EXR - REIT Meltdown: 3 Rarely Discounted Buying Opportunities

2023-09-11 09:15:00 ET

Summary

- REITs are reviled and shunned by the market, having lost ~30% of their value since the beginning of 2022.

- Higher interest rates along with negative sentiment from office properties' particular troubles have created a perfect storm for public real estate stocks.

- But historically, REITs have outperformed every other stock sector in the years after a drawdown this severe.

- From the trough of the GFC to the beginning of COVID-19, REITs outperformed the market on a total returns basis.

- I highlight three of my favorite high-quality, heavily discounted REITs to buy today.

Is there a more reviled and shunned sector of the stock market today than real estate?

Since the beginning of 2022, publicly traded real estate investment trusts ("REITs") have been one of the worst, if not the worst, performing areas of the market.

In sharp contrast to soaring energy stocks (XLE), real estate stocks ( VNQ ) have suffered a decline of nearly 30% since early 2022.

Why?

In " Nightmare On REIT Street - Briefly Explaining The Bloodshed ," I talked about the three ways that rising interest rates typically cause REITs to drop:

- It incrementally increases borrowing costs over time

- It often causes companies' underlying asset values to fall

- It creates competition for scarce shareholder capital by making bond yields attractive in comparison

That last point is a major one. I hear from commenters again and again: "Why buy a REIT when you could get a 5%+ yield on cash risk-free?"

Of course, the 5%+ yields on cash offer no upside, growth, or inflation protection. But in any case, this is a big reason why investors have shunned REITs.

And then there's one last reason why REITs have performed so badly:

- Negative sentiment due to the media's consistent equating of "commercial real estate" with downtown office buildings. But as I explained in " Blue-Chip Real Estate Is A Bargain ," these are not identical. In fact, office REITs make up less than 5% of the overall REIT index by market cap and less than 10% by funds from operations ("FFO") and net operating income ("NOI").

It is true that office real estate still faces continued struggles for years to come as hybrid work takes its toll on leasing demand, capital spending requirements ramp up in order to retain or attract tenants, and low-interest loans mature and need to be refinanced at much higher rates.

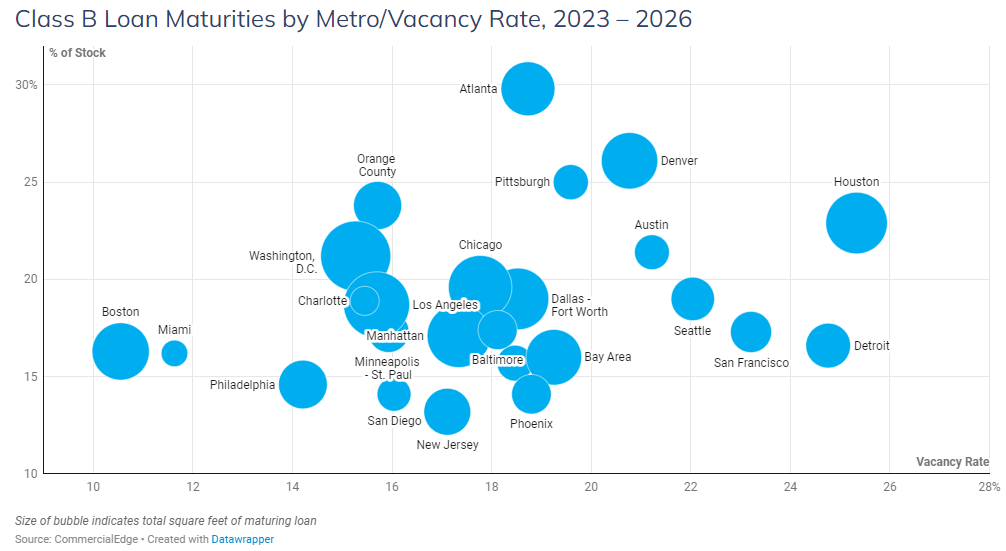

For example, in the next three years, a steady slate of mortgage loans will continue to mature for mid-quality Class B office properties, which will put tremendous pressure on landlords and undoubtedly create ample pockets of distress.

