PEAK - REIT Merger Standoff: Spirit Realty The Clear Winner With A Low Risk Potential 18.5% Return

2023-11-01 09:44:31 ET

Summary

- Spirit Realty shares merging with their fixed exchange ratio of 0.762x and Realty Income shares returning to their pre-merger AFFO multiple of 12.3x provides for an 18.5% total return potential.

- $1.8 billion in combined equity value lost despite over $100 million in combined merger synergies with no need to for expensive debt financing represents a dislocation from fundamentals.

- Spirit Realty shares are currently trading below its fixed exchange ratio despite the merger not requiring approval by Realty Income shareholders.

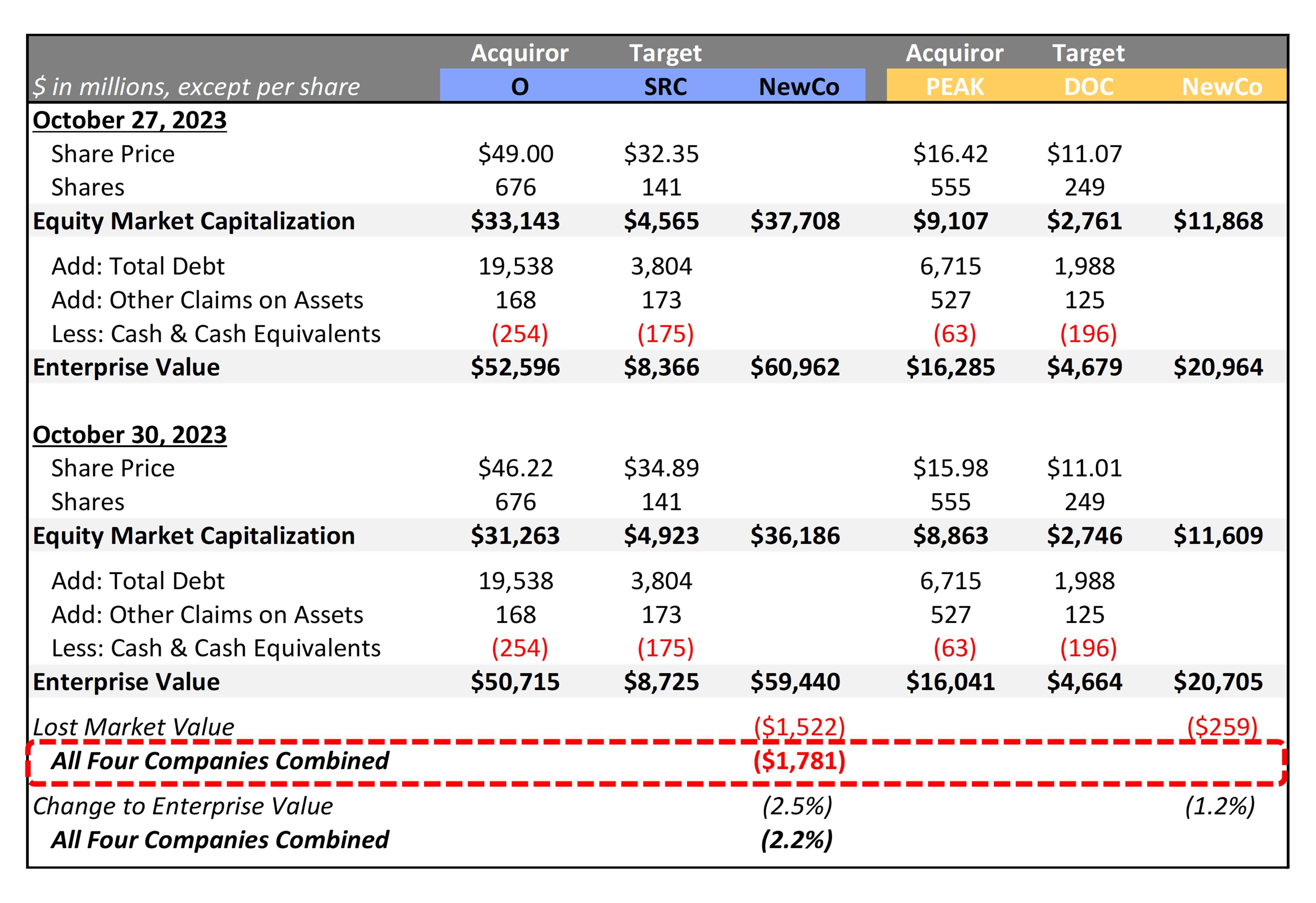

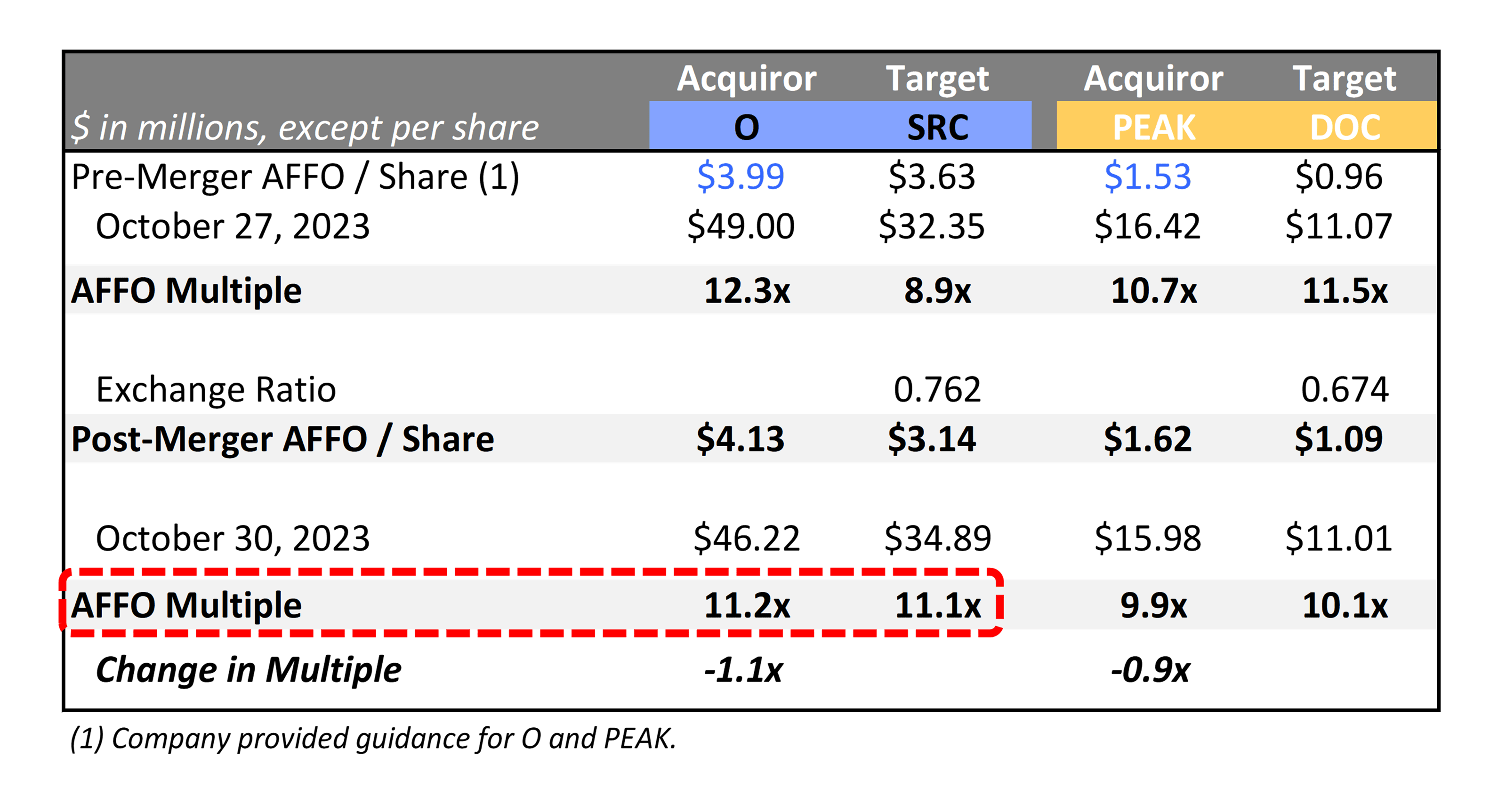

On October 30, 2023, two REIT mergers were announced within the net lease and healthcare REIT subsectors. Net lease REIT Realty Income (O) announced its merger with smaller peer Spirit Realty Capital (SRC) coincident with Healthpeak Properties (PEAK) announcing its merger with smaller peer Physicians Realty Trust (DOC). While the mergers were both considered to be mergers of equals, for the sake of this article, I will refer to the larger REIT as the acquiror and the smaller REIT as the target.

Comparing the market value of all four companies as of Friday October 27th's close (pre-merger announcements) to Monday October 30th's close (post-merger announcements) reveals that a combined $1.8 billion of equity market value was lost after the mergers were announced representing a -2.2% combined decline in Enterprise Value (EV) between the four companies.

Given that both are non-cash stock-for-stock transactions (i.e. no need to raise new debt in the current unfavorable interest rate environment) with expected merger synergies of over $100mn between both transactions, I think current levels represent a potential opportune point of entry that warrants a deeper dive on both mergers.

