PLYM - REITs Fundamentally Like Higher For Longer

2023-10-03 16:27:15 ET

Summary

- The Fed's hawkish rhetoric suggests fewer rate cuts in 2024 and a possible rate hike in 2023, leading to a sell-off in REITs.

- However, historical data shows that REITs have performed well in rising interest rate environments.

- The COVID era cuts and the resulting free money environment have negatively impacted REITs, but rising rates are the cure for the unhealthy conditions.

The Fed strikes again with more hawkish rhetoric indicating fewer rate cuts anticipated for 2024 and perhaps one more 25 basis point hike here in 2023. The exact changes to interest rates are subject to change via our data-dependent Fed. One thing is clear though - we are now in an environment the media refers to as "higher for longer".

So what does this mean for REITs?

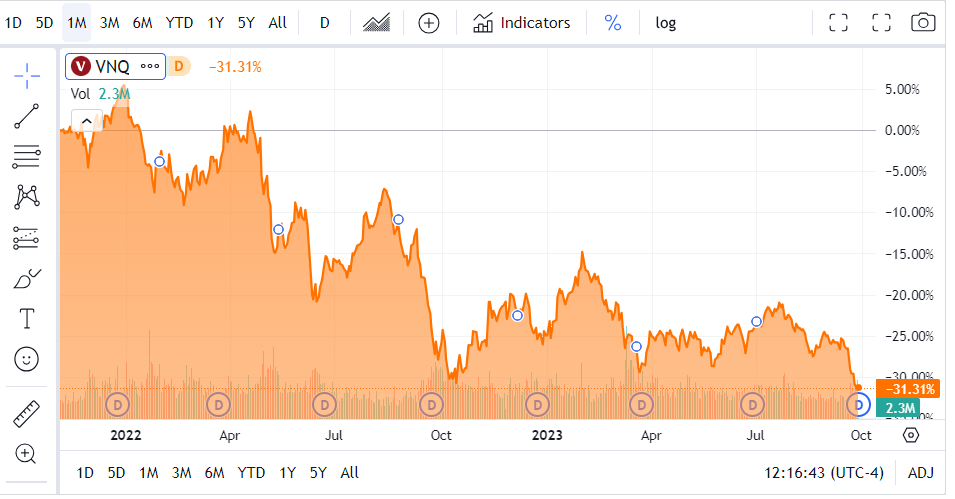

The market's knee-jerk reaction is to sell REITs to oblivion with the Vanguard Real Estate ETF ( VNQ ) down over 30% from its 2022 highs.

{kind=link}

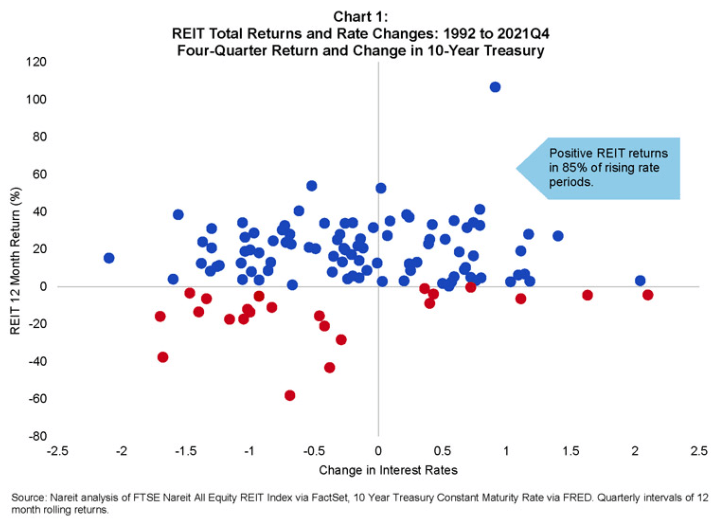

Yet a longer look at history tells a different story. REITs have traditionally performed well in rising interest rate environments. Since 1992, REITs have been up in 85% of years in which the 10-year treasury yield rose.