{kind=link}

I would not want to be a Class B office landlord in Houston, for example, because of its unappealing combination of ~25% vacancy rate and ~25% of square footage with loan maturities in the next three years.

Surely this will inhibit the growth of most office real estate going forward as the competition for tenants heats up.

Again, though, office REITs make up a tiny sliver of the overall REIT universe.

Perhaps some investors assume that other property sectors are suffering similar problems as office, but that assumption is incorrect.

According to NAREIT , both FFO and NOI for the overall REIT index hit new all-time highs in Q2 2023.

Moreover, as I explained in " Fed Rate Hikes Create Short-Term Pain But Long-Term Gain for REITs ," high interest rates are not purely bad for REITs.

That is because the higher cost of capital is causing construction starts of new properties to absolutely plummet across all real estate sectors. Hence you see headlines like this one from Globe Street :

{kind=link}

Yes, REITs are hurt by high interest rates. But they are not hurt nearly as bad as the many bank-dependent, highly leveraged private real estate owners out there.

And now, with REIT prices down ~30% from their early 2022 highs, publicly traded real estate stocks look like a phenomenal value, especially for certain heavily punished yet high-quality REITs.

I'll pitch three of my favorite discounted yet high-quality REITs below. But first, let me demonstrate real estate's ability to powerfully rebound from selloffs like the current one.

REITs Across The Cycle

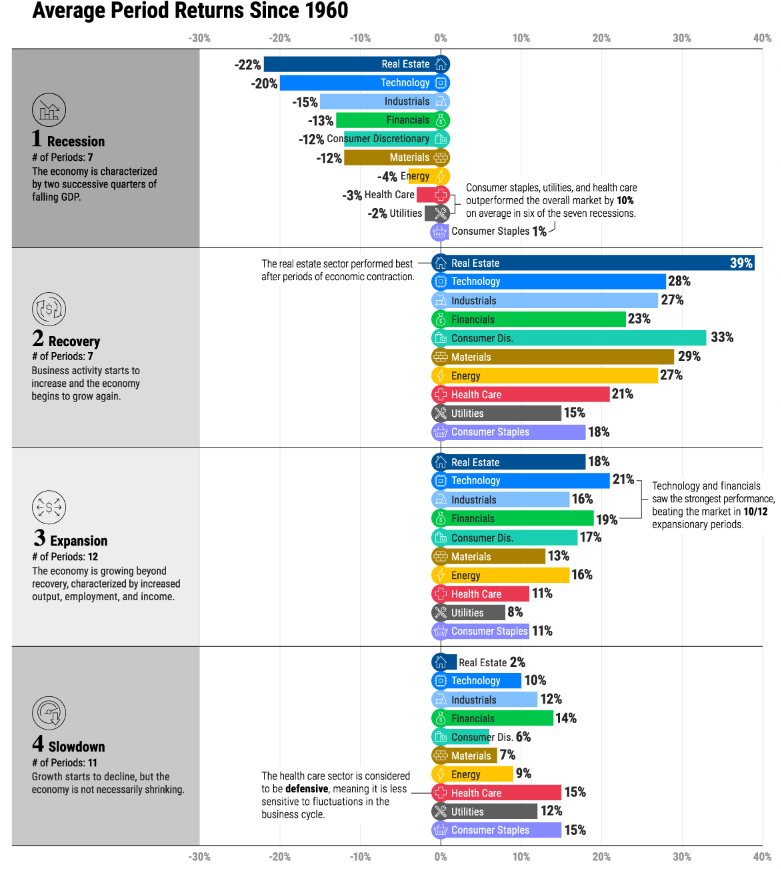

Across the last 7 recessions, REITs have been the worst performers, averaging a 22% drawdown during these periods. Although we have not been in an officially declared recession, consider that the almost 30% drawdown since the beginning of 2022 is worse than this average.

{kind=link}

But then, notice that real estate has been the #1 strongest performing sector during recoveries. Moreover, it is among the strongest performing sectors during expansionary periods.

It is only during slowdowns and recessions that REITs underperform. And when it does underperform, the underperformance is typically lower than what we've experienced during the current REIT bear market.

As such, if and when a recession is finally declared and interest rates come down from current levels, REITs should be among the strongest performing sectors, if not the strongest performing, going into the next recovery phase.

