RELX - RELX: Share Price Looks Fully Valued Even For Strong Business Performance (Rating Downgrade)

2023-10-26 05:23:13 ET

Summary

- RELX has a strong business performance with double-digit growth in revenues and profits for the first half of the year.

- The company's dividend outlook remains solid, with a history of consistent growth and a target cover of at least two times.

- The current valuation of RELX shares is fully valued, leading to a downgrade from buy to hold, despite potential opportunities with AI in the future.

While the P/E ratio is lower than for information rivals like Equifax U.K.- based information and exhibition provider RELX (RLXXF) has an attractive set of businesses and a long record of strong profitability. But its share price has grown strongly lately, affecting the attractiveness of its current valuation.

I last covered the name in my January 2022 buy piece Improving Performance Underlines Investment Case , since when the shares have moved up 17%.

My thesis at that time continued to be that the core of the company consisted of stable businesses with steady ongoing demand and an attractive competitive positioning, while the ongoing problems in the exhibition business caused by the pandemic would likely pass with time.

Business Performance is Strong

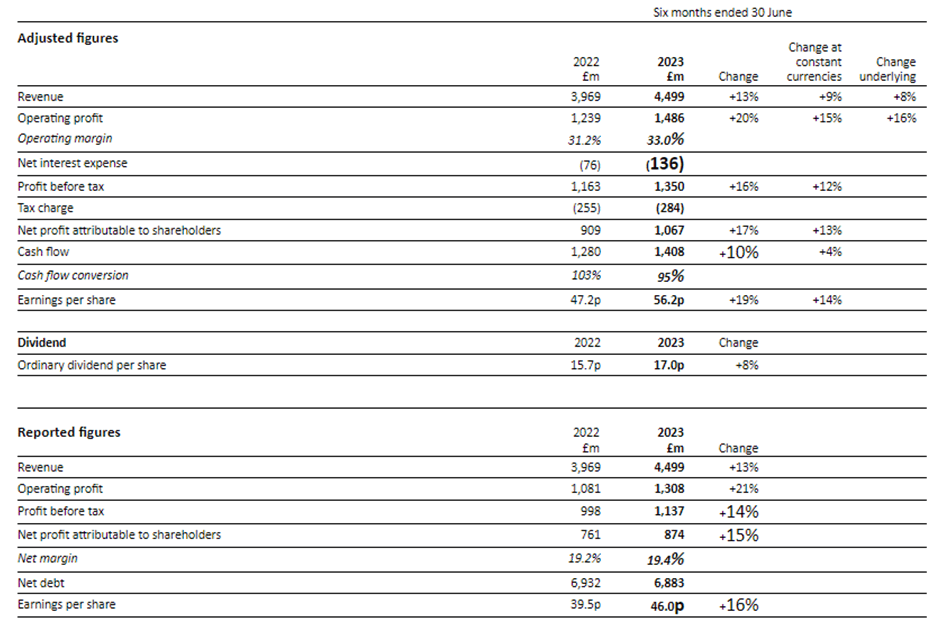

The company released fairly concise interim results in July that showed the company continues to move forward well, with both revenues and profits for the first half of the year showing double digit percentage year-on-year growth.

Interim results (Interim results announcement)

{kind=link}

The full-year outlook was affirmed, which is that the company expects underlying growth rates in revenue and adjusted operating profit to remain above historical trends. It foresees another year of strong growth in adjusted earnings per share (on a constant currency basis).

RELX has been busy buying back £800m of its own shares, which could help earnings per share though given the current market capitalisation of £54bn is fairly small beer. Given my view of the current valuation, discussed below, I do not see that as a great use of funds at the moment albeit it should help boost earnings per share.

