RELX - RELX: Substantially Overvalued Be Careful

2023-05-02 08:24:28 ET

Summary

- RELX PLC is a company I've reviewed in the past, considering it to be overvalued, and more so at this time. RELX has outperformed, but I view it as dangerous.

- RELX only has upside if this valuation holds - and I do not believe it will. Even if it does, it's too much for what is on offer.

- I give you my update on RELX and an updated price target for the company.

Dear readers/followers,

It's important to know when something is too expensive. I believe this was the case for RELX PLC ( RELX ) the last time I wrote about it, and I believe it's the same scenario we have at this particular time - with RELX up around 15% since my last article. I love investing in quality companies, but not at any price.

This article will serve as an update going into 2023 and the first quarters of the year. If anything relevant is reported to change this particular thesis or the price target that can be justified, I will edit this article over the coming weeks - but for now, here is my update for RELX.

RELX - An update

This is a pretty complex company, and hard to describe in simple or quick terms. In essence, if offers companies decision-making tools. Now, as anyone who at any time has worked for a large organization, you'll likely know that efficient decision-making equals profitability and productivity. So the theoretical appeal of a company such as this is absolutely massive. RELX has a long tradition that technically goes back to the 1880s, and RELX is the name it has held since 2015.

At first, it started out as trade books, magazines, and scientific publications - and there is still some of that inherent to the company's mix - but less than 10% at current revenues.

It works through a mix of M&As and organic growth, and is a Europe-based company that has a very attractive earnings profile, in terms of its history. This company is extremely rare in seeing earnings declines. They do happen, but usually less than 5%. Only 3 times during the last 20 years has the company recorded an EPS decline larger than 5%.

{kind=link}

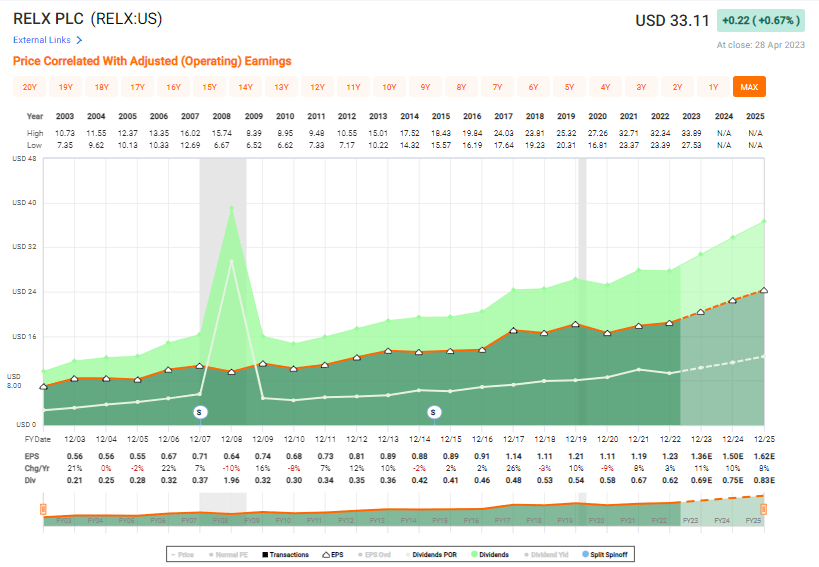

If you had invested in the company 20 years back, you would have generated market-beating EPS of around 8% since that time. It's not exactly the best available, but at the right times, this company could have really provided market-beating upside - especially if you start adding an eye for valuation. Let's say you apply a "SELL" or "TRIM" at 21-22x P/E, then you have an upside/RoR of above 15% per year. Those are some good returns.

The 2022 returns were actually excellent. Revenue above £85.B, operating margin at over 31% with an over-100% cash flow conversion and a less than 2.2x net debt/EBITDA. The company now employs ~35,000 people. It has over 180 countries, and separate listings in three markets - London, Amsterdam, and New York. This is a slow-moving company but with a good upside. Here are the 2022 results.