{kind=link}

So why is the response so different this time around?

The difference is the starting point.

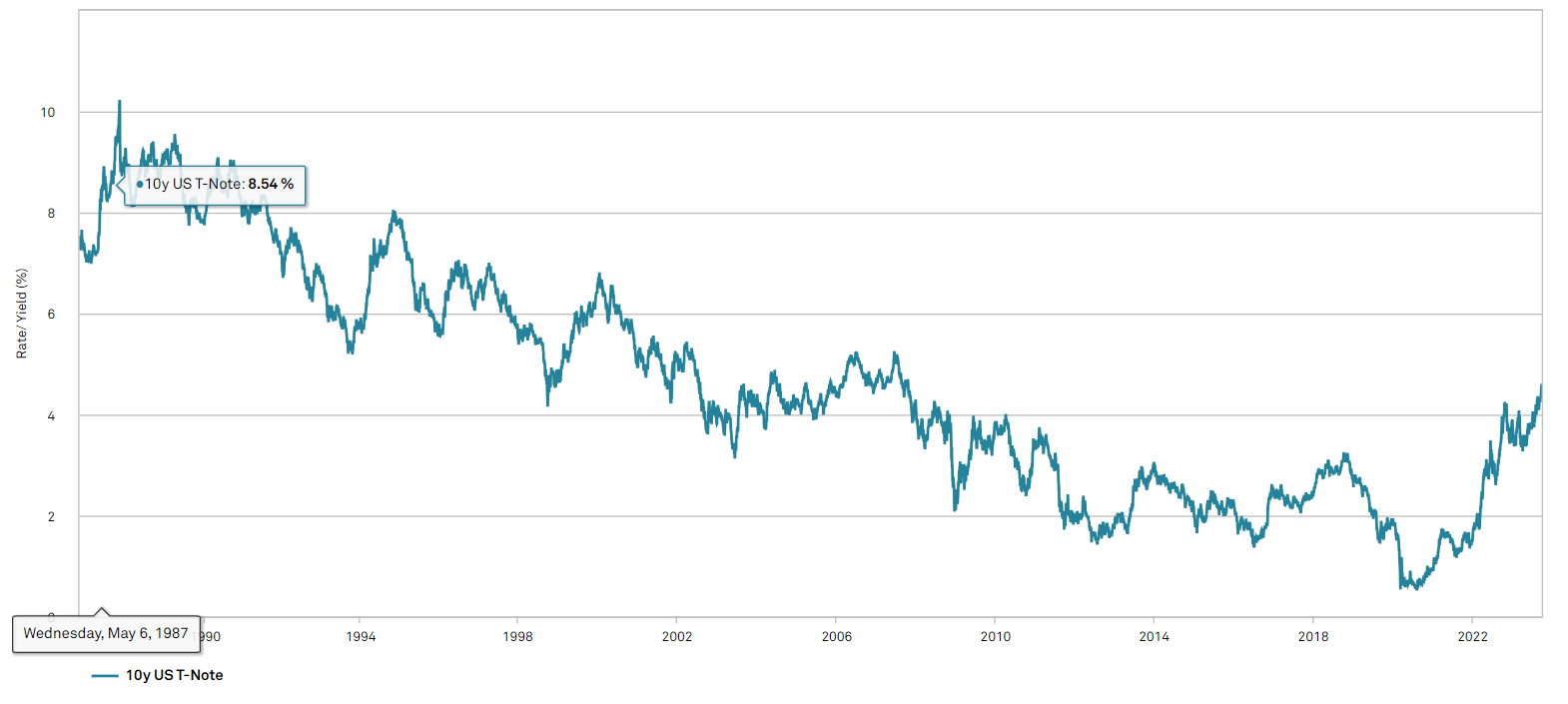

There have been many interest rate increase cycles over the past 35 years.

{kind=link}

- In the late 80s, the 10-year Treasury yield went from the 7s to briefly over 10%.

- In the early 90s it went from the 5s to 8%.

- Late 90s from the 4s to almost 7%.

