RLAY - Relay Therapeutics: It Could Be Time To 'Be Greedy When Others Are Fearful'

Summary

- Relay's share price was hammered throughout 2022, losing >70% of its value.

- That may have been down to short-termism since Relay has built a credible pipeline in a short space of time.

- The company uses a cutting-edge AI-driven drug discovery engine to model disease-causing proteins and learn how to target them optimally.

- The company may have the data it needs to secure an accelerated approval for a bile duct cancer drug in early 2024 - and that drug has significant label expansion opportunities.

- There's also a promising breast cancer franchise being built from the ground up. Institutions may have turned their backs on Relay but there is an argument it's time to "be greedy when others are fearful."

Investment Overview - Cash Intensive But Cash Rich - At Current Price Relay Offers The Patient Investor Value

I have covered Relay Therapeutics (RLAY) several times for Seeking Alpha since the company completed what was, at the time, the third largest biotech IPO in history, raising ~$400m at a price of $20 per share in July 2020.

Relay already had raised $520m from a private funding round that included participants such as the SoftBank Vision Fund, Google Ventures, the Biotechnology Value Fund, and Third Rock Ventures, giving it a war chest of >$1bn.

In its Q322 10Q submission Relay describes itself as follows:

We are a clinical-stage precision medicine company transforming the drug discovery process by combining leading-edge computational and experimental technologies with the goal of bringing life-changing therapies to patients.

As we believe we are among the first of a new breed of biotech created at the intersection of disparate technologies, we aim to push the boundaries of what's possible in drug discovery.

One issue with this new breed of drug discovery companies is that their cutting edge technology platforms tend to be capital intensive. As of Q322, Relay's total operating expenses for the year were $228m, compared to $299m in the prior year period, and net loss was $223m, versus $296m in the prior year period.

In fairness, Relay has been able to complete additional at the market fundraisings of ~$350m in October 2021 , and $300m in September 2022 , meaning as of Q322, Relay reported a cash position of $1.1bn. That will be sufficient to fund operations until 2025, management says.

The fundraisings - and the biotech bear market of 2022, which saw investors pull money out of the biotech sector, searching for safer havens that offered nearer term commercial revenue opportunities, have dragged Relay's share price down from a post-IPO price of >$50, to a value as low as $14 as of December last year.

At today's share price of $17.5, Relay still boasts a market cap valuation >$2bn, which is high for a drug developer that has not progressed any asset beyond Phase 1 clinical studies, but also potentially attractive - given the rewards on offer - for investors prepared to be patient.

Pipeline Focus - FGFR2 Inhibitor Offers Approval Shot, Label Expansions, Validation of Approach