{kind=link}

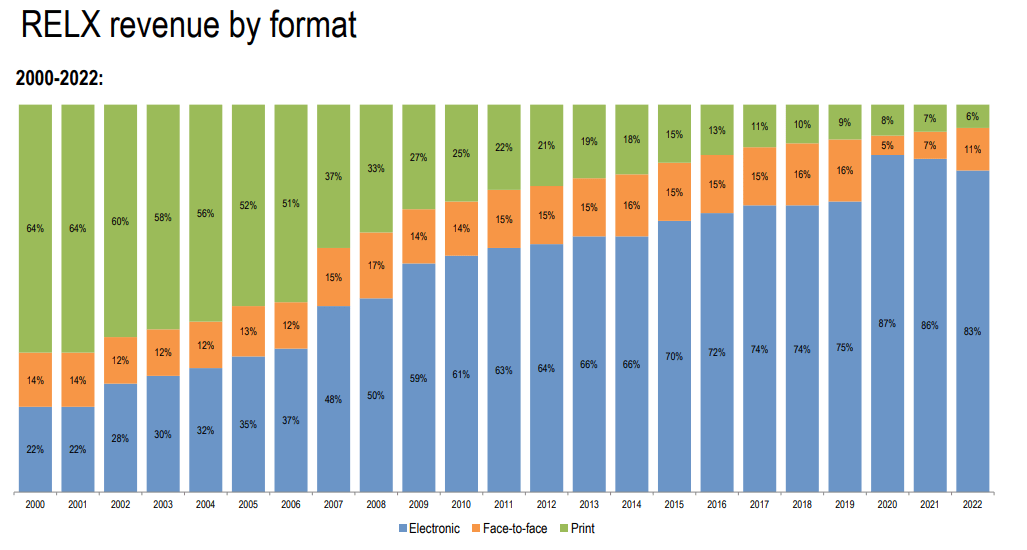

And take a look at the mix development over the past 22 years. That is a massive shift, given that the company has a 100+-year-old history.

{kind=link}

In less than 25 years, the company has gone from being a major print-company, to being fully digital/electronic. The company's objective has stayed roughly similar - but the outcome of this shift is a better growth profile, better margins, and better customer outcomes.

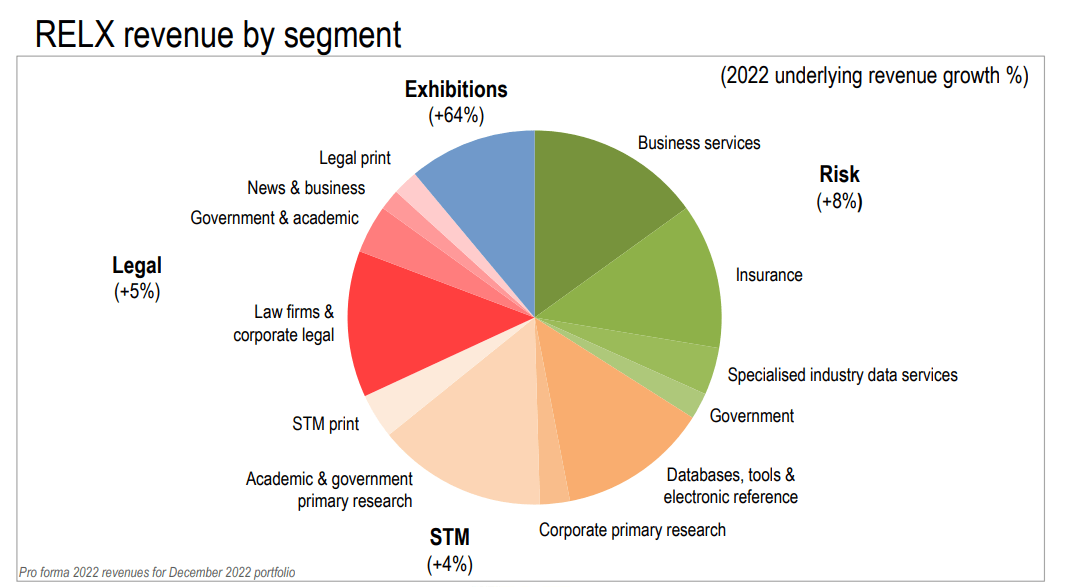

We can also look at a much more granular view in terms of mix, which I personally believe to be a lot more interesting.

{kind=link}

More interesting even than this, is the comparative overall data for the company in the context of its sector. RELX is without a doubt one of the best businesses in the entire segment, known as Business Services. I say this because the company is in the 90th or above in terms of percentile in almost every single profit-related metric. RELX is, in terms of market capitalization, the largest company next to storied names like Thomson Reuters ( TRI ), Cintas ( CTAS ), Wolters Kluwer N.V., Sodexo, Teleperformance, and others. It's an interesting mix, and not every one of these is a perfect match in terms of mix, but it's still relevant in terms of comparison.