Let me demonstrate the power of this from the Great Financial Crisis.

During the GFC, the REIT index got obliterated, losing nearly 2/3rds of its value from the Summer of '08 to the trough in March 2009, compared to "only" 46% for the S&P 500 ( SPY ).

But (and this is extremely important) those who bought REITs anywhere near their bottom in early 2009 were richly rewarded in the years after, as the REIT index outperformed the broader market on a price basis alone (not considering REITs' higher dividend yields) until 2018!

On a total return basis (including dividends), REITs outperformed the market from their GFC trough all the way up to the beginning of COVID-19.

The current selloff creates a very compelling opportunity for the long-term investor.

Interest rates don't need to go all the way back to zero for REITs to outperform. They just need to stabilize at a more modest level in order to better align costs of capital with property cap rates. That will be a massive boon to REITs.

Let's look at three of my favorite high-quality picks that I view as coiled springs, ready to outperform in the years ahead while generating strong dividend growth.

1. Alexandria Real Estate Equities ( ARE )

{kind=link}

If you've read my articles before, you've probably heard me pitch ARE multiple times. The Buy thesis remains the same, so I'll keep it brief here.

ARE owns Class A, state-of-the-art life science / biotech laboratory properties located in the nation's most innovative and productive research clusters and leased to the world's most innovative and productive biotech companies.

Alexandria Real Estate Equities

{kind=link}

ARE has zero balance sheet stress. Its credit ratings are BBB+/Baa1. It has over $6 billion in liquidity. Slightly over 99% of debt is fixed-rate. And the weighted average debt maturity sits at 13.2 years (among the highest in the REIT space), with no maturities until 2025.

The real concern is the amount of life science supply coming to market. Labspace is different than traditional office, and its demand outlook is vastly superior. But there are lots of traditional office owners redeveloping their empty buildings into new labs.

The market is worried that this will spell the end of ARE's impressive record of double-digit rent growth.

I'm not so sure.

For one thing, the life science development pipeline is slowing down amid a drop in leasing activity This should eventually diminish the oversupply worries.

Another, perhaps more important point is that ARE's property location and quality acts as a "moat" in itself. The best biotech tenants want to be located in the best life science buildings, especially those that are situated in highly productive research clusters -- multi-building campuses where biotech researchers congregate.

Case in point: ARE expects to grow FFO per share by 6.4%, only a little shy of its 10-year average growth rate of 7.4%.

Looking at price to operating cash flow, a proxy for FFO, we find that ARE has not been this cheap since the wake of the GFC.

Between a 4.3% dividend yield and 6% average annual dividend growth rate, ARE looks like a phenomenal Buy for long-term dividend growth investors.

2. Crown Castle ( CCI )

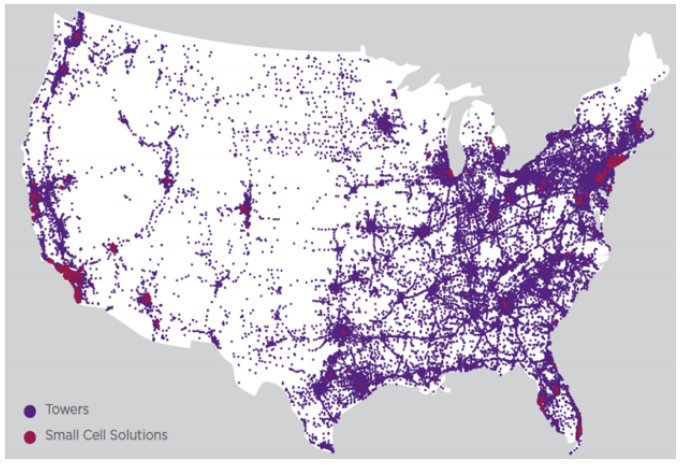

CCI owns perhaps the largest telecommunications infrastructure portfolio in the United States, consisting of about 40,000 towers, ~120,000 small cell nodes, and over 80,000 route miles of fiber cables.

{kind=link}

The telecom infrastructure REIT has taken a huge hit to investor sentiment from cancellations of tower leases used by Sprint due to the merger of Sprint and T-Mobile ( TMUS ).

