RLAY - Relay Therapeutics: Selloff On Poor Breast Cancer Data May Have Been Overblown

2023-05-09 11:58:50 ET

Summary

- Relay is a drug developer using sophisticated modeling techniques to find better binding sites for its drug targets.

- The company's stock price had been holding up reasonably well despite the savage bear market of 2022 - thanks to some strong bile duct cancer data.

- Last month, however, the share price tanked after some very ordinary breast cancer data that generated a single partial response.

- Relay believes a higher dose of RLY-2608 may make the difference, but the market was quick to punish Relay stock.

- Relay therefore needs to find further validation for its platform before 2025, by which time its funding will be close to exhausted.

Investment Overview - Relay's Tangible Progress Since Mega-Money IPO

I've covered Relay Therapeutics (RLAY), its Dynamo drug discovery engine, and its clinical stage pipeline several times for Seeking Alpha, most recently in February when I gave the company a "buy" rating, based on its stock being oversold through the biotech bear market of 2022.

Relay joined the Nasdaq in 2020, completing the third largest biotech IPO in history, raising ~$400m at a price of $20 per share in July 2020. Today, shares have lost nearly half of their value, trading at $10.8 at the time of writing.

The elevator pitch is that Relay can leverage its powerful technology to model the behavior of genetically validated target proteins, and design drugs that can bind to them with greater affinity and selectivity, creating more potent drugs with less off-target activity. To elucidate, here are a couple of quotes from the company's 2022 10K.

While conventional approaches are well suited to solving some drug discovery problems such as orthosteric site kinase inhibitors, their reliance on static images of protein fragments limit their ability to gain accurate insights into the dynamic behavior of proteins in their natural state, which in turn limits their ability to discover medicines with exquisite specificity.

In 2016, the confluence of three forces - the proliferation of readily-available genomic data, the evolution of experimental techniques, and advancements in computational power and speed - led to the establishment of our Dynamo platform.

We believe we are uniquely situated in our ability to consolidate these advances and, when combined with our world-class team of both experimental and computational experts and experience to date, to integrate these solutions into Motion-Based Drug Design to create medicines that will make a transformative difference for patients.

Theoretically, at least, Relay's approach makes good sense, and the company's ability to identify and move four assets into the clinic has been timely.

