PLDGP - REITs For Rip Van Winkle

Summary

- The Rip Van Winkle approach to investing is one in which an investor initially pays a reasonable price for a quality business.

- Just like me, Rip Van Winkle can sleep another 10-15 or 20 years and wake up a wealthy investor.

- That's how SWAN investing works, you can practically ignore Mr. Market, as long as you have a strong conviction about what the company is really worth.

I’m sure you’ve heard the story of the fictional Dutch villager named Rip Van Winkle. He lived at the foot of New York's Catskill Mountains, where he enjoyed wilderness activities (admittedly I had to get a refresher on Wikipedia ).

One day, he was strolling up the mountains when he ran across a man trying to carry a keg. Together the two continued until they heard loud noises. When they got closer, they spotted a lavishly dressed bearded man playing ninepins. Van Winkle did not ask who they were, but instead kept on drinking more of their moonshine.

When he awakened, he discovered that his beard was over a foot long and his musket was rotting and rusty. As he walked back into the town, he learns that the American Revolution had ended and that George Washington was in charge, not King George III.

Rip Van Winkle had been asleep for over twenty years, and he had the luxury of sleeping through the difficulties of the American Revolution. So what does this story have to do with investing?

The Rip Van Winkle approach to investing is one in which an investor initially pays a reasonable price for a quality business.

Then, they sleep through the inevitable stock price ups and downs (though they are quite alert as to the operating performance of the business). Finally, they wake up in 5-10 years to find that they have made a considerable sum of money.

So now you see why I titled this article: REITs for Rip Van Winkle.

Prologis, Inc. ( PLD )

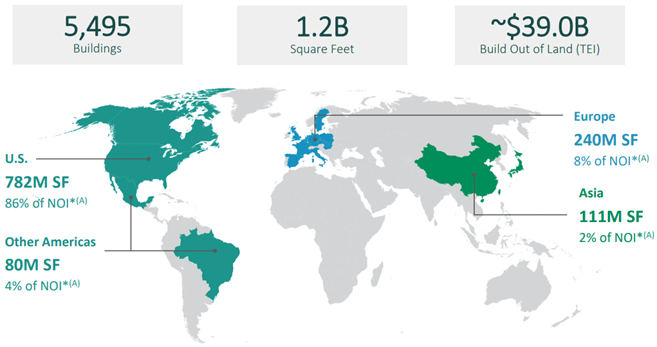

Prologis is a real estate investment trust (“REIT”) that specializes in industrial properties and logistical facilities. Prologis has an established international footprint, with 5,495 properties spread across 19 countries that serve 6,600 customers, mainly in business-to-business categories and online fulfillment. Prologis processes 2.8% of global GDP through its distribution centers.

PLD puts an emphasis on high growth markets and markets that have high barriers to entry. Their properties are in high demand, with a global occupancy rate of 98.2%. In all, they have 1.2 billion square feet of real estate and have $39 billion invested in land banks for future expansion.

{kind=link}

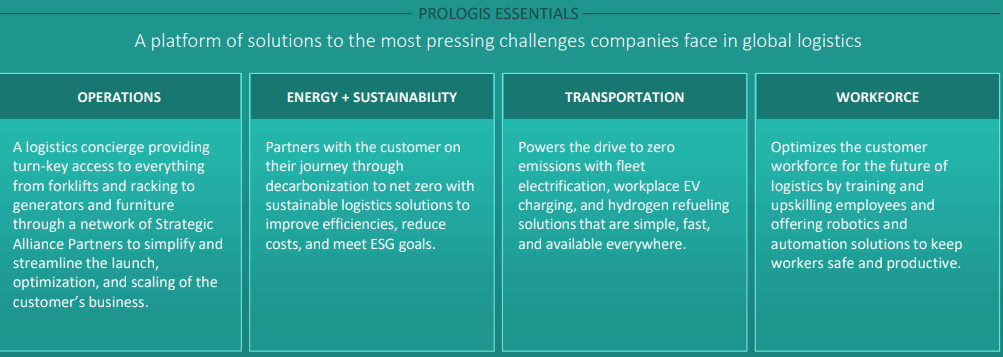

Along with rental revenue, Prologis has additional streams of income through their Prologis Essentials platform that includes products and services that offers solutions to their tenants.

The Essentials platform offers an array of services including warehouse racking, forklifts, moving and relocating services, workforce training, robotics and automation, and energy solutions through their solar panels and electric vehicle ("EV") charging stations.

{kind=link}

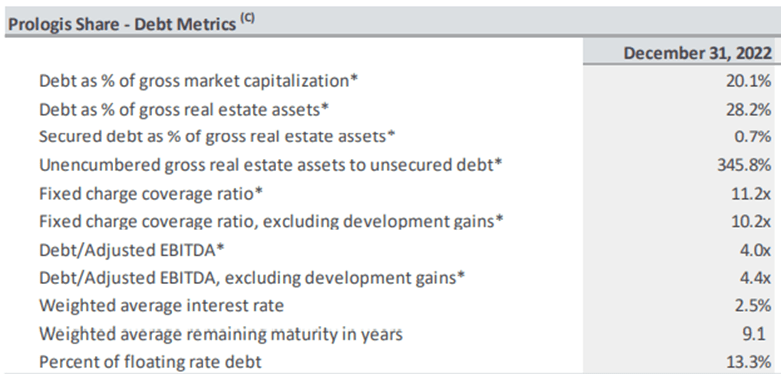

Prologis has one of the strongest balance sheets around with an A3/A credit rating by Moody’s & S&P. As of December 31, 2022, Prologis had a debt to adjusted EBITDA of 4.0x and a fixed charge coverage ratio of 11.2x.

Their weighted average effective interest rate is 2.5% and their weighted average to maturity is 9.1 years. As of December 31, 2022, Prologis had $3.9 billion availability under their credit facilities and $278 million in unrestricted cash for a total available liquidity of $4.1 billion.

{kind=link}

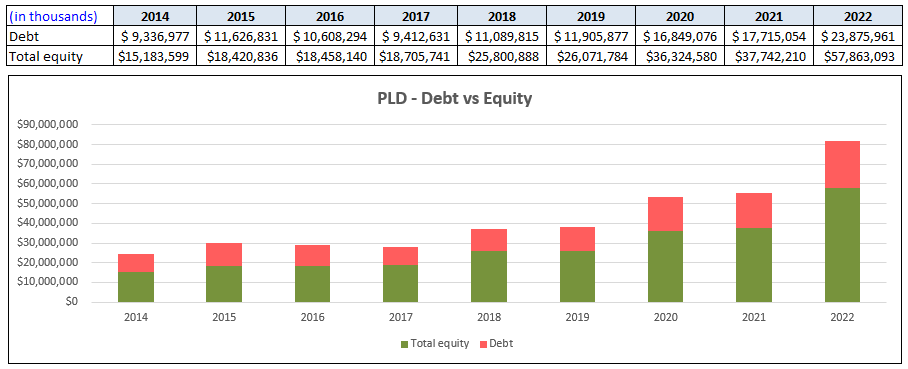

Prologis has a conservative capital structure, with the majority of its investments financed through equity. Their debt-to-equity ratio has been improving over the years, with a debt-to-equity ratio of 61.49% in 2014 vs a debt-to-equity ratio of 41.26% in 2022.

