RLXXF - RELX: AI And Data Can Drive Big Gains

2023-07-16 00:46:30 ET

Summary

- RELX PLC specializes in providing information-based analytics and decision tools to professional and business customers worldwide.

- The business has developed a market-leading position in the provision of data analytics for a wide range of industries.

- AI represents an unquantifiable opportunity to develop its analytics capabilities further. This will be supplemented with M&A.

- Revenue is highly reoccurring with an EBITDA-M of 31%. The business is highly attractive long term.

Investment thesis

Our current investment thesis is:

- RELX is growing well as the demand for information and data analytics continues to improve.

- Its financial profile is fantastic, with an EBITDA-M of 31% and a series of supporting transactions.

- Its diversified scale gives the business a defensible position against new entrants.

- AI represents an opportunity for supercharged returns in the coming years if the company executes.

Company description

RELX PLC ( RELX ) specializes in providing information-based analytics and decision tools to professional and business customers worldwide. The company operates through four segments: Risk, Scientific, Technical & Medical, Legal, and Exhibitions.

Share price

RELX's share price has made consistent gains across the last decade, generating returns of over 150% during this period. This is a reflection of consistent financial improvement across the period.

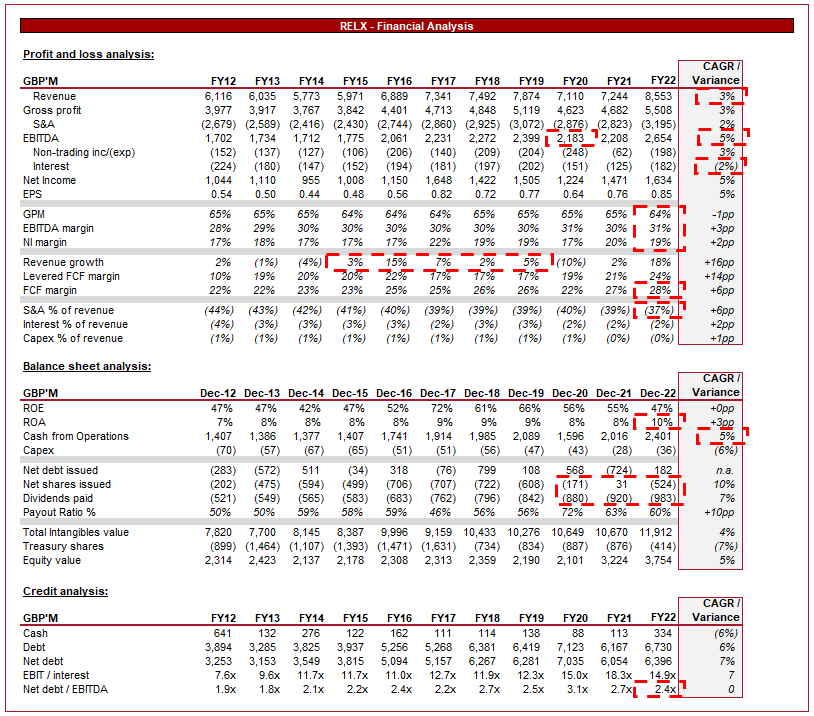

Financial analysis

{kind=link}

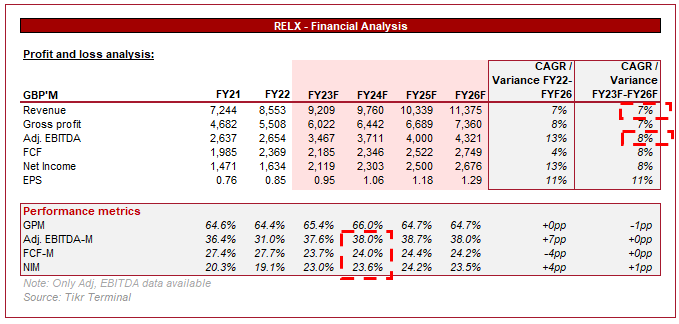

Presented above is RELX's financial performance for the last decade.

Revenue

Revenue has grown at a CAGR of 3% across the historical period. This is a soft performance by the business as it implies purely inflationary price increases during the period.