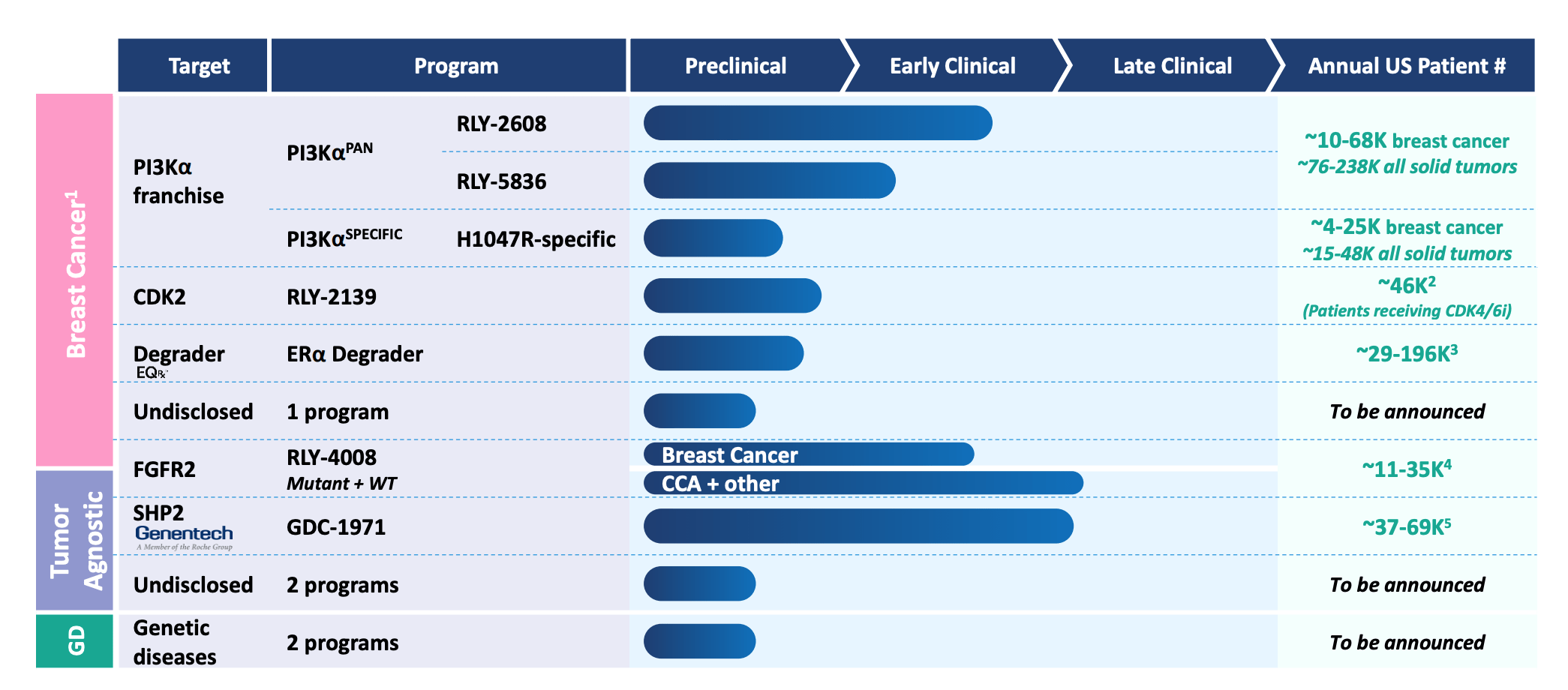

Relay Therapeutics current pipeline (Relay Corporate Presentation)

{kind=link}

As we can see above, Relay is developing a breast cancer franchise that it believes can "transform the standard of care for HR+/HER2- breast cancer," according to a recent corporate presentation , while its Fibroblast growth factor receptor ("FGFR") inhibitor has delivered some outstanding data in a Phase 2 study in patients with bile duct cancer - an 88.2% Objective Response Rate was revealed at a European Society for Medical Oncology conference presentation late last year.

With the biotech beginning to deliver clinical data to match preclinical promise, I felt back in February that Relay stock could challenge and exceed its IPO share price of $20, but unfortunately, the very positive RLY-4008 data announced at ESMO last year was followed by some much more sobering data from the breast cancer franchise, announced at the American Association for Cancer Research ("AACR") annual conference last month.

RLY-2608 Data Disappoints In Larger Breast Cancer Market

Relay describes its candidate RLY-2608 as "the first known allosteric, pan-mutant and isoform-selective phosphoinostide 3 kinase alpha, or PI3K?, inhibitor in clinical development." Relay says that PI3K? is "the most frequently mutated kinase in solid tumors, and ~100k breast cancer patients in the US currently express the PI3K? mutation.

PI3K? is expressed in ~14% of all solid tumor cancers, Relay says, comparing that to EGFR - expression in 7%, ERBB2, 6%, and BRAF, 6%. Drugs targeting these three proteins - Tagrisso targeting EGFR, for example, Herceptin Ein RBB2, and Braftovi in BRAF represent markets of respectively ~$7bn, ~$9bn, and ~$2bn.

There's only a single approved therapy targeting PI3K? - alpelisib, marketed and sold by Novartis under the brand name Piqray, and earning $116m of revenues in Q123, but Relay says that Piqray has notable limitations due to the fact it's not mutant-selective, leaving patients in danger of experiencing hyperglycemia. According to OncLive :

Currently, 4 PI3K inhibitors are approved by the FDA in hematologic malignancies based on single-arm data: idelalisib (Zydelig), copanlisib (Aliqopa), duvelisib (Copiktra), and umbralisib (Ukoniq), the latter of which was recently withdrawn from market

The fact that Zydelig earned <$50m of revenues in 2022, and that TG Therapeutics ( TGTX ) Ukoniq was withdrawn from sale speaks to the clear difficulties involved in making PI3K inhibitors work, but preclinical data certainly seemed to endorse Relay's candidate.