{kind=link}

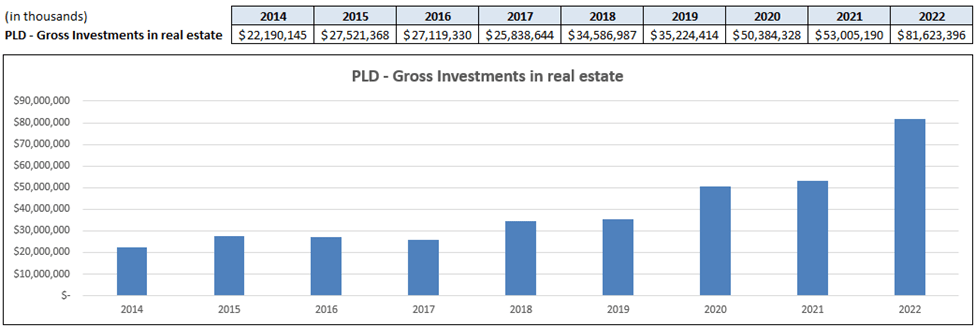

Prologis has grown its investments in real estate from $22.19 billion in 2014 to $81.62 billion in 2022. The large increase in 2022 was in part due to their acquisition of Duke Realty. In October 2022, Prologis announced the completion of its all-stock acquisition of Duke Realty.

The transaction was valued at approximately $23 billion and expanded Prologis’ exposure to key U.S. markets. In total, the acquisition added over 500 new customers and around 480 logistics buildings covering 42 million square feet. The chart below shows PLD’s gross real estate investments at cost and does not include depreciation.

{kind=link}

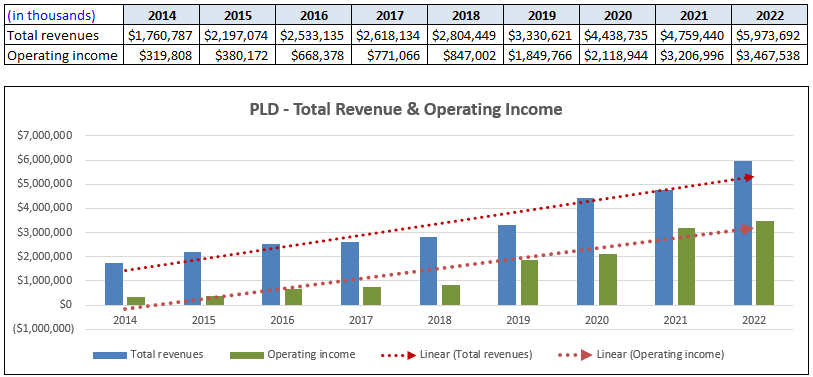

Their real estate investments have materialized in revenue and operating income growth. Since 2014, Prologis has grown its revenue at a compound annual growth rate of 16.50%.

{kind=link}

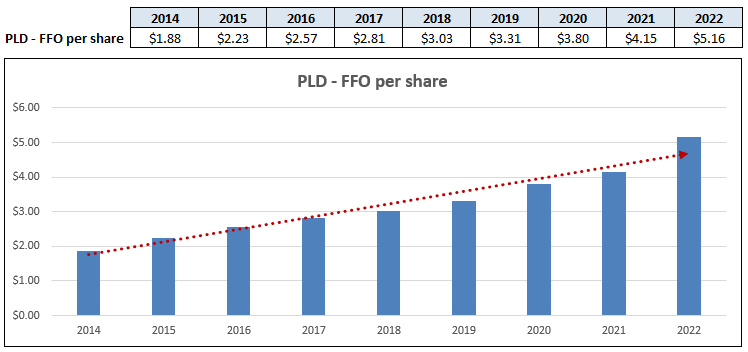

The growth in revenue and operating income has flowed through to the bottom line, with funds from operations (“FFO”) averaging a growth rate of 11.95% since 2014. Analysts project a 7% increase in FFO per share in 2023, a 2% increase in 2024, and a 14% increase in 2025.

{kind=link}

Prologis currently pays a 2.52% dividend yield that is secure with an AFFO (Adjusted FFO) payout ratio of 72.31%. Additionally, since 2014 PLD has an average dividend growth rate of 12.36%.

{kind=link}

Prologis is 1 of the 3 REITs we cover with a perfect quality score of 100 and is one of the highest-quality REITs you can own. They have excellent growth rates in revenue, operating income, funds from operations, and their dividend payout.

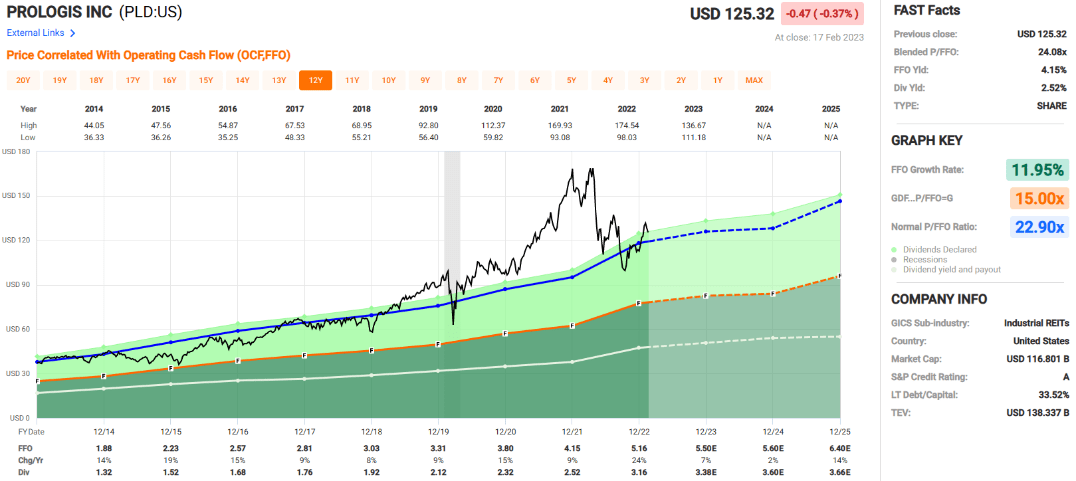

Additionally, they have some of the best debt metrics around and pay an above average dividend yield that is well covered. They are currently trading at a P/FFO of 24.08x, which is a slight premium to their normal multiple. At iREIT, we rate Prologis a BUY.

