SRVR - REITs: Ever Changing Ever Valuable

2023-06-08 14:20:00 ET

Summary

- In recent years, specialized technology-adjacent property types such as towers, data centers and industrial have gained prominence in the real estate market due to changes in consumer behavior, technological advancements, and their critical role in supporting the modern economy.

- The REIT universe looks much different today, appropriately reflecting the changes that are happening all around us.

- REITs are not just constrained to malls and offices; quite the contrary, the REIT sector is a dynamic one, with exposure to both secular growth dynamics and sources of bulwark stability.

By Blair Schmicker, CFA, Portfolio Manager, Research Analyst, Franklin Equity Group | Daniel Scher, Portfolio Manager, Research Analyst, Franklin Equity Group

Until recently, office buildings were the pinnacle of commercial real estate - skyscrapers stretched perception and awed as symbols of prestige and value. Malls were the buttressed center of communities, where young people reliably gathered to hang out at the video arcade and their families would do what Americans do best: consume. What happens when behaviors change? Franklin Equity Group Portfolio Managers Blair Schmicker and Daniel Scher reflect on the ever-evolving landscape of commercial real estate, and the answer to that question might surprise you.

Digital disruption has come for real estate!

That's the headline, right? First, e-commerce emptied brick-and-mortar retail stores and malls, and now, offices have been laid bare by technology tools that make work-from-home a durable reality. If you only read the headlines, you might expect this spells doom for commercial real estate in general, and for real estate investment trusts (REITs) in particular.

At its core, the value of real estate lies in the land, not the structure. That's what the colloquialism "location, location, location" means. And the best, highest-value use of land is always changing. I [Blair] learned this lesson first-hand as the child of a real estate investor/developer. My father preferred the backwaters of real estate-marinas and mobile home parks-rather than shiny office buildings. But it was his discovery of a specific up-and-coming backwater in the late-1980s that turned odd parcels of unloved but well-located land into gold that built his career. What was it? Self-storage, which has since emerged from the backwaters to be one of the most important subsectors within the US REIT universe.

It shouldn't be surprising to learn that the composition of the investable REIT universe has continually evolved to favor the disruptors over the disrupted. Indeed, the REIT landscape has seen significant changes over the past decade, reflecting shifts in the real estate market and investor preferences. While it's true that malls and office space used to be the pinnacle of commercial real estate as measured by value, that's no longer the case. The base building block of commercial real estate is land. How the economy has deployed inherently scarce land has evolved over time, and equity markets have adjusted in tandem to reflect this evolution.

In recent years, specialized technology-adjacent property types such as towers, data centers and industrial have gained prominence in the real estate market due to changes in consumer behavior, technological advancements, and their critical role in supporting the modern economy. Cell towers, for instance, have become crucial in supporting wireless communication infrastructure with the proliferation of smartphones and wireless devices. Data centers have seen significant demand growth as the reliance on cloud computing and data storage continues to increase. Meanwhile, the industrial subsector has seen a surge in demand amid the rise of e-commerce, because fulfillment of online orders requires roughly three times the logistics footprint of traditional brick-and-mortar. Simultaneously, the value ascribed to disrupted property sectors like malls and office has eroded considerably, reflecting the new realities of the economy.

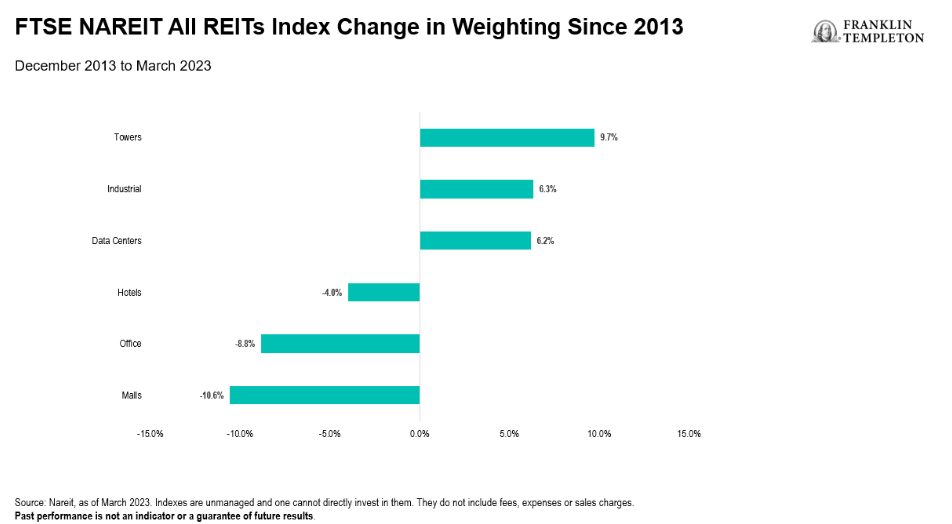

To provide some quantification of these changes, in December 2013, malls and office comprised more than a quarter of the market capitalization-weighted FTSE NAREIT All REITs Index. 1 By contrast, technology-adjacent subsectors (towers, data centers and industrial) comprised, in aggregate, just 14% of the index. 2 Times have changed, but the relative importance of these subsectors has changed within the index, too.