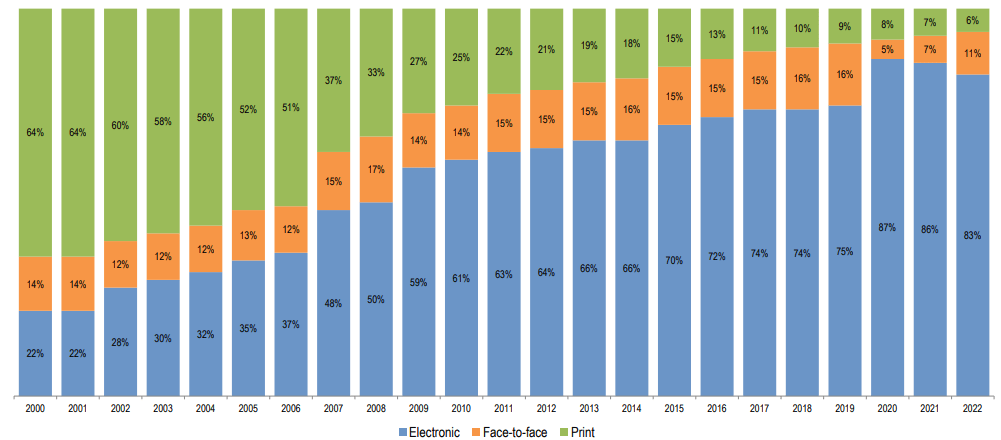

Before we do a deep dive into the company's earnings potential, it is worth understanding RELX's revenue profile.

The company has transitioned from print and face-to-face to electronic, as technological development encourages ease of information transfer. This improves the distribution potential of the products globally and reduces the need for headcount growth in line with revenue.

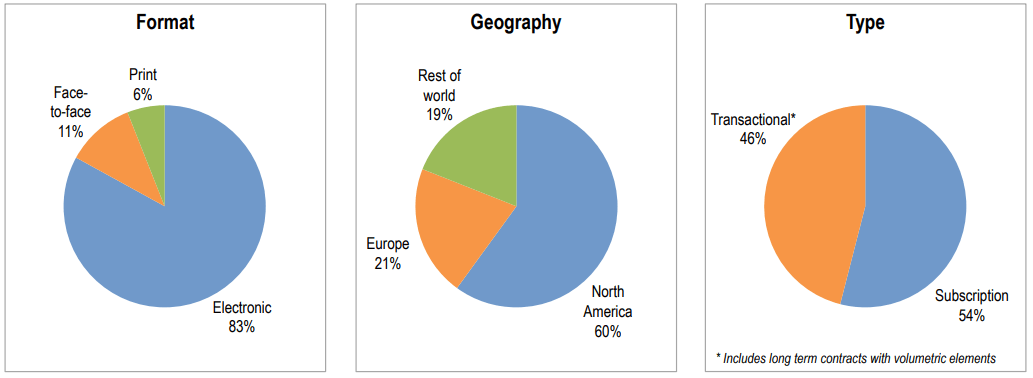

{kind=link}

Further, the company is globally diversified, with NA representing the largest segment of revenue (60% of FY22). This is a reflection of the standardized nature of RELX's product, allowing RELX to sell to any type of business. This represents an opportunity over time to target growth markets.

Finally, the nature of revenue is high quality. c.54% (FY22) is subscription based (with transactional being long-term contracts with volume-based elements), which is recurring in nature. With high-quality products, this is generally "sticky", which means customers stay Y/Y. RELX then has the scope to initiate incremental price increases, essentially smoothing out its revenue profile. The early concern here is that with a growth rate of c.3%, the company seems unable to materially grow its transactional segment and generate upsell.

{kind=link}

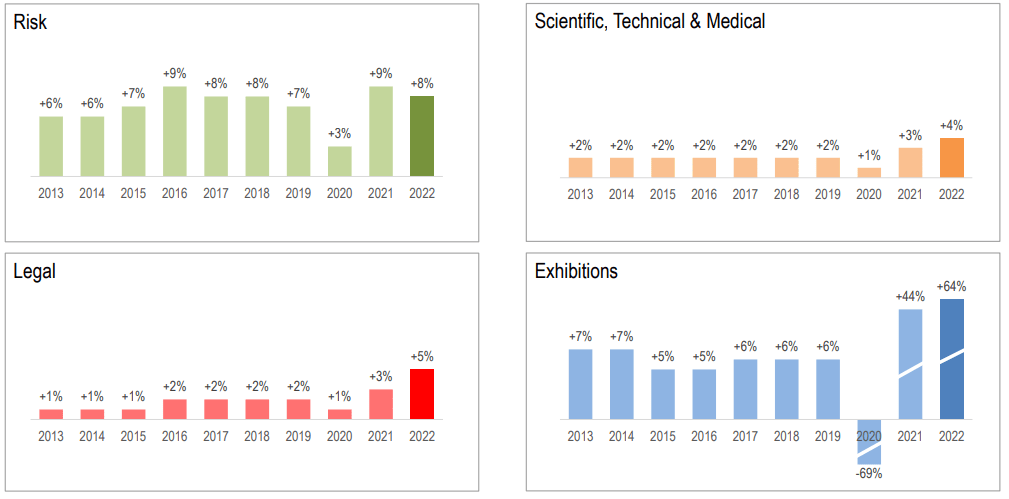

Overarchingly, RELX's 4 divisions have generated consistent growth in recent years. Risk and Exhibitions have outperformed, while STM and Legal have been softer.