{kind=link}

Public Storage ( PSA )

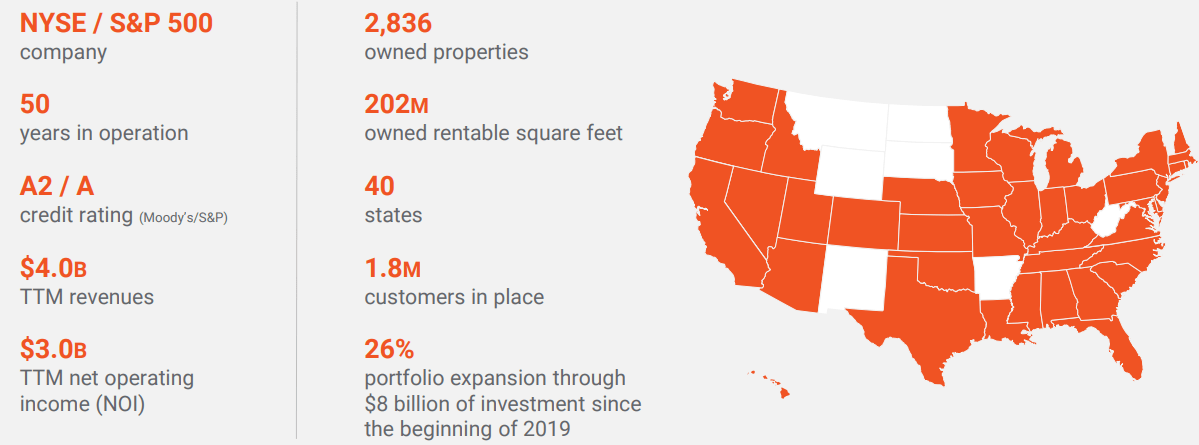

Public Storage is a REIT that specializes in self-storage facilities. They are the largest owner, operator and developer of self-storage properties, with 2,836 facilities across 40 states in the U.S.

Their properties cover more than 202 million net rentable square feet and serve approximately 1.8 million customers. Since 2019, PSA has invested $8.0 billion in acquisitions and development that has added 42 million square feet of real estate for a 26% increase in total portfolio size.

{kind=link}

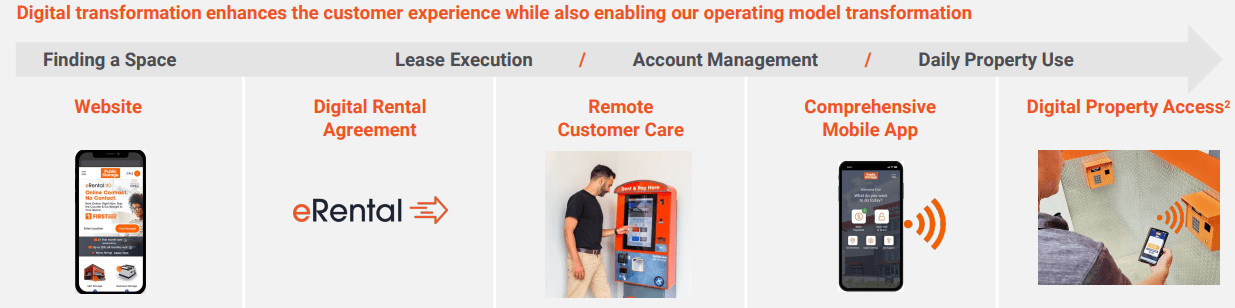

Public Storage has invested in technology to increase convenience and enhance the customer experience. They built a comprehensive mobile app with a click-to-call and AI-enabled chat where customers can get pricing and execute digital rental agreements.

At many of their locations they have installed remote customer care kiosks with leasing and account management functionality that also includes live-video customer service. Additionally, they have digital access systems and smart security cameras for convenience and safety.

{kind=link}

Public Storage has excellent credit and debt metrics. PSA has a credit rating of A2 / A by Moody’s and S&P respectively. As of the third quarter of 2022, PSA has a Debt to EBITDA of 2.2x, a Fixed Charge Coverage of 9.3x, and a Debt and Preferred to EBITDA of 3.6x.

Their long-term debt to capital is 40.20% and as of the third quarter 2022, PSA had $481.4 million available to them under their revolving credit facility and $883.8 million in cash and cash equivalents.

PSA Update

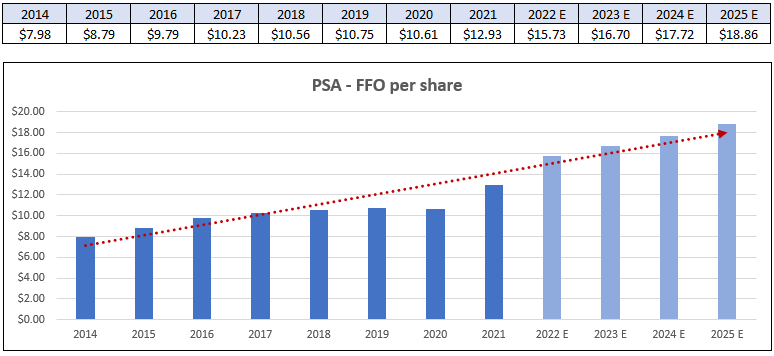

Since 2014, PSA has averaged a FFO per share growth rate of 7.95%. In that time, they increased FFO per share every year except 2020, when it declined by -1%. Analysts project FFO growth rates of 6% in years 2023, 2024 and 2025.

{kind=link}

From 2017 to 2021 Public Storage’s dividend remained fixed at $8.00 per share. In 2022 PSA’s normal dividend continued to be $8.00 per share, but they also paid a one-time special dividend of $13.15 per share in connection with the PS Business Parks merger.

Public Storage’s dividend growth in recent years has been less than desirable, but on February 5, 2023, PSA announced a 50% increase in their dividend. The quarterly dividend was raised from $2.00 to $3.00 per share for an annualized increase from $8.00 to $12.00 per share.

{kind=link}

Public Storage pays a 4.01% dividend yield. The AFFO payout ratio for 2022 comes in at 155.63%, but that is due to the special dividend of $13.15. If we back that amount out, their normal dividend of $8.00 gives us an AFFO payout ratio of 58.86% in 2022.