{kind=link}

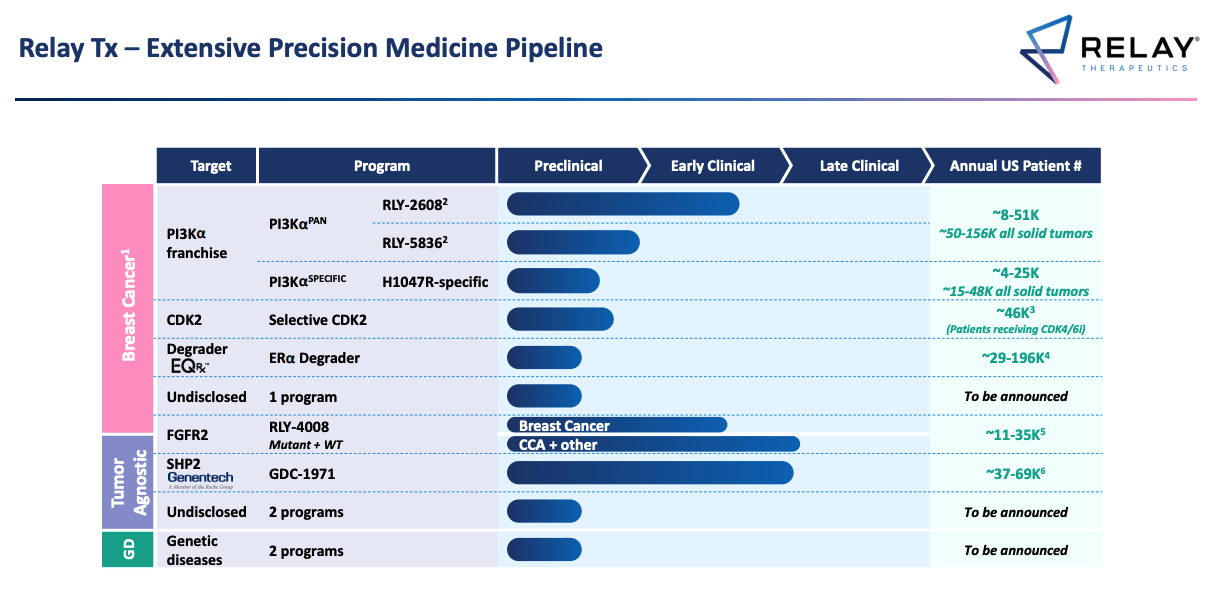

As we can see above Relay's high cash spend has allowed the company to develop a promising pipeline of assets using its Dynamo platform, which the company says:

Integrates an array of leading-edge computational and experimental approaches designed to drug protein targets that have previously been intractable.