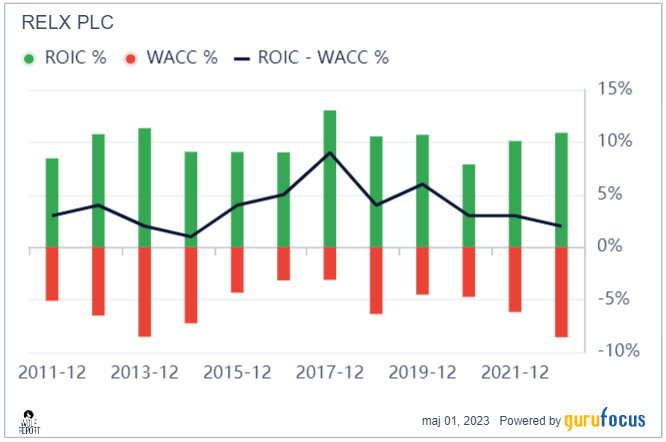

The company isn't above average in terms of yield or debt. Its main arguments are related to an absolutely solid set of fundamentals, and an expanding and already sector-leading operating margin. The company ROIC net of WACC has been positive for the past 10+ years - this company very rarely misses here.

{kind=link}

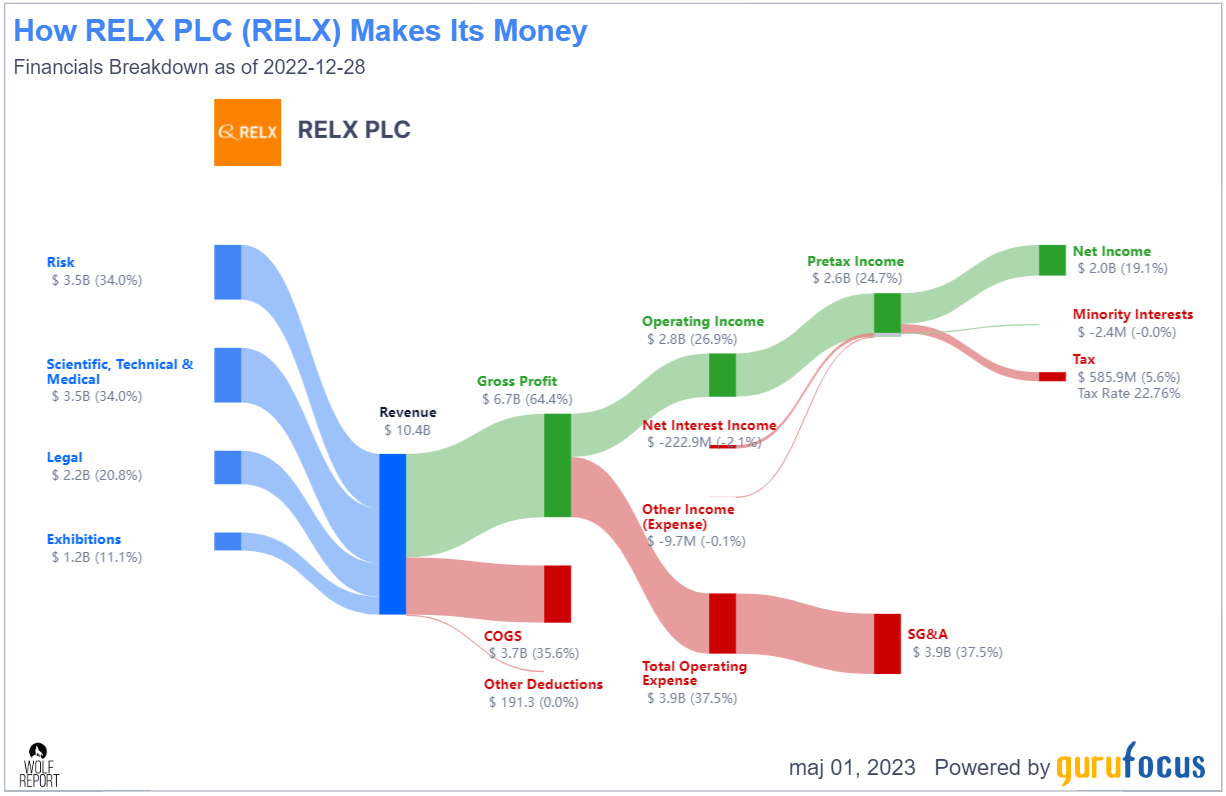

The company has been increasing shareholder equity step by step over the years - and its operational profile and margins have one of the better looks I have ever seen, going from gross to net.

{kind=link}

These sorts of overviews are often underestimated, but they do provide good value. Looking at data like this, you can quickly spot, if you have the relevant sector