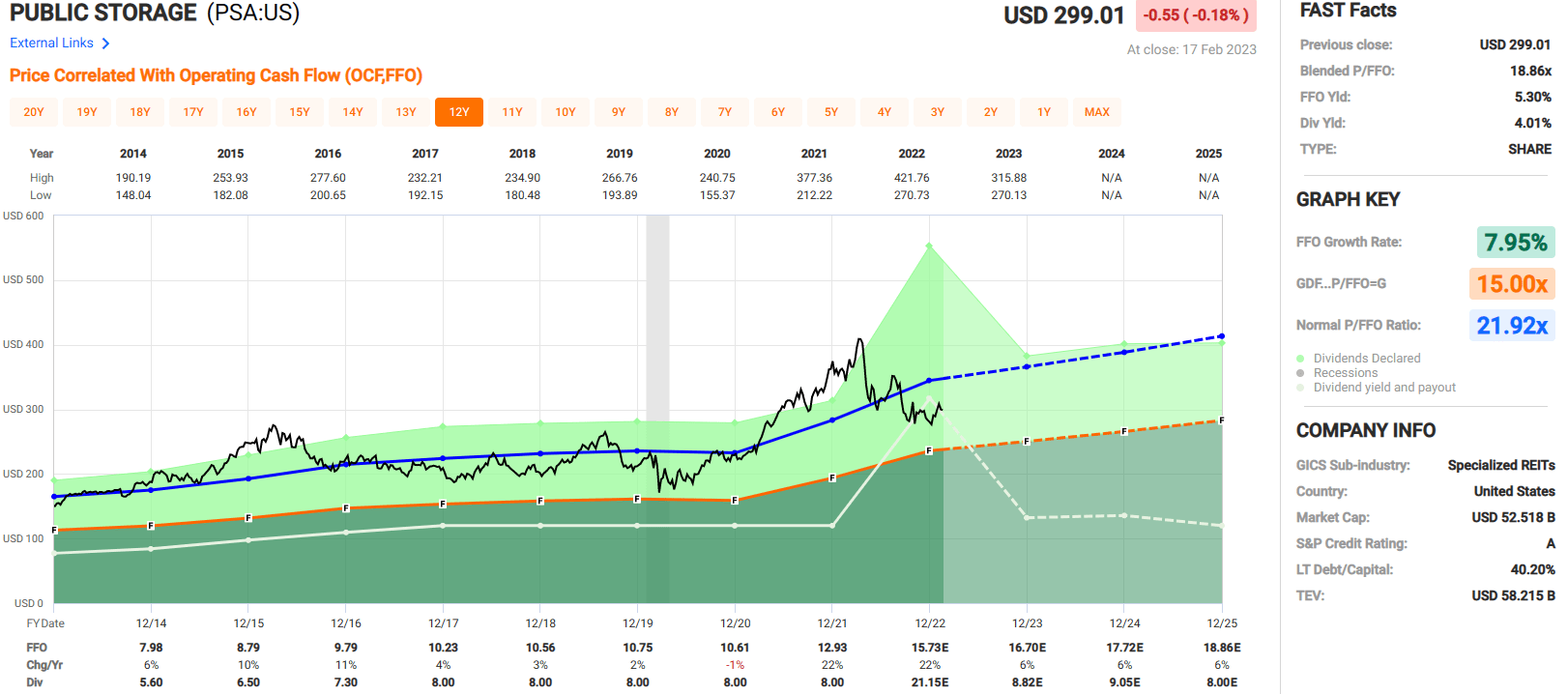

Currently PSA is trading at a P/FFO ratio of 18.86x, which is well below their normal P/FFO of 21.92x. Public Storage is a high-quality company with 50 years of operating experience and is the leader in the self-storage space.

PSA has excellent credit metrics and has delivered consistent high growth rates in funds from operations. PSA shows confidence in the future with their recent 50% dividend increase and are currently priced at a discount. At iREIT, we rate Public Storage a BUY .

{kind=link}

Essex Property Trust, Inc. ( ESS )

Founded in 1971 and publicly listed in 1994, Essex Property Trust is an internally managed REIT that acquires, develops, and manages multifamily apartment communities in supply-constrained coastal markets of California and Washington.

The Essex portfolio is concentrated in Southern California, the San Francisco Bay Area, and the Seattle metropolitan area and derives 42% of its net operating income (“NOI”) from Southern California, 40% from Northern California, and 18% from Seattle. In total, ESS is in 8 major markets with 253 apartment communities that contain approximately 62,000 apartment homes.

{kind=link}

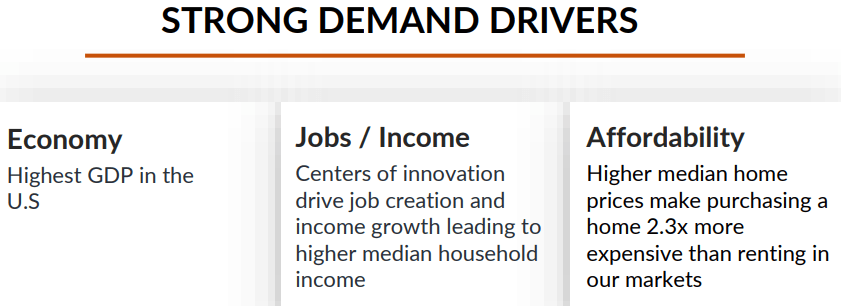

Essex strategically acquires properties in supply-constrained markets that have high demand. California and Washington combined make up the 5 th highest GDP in the world, with high paying jobs and a higher median household income. Affordability is another driver of demand, with high home prices that makes buying a house 2.3x more expense than renting.

{kind=link}

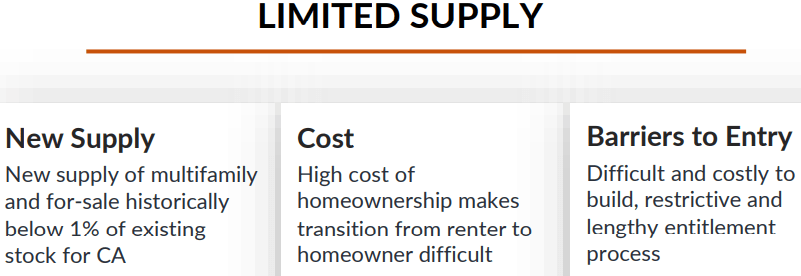

Along with strong demand, Essex’s markets have limited supply. New supply of apartments and for-sale residential properties is below 1% of the existing stock in California.

Additionally, the high cost of owning a home in Essex’s markets makes it difficult to transition from renting to owning a home, and the restrictive entitlement process creates barriers to entry for new supply to be built.

{kind=link}

Essex Property Trust has a solid balance sheet with $1.2 billion in liquidity and a BBB+ investment-grade credit rating. Their interest coverage is 567% and their Net Debt to Adjusted EBITDAre is 5.8x as of the third quarter in 2022.

This leverage ratio has been improving over the past several years, with Net Debt to Adjusted EBITDAre levels of 6.6x and 6.3x in 2020 and 2021, respectively, compared to their current ratio of 5.8x.

{kind=link}

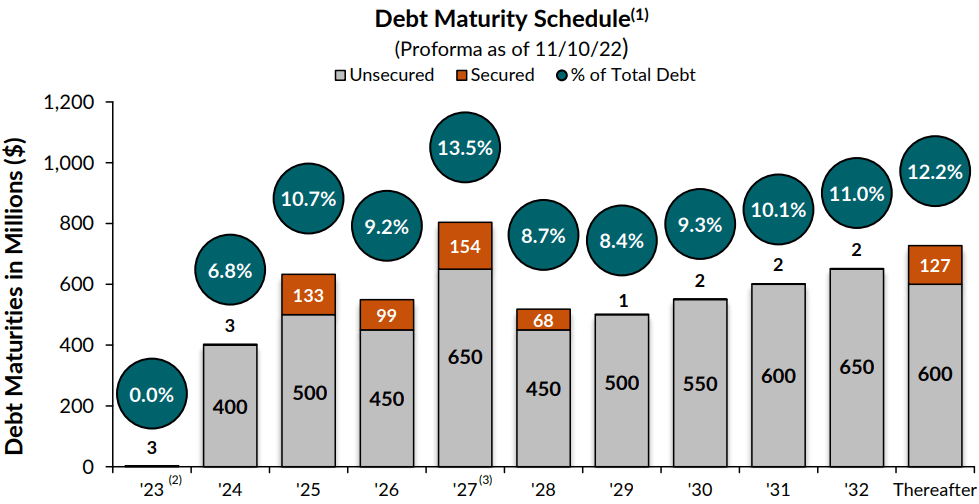

Additionally, only 11% of their debt is secured and they have a weighted average years to maturity of 7.7 years, with a weighted average interest rate of 3.3%. Their debt maturity schedule is well spaced out and they have no debt maturity due in 2023.