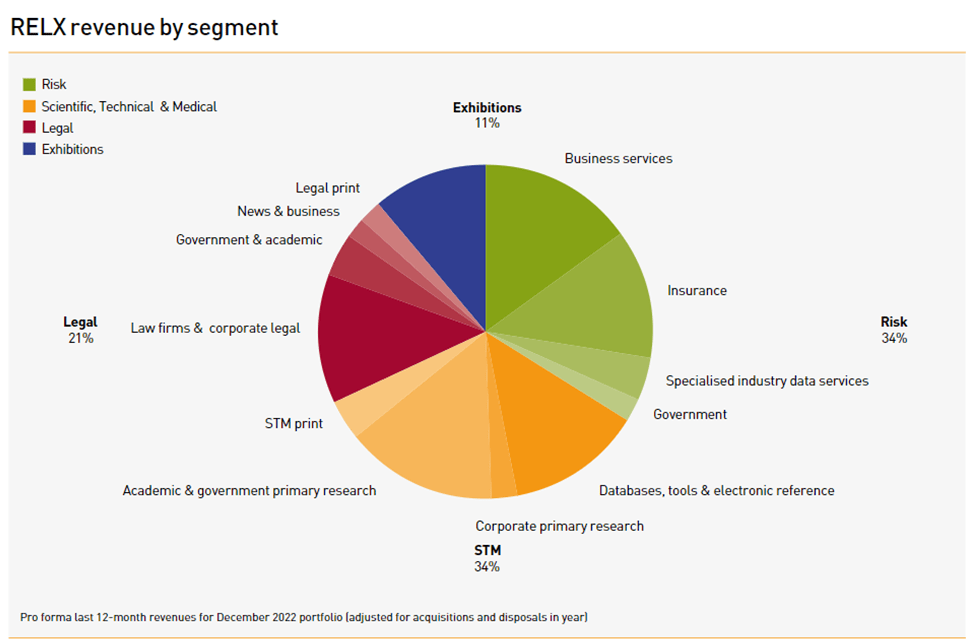

More detail on business performance in the interims would have been helpful in assessing the overall performance of specific business divisions.

Last year's full-year results, though, provided more detail on divisional performance and weight within the company.

{kind=link}

Some Risks

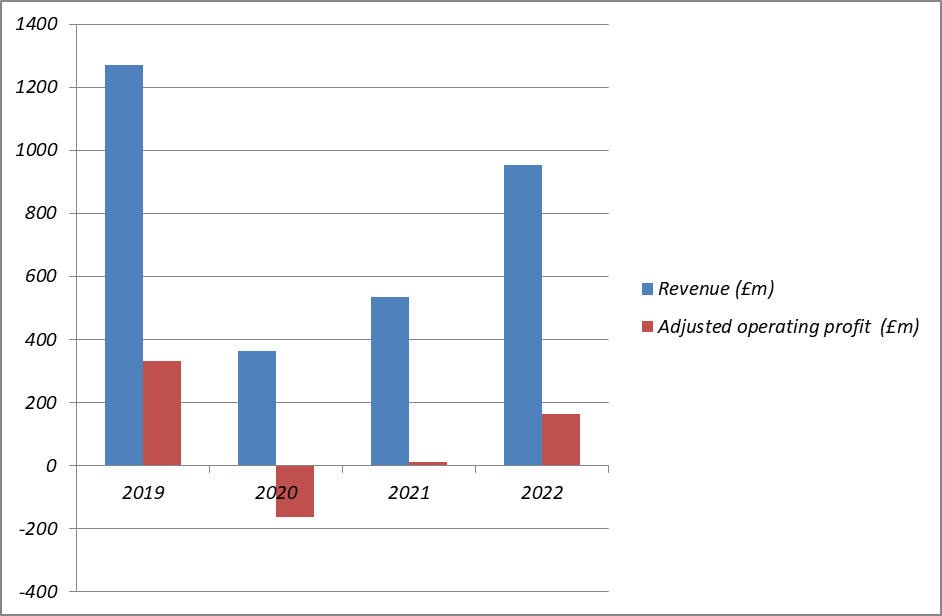

While the exhibition business continued to improve financial performance last year, revenue and adjusted operating profit continue to lag pre-pandemic levels.

Chart compiled by author using data from company annual reports

{kind=link}

With time, the division may come back to its former profit levels. But I think the risk of another unexpected plummet in demand for exhibitions must be considered one of the key ongoing risks for RELX. The pandemic battered demand in the exhibitions business more or less overnight, with big negative implications for RELX. Such a risk could materialise in various ways in future, whether due to a pandemic or some other event that significantly reduces international travel, such as a recession.

I also see AI as both a risk and an opportunity for the firm. Although it provided potential (discussed below) it could also lower the competitive barriers to entry in an information rich business, hurting RELX's pricing power.

Dividend Outlook

One of the historical attractions of the shares was the solid dividend and this continues to be the case. Since the turn of the century, the company has only failed to grow its annual dividend once (in 2010), and in that year it kept the payout level.