{kind=link}

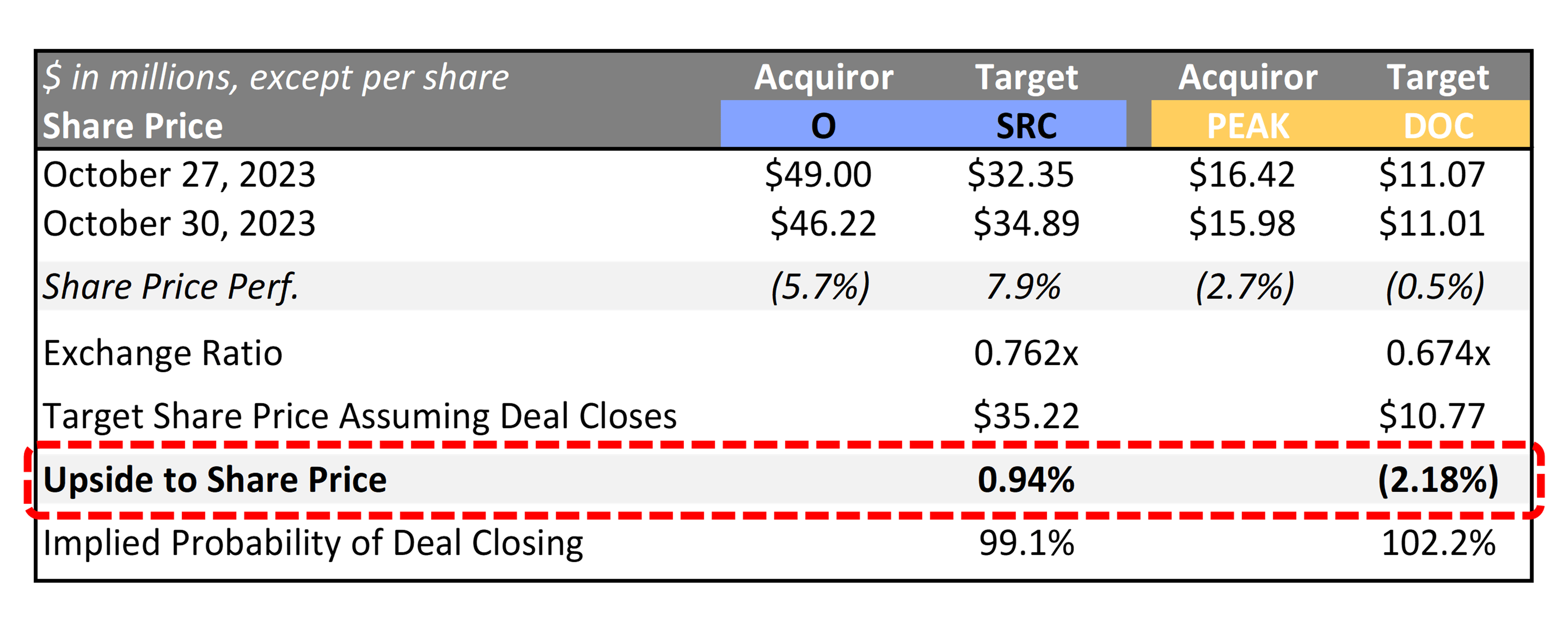

In a stock-for-stock transaction, shareholders of the target company receive a fixed ratio of the acquiror's shares for every share of the target company that the investor owns. In this case assuming the mergers close SRC shareholders will receive 0.762x shares of O for every share of SRC they own and DOC shareholders will receive 0.674x shares of PEAK for every share of DOC that the investor owns.

Typically, after a merger is announced, the target's shares trading at a ratio below the announced ratio indicates that investors have doubt that the merger will close. In this case SRC's current share price of $34.89 is trading at a -0.9% discount to its implied post-merger value, while shares of DOC are currently trading at a +2.2% premium to its implied post-merger value. Assuming O's share price remains at current levels and the merger closes (which does not require approval by O shareholders), SRC shares should merge with their $35.22 post-merger value providing investors with a low risk return of +0.9%.