{kind=link}

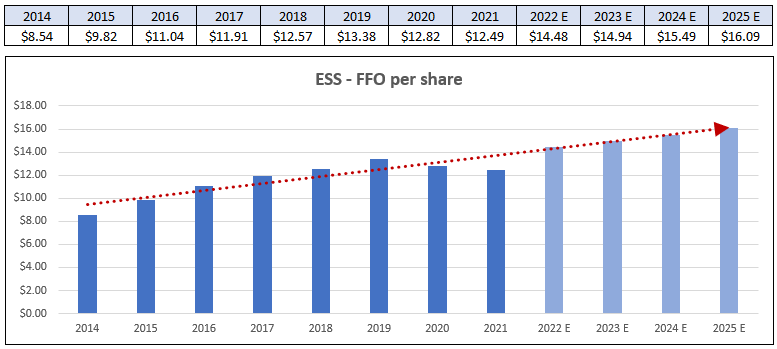

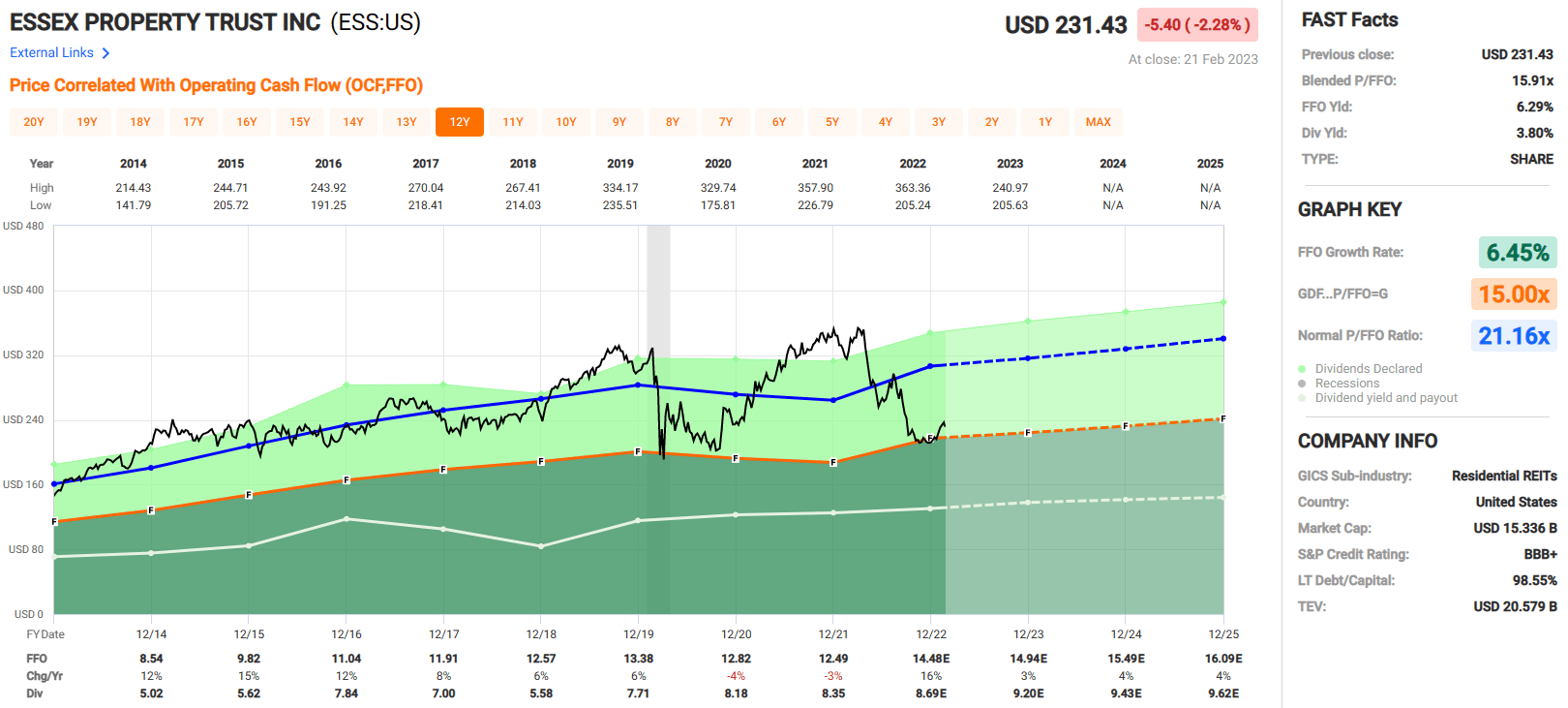

Essex has delivered an average FFO growth rate of 6.45% since 2014 and increased FFO each year except during 2020 and 2021, when FFO declined by 4% and 3%, respectively.

The expected FFO per share in 2022 is $14.48, which would be a 16% increase over the previous year. FFO growth is expected to normalize in the next several years, with projected growth rates of 3% in 2023 and 4% in 2024 & 2025.

{kind=link}

Essex is one of the few REITs that holds the status of an S&P Dividend Aristocrat. They have raised their dividend for 28 consecutive years for total cumulative dividend growth of 427% since their IPO in 1994.

Over the last ten years, they have an average dividend growth rate of 8.60%. They currently pay a 3.80% dividend yield that is well-covered, with an AFFO payout ratio of 68.13% in 2022.

ESS Investor Presentation

Essex’s stock has been beaten down recently, with a decline of 26.67% over the last year. The drop in share price has pushed their FFO yield up to 6.29% and their blended P/FFO multiple down to 15.91x, which is a significant discount to their normal FFO multiple of 21.16x.

Essex has delivered growth in its FFO and dividend for decades and is currently priced at an attractive level. At iREIT, we rate Essex Property Trust a STRONG BUY.

{kind=link}

American Tower Corporation ( AMT )

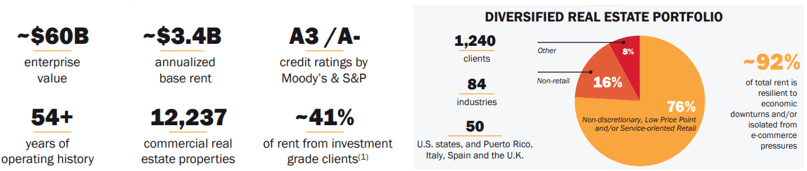

American Tower is the largest cell tower REIT, with around 223,000 communication assets across 25 countries on 6 continents. American Tower primarily owns cell towers, but has recently moved into the data center space with the acquisition of CoreSite in late 2021.

AMT is a global provider of wireless communications infrastructure that is critical for everyday activities like making a phone call or text or ordering a product online. E-Commerce and the infrastructure that supports it has a long runway for growth, and the adoption of 5G will continue to drive this growth.