This immediately flags another issue. The revenue growth looks disjointed from the divisional growth. This is partially due to the impact of FX, as RELX issues its accounts in GBP. With a substantial amount of income generated in NA, RELX faces the risk of a depreciation in the USD vs. GBP (Which are currently experiencing).

{kind=link}

Risk

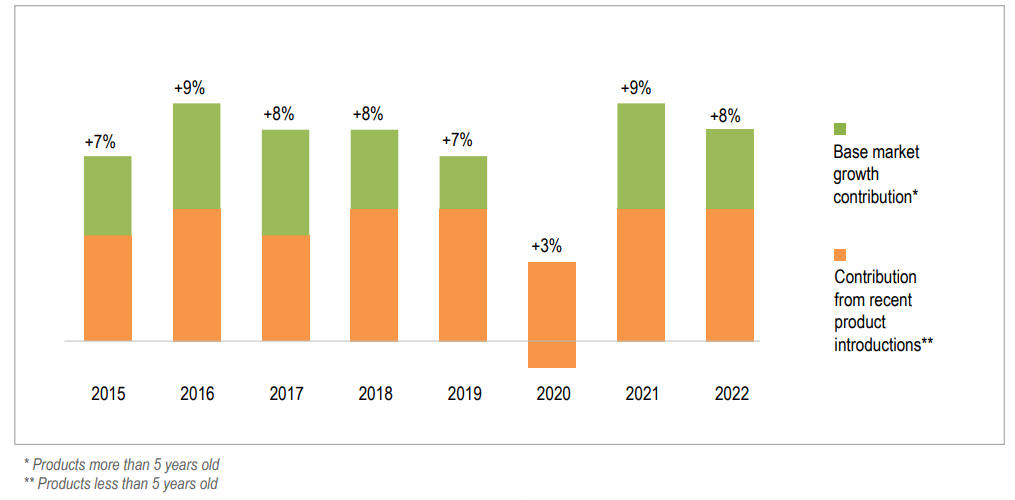

The Risk segment offers analytics and decision tools that utilize technology and algorithms to evaluate and predict risk by combining public and industry-specific content. This is the joint largest part of the business, generating c.£2.9bn in revenue (34%).

Risk is an area of growth in our view, as current business conditions are arguably the most risky in history. Firstly, regulatory conditions continue to develop globally and are becoming more stringent and complex. This has contributed to greater demand for information in order to support decision-making. Secondly, businesses face a wide range of industry-related risks (Financial crime, credit risk, fraud, etc.), which information can help understand and mitigate. RELX's value proposition is that it works with petabytes of data and creates a valuable output that can be easily analyzed, visualized, and modeled.

Further, this is an ever-evolving space and so innovation is key. RELX has seen strong growth from new products introduced, suggesting it is remaining highly competitive in the market.

{kind=link}

Risk is weighted more toward Transactional than average, but we note c.90% of this is based on volumetric indicators and so is quasi-subscription based. Given the strong growth, this suggests an increasing volume of purchases over time.

Risk (2) (RELX)

Scientific, Technical & Medical

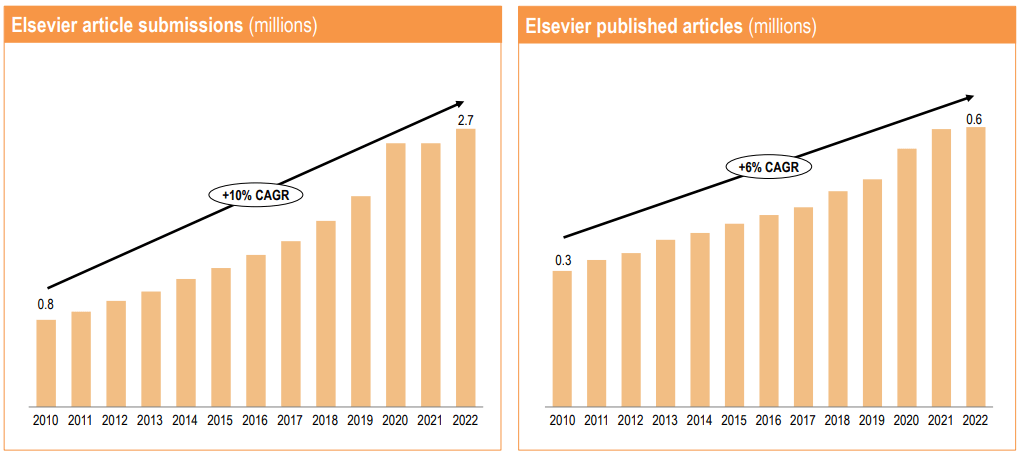

The Scientific, Technical & Medical segment provides information and analytics to support scientific progress and advance healthcare. This is the joint largest part of the business, generating c.£2.9bn in revenue (34%).