{kind=link}

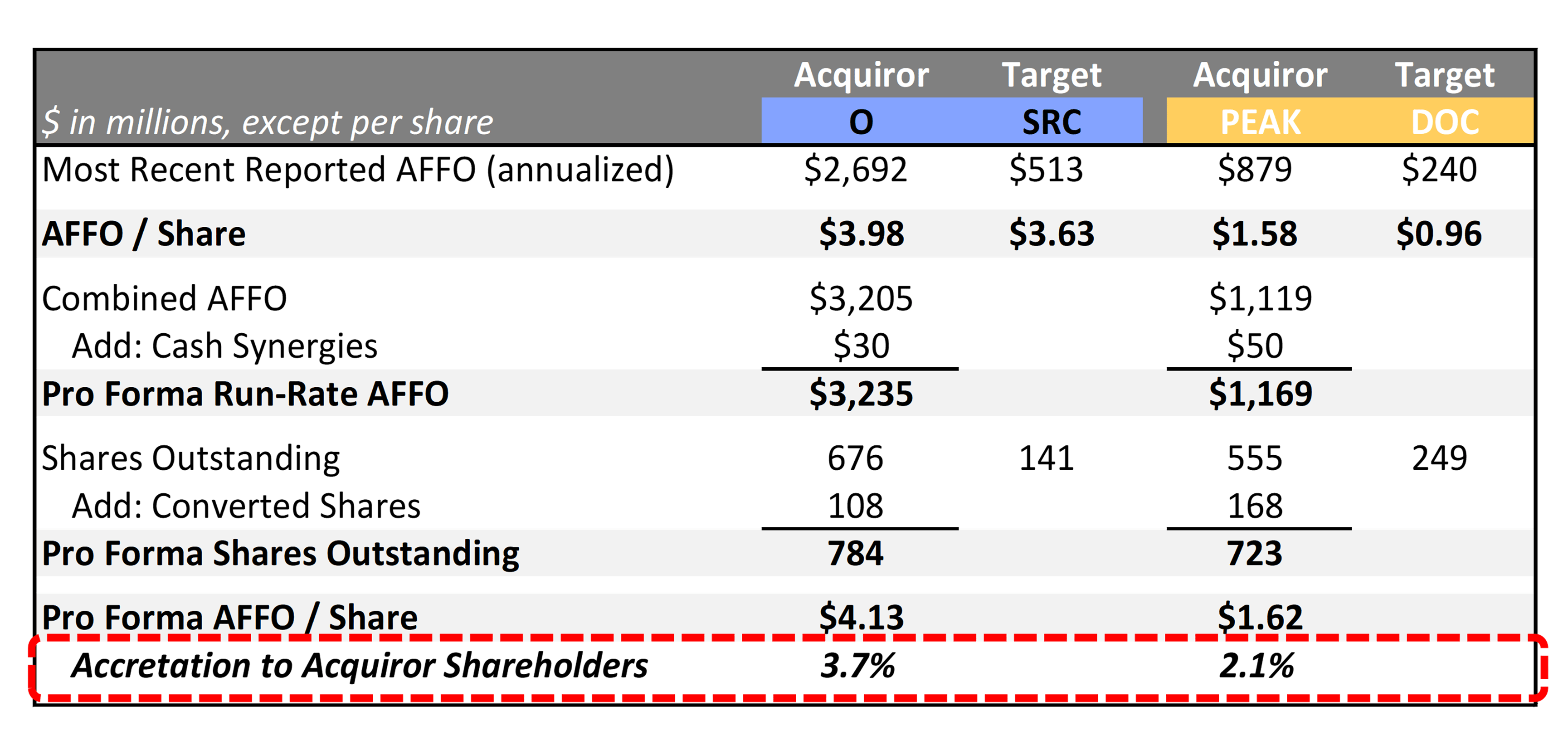

In terms of accretion to AFFO (i.e. cash earning), O's merger presentation states that management expects the transaction to be over +2.5% accretive to O's AFFO per share. While PEAK's management did not explicitly say how accretive they expect the transaction to be, they did indicate that the merger should be accretive to both company's shareholders . Comparing the two transactions and assuming that the expected synergies are achieved, the O/SRC merger is the clear winner as I estimate that O shareholders should see earnings accretion of +3.7% compared to PEAK shareholders of +2.1%. Given that the O/SRC merger has nearly double the earnings accretion relative to the PEAK/DOC merger, it is even more surprising that the combined Enterprise Value (EV) of O/SRC declined -2.5% compared to the combined Enterprise Value (EV) of PEAK/DOC declining only -1.2%.