The market seems to fear that CCI will never be able to revive growth. But management insists that it will be able to return to 5% organic revenue growth and 7-8% dividend growth after the bulk of the Sprint lease cancellations take effect in 2025. In fact, around 75% of this 5% revenue growth is already contracted through 2027.

As I wrote in " Bloodshed On REIT Street: 5 High-Quality Landlords I'm Buying For The Long Haul ":

Ask yourself these questions:

- Will the huge growth in mobile data usage and 5G applications really not need any more infrastructure investment from the wireless carriers? (Of course it will.)

- Is it likely that we will see more consolidation among telecom providers? (No, it's already an oligopoly.)

- Am I willing to wait until 2026 before I see AFFO and dividend growth pick up for CCI again?

CCI's scale, cost of capital, and leading market position in small cells together act as major competitive advantages that should serve it well in the long run.

{kind=link}

Being priced at 13.3x AFFO, I think CCI has about 60-70% upside to a post-2025 fair value AFFO multiple of about 22x. That's on top of its 6%+ yielding dividend.

By price-to-AFFO (and price to operating cash flow, as pictured above), CCI has never been this cheap during its lifetime as a REIT.

3. Extra Space Storage ( EXR )

After its merger with Life Storage (LSI), EXR has become the largest owner and operator of self-storage properties.

{kind=link}

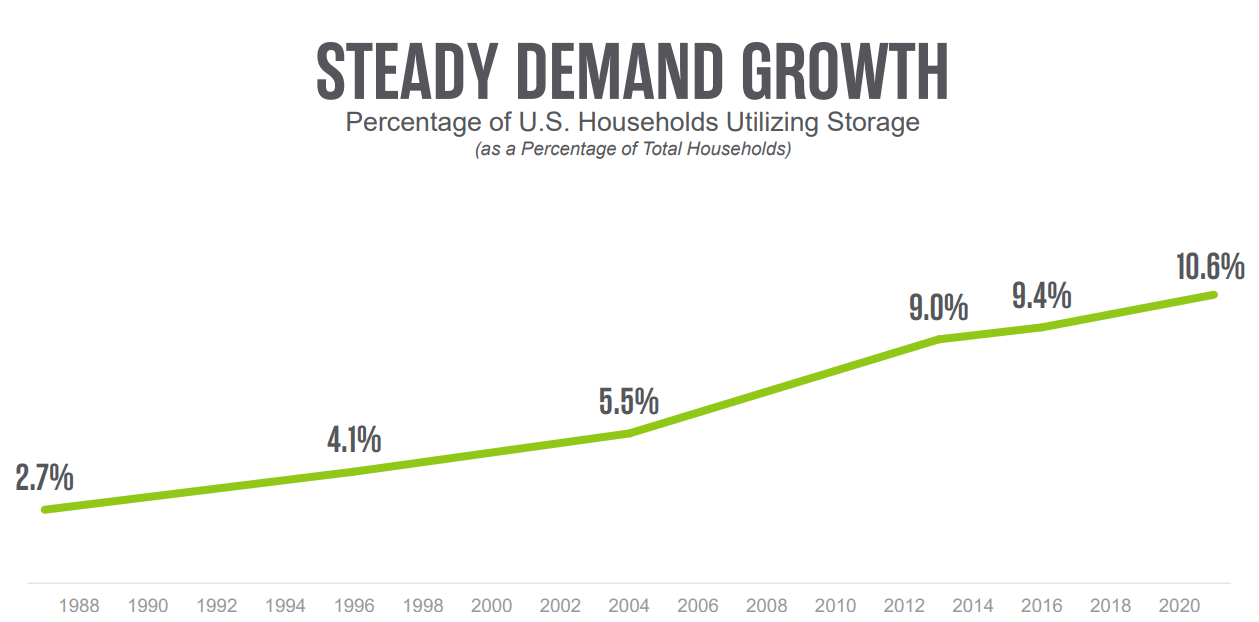

I like storage REITs because they have a strong history of outperformance as Americans have accumulated more stuff than they've been able to fit in the amount of housing they can afford, and therefore they've increasingly relied on storage units.