{kind=link}

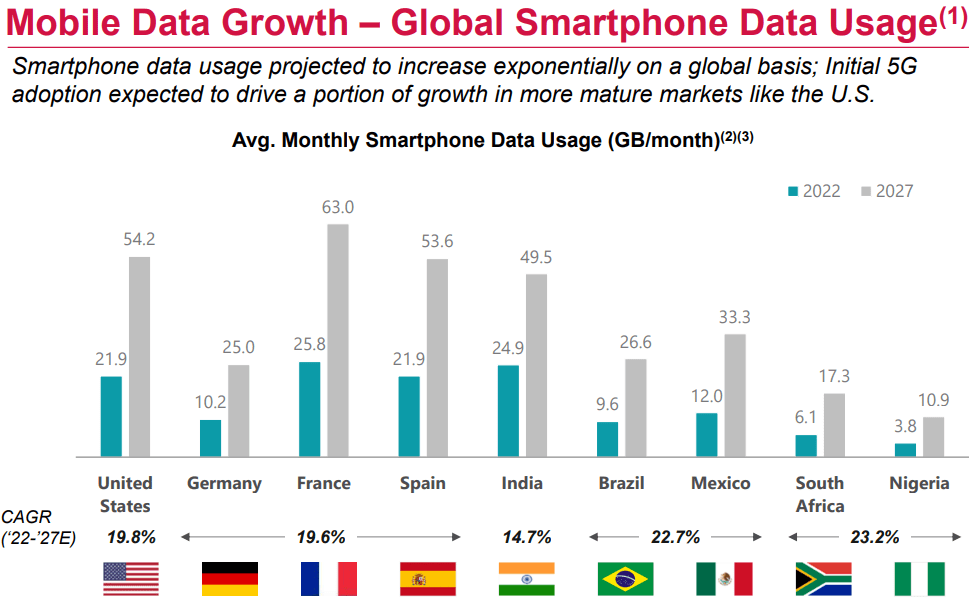

More and more people are using Mobile Data every day, and that trend is only expected to increase for the foreseeable future. Smartphone data usage is expected to increase globally, especially in mature markets with the adoption of 5G. Data usage is projected to more than double by 2027 in the U.S., Germany, France, Spain, and India, to name just a few markets.

{kind=link}

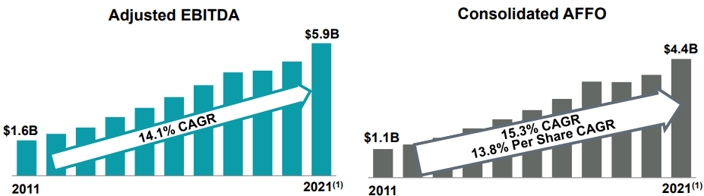

While the future looks bright for data usage and cell towers in general, American Tower has been a growth machine for over a decade. AMT has an Adjusted EBITDA compound annual growth rate of 14.1% and a Consolidated AFFO compound annual growth rate of 15.3% since 2011.

{kind=link}

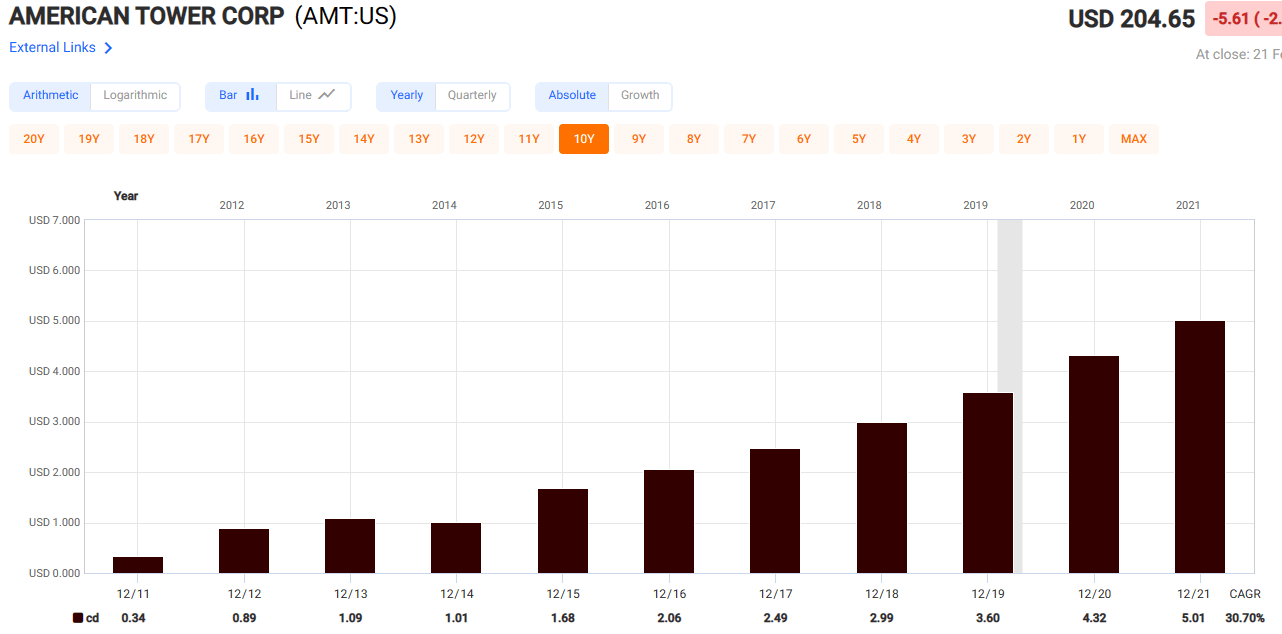

To top it off, AMT has increased its dividend at a compound annual growth rate of 30.70% since 2011. Currently, they pay a 2.86% dividend yield that is relatively safe, with an AFFO payout ratio of just 58.89% in 2022.

AMT’s earnings growth supports the dividend, which is how they have been able to increase the dividend at such a high rate while keeping a very reasonable AFFO payout ratio.

{kind=link}

American Tower is investment-grade rated at BBB- and has improved its balance sheet and debt metrics since 2021. Comparing their credit and debt metrics from 2021 to the third quarter of 2022 shows improvements in several key areas.

Their Net Leverage has been reduced from 6.8x to 5.5x, their liquidity has increased from $6.1 billion to $7.0 billion, and their floating rate debt has been reduced from 31% to 23%.