{kind=link}

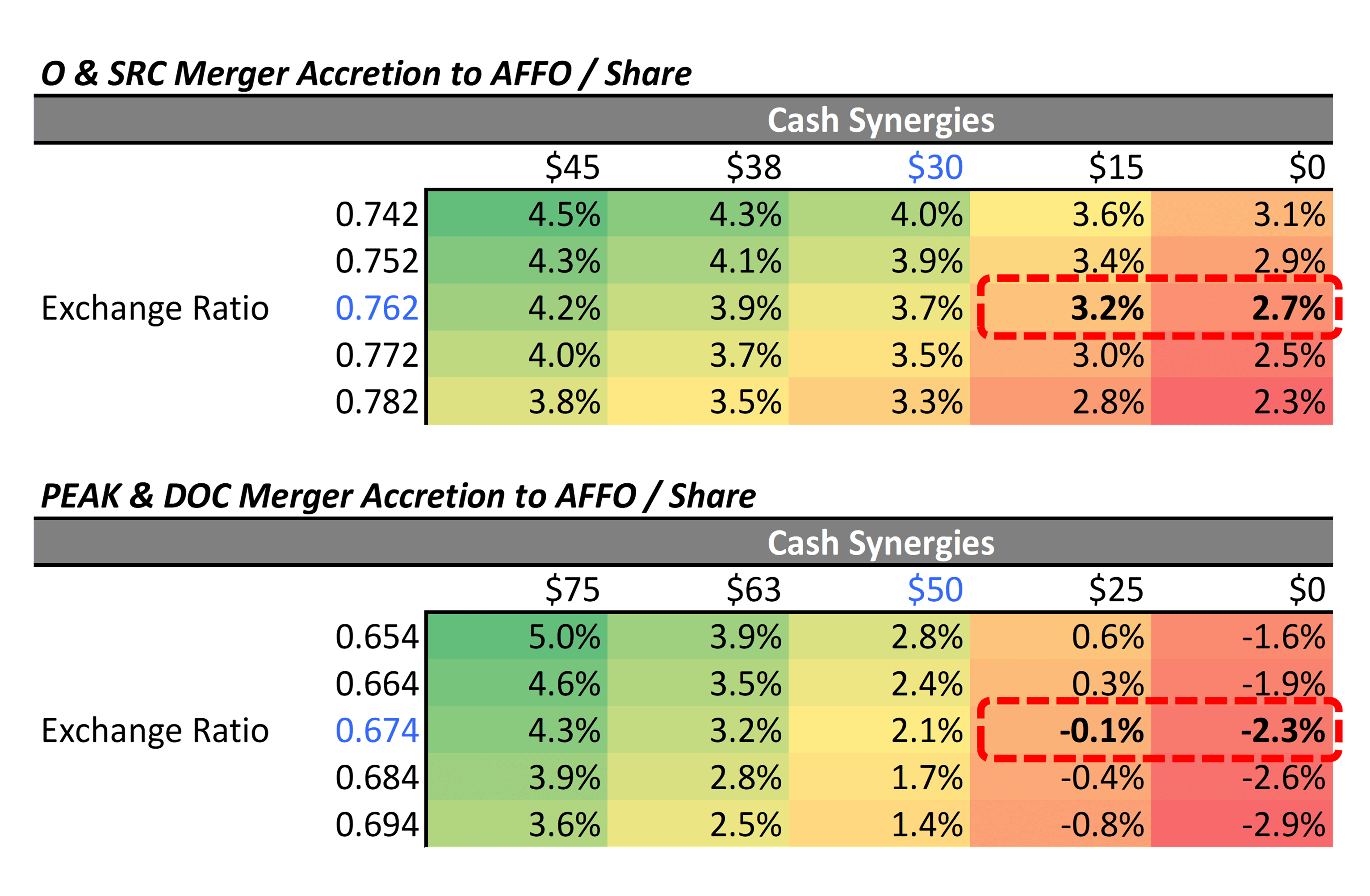

While synergies are often a key motivating factor behind mergers, reality often turns out to be less rosy than the investment bankers' estimates when the merger is pitched. I estimate that even if no synergies are realized, the O/SRC merger will still be +2.7% accretive to O shareholders. On the other hand, given a considerably narrower valuation gap between the shares of PEAK and DOC, I estimate that the PEAK/DOC merger requires synergies in order to be accretive. I estimate that the post-merger PEAK/DOC REIT will need to recognize at least half of its estimated synergies in order for the merger to be accretive, and the earnings accretion will actually turn to dilution of -2.3% in the event that no synergies are realized.

While I have no reason to think that the estimated synergies from either transaction will surprise to the downside, the fact that the PEAK/DOC merger requires synergies to be accretive, makes me considerably more bullish on the O/SRC merger.