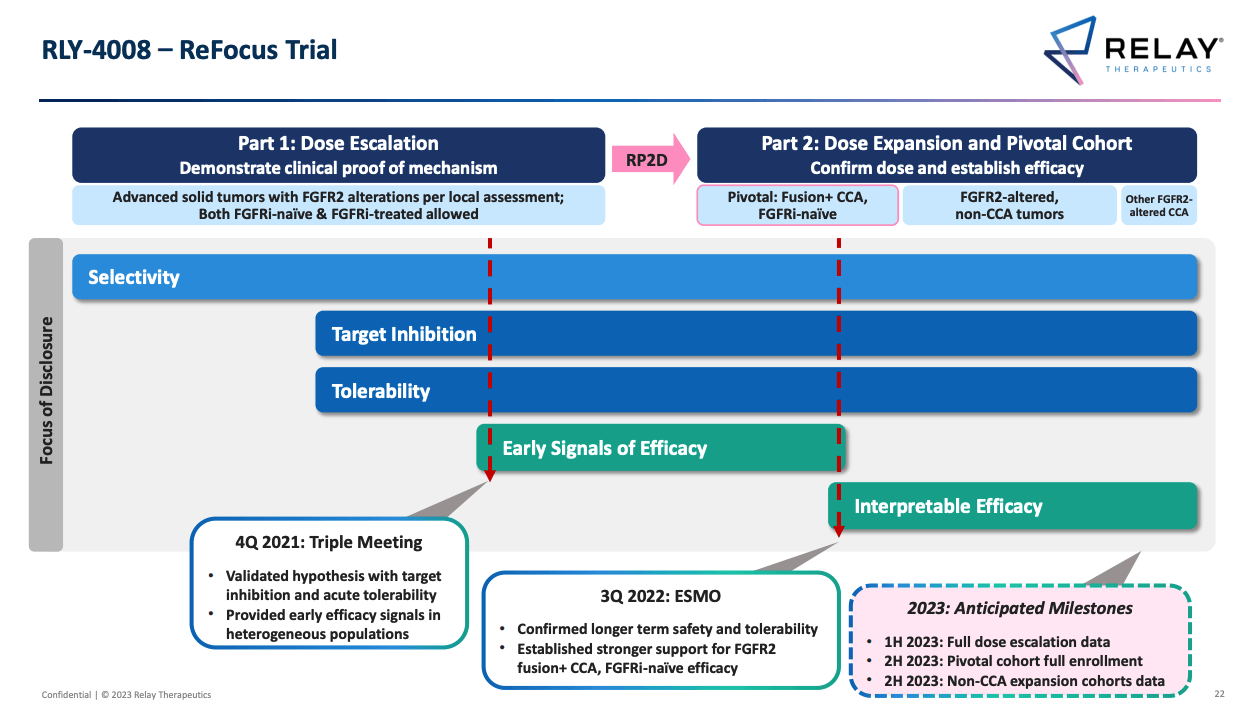

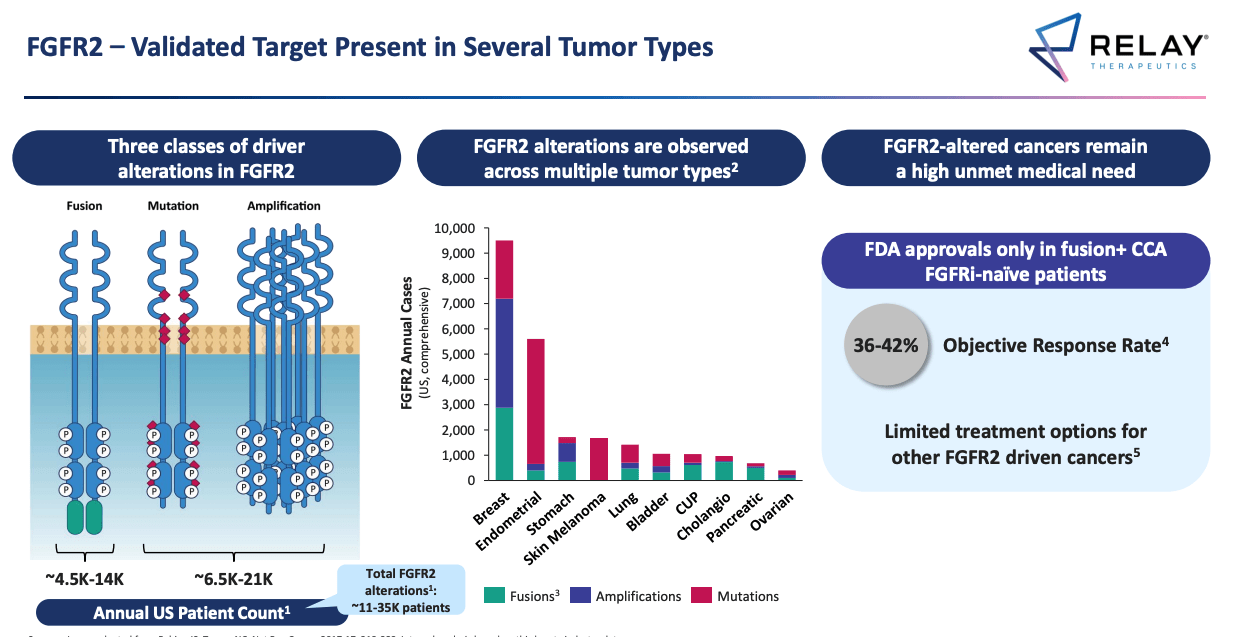

Near term, Relay's commercial opportunities are small scale. Its most advanced asset to date is RLY-4008, an oral small molecule inhibitor of fibroblast growth factor receptor 2 ("FGFR2"), which is expected to enter a pivotal study this year in patients with Cholangiocarcinoma ("CCA"), otherwise known as bile duct cancer - expressing FGFR2 mutations.

CCA has a patient population of ~1,000 in the US, Relay estimates, and therefore represents a revenue opportunity that's likely <$100m per annum. More encouraging, however, is the potential for expanding the drug into new indications.

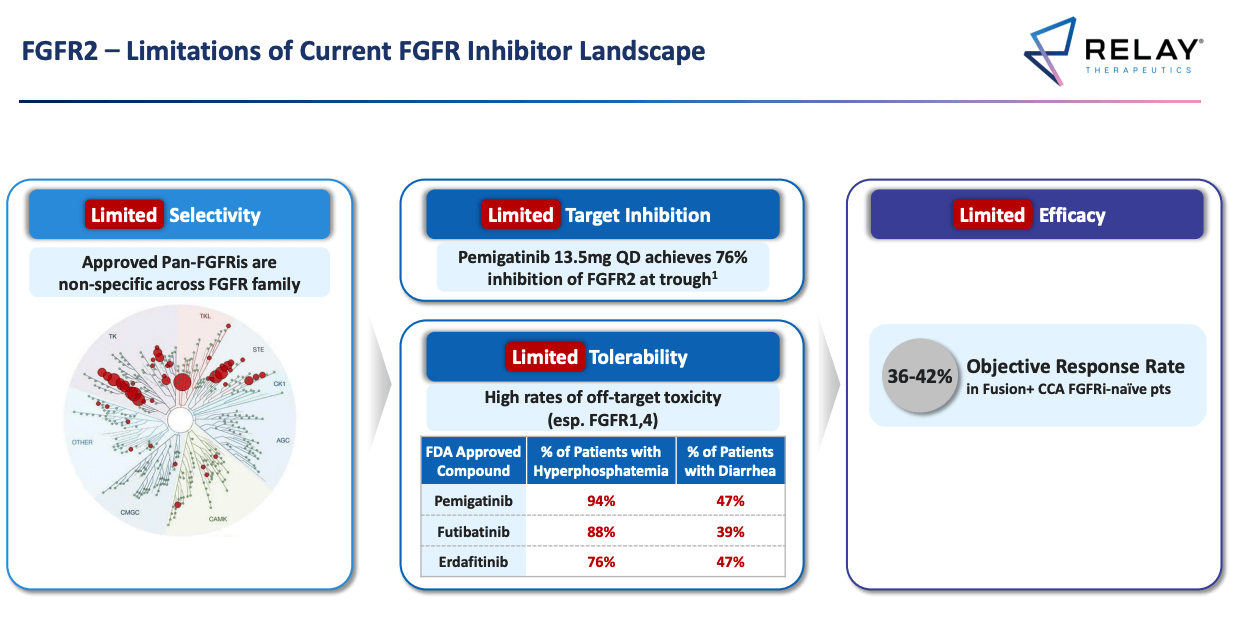

The FDA has approved three FGFRs in recent years:

- Incyte's ( INCY ) Pemazyre (pemigatinib) was approved in April 2020 in unresectable locally advanced or metastatic CCA exhibiting FGFR2 fusion, earning $83.5, of revenues in FY22.

- Privately-owned Taiho Oncology's Lytgobi (futibatinib) was approved in October last year for treatment of intrahepatic cholangiocarcinoma harboring FGFR2 gene fusions.

- Janssen Pharmaceuticals' Balversa (erdafitinib) was approved in April 2019 for treatment of patients with locally advanced or metastatic urothelial (bladder) cancer. Sales have not been disclosed by Johnson & Johnson ( JNJ ), Janssen's parent company, although JNJ apparently believes the drug can reach blockbuster (>$1bn per annum) sales based on label expansion opportunities.

Relay believes something similar to Janssen in the case of RLY-4008. Using its higher resolution technology, Relay was able to identify that targeting FGFR2 as opposed to FGFR1 - as Pemazyre, Lytgobi, and Balversa do - gives its candidate superior selectivity, target inhibition and tolerability - and Relay has produced the data to prove this thesis.

{kind=link}

As we can see above the three approved FGFR targeting drugs have been able to generate an average 36%-42% Objective Response Rate ("ORR") in clinical studies in CCA. Interim data from Relay's Phase 1 ReFocus study however has shown an ORR of 88% (15 of 17 patients) at the dose level - 70mg QD - it will use in its pivotal study of the drug in CCA. Across all doses, the ORR achieved was 63% (24 of 38 patients).

Admittedly, RLY-4008 has not been able to generate any complete responses ("CRs") so far - only partial responses ("PRs"), but at the time of the data cutoff, 13 of 15 high dose responders remained in treatment and as importantly, Relay reported from a safety perspective that:

Most AEs have been expected FGFR2-on target, low-grade, monitorable, manageable and largely reversible

ReFocus Trial dose expansion & pivotal cohort overview (investor presentation)

{kind=link}

As above, Relay is now in the process of initiating a pivotal fusion positive CCA expansion cohort that could potentially pave the way for an accelerated approval of RLY-4008 in CCA, perhaps as early as 2024 given the cohort is expected to be fully enrolled by the end of the year.

And just as importantly - for investors looking for more than a <$100m revenue opportunity - Relay also will initiate a non-CCA cohort looking at the ability of RLY-4008 to target other types of solid tumor.

FGFR2 alterations observed in multiple tumor types (investor presentation)

{kind=link}

The fact that RLY-4008 can target FGFR mutations and amplifications as well as fusion potentially increases the candidates' addressable market compared to its rivals, and as we can see in the middle of the above slide from Relay's latest investor presentation , FGFR alterations are observed across multiple tumor types, including pancreatic, skin / melanoma, lung and breast cancer - markets that add up to an addressable market that easily exceeds $50bn.

To summarize, having spent likely >$600m in 2021 and 2022, investors have a right to demand tangible signs of progress, and Relay has broadly delivered that progress.

That's not to suggest that RLY-4008 is a slam dunk that's guaranteed to validate Relay's approach with a CCA approval, and then make the company profitable by commanding blockbuster sales, but neither is it too much of a stretch to believe that may be the case.

Establishing A Breast Cancer Franchise

Obviously Relay's opportunities stretch beyond its FGFR inhibitor candidate, even if that's the most prominent near-term commercial opportunity.

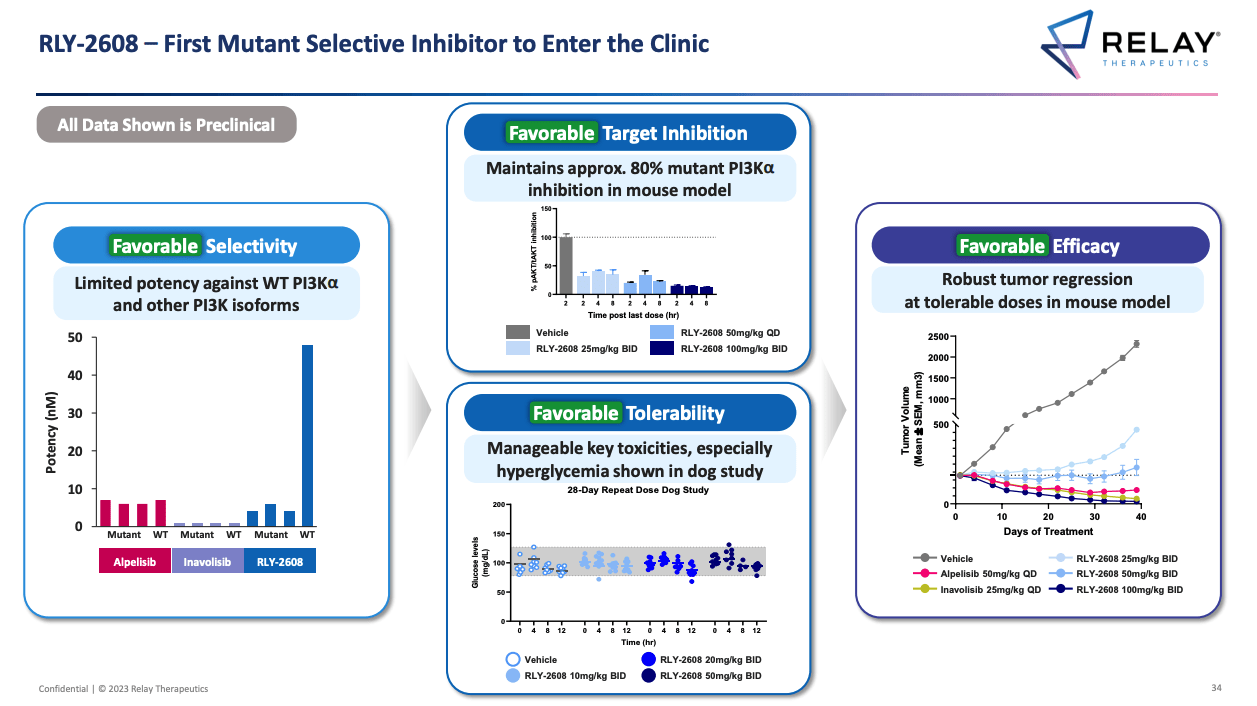

In breast cancer, Relay has ambitious plans to establish a drug franchise and its approach / thesis is similar to the FGFR opportunity. With its advanced modeling tools, Relay has been able to create what it believes are the first full length structures of a pan-mutant and isoform-selective phosphoinostide 3 kinase alpha, or PI3Ka for short.

In doing so, Relay has been able to identify a "novel allosteric pocket" to target - as opposed to the "orthosteric," more easily accessible but potentially less promising sites that traditional drug discovery approaches have focused upon. Relay's candidate is named RLY-2608.

Once again - although this time based on preclinical studies only - Relay believes that its PI3KA has superior properties to e.g. Danish pharma giant Novartis' Piqray (alpelisib), which earned ~$370m of revenues in FY21, or Roche's (RHHBY) Phase 3 stage candidate Inavolisib, also indicated for breast cancer.

RLY-2608 will shortly become the first mutant (as opposed to wild type) selective inhibitor to enter the clinic, backed by encouraging preclinical data as shown below.

favourable preclinical profile of RLY-2608 (investor presentation)

{kind=link}

One arm of the study will focus on RLY-2608 plus fulvestrant - a type of hormone therapy - in patients with PIK3CA mutated breast cancer, while the other will look at other solid tumors that express PIK3CA such as ovarian, cervical and head and neck cancers. Both arms of the study will then enter a dose expansion phase with 15 patients in each indication.

The initial clinical data update has been promised for the first half of this year, which is potentially strong upside catalyst for investors to look forward to (although disappointing results will conversely drag the share price down).

The plan is to then introduce two other members of its PI3KA franchise into the mix: RLY5836 - which has a "similar clinical profile, but different chemical properties" to RLY-2608, according to Relay, followed by an "H1047R-specific" candidate - H1047R being a "hotspot" mutation that's found within the kinase domain of PI3KA.

And that's not all - next will come a selective Cyclin-dependent kinase 2 ("CDK2") asset - CDK2 being a gene encoding a protein associated with cancer cell proliferation - followed by an Estrogen Receptor ("ER?") degrader - protein degradation being an exciting but unproven method of dipsosing of unwanted proteins inside a cell.

At this early stage in the development cycle it's probably natural for any prospective investor in Relay to harbor doubts as to whether all of these new asset types will add up to more than the sum of their parts, and genuinely be able to deliver a commercial stage breast cancer franchise.

The breast cancer market is expected to reach ~$70bn in size by 2030, and is typically the domain of big pharmas such as Gilead Sciences ( GILD ), Roche, Johnson & Johnson, Pfizer ( PFE ) etc., which will not want to loosen their grip on the space.

With that said, Relay's approach has a certain amount of preclinical validation to it, and the company is delivering on its promise - namely to create more sophisticated modeling of oncogenic drivers and mutations and identify ways of targeting them more effectively.

I would not be overly surprised if Relay's Dynamo engine gives the company a slight edge over even a large Pharma concern. If you also find yourself persuaded by Relay's progress to date, then investing today, when the company is worth a fraction of what it was post-IPO, looks like a sensible move.

Relay is trading at just 2x cash, after all, and we could see it commercialise a first asset within two years, which in my view, marks it out as one of the most promising and prominent precision oncology companies, with a reasonable chance of building - from the ground up - a genuinely innovative one-stop-shop for breast cancer treatment.

If such a situation were to arise, investors can rest assured that Relay's share price is guaranteed to rise by at least 2/3 times.

Genentech Collaboration An Additional Fillip

One concern or question investors may run along the lines of "if Relay's platform is so impressive, why is Big Pharma not queueing up to partner with its technology?"

In Relay's case, however, it does have an ongoing partnership with Genentech, which is Roche's drug development subsidiary, over an inhibitor of Src homology region 2 domain-containing phosphatase-2, or SHP2 name RLY-1971. This candidate entered a Phase 1 study in 2020, and according to Relay's Q322 10Q submission:

Genentech initiated the cohort of RLY-1971 in combination with GDC-6036, its KRAS G12C inhibitor, in a Phase 1b trial in July 2021, and a Phase 1b trial of RLY-1971 in combination with atezolizumab in August 2022.

KRAS is an exciting druggable target that is targeted by two recently-approved, drugs, Amgen's ( AMGN ) Lumakras and Mirati Therapeutics ( MRTX ) Krazati. Both are expected to deliver blockbuster sales, although a next generation candidate could improve on both drugs safety and efficacy profiles, and perhaps expand beyond later line lung cancer. Atezolizumab is Roche's answer to Merck's >$20bn selling cancer wonder drug Keytruda - an immune checkpoint inhibitor that often works better when paired with an adjuvant therapy.

Genetech Relay has received a $75m upfront payment and there's an option to enter into a profit / cost sharing agreement, or to receive up to $685m in milestone payments, plus royalties on net sales. A useful additional source of revenue, while the partnership raises a possible M&A opportunity that would likely take place at a substantial premium to Relay's current valuation.

Relay may not have secured as many or as high value deals with big pharma as some drug developers have - to name a couple, Arrowhead ( ARWR ) and Poseida Therapeutics ( PSTX ) - but arguably Relay does not need to, since it has >$1bn cash and perhaps prefers not to sacrifice future revenues for the near term cash injections such partnerships provide.

Conclusion - I Like Relay's Outlook Since I Feel I Know What I'm Investing In

An old investment adage runs that you should never invest in what you don't understand, and therefore it may sound foolish of me to say that I believe in Relay's technology and approach. Since I'm not a biophysicist or biochemist, how can I be sure I am not having the wool pulled over my eyes?

To answer that, firstly I actually find that Relay's presentations and investor communications are telling me a story that makes a certain amount of sense. Even if I don't understand precisely how e.g. the compound mapping works, having followed Relay for several years the consistency of approach - and of messaging - impresses me.

From the outset Relay has been clear about how it will use its drug discovery engine and what it's looking for. The establishment of such a promising pipeline in such a short space of time validates the approach, in my view.

Outlining an entire approach to building a breast cancer franchise to a layman cannot be an easy task, but I personally find each drug type identified and the description of how it will be used in a clinical trial both familiar in that I'm aware drugs with these mechanisms of action are in high demand, and innovative, in that it makes sense how they may be used together.

Secondly, it may only be a small market, but Relay has a genuine shot at a drug approval within the next two years. When you look at what rival developers have done in the same FGFR space, it's hard not to be impressed by Relay's data, and there's likely a bona fide opportunity in play to expand the label of RLY-4008 rapidly upon a first approval.

Thirdly, a wise investor once advised that I should "be greedy when others are fearful." Hedge funds and venture capital largely turned its back on Relay in 2022, but for those who are prepared to be more patient than institutions that have customers to impress with short-term yields and upside, Relay stock looks cheap today, in my view.

$2.1bn is still a substantial valuation for a pre-commercial company that is at least 18 months away from a first full approval in a small market, but if that continues to be the way the market thinks about Relay, I'd be broadly happy to make the bet that they underestimate this company, its technology, and its pipeline.

For further details see:

Relay Therapeutics: It Could Be Time To 'Be Greedy When Others Are Fearful'