AMT Investor Presentation

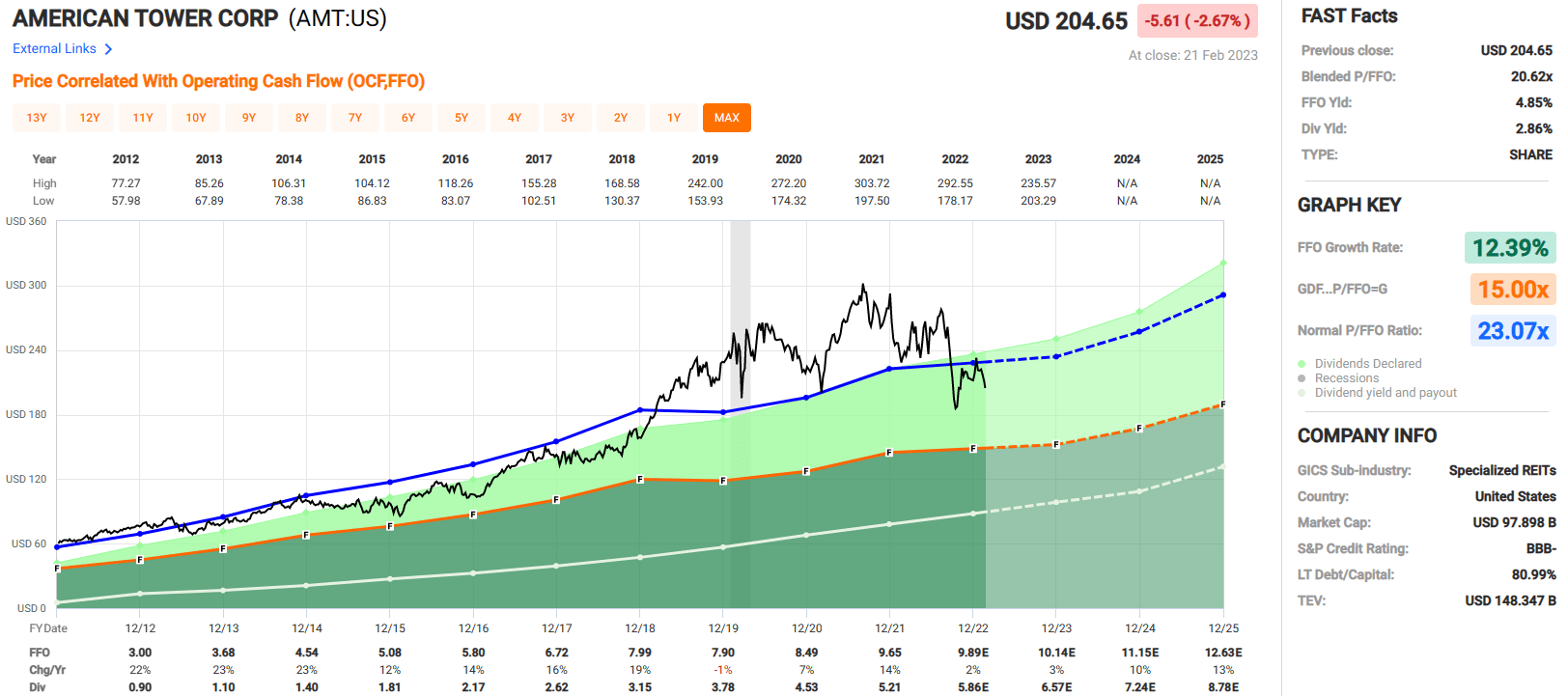

American Tower currently trades at a P/FFO multiple of 20.62x which is a discount to normal FFO multiple of 23.07x and pay an above average yield that is very well covered by their AFFO.

Given the past earnings and dividend growth, along with the future potential for continued growth as data usage increases, we see a bright future ahead for AMT. At iREIT, we rate American Towers a STRONG BUY.

{kind=link}

Realty Income Corporation ( O )

Realty Income is the King of triple net-lease REITs, with 12,237 commercial properties serving 1,240 tenants in 84 industries. They have properties in all 50 states and a growing international presence with properties in the UK, Spain, and Italy. In all they have 236.8 million square feet of leasable space that generated approximately $3.4 billion in base rent in 2022.

Roughly 81.9% of their annual rent came from retail properties, 13.3% from industrial properties, and 2.9% from their gaming property. Their occupancy rate as of December 31, 2022, was 99.0%, with a weighted average remaining lease term of almost 9.5 years.

{kind=link}

On February 21, 2023, Realty Income released their earning results for the fourth quarter and full year 2022. I’ve highlighted some key points below:

Earnings update for full year 2022

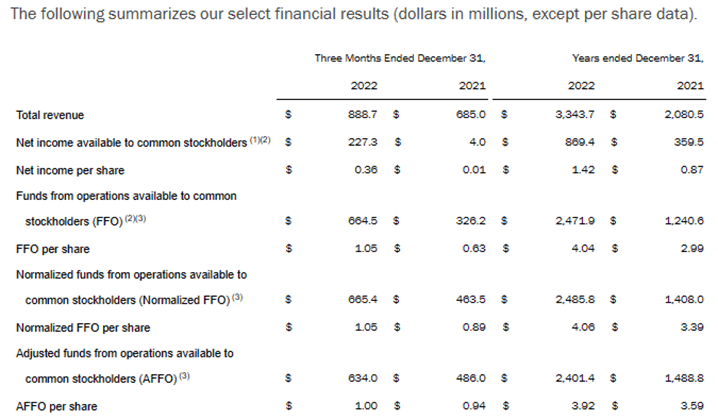

- Net Income came in at $869.4 million or $1.42 per share. The consensus estimate by analysts was for EPS to come in at $1.36.

- Normalized Funds from Operations (“FFO”) came in at $4.06 per share which was a 19.8% increase over the prior year.

- AFFO (Adjusted FFO) increased 9.2% over the prior year at $3.92 per share.

- During 2022 Realty Income invested $9.0 billion in 1,301 properties, including $2.5 billion in Europe.

- Achieved their highest property-level occupancy in over 20 years with a property-level occupancy of 99.0%.

- Raised $4.6 billion through the issuance of common stock with a weighted average price of $67.04.

- Dividends paid in 2022 increased 4.7% compared to the prior year.

- As of December 31, 2022, Realty Income had $1.7 billion of liquidity, consisting of cash and cash equivalents of approximately $171.1 million and $1.5 billion available to them under their revolving credit facility.

Sumit Roy, the CEO of Realty Income, made the following statement (emphasis added):

"I am proud of our team's outstanding accomplishments in 2022, culminating in AFFO per share growth of 9.2% and a record year for property-level acquisitions of approximately $9 billion,"

Our investment philosophy is centered around acquiring prime real estate assets in partnership with operators who are leaders in their respective industries. Illustrating this philosophy was the acquisition of our first gaming asset, the Wynn Encore Boston Harbor, which contributed to a record quarter for property-level acquisitions during the fourth quarter of approximately $3.9 billion.

In addition, since the start of the fourth quarter, we have acquired properties in several distinct verticals for future potential growth, including investments in properties related to the consumer-centric medical industry , a debut transaction in Italy , and the formation of a real estate development partnership with a leading vertical farming operator ."

"Our diversified portfolio continues to demonstrate strength with occupancy ending the year at 99% and a rent recapture rate of 105.9% for the year.

Our investment pipeline remains healthy as investment yields trend higher, our investment capacity is well-funded with approximately $850 million of outstanding forward equity raised, and our confidence in the long-term outlook of our platform remains steadfast.

To that end, we announced an increase to the March 2023 d ividend of 2.4%, representing 3.2% growth over the year-ago period ."

{kind=link}

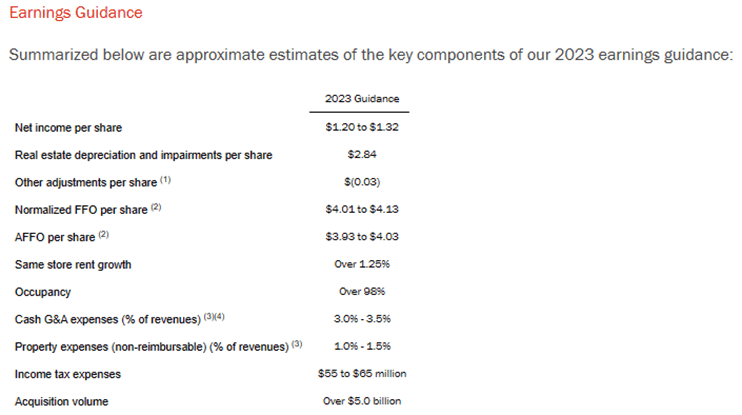

In their 2023 earnings guidance , they expect net income to come in between $1.20 to $1.32 per share, normalized FFO to come in between $4.01 to $4.13, and AFFO per share to come in between $3.93 to $4.03. They also guided for $5.0 billion in acquisition volume in 2023.