In the early 2000s interest rates rose for almost five years straight. This was a golden period for REITs characterized by massive outperformance over the broader market.

Generally, REITs did fine in all these periods.

The main economic event that makes this period different is the COVID era cuts which took the 10-year treasury yield to below 1%. That is an extraordinarily unhealthy level of interest rates. I posit that the rise in rates is not what is hurting REITs, but rather the problems that arose from free money.

To understand why the COVID period was so rough for REITs we can look at a broader picture of the equilibrium that governs real estate.

The equilibrant state of real estate is one in which the expected internal rate of return on real estate is at a normal premium over the risk-free rate. I would consider a normal premium to be anything from 3%-7%.

So in a normal environment where the 10-year Treasury yield is around say 4%, real estate would equilibrate to a compounded rate of return of about 8%-9%. This return comes from a combination of going in cap rate and net operating income growth rate.

In an equilibrated 4% 10-year treasury yield environment that would be going in cap rates of 6%-7% with expected annual NOI growth of 1%-3%.

There are mechanisms in place that push toward and maintain this equilibrium. If, for example, real estate is positioned to deliver an outsized return over treasury yields of let's say 12% when treasuries are yielding 4%, real estate will be too desirable of an asset to invest in. Developers will build which increases supply and thereby lowers expected returns. They will build until such a point that the expected return on real estate is back to a normal spread over the risk-free rate.

This is what happened when interest rates went to zero. Allow me to digress into why a zero interest rate environment is so unhealthy for real estate.

The perverse implications of free money

If we look back to the previous healthy environment of 2019, 10-year yields were around 3% which is somewhat low but still in a healthy range. At that level, real estate would typically return about 8% or so annually and to make development worth the risk and time lag, development yields would need to be maybe 9.5% to 10%.

So the equilibrium bounces around in that range. Real estate gets a bit too high return and developers build a bit then it gets a little bit low return and development stops which pulls the returns back up. Each property sector has its own individual development cycles, but they largely stay in balance.

Then, suddenly, interest rates on the short end of the curve go to 0 and on the long end go to below 1%.

All those potential developments that weren't quite viable when there was a 9% hurdle rate suddenly pencil out. It is very easy for underwriting of a development to look good when the cost of borrowing is essentially zero.

A surge of development hit basically every sector, even those which were already oversupplied. The office vacancy rate was already around 10% nationally which I would consider oversupplied, yet new construction activity poured in.

People were developing at cap rates as low as 6% and cap rates on fully leased real estate dropped in some cases to below 4% and frequently into the 4s.

While those yields still presented a significant margin over the "risk-free" treasury yield so there was technically a proper risk premium, it creates a situation of razor-thin margins.

With cap rates that low, the volatility of operating expenses has an amplified impact on the bottom line. It so happens that hurricanes and other disaster activity picked up and insurance companies had to adjust their rates. Insurance costs depending on the sector rose between 20% and 75%.

Ordinarily, insurance cost is a small line item, but when cap rates are as low as they were in the free money era, this extra OpEx had a huge impact on the bottom line. Property maintenance costs have also risen and again the change was amplified as a percentage of NOI because cap rates were so low.

In the zero interest rate environment, any volatility in line items becomes a big deal. The dollar value of interest rate expense going from 5% to 8% interest rates is the same as going from 1% to 4%, but because cap rates were so low it has been harder for REITs to absorb the rising interest expense in this particular cycle.

The market has it wrong

REITs are not hurting right now because interest rates are rising. They are hurting because rates were at 0% and that was a profoundly unhealthy environment.

The 10-year treasury yield today is at 4.6%. That is a healthy level. REITs perform well at that level.

So while the market of REIT investors' fears higher for longer, I say bring it on. If the 10-year treasury yield could sit between 3.5% and 7% forever that would be phenomenal for real estate.

Rising rates are the cure to the Keynesian hangover from the free money party.

The medicine is starting to work

The same equilibrium maintaining forces that keep real estate in check when it gets a bit too hot also bail it out when it gets too cold.