Last year the annual dividend - which increased by 10% -- was covered by earnings 1.9x. Free cash flows after dividends of £983m came in at £208m, which while fine for now would provide limited scope for double digit dividend increases in the coming years with that fairly narrow free cash flow.

Indeed, while this year's interim dividend rose, that was an 8% increase to 17p per share, suggesting a prospective annual dividend yield of around 2.1%.

RELX remains a fairly cash generative business and I expect it to continue to increase its dividend. The dividend policy is "over the longer term, to grow dividends broadly in line with adjusted earnings per share, while targeting cover of at least two times."

Valuation Downgrade

Given the increase in share price since my 2022 article, how does the valuation currently look?

On a price-to-earnings ratio of 28, I now think the shares look fully valued. Accordingly I lower my rating from buy to hold. A similar view was taken by The Value Pendulum in last month's piece RELX: Taking A Breather (Rating Downgrade) although more bullish recent coverage can be found in Welbeck Ash Research' July note RELX: AI And Data Can Drive Big Gains . While the P/E ratio is lower than for information rivals like Equifax (EFX) - currently trading on a P/E ratio of 42 - it still does not look to me like it offers an attractive entry point for a business that, over the long term, offers modest growth opportunities (CAGR of earnings per share in the past decade has been 5.7%, which I see as solid but not outstanding).

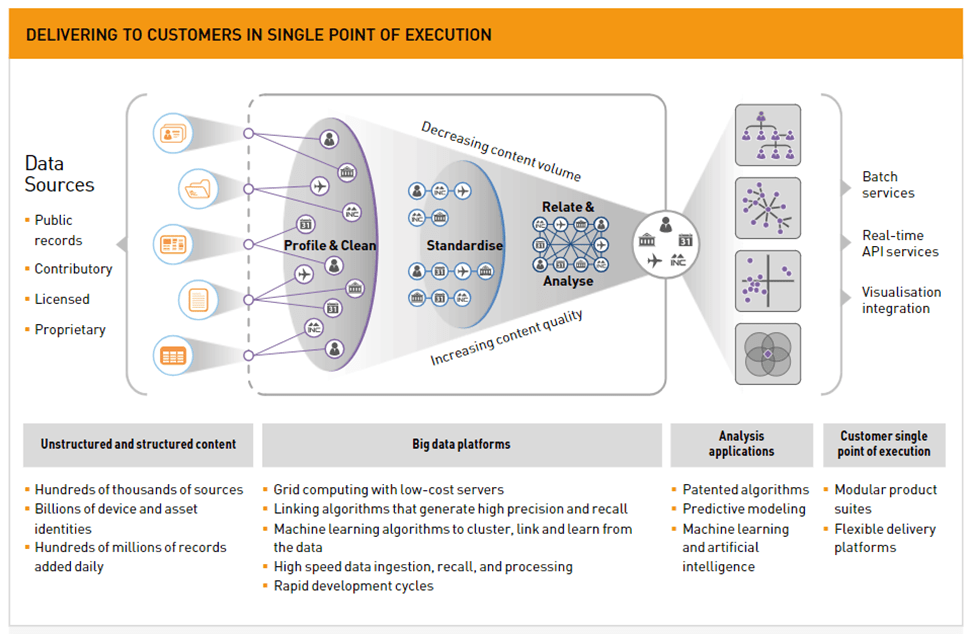

In principle I think AI could yet turn out to be a driver for more value, if RELX is able to use it to lower its costs in information-heavy parts of its business like LexisNexis where AI could feasibly play a useful role. In the interim results, the chief executive made this point explicitly:

By embracing artificial intelligence technologies for well over a decade we have been able to develop and deploy these analytics and decision tools across the company, and we believe that our ability to leverage AI, as it evolves, will continue to be an important driver of our business going forward.

This is an illustration of how this could play out practically.

{kind=link}

Last year, for example, RELX's Insurance Solutions division acquired Flyreel, a property insurtech that uses AI and machine learning to enable self-service property inspections. For now, though, I think such use of AI feels experimental and marginal rather than transformational, so I do not see it driving substantial valuation changes in the near-term future.

I continue to see RELX as a strong, resilient and solid business for the long term. But I do not find the current share price attractive as an entry point.

For further details see:

RELX: Share Price Looks Fully Valued Even For Strong Business Performance (Rating Downgrade)