RTMNF - Reitmans: Mixed Q4 FY23 Results And Dim Outlook And I'm Out (Rating Downgrade)

2023-04-17 23:59:59 ET

Summary

- The company posted weak sales growth in Q4 FY23, but the gross margin grew, and the operating loss was in line with my expectations.

- There was no news in the financials related to the perceived catalysts here – stock uplisting, dividend resumption, or asset sales.

- In addition, the CEO spooked investors about macroeconomic headwinds for Q1 FY24 and the share price sank by over 20% on Friday.

- In my view, Reitmans is still cheap but there are no significant catalysts for the next few months, and it could be a bumpy ride for the share price.

- I've closed my position for the time being and I’ve redeployed capital to shares of DATA Communications Management and Friedman Industries.

Introduction

In February, I wrote a bullish article on SA about Canadian women’s clothing retailer named Reitmans ( RET.A.CA ) ( OTCPK:RTMAF ) ( RET.CA ) ( OTCPK:RTMNF ) in which I said that it looked like a good turnaround story and that institutional investors were finally starting to take notice of the improvement in the fundamentals. I added that there was very little difference between the common and Class A shares and that I expected the 24% difference in their price to close soon.

Well, the share price gap had closed significantly by the middle of last week, but it then widened to 13.8% on Friday as the common shares lost 21.1% while the Class A shares slumped by 26.8% on the TSX as Reitmans released its Q4 FY 2023 financial results. In my view, the financials were mixed, and the outlook looks grim which is why I decided to close my position. I’m changing my rating to neutral as it seems there is at least one bumpy quarter ahead. Let’s look at the good, the bad, and the ugly in the Q4 FY23 financial results of Reitmans.

The good

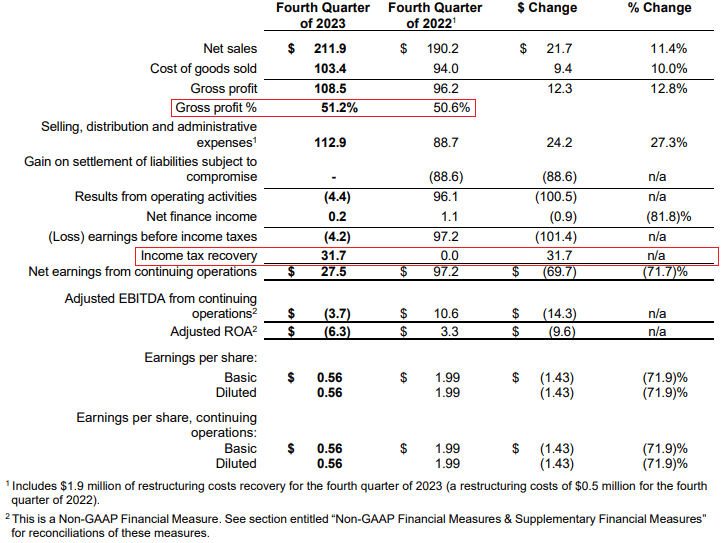

Net sales rose at a decent pace of 11.4% in Q4 FY23 to C$211.9 million ($158.5 million) and I think that it was a pleasant surprise for investors that the gross profit margin grew by 60 basis points to 51.2% considering the Canadian clothing retail sector has been under pressure by cost inflation over the past year. The reason for the improvement of the gross margin was lower promotional activity as well as lower overall supply chain costs as global supply chain issues diminished. Compared to Q4 FY22, Reitmans used less air freight for its products. Reitmans also booked a C$31.7 million ($23.7 million) of income tax recovery in Q4 FY23 as a result of the recognition of previously unrecognized deferred tax assets on all temporary differences and operating losses carried forward relating to its Canadian operations. Basically, the company plans to take advantage of its net operating loss carryforward from its restructuring days as it expects to remain profitable in the future. Definitely a positive development.

{kind=link}

{kind=link}

Back in February, I forecast that Reitmans would book an operating loss of between C$3 million ($2.2 million) to C$5 million ($3.7 million) in Q4 due to cost inflation pressure and I consider it a positive development that the operating loss came in at C$4.4 million ($3.3 million). Yet, it seems that many Reitmans investors were much more optimistic than me as there were forecasts on the message boards on Stockhouse that included operating income of above C$10 million ($7.5 million).