With the 10-year treasury at 4.6%, stabilized real estate needs to generate IRRs around 9%-10%. Developments often use short-term bridge lending which is really expensive right now due to the inversion of the yield curve. It has become the opposite of the free money environment. Suddenly all that development underwriting that used to pencil out no longer does. The hurdle rate on developments is close to 11% now, give or take a few percentage points depending on the sector.

Having to swallow 8%+ bridge loans and having to wait a year or more for the property to cash flow just doesn't work. New supply is dropping off a cliff, even in the hot sectors.

A September Yardi Matrix report discusses industrial construction falling to about 1/3 of its previous levels.

"A delivery slowdown is on the horizon, with starts falling sharply this year. Just 204.3 million square feet of industrial space have been started so far in 2023, down from 614.1 million last year and 586 million in 2021"

Apartments were the other hot sector in regard to construction activity and it too is slowing down considerably. Deliveries are slated to be just a fraction of the planned supply as permitted construction no longer hits the hurdle rate. Developments are being intentionally delayed or cancelled altogether.

Retail has virtually no new supply coming in despite rumblings among shopping center owners that it could be the next industrial in terms of growth rates.

The demand side of the equation also works to restore equilibrium. People and businesses need places to live, work, and manufacture. They can obtain the real estate by building or by renting and with building prohibitively expensive, more are renting.

For example, single-family rental demand is surging because mortgage rates priced people out of ownership.

A high cost of money is good for real estate

Most good businesses have moats of some sort. Biotech might have a patent on a drug preventing others from moving in on their territory.

Real estate's moat is the capital barrier to entry. In the free money environment this moat was destroyed. Incumbent real estate had no protection against rampant development.

With interest rates now at a higher, healthier level, the moat is restored. Let me give a quick example of this.

Plymouth Industrial ( PLYM ) is essentially untouchable by new supply. It has an enterprise value per square foot of $50. It is impossible to replicate their portfolio for anywhere near that price.

With cost of money where it is today, developments cost north of $100 per foot so there is no way for a new build to charge anywhere near the level of rent that PLYM charges. The new supply would have to charge rent of at least $9 a foot, while PLYM is highly profitable with rent of $5 a foot.

Restoration of equilibrium

Equilibrium is on the cusp of being restored. With the 10-year yield at 4.6%, real estate needs to return 8%-9%. The mechanism by which that will happen is rising rental rates. Supply levels have retreated to healthy amounts and occupancies reaching a full level is causing market rents to rise materially. With forward NOI growth looking better, we are within spitting distance of 8%-9% annual returns on real estate.

REIT Outlook

REIT returns are an entirely different calculation than real estate returns. REIT returns are dampened by overvaluation or amplified by undervaluation.

Right now, REITs are firmly on the amplified side with the average REIT trading at 72% of net asset value ((NAV)). Frankly, buying a REIT nets an investor much more exposure to real estate than simply buying real estate. REIT forward returns already look to be well above the 8%-9% level. Here's how we calculate that:

FFO yield is simply the inverse of FFO multiple. Right now the average REIT is trading at 12X forward FFO so that is an FFO yield just north of 8%. So with zero growth, REITs would already be in the 8%-9% range. REITs are, however, growing cashflows at a pace of about 4% for this year and given the supply/demand dynamics I anticipate that accelerating into 2025. The combination of current yield and growth suggests annual returns in the double digits.

This too is subject to equilibrium. A double-digit expected forward return is too high relative to the rest of the market (which trades at a much higher multiple with similar growth). Over time, if this becomes the consensus outlook, prices of the REITs will be bid up until such a point that its forward returns are in line with the rest of equities of similar risk level.

As such I view REITs as opportunistic right now. Rising rates may not have been kind to market prices, but high stable rates are fundamentally beneficial to growth. It is hard to predict how long it will take before the market prices recover, but with high dividend yields and lower construction activity, time is on our side.

For further details see:

REITs Fundamentally Like Higher For Longer