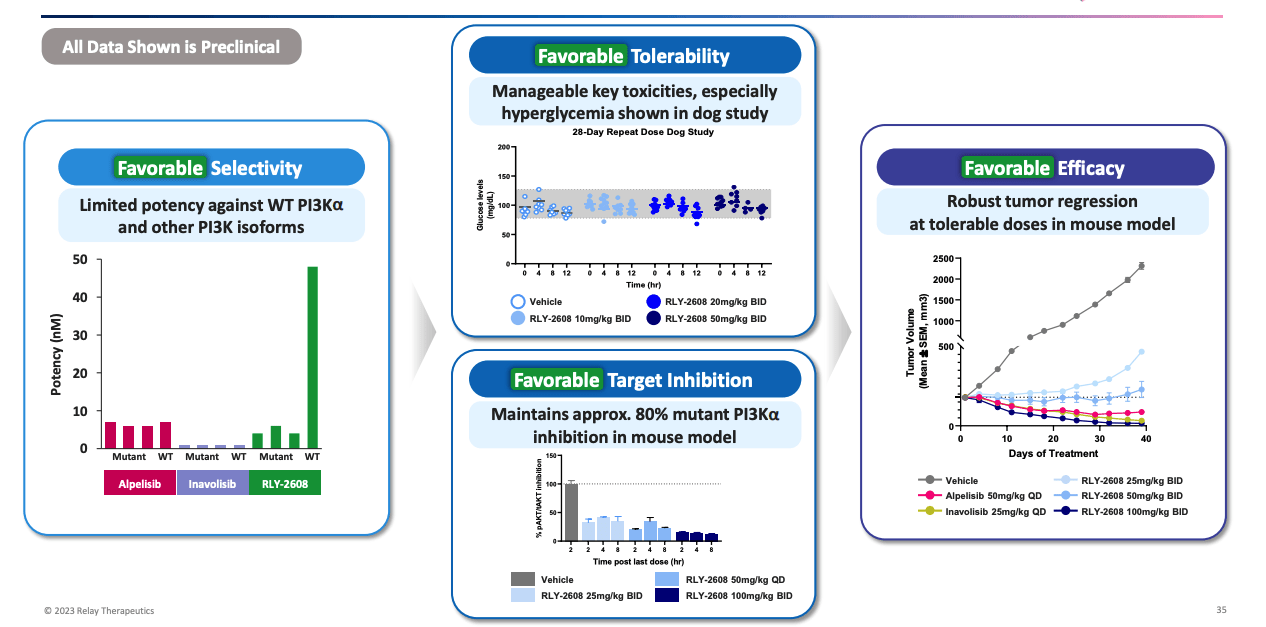

RLY-2608 - preclinical data (Relay Presentation)

{kind=link}

Safe, effective, and targeting a kinase expressed in a large subset of all solid tumor cancers, if RLY-2608 could deliver in the clinic, it would represent a potentially much larger market opportunity than RLY-4008.

What the data presented at AACR last month showed, however, is that although RLY-2608 showed ~80% target inhibition, and appeared safe, with no Grade 3 instances of hyperglycemia, or rash or diarrhea reported, its efficacy was weak at the selected doses, which ranged from 100mg BID, to 800mg BID.

