RTMNF - Reitmans Is Starting To Look Like A Value Trap

2023-07-05 12:29:27 ET

Summary

- The company’s net sales rose by 7.2% in Q1 FY24, but it seems that the company is losing market share.

- In addition, adjusted EBITDA went into the red as rent levels and salary expenses increased.

- In my view, EBITDA for FY24 could be negative and there are no catalysts on the horizon for the share price.

- I think that risk-averse investors should avoid this stock.

Introduction

In April, I wrote an article on SA about Canadian specialty apparel retailer Reitmans ( RET.A.CA ) (RTMAF) ( RET:CA ) (RTMNF) in which I said that there were no significant catalysts for the next few months and that the company could be in the red for Q1 FY24.

Well, Reitmans released its Q1 FY24 financial results on June 14, and adjusted EBITDA slipped into the red despite a 7.2% increase in net sales. It seems that rent expenses and labor costs are rising and I'm concerned that the company could be in the red for the full fiscal year. In addition, Reitmans seems to be losing market share as apparel retail sales in Canada have been rising by double digits over the past few months. Overall, I'm keeping my rating on the stock at neutral. Let's review.

Overview of the Q1 FY24 financial results

In case you're not familiar with Reitmans or my earlier coverage, here's a brief description of the business. The company was established in 1926 and is a family-owned clothing retailer with over 400 stores across Canada under the Reitmans, Penningtons, and RW&CO brands. Reitmans focuses on specialty fashion, Penningtons specializes in plus-size fashion, and RW&CO is a ready-to-work fashion brand. The stores are primarily located in malls and retail power centers and e-commerce accounts for about a quarter of revenues. In Q1 FY24, the number of stores remained unchanged as the company opened two stores and closed another two.

Reitmans

Back in 2020, Reitmans had a network of 576 stores, but COVID-19 lockdowns led to mounting losses which forced the company to seek creditor protection and restructure its business. In January 2022, Reitmans emerged from restructuring proceedings after closing its Thyme Maternity and Addition Elle banners, shutting down 140 stores, and firing about a quarter of its workforce. With COVID-19 lockdowns ending, retail leases renegotiated at lower price levels, and unprofitable stores closed, the company booked an operating income of $15.3 million and $34.3 million in FY22 and FY23, respectively. In addition, Reitmans has no debt and in February 2023, Canadian asset management firm Donville Kent said that its real estate assets in Montreal could be worth C$240 million ($181.1 million).

Turning our attention to the Q1 FY24 financial results, I think that the expectations of investors were low considering former CEO Stephen Reitman had warned about headwinds related to the economic environment that could persist through the first part of fiscal 2024. Well, net sales for Q1 FY24 rose by 7.2% year on year to C$165 million ($124.5 million) thanks to higher in-store traffic as well as improved sales dollars per unit. While this might seem like a good result at first sight, there are several red flags here. First, the sales increase came from physical stores as e-commerce sales inched down by 0.7%. I find this disappointing considering Reitmans launched in February an online marketplace named RCL Market and I was expecting to see a significant increase in e-commerce sales thanks to it.

Reitmans

Second, data from Statistics Canada showed that clothing and clothing accessories retail sales in the country have strong momentum and are still growing by double digits. In April, they rose by 12% year on year to C$2.93 billion ($2.21 billion). This means that despite growing sales by 7.2% in Q1 FY24, Reitmans lost market share during the period.

{kind=link}

Third, among the key drivers behind the increase in the sales of Reitmans in Q1 FY24 was higher promotional activity, and this led to a decrease in the gross profit margin to 53.4% from 54.6% a year earlier. Coupled with an 8.6% increase in selling, distribution and administrative expenses, this led to adjusted EBITDA for the period turning negative.

Reitmans

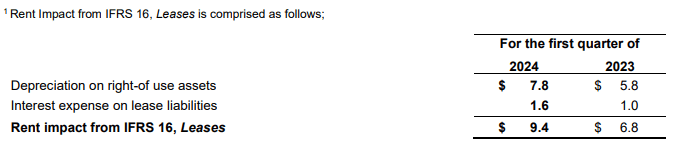

The key reasons selling, distribution and administrative expenses rose by C$7.3 million ($5.5 million) year on year include higher store operating costs as Reitmans hired more people to support the increased sales as well as higher head office and distribution center personnel costs as a result of salary increases. In addition, previous preferential rent arrangements were renewed at closer to market lease rates. This drove up rent expenses significantly, and I'm concerned that the higher SG&A costs and the expiry of more preferential rent arrangements over the coming months could push Reitmans into the red for FY24.

{kind=link}

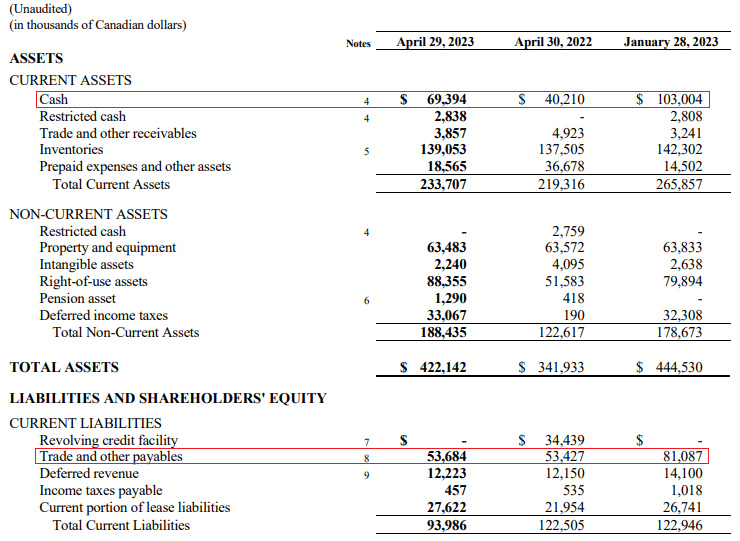

Looking at the balance sheet, the current portion of lease liabilities rose to C$27.6 million ($20.8 million) as of April 29, 2023, compared to C$22 million ($16.6 million) a year earlier. Another major change during the quarter was a C$33.6 million ($25.4 million) quarter on quarter decrease in the cash position of Reitmans as trade and other payables declined.

{kind=link}

Looking at the valuation, Reitmans has a market capitalization of C$159.3 million ($120.2 million) as of the time of writing. This puts the enterprise value at just C$87 million ($65.7 million), which is just over a third of the possible valuation of the company's real estate assets in Montreal. Yet, I don't think it's unlikely that the market valuation of Reitmans will increase much over the coming months. You see, the company has given no indication that it plans to sell real estate assets. In addition, the has been no news of an uplisting to the TSX and the resumption of dividend payments seems unlikely as financial results have been deteriorating over the past few quarters. Overall, I think that FY24 could be a tough year for the company as rent levels and salary expenses increase.

Investor takeaway

In my view, Reitmans posted mixed Q1 FY24 financial results. While net sales rose by over 7%, it seems that the company is losing market share and I'm concerned by the weak e-commerce sales in light of the launch of a new online marketplace in February. In addition, higher rent prices are starting to bite, and I think that EBITDA could be negative for FY24. While Reitmans has significant cash reserves and its real estate assets in Montreal could be worth almost three times its EV, there are no catalysts on the horizon for the share price and I think that Reitmans could be turning into a value trap. In my view, it could be best for risk-averse investors to avoid this stock.

For further details see:

Reitmans Is Starting To Look Like A Value Trap