{kind=link}

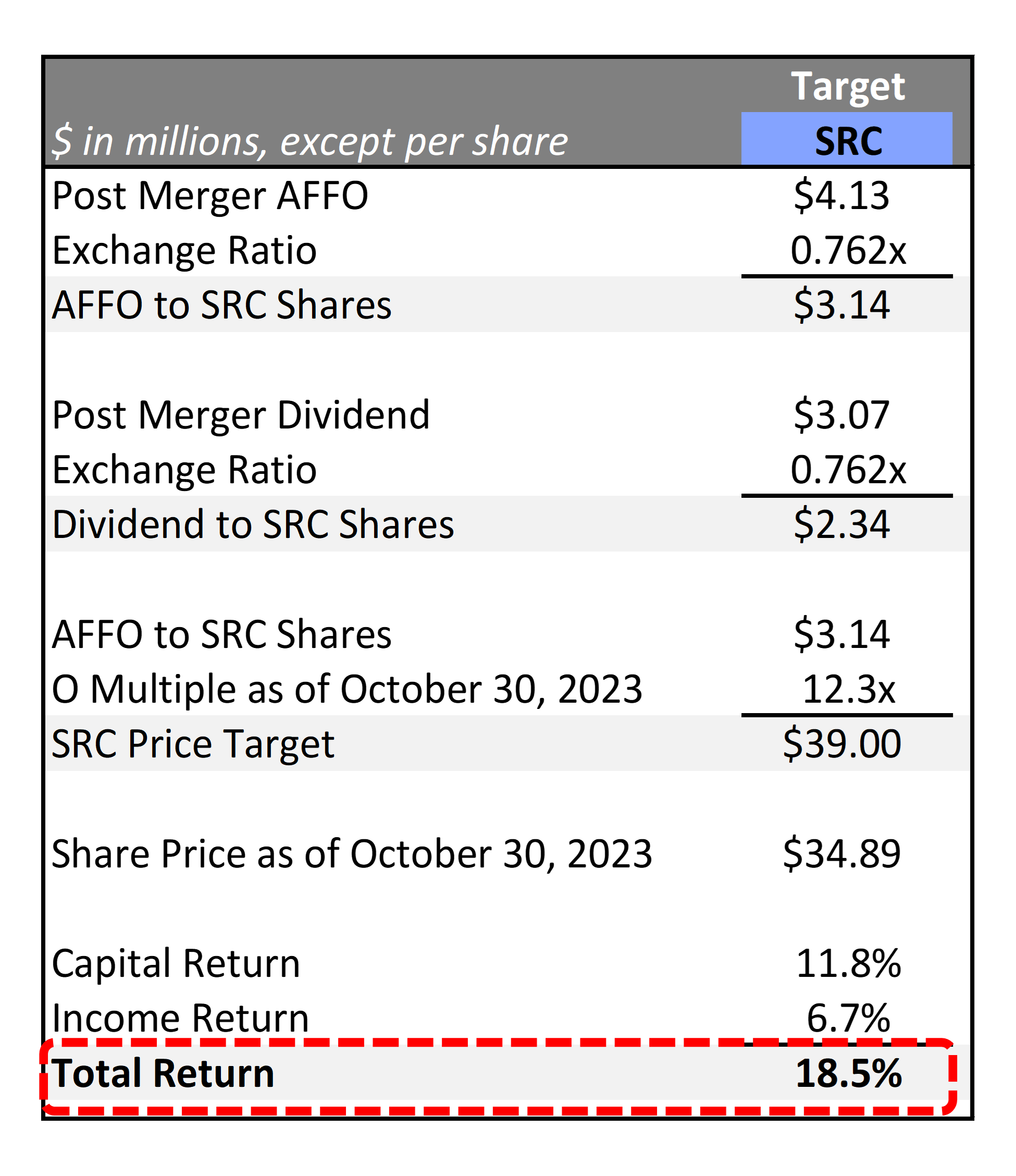

Turning to valuation, I estimate that O shares currently trade at an 11.2x multiple on higher post-merger earnings compared to a 12.3x multiple on lower pre-merger earnings as of Friday, demonstrating a compelling value opportunity given that the company just announced a merger that should be accretive to O shareholders even if no synergies materialize. However, given that SRC is currently trading below its exchange ratio with O, means that investors can buy shares of O at an 11.1x multiple (-0.1x relative to buying shares of O directly) by purchasing shares of SRC today.

{kind=link}

Assuming an investor purchases shares of SRC today at $34.89, the merger closes, and O shares re-rate to the same 12.3x multiple that they were trading at on Friday (before the merger was announced), investors should realize a capital return of 11.8% along with an income return of 6.7% (O's pro rata dividend to SRC shareholders) for a total annualized return potential of 18.5%, representing what is in my opinion a compelling opportunity with minimal risk.

{kind=link}

For further details see:

REIT Merger Standoff: Spirit Realty The Clear Winner With A Low Risk Potential 18.5% Return