{kind=link}

In my estimation, EXR boasts best-in-class management (19-year average tenure for the executive team), cost of capital (BBB+ credit rating), portfolio quality in top markets, and operational excellence. This operational advantage includes a top-tier technology package, which is one of the primary ways management expects the newly added LSI properties to outperform in the coming years as they are added to the system.

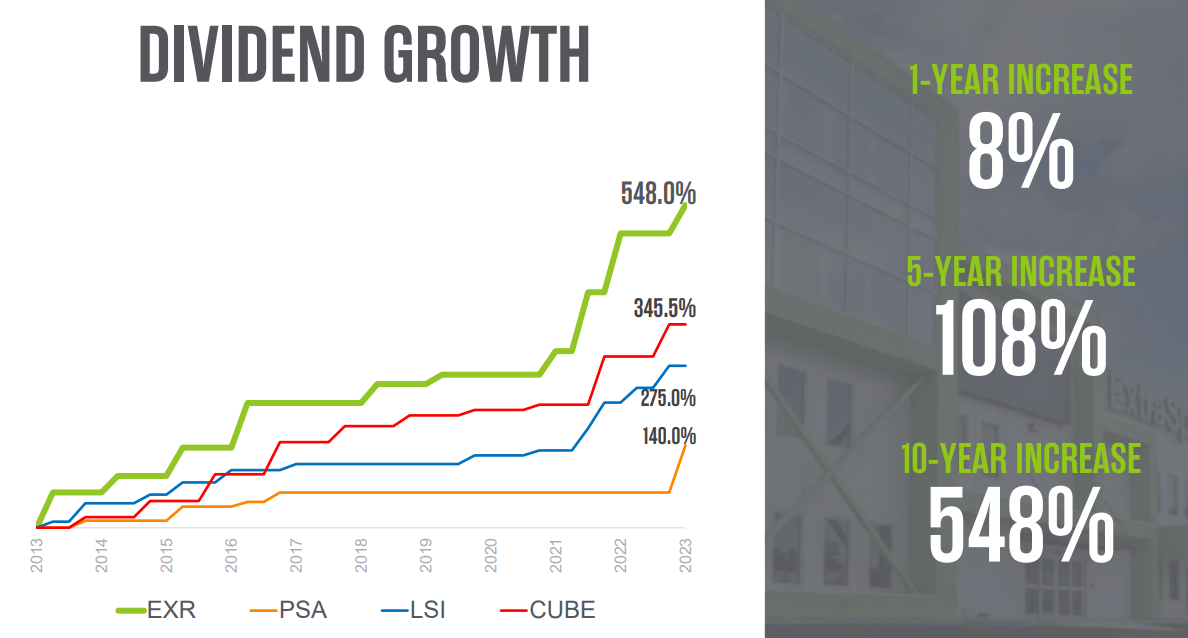

There is perhaps no better way to exhibit EXR's quality than by looking at its massive long-term outperformance in total returns over its primary peer Public Storage ( PSA ) as well as the broader REIT index and the S&P 500:

As for ARE, there is a lot of recent new supply of storage properties in many markets, which is expected to blunt rent growth for at least the next year. But also like for other property sectors, construction starts for new storage properties has plunged, which means that supply and demand should eventually come back into equilibrium and allow for organic growth to resume.

EXR now yields 5.1%, far above its 5-year average of 3.4%, and the REIT has an extremely impressive history of dividend growth.

{kind=link}

And with an ~80% payout ratio, that dividend looks well-protected and able to continue EXR's 13-year dividend growth streak.

I wouldn't expect anything more than a measly raise next year, but a top-quality REIT like EXR is likely to return to strong growth within a few years.

By price to operating cash flow, EXR has not been this cheap since the wake of the GFC in 2011.

And at an AFFO multiple of 16.2x, EXR has about 35% upside to its 5-year average price-to-AFFO of ~22x. I think shareholders will enjoy that upside and perhaps more within a few years.

Bottom Line

This is an exciting time to be a long-term REIT investor. The discounts offered for high-quality names across various sectors are ridiculous. But I'm not complaining. I'm buying.

I believe buyers of blue-chip REITs will be richly rewarded for their bravery -- eventually.

For further details see:

REIT Meltdown: 3 Rarely Discounted Buying Opportunities