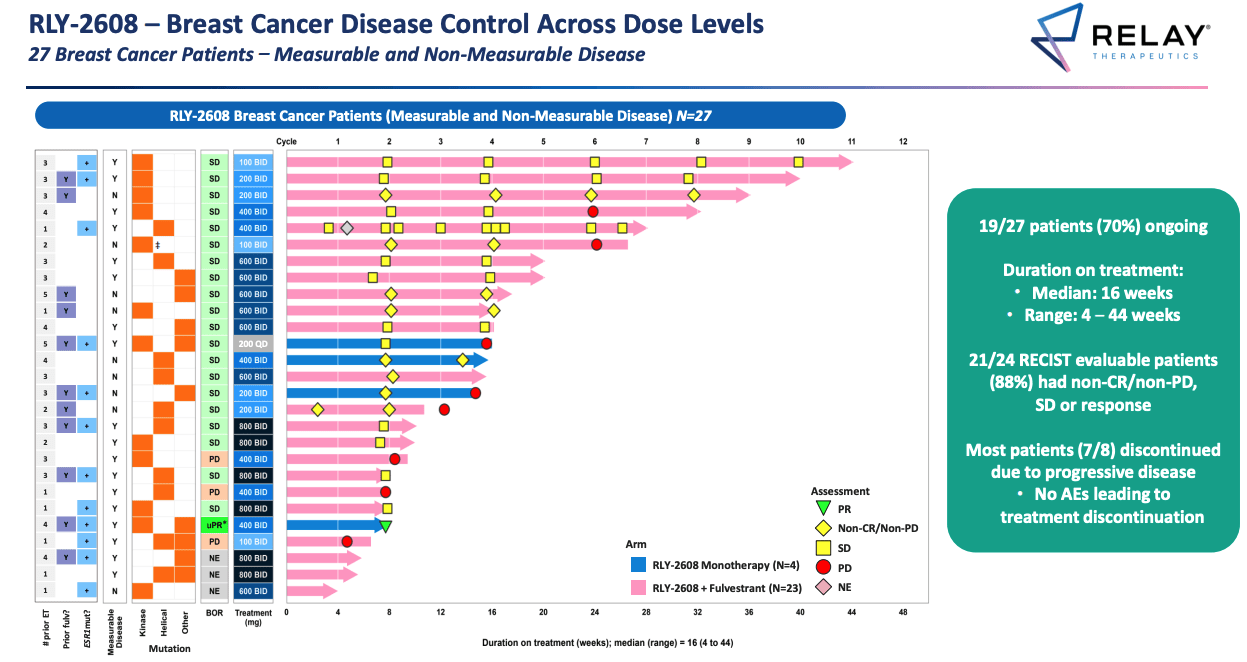

RLY2608 - breast cancer disease control (Relay presentation)

{kind=link}

As we can see above, only a single partial response was achieved out of a patient pool of 27 in breast cancer, while there were no responses of any kind in any other tumor type. Being safe and well tolerated is all well and good, but ultimately the drug must be capable of shrinking tumors, which based on the Phase 1 ReDiscover data collected to date, RLY-2608 is not.

As soon as the data were released Relay's share price tumbled from >$18, to $11.5. The company - and its supporters, defended itself, pointing to highlights such as a lack of off-target toxicity, and, according to Relay's President and CEO Sanjiv Patel, the fact that:

Of the eight patients with measurable breast cancer who received a dose at target exposure, one experienced a confirmed partial response after data cut-off and the other seven experienced a best overall response of stable disease; seven of these patients continue on treatment. Given the early but promising nature of these data, we are moving quickly to initiate dose expansion cohorts in the second half of the year."

The last sentence of the above quote - promising a rapid move into the dose escalation portion of the study - is possibly a tacit acknowledgement on management's part that the data disappointed. Given that the safety data was positive, however, dose escalation is an avenue that is still available to Relay.

Analysts at Raymond James called the sell-off post AACR "overdone," claiming that the safety angle validated the Dynamo platform. The median treatment duration was additionally only four months, potentially not quite long enough for the drug to have reached its full effect. 70% of patients remained on the treatment at the data cut-off date.

It's certainly still early days for Relay, a company that was founded in 2015 and has been listed for less than three years, and even if RLY-2608 proves to be a busted flush shareholders should not necessarily be too disappointed - drug development takes a long time, and typically there are ~10 failed candidates for every success.