As shown in Exhibit 1, the index's weighting to towers increased nearly 10% in the roughly 10 years through March 2023, while the weightings to industrial and data centers have each grown more than 6%. In contrast, the importance of malls (as measured by benchmark weighting) has fallen more than 10%, traditional office has declined nearly 9%, and even hotels has fallen by 4%.

Exhibit 1: Change in Key REIT Sectors, FTSE NAREIT All REITs Index, December 2013 to March 2023

{kind=link}

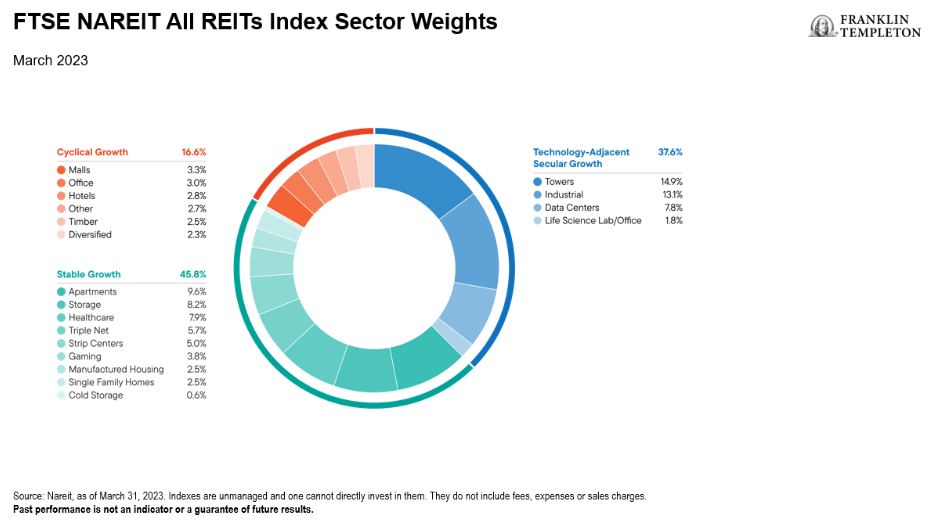

Consequently, the REIT universe looks much different today, appropriately reflecting the changes that are happening all around us (Exhibit 2). Malls and traditional office REITs combined have fallen to only 6%, with office, in particular, comprising only 3%. 3 Meanwhile, the technology-adjacent subsectors mentioned above now comprise over 35% of the index. Additionally, an array of other new and emerging growth areas has emerged within REITs, including gaming, manufactured housing, single-family homes, self-storage, health care and cold storage. Several of the other more mature subsectors such as multifamily, neighborhood centers and single-tenant triple net lease 4 each possess stable demand drivers of their own.

Exhibit 2: FTSE NAREIT All REITs Index, March 31, 2023

{kind=link}

REITs are not just constrained to malls and offices; quite the contrary, the REIT sector is a dynamic one, with exposure to both secular growth dynamics and sources of bulwark stability. We believe active management of portfolios can further augment each of these investable aspects.

Digital disruption has come for real estate, indeed. But the investable universe already reflects these changes. In our view, an investment in REITs today is much more an allocation into the physical assets that empower the business models of the disruptors than it is a claim of value on the assets that are being disrupted. For this reason, we see tremendous opportunity in the asset class.

What Are The Risks?

All investments involve risks, including the possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stocks historically have outperformed other asset classes over the long term but tend to fluctuate more dramatically over the short term. Bond prices generally move in the opposite direction of interest rates. Thus, as the prices of bonds adjust to a rise in interest rates, the share price may decline.

The risks associated with a real estate strategy include, but are not limited to various risks inherent in the ownership of real estate property, such as fluctuations in lease occupancy rates and operating expenses, variations in rental schedules, which in turn may be adversely affected by general and local economic conditions, the supply and demand for real estate properties, zoning laws, rent control laws, real property taxes, the availability and costs of financing, environmental laws, and uninsured losses (generally from catastrophic events such as earthquakes, floods and wars).

Investments in alternative investment strategies are complex and speculative investments, entail significant risk, and should not be considered a complete investment program. Depending on the product invested in, an investment in alternative investments may provide for only limited liquidity and is suitable only for persons who can afford to lose the entire amount of their investment.

Additionally, investments in private securities and obligations may be thinly traded, have no ready market or exchange and require private negotiation, and which may be restricted as to their transferability. These factors may limit the ability to sell such securities at their fair market value.

1. Source: Nareit, as of March 31, 2023. Data has been adjusted to exclude mortgage REITS. Franklin Templeton has adjusted subsector classifications to improve clarity.

2. Ibid.

3. Ibid.

4. Single-tenant/freestanding assets leased on a long-term basis; the tenant pays the full expenses of the property.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

REITs: Ever Changing, Ever Valuable