Demand for STM information is in large part driven by research conducted by individuals to seek insight into a wide variety of fields. The informational development for RELX is illustrated in the following graphs, with published articles growing at a CAGR of 6% and submissions at a CAGR of 10%. This reflects a healthy increase in new and available findings.

{kind=link}

This translates into soft revenue growth in the last 8 years. Our view is that RELX is underperforming in this regard. Technological development in the pharmaceutical industry has been exponentially rising in recent years, suggesting a higher growth rate is achievable.

STM (2) (RELX)

The majority of this revenue source is subscription based, which given the recurring and continuous nature of scientific publishing, looks reasonable. It is likely clients will want access regardless of the level of usage.

STM (3) (RELX)

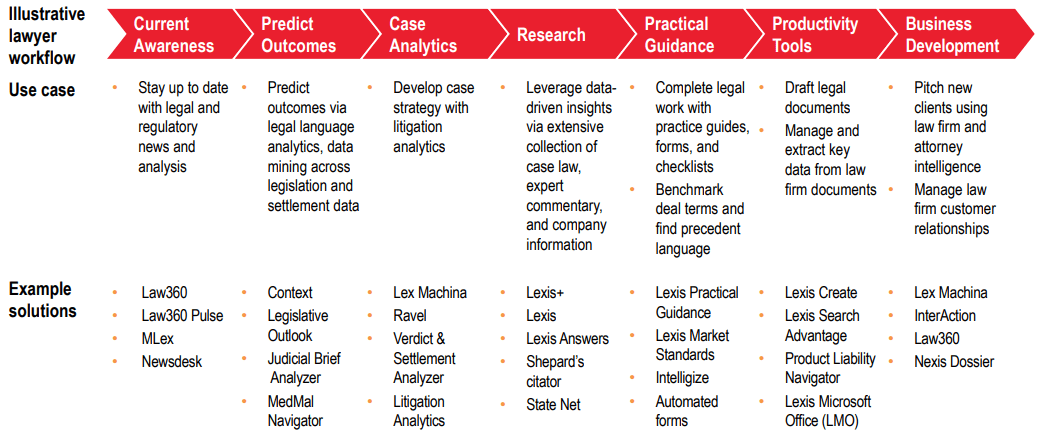

Legal

The Legal segment offers legal, regulatory, and business information and analytics to aid decision-making and increase productivity for customers. This is the third largest segment of the business, generating c.£1.8bn in revenue (21%).

Legal operates similarly to a combination of Risk and STM. This represents an opportunity for improved growth as historically, RELX has focused on the provision of reference/research information. This is transitioning toward what Risk is offering, which is information that can be used for analytics and decision-making. We can see this contributing to growth levels similar to that of Risk, 4-6%, in the coming years. There is a wide breadth of services.

{kind=link}

Growth thus far has been mild but there is a clear improvement in the last 2 years, which could be evidence of the product transition RELX is currently experiencing.

Legal (2) (RELX)

Similar to STM and for the same reasons, revenue is weighted toward subscriptions.

Legal (3) (RELX)

Exhibitions

The Exhibitions segment combines face-to-face interactions with data and digital tools to assist customers in learning about markets, sourcing products, and completing transactions. This is the smallest part of the business, generating c.£0.6bn in revenue (7%).

Growth has been strong in the last 7 years, marginally impacted by Covid-19. This represents an opportunity to advertise the business beyond anything in our view. It generates a material amount of revenue and we do not want to diminish this, but it is clear that scaling this is not feasible. We do not want to see the business recruiting a significant number of heads due to the operational cost and thus margin impact of doing such a thing.

Nevertheless, demand is strong. This represents a "buy-in" from corporates that RELX is a reliable provider of information.

(1) Exhibitions (RELX)

Revenue is primarily from fees, which reduces the downside risk of low admission.

Exhibitions (2) (RELX)

AI

Between 21st Apr and 8th May 2023, RELX's share price declined by almost 10%. Why? Investors suddenly feared the demise of RELX in the wake of AI (The share price remains down c.5% from this level).