While the Dynamo platform is designed partially to reduce the odds of failure, it's clearly not going to completely derisk the drug development sector.

Looking Ahead - Catalysts To Keep An Eye On

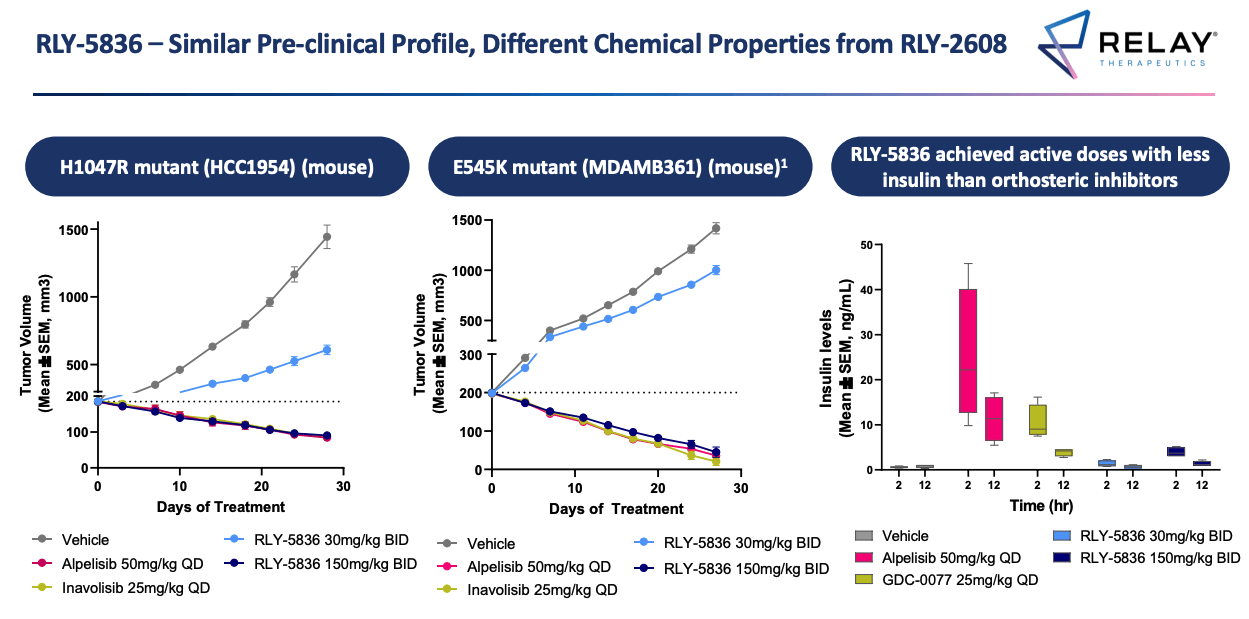

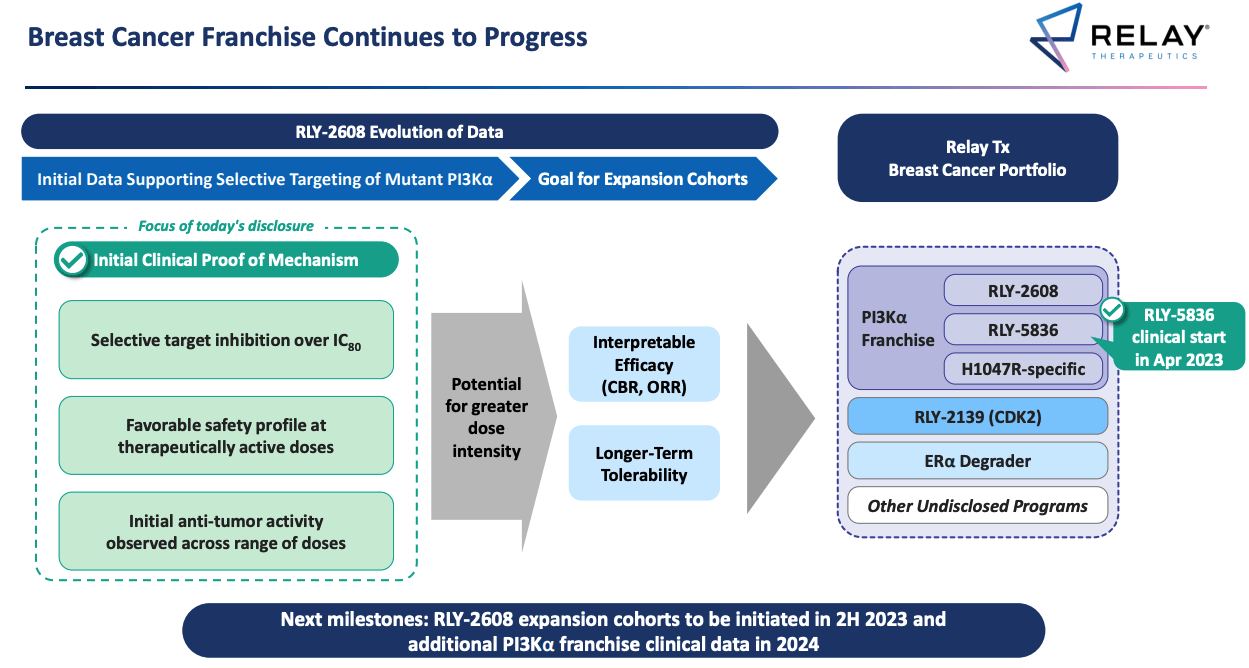

The next round of RLY-2608 data will not now arrive until 2024, but in the meantime, another PI3K? Pan inhibitor has entered a Phase 1 study - RLY-5836. Relay says it has a "similar preclinical profile," but "different chemical properties" from 2608, and it has shrunk tumors in mice, although apparently only at a much higher dose than its PI3K rivals:

{kind=link}

There isn't a timeline available for RLY-5836 data yet, although a concern may be that it's not sufficiently differentiated to 2608 to make an impact in the clinic - which would be bad news for Relay's planned assault on the breast cancer sector. Of course, we don't know that yet, and the opposite could be true.

Relay breast cancer franchise progress (Relay presentation)

{kind=link}

As we can see above, besides 2608 and 5836, there's a third member of the PI3K franchise, RLY-2139 which is targeting CDK2 as opposed to PI3K, and a protein degrader - an intriguing mechanism of action that essentially marks mutated proteins out for destruction by the immune system, currently being pioneered by 2 other biotechs, Kymera Therapeutics ( KYMR ) and Nurix Therapeutics ( NRIX ).

Nevertheless, to say that Relay is developing a "breast cancer franchise" would be a little premature, after the 2608 data has shown how much more needs to be done to validate the key candidates, if they can be validated at all.

Other Factors Influencing Relay's Valuation

Relay's market cap is presently just over $1.3bn, and in its latest presentation the company reports a cash position of $938m. That may sound like a substantial sum for a biotech - most drug developers would give an arm and a leg to be in such a strong financial position - however management only expects current cash to last until 2025.

Relay made a loss from operations of $102m in Q123 - the problem with its technology is that, as powerful as it may be, it is also expensive to run, and requires hundreds of well paid, highly qualified staff to make it run. Since it seems unlikely that Relay will have an approved drug on the market by 2025, let alone one generating >$100m per quarter in revenues, Relay may find itself needing to complete substantial at the market fundraisings which will dilute the value of shareholders holdings.

One thing that could provide a boost to Relay's finances and chances of commercial success is a partnership with a larger pharma - these partnerships usually come with a cash injection and plenty of pledged development and commercial milestone payments.

