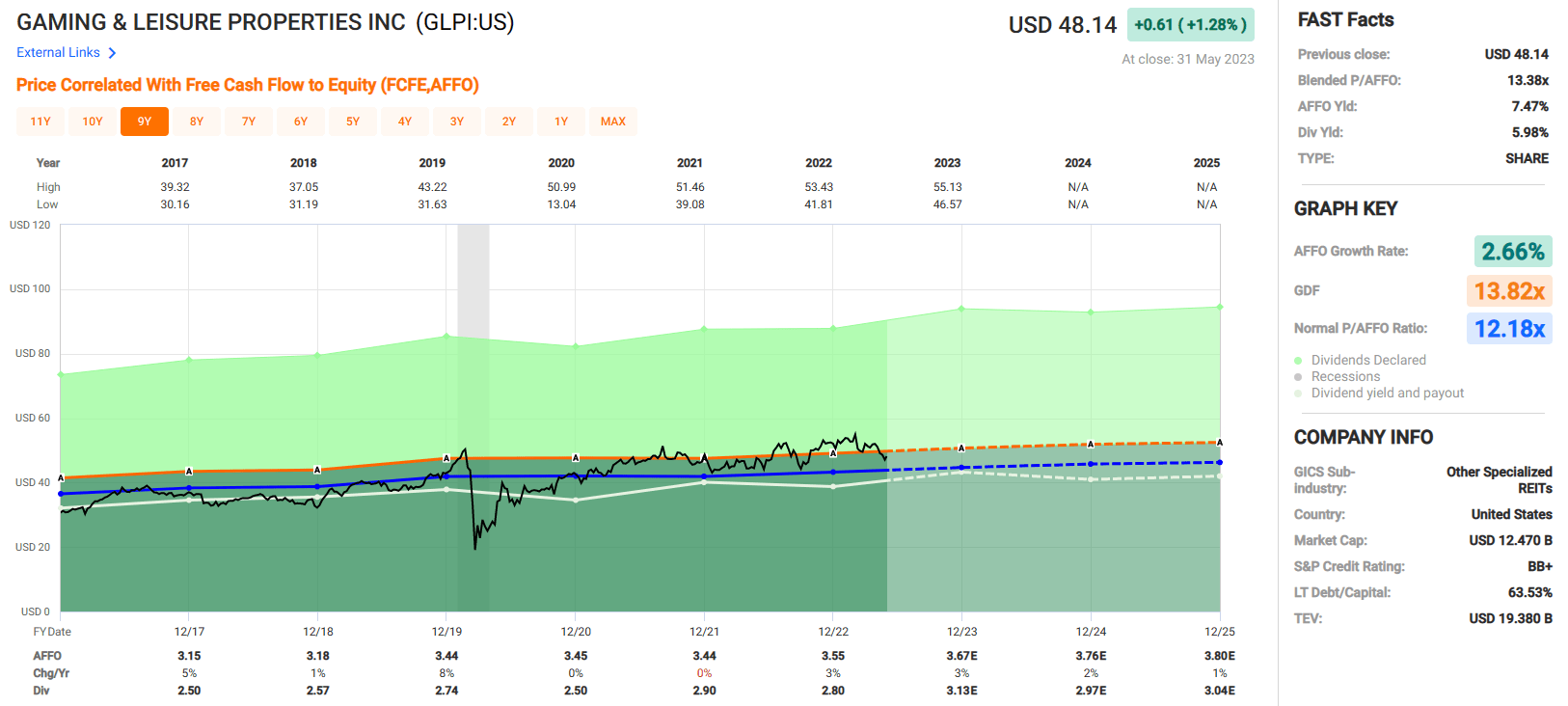

Gaming and Leisure Properties, Inc. ( GLPI )

Gaming and Leisure Properties is an internally managed REIT that specializes in gaming properties that are leased to leading gaming operators under a triple-net lease arrangement. Their operators include Penn National Gaming, Boyd Gaming, Caesars Entertainment, Bally, and the Casino Queen.

They are regionally well diversified with gaming properties spread across 17 States and as of year-end 2022, they had an occupancy rate of 100%. In total their portfolio includes 52 gaming properties and 15,206 hotel rooms that cover 25.6 million square feet.

{kind=link}

Gaming properties are one of the most experiential real estate sectors and are very resistant to e-commerce. We think there is a reasonable chance that GLPI could be an acquisition target for Realty Income.

Realty Income has been positioning its portfolio to be more resilient against e-commerce in the types of properties they acquire. Their portfolio now consists of 82% retail properties, but also is made up of industrial properties at 13% of their annual contractual rent and gaming properties at 2.8%.

Realty Income - IR

Realty Income made its first move into the gaming space with its acquisition of the Encore Boston Harbor which is a super-regional resort and casino that features fine dining, gaming, and hotel rooms.

We believe this trend will continue as Realty Income has signaled interest in the gaming sector and is continuously adding e-commerce resistant properties to its portfolio. If Realty Income were to acquire GLPI, it would automatically add regional and operator diversification to its portfolio of gaming properties.

At iREIT, we rate Gaming & Leisure Properties a Spec BUY.

{kind=link}

In Closing...

With 3 REIT M&A deals announced so far in 2023, I expect to see more opportunities as the year progresses due to the wider discounts being offered by Mr. Market. All of the above referenced targets are trading at elevated equity yields:

- SRC 9.1% vs O 6.6%

- PINE 10.8% vs ADC 6.0%

- NLCP 17.7% vs REFI 15.0% (using EPS)

- ROIC 6.3% vs KIM 6.4%

- ONL 26.5% vs BX (11% est.)

- GLPI 13.4% vs O 6.6%.

While I hate to see the REIT sector shrinking, it is likely than many REITs will become suitors, which is a sign that the sector is healthy.

Also, I would be remiss to say that these ideas are just that, ideas, and they may never occur. In addition, I would never use M&A as a catalyst supporting a recommendation as investors should always focus on underlying fundamentals.

Nonetheless, it's fun to play the REIT matchmaker game and I look forward to your thoughts and comments below.

Happy SWAN Investing!

For further details see:

REIT Matchmaker: Survival Of The Fittest