So is AI actually a risk? We think so (Spoiler alert, not close to the degree some are suggesting). AI allows businesses to rapidly crunch data and produce real-time analytics. The true value is in its adaptability and response potential to changing variables.

Investors are underestimating the potential of a c.£60bn business. RELX will not sit back and be innovated out of the market it dominates. The company acquired Aistemos in February , a company that uses AI to classify patents. Further, RELX announced it is already using generative AI to upgrade its legal, health, and science products. We expect continued investment into this space in the coming 3-5 years.

If RELX executes properly, this will be the biggest opportunity since the transition to electronics (the company is over 100 years old). The company has already transitioned to being an analytics provider (information & value enhancement) and so the informational threat from AI is far lower. AI will make what RELX is doing easier and thus potentially contribute to improving margins.

Margin

RELX has fantastic margins. It has an EBITDA-M of 31% and a NIM of 19%.

EBITDA-M has marginally improved over the historical period but for the most part, has remained sticky. This implies no material degradation in the company's competitive position.

The majority of this profitability directly translates to FCF, which has shown little cyclicality or volatility. This allows the business to accumulate cash for distributions and also M&A, which can support further growth.

Balance sheet

RELX is conservatively financed, with an ND/EBITDA ratio of 2.4x. This gives the business scope for further M&A and flexibility in the event of changing circumstances.

The strong cash flow is reflected in RELX's distributions, with a healthy dividend yield partnered with buybacks.

Outlook

{kind=link}

Revenue growth is forecast to improve interestingly, with analysts expecting a 7% growth rate. This is a reflection we believe of the AI improvement scope, as well as the developing demand for value-driving analytics. Margin improvement is also forecast, likely driven by operational cost leverage in line with what has been achieved in the last decade.

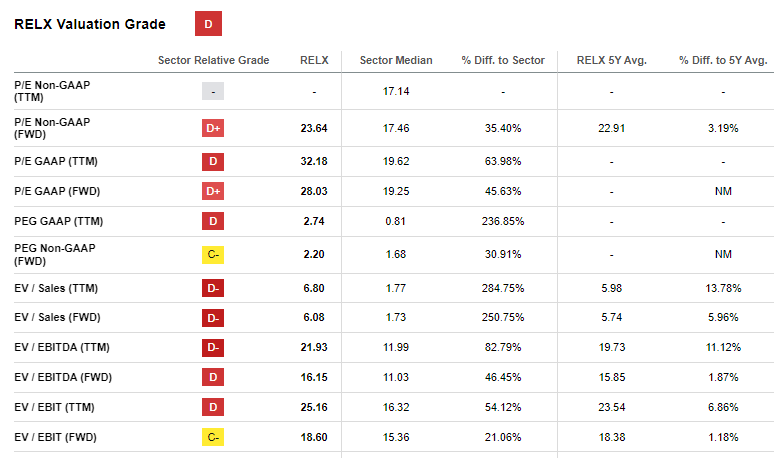

Valuation

{kind=link}

RELX is currently trading at 16x NTM EBITDA and 23x earnings. This current valuation is a premium to the 10Y historical average of 12x/17x. This premium is driven by the following factors in our view:

- Strong underlying growth despite the top-line figures masking this.

- Margin improvement and protection of said margins with scale are impressive.

- The underlying demand for analytics and informational insight is increasing. Further, slower growth segments such as Legal and STM are transitioning toward this.

The unquantifiable portion is the impact of AI. If RELX utilizes this to improve the quality of its output, alongside reducing its cost to analyze, we would not be surprised to see a substantial increase in share price.

Key risks to our thesis

The key risks to our thesis are:

- FX. As a global business, the company faces concerns around unfavorable movements of the Sterling (reporting currency) against various currencies it earns revenue in. This has the potential to depress earnings.

- AI. As a globally diverse and mature business, there are few risks to a company beyond fundamental change. Although we consider AI to be a key opportunity, failed development can quickly make this a concern if its competitors are able to sufficiently improve their offering relative to RELX.

Final thoughts

RELX is a fundamentally resilient business. Revenue growth is strong for a mature business, margins are extremely attractive, and the industry is facing tailwinds as the demand for insight improves.

We like the current iteration of the business given its size, which means competition is unlikely to materially dislodge the business. Further, it is positioned well to conduct continuous M&A to enhance its current product suite.

We believe AI represents opportunities for the business. Generative AI will likely be a game changer for analyzing and interpreting information and so RELX is best placed to exploit this. We see this as an unquantifiable potential upside currently.

For further details see:

RELX: AI And Data Can Drive Big Gains