{kind=link}

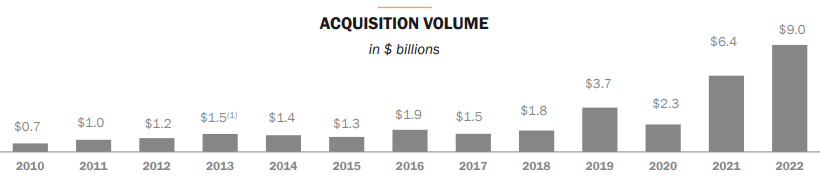

Realty Income has steadily increased its investments in real estate over the years. Gross real estate investments totaled approximately $5.9 billion in 2012 compared with $42.6 billion in 2022.

A large increase in their real estate investments occurred in 2021, when they merged with fellow REIT VEREIT, and in 2022 they made a notable acquisition when they transacted a sale-leaseback for the Encore Boston Harbor with Wynn Resorts (WYNN).

Additionally, in late 2022, Realty Income acquired 454 single-tenant retail properties from CIM Real Estate Finance Trust for approximately $1.25 billion. In total they had a record year for acquisition volume in 2022 at $9.0 billion. Acquisition guidance for 2023 is around $5.0 billion.

{kind=link}

{kind=link}

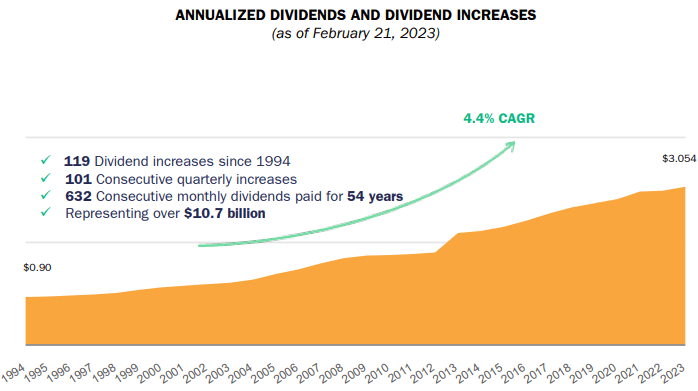

Known for its monthly dividend, Realty Income is a Dividend Aristocrat with 28 years of consecutive increases since going public. Since 1994, they have increased their dividend 119 times and have 101 consecutive quarterly increases for a compound annual growth rate of 4.4%. Over the last 54 years, since their inception in 1969, Realty Income has paid 632 consecutive monthly dividends.

{kind=link}

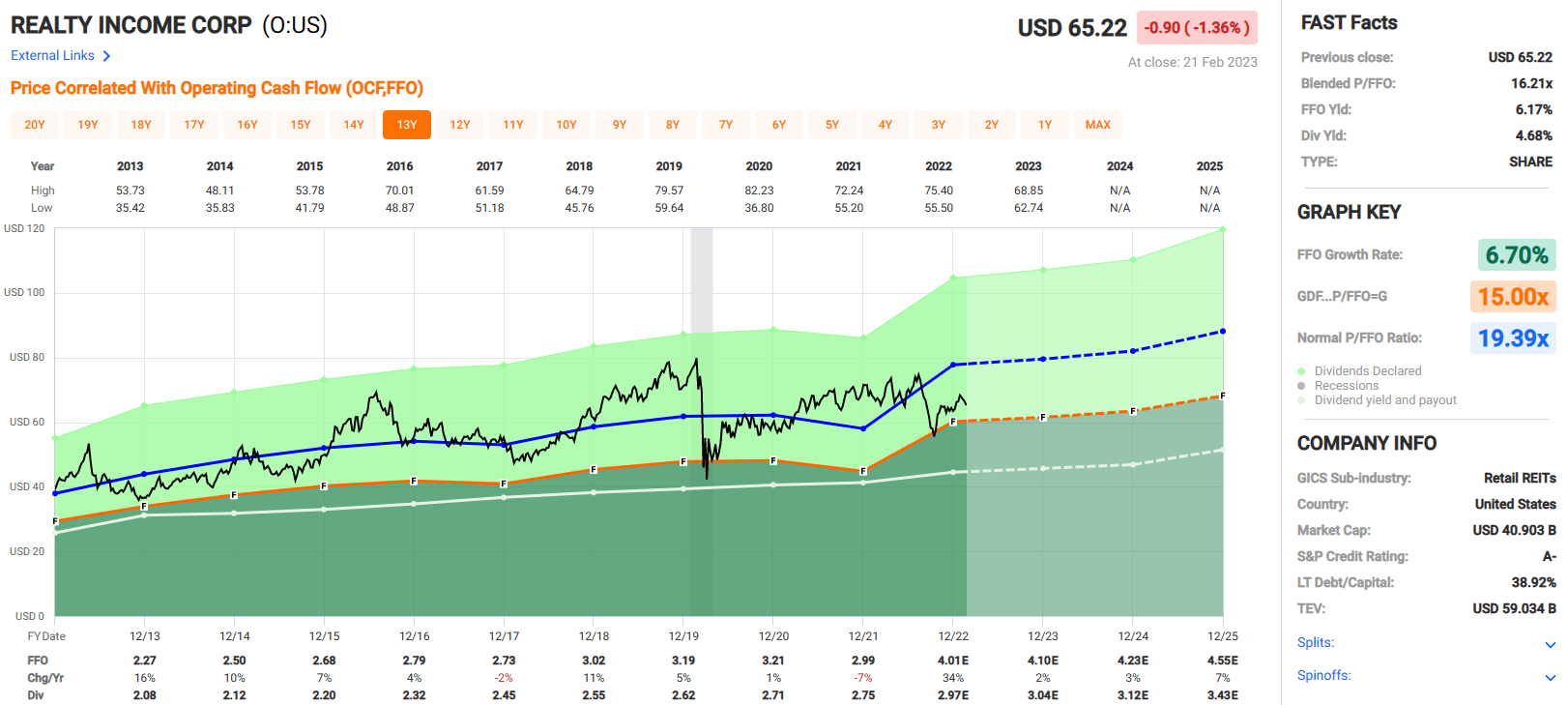

Realty Income currently pays a 4.68% dividend yield that is well-covered, with an AFFO payout ratio of 76.17%. They have an A3 / A- investment-grade credit rating from Moody’s and S&P and a strong balance sheet with a 5.3x Net Debt to Pro Forma EBITDAre and a 5.2x Fixed Charge Coverage ratio. 95% of their debt is unsecured and 85% is fixed rate. In total, they have a weighted average term to maturity of 6.2 years.

Realty Income has a scale and cost of capital advantage which is critical for real estate companies. They have operated through multiple recessions and inflationary environments and have continued to grow their investments in real estate and their funds from operations. They pay a high yield that is well-covered and are currently trading at a discount to their normal P/FFO multiple. At iREIT, we rate Realty Income a BUY.

{kind=link}

The Moral to the Story

Rip Van Winkle was perhaps one of the first SWAN investors. He managed to sleep right through the American Revolution, which is quite a feat when you think about how noisy that must have been.

That's how SWAN investing works, you can practically ignore Mr. Market, as long as you have a strong conviction about what the company is really worth. As Benjamin Graham explains,

“In the short run, the market is a voting machine but in the long run it is a weighing machine.”

And Warren Buffett said it best (emphasis added):

The speed at which a business’s success is recognized is not that important as long as the company’s intrinsic value is increasing at a satisfactory rate. In fact, delayed recognition can be an advantage : It may give us the chance to buy more of a good thing at a bargain price."

For further details see:

REITs For Rip Van Winkle