Moving on to the balance sheet, I said in February that I expected the cash balance to increase significantly in Q4 as the holiday season is usually marked by destocking. Well, cash and cash equivalents soared by C$38.7 million ($29 million) quarter on quarter as inventories decreased by C$17.4 million ($13 million) while trade and other payables shrank by C$14.7 million ($11 million). As you can see from the table below, inventory levels were still higher than a year ago, but I don’t expect them to fall any further as revenues are higher now.

Reitmans

The bad

Moving on to the disappointing parts of the Q4 FY23 financial report, I think we have to start with what was missing in the results announcement. You see, with the cash position increasing, many retail investors that are active on the Stockhouse message boards expected at least some hint of an uplisting of the stock or a resumption of dividend payments. There was none of that in the report and in addition, Reitmans isn’t planning to sell any real estate assets for which Canadian asset management firm Donville Kent seems to be pushing. The latter recently said that the real estate assets of Reitmans in Montreal could be worth C$240 million ($179.6 million). Well, the deferred income tax assets relating to allowable capital losses were not recognized as of January 28 as Reitmans revealed in its Q4 FY23 financial report that it’s not probable that sufficient future taxable capital gains will be available from the Canadian operations to utilize the benefits.

Reitmans

In addition, I think that the sales growth for the quarter was underwhelming as clothing and clothing accessories retail sales across Canada have been expanding by over 20% year on year over the past few months. Considering the net sales of Reitmans grew by just 11.4% during Q4, it seems that the company is rapidly losing market share to competitors such as Aritzia ( ATZAF ) ( ATZ:CA ). Reitmans could be in serious trouble from a net sales point of view if demand for discretionary goods in Canada declines due to high inflation and lower disposable income in FY24.

{kind=link}

Finally, I find it disappointing that CAPEX for FY24 is forecast to be just C$20 million ($15 million) as this leads me to think that Reitmans will open only a few stores over the coming months. You see, the company’s CAPEX for FY23 stood at C$10.7 million ($8 million), and only eight stores were opened during the period.

{kind=link}

The ugly

In my view, the main reason that the market capitalization of Reitmans tanked on Friday was this statement from President and CEO Stephen Reitman when the Q4 FY23 results were released:

"I am extremely proud of our team's performance in fiscal 2023 after exiting from the Companies' Creditors Arrangement Act in January 2022 with net sales up 20.9% over fiscal 2022. And despite near term headwinds related to the economic environment, which impacted our performance in the fourth quarter of 2023 and which may persist through the first part of fiscal 2024 , we remain excited about our strong competitive positioning and ability to serve our customers, as we work towards delivering on our long-term growth aspirations". - source

Considering clothing retail sales in Canada are booming at the moment and the gross profit margin of the company is growing, it’s unclear what headwinds Stephen is referring to here and I think this statement caught many investors off guard. Since he said that the headwinds could affect Q1 FY24 results, I think this has cost the stock a lot of momentum and created a rout in the market on Friday. The trading volume for both classes of shares combined is usually below 70,000 shares and on Friday, it surpassed 690,000 shares as investors rushed for the exits.

Investor takeaway

I think that the Q4 FY23 financial results of Reitmans were good in terms of margins although sales growth was disappointing. Also, many people expected news about an uplisting or resumption of dividends but what I think was the main reason behind the slump in the share price on Friday is a statement from the CEO about macroeconomic headwinds in Q1 FY24. In my view, it cost the stock a lot of momentum as it seems that the company could be in the red for the current fiscal quarter.

Overall, I continue to think that Reitmans is undervalued as the business is likely to remain profitable over the coming years and cash has increased to C$103 million ($77.1 million). The company has no debt, and its market capitalization is just C$152.5 million ($114.1 million) as of the time of writing. However, there are no significant catalysts for the next few months, and it could be a bumpy ride for the share price. In view of this, I’m changing my rating on the stock to neutral and I've closed my position for the time being. I’ve put the sale proceeds into shares of Canadian business communications solutions company DATA Communications Management ( DCM:CA ) ( OTCQX:DCMDF ) and U.S. steel service center operator Friedman Industries ( FRD ).

For further details see:

Reitmans: Mixed Q4 FY23 Results And Dim Outlook And I'm Out (Rating Downgrade)