Relay does have such a partnership - with Roche's ( RHHBY ) drug development subsidiary, although it's relatively low key thus far. According to Relay's 10K submission:

In December 2020, we entered into a global collaboration and license agreement with Genentech for the development and commercialization of RLY-1971 (now referred to as GDC-1971). Genentech initiated the cohort of GDC-1971 in combination with GDC-6036, its KRAS G12C inhibitor, in a Phase 1b trial in July 2021, and a Phase 1b trial of GDC-1971 in combination with atezolizumab, its PD-L1 antibody, in August 2022.

Atezolizumab is Roche's Tecentriq, an immune checkpoint inhibitor ("ICI") that is a rival to Merck's ~$20bn per annum ICI Keytruda, and Bristol Myers Squibb's Opdivo. Roche would like nothing better than to find a combo therapy capable of outperforming these two dominant drugs, and increasing its own market share - Tecentriq earned >$4bn in 2022.

Genentech is mainly responsible for the development of this drug, and the scheduling of data readouts, but there's at least a large market opportunity here which Relay estimates is in the region of 37 - 69k patients. Relay would likely earn only a small share of net revenues from this deal, but success may persuade Genentech to develop more candidates, and attract other pharmas to the platform.

Concluding Thoughts - Time To Sell Relay? Not Yet, But Next Data Set Could Be Decisive

After the success of the RLY-4008 data - which should not be underestimated, given the >85% response rate is nearly double that of any approved drug in bile duct cancer, apparently, with a superior safety profile - the RLY-2608 data reveal does feel like two steps backward unfortunately, and the market's frustration is understandable.

Ultimately, Relay hasn't quite validated its technology, and doubts persist about the "science of drug discovery" - even with the most advanced technology, arguably Relay is still in the business of finding needles in haystacks, albeit with a much higher cash burn than many of its rivals.

Relay had been promising a breast cancer franchise that could tackle a variety of different lines of therapy, validated targets, and work in combo with other therapies, but now that entire franchise is under threat, and the company may have a better chance of securing approval in this indication with 4008, not 2608, or 5836.

Nevertheless, I'm not quite prepared to hand Relay a "Sell" recommendation just yet. The excellent RLY-4008 data gives management a stay of execution, in my view, and although the bile duct cancer market may be small, the label expansion opportunities are promising and there is a non-CCA cohort in the current ReFocus study that is looking at various solid tumors.

Meanwhile, could it be possible that the 2608 data improves over time, as patients use the therapy for longer, or that a larger dose starts to result in better efficacy? Or, could the next-generation 5836 deliver where 2608 struggled, thanks to some tweaks made in the lab?

I would not dismiss either of those eventualities, nor the prospect of a positive result with the Genentech partnership, nor further partnerships with other large pharmas.

In a recent note I was critical of the business model of AbCellera, another tech / AI enabled drug developer, that's focused on commercial partners only and does not develop its own drugs. After three years as a listed company, Relay has put together a proprietary pipeline, with at least one drug that looks distinctly approvable. That drug may not solve Relay's cash flow problems, and the breast cancer franchise may now require a rethink, but even so, based on progress to date, Relay's business deserves to be valued >$1bn in my view - in the region of 5x the future peak sales potential of RLY-4008.

It's also the case that by the time 2025 comes around and finances are dwindling, Relay must have found some further validation for its platform, whether it comes from better breast cancer data, the Roche partnership, label expansions for 4008, the protein degrader, a new partner, or a different source entirely. There has been enough post-IPO success to suggest that Relay can deliver that validation, in my view.

I think Relay should be targeting $500m in revenues by 2030. At 5x peak sales potential that could imply Relay's market cap ought to be higher - ~$2.5bn - but bearing in mind the time value of money, and the risk, I would say a valuation of $1.5bn - 2bn would be appropriate.

The long wait for more data will likely see some downside in play in the coming months - I think picking up Relay stock <$10 is a strategy that could pay off for long-term, patient, investors looking to add a dollop of risk to their portfolios.

For further details see:

Relay Therapeutics: Selloff On Poor Breast Cancer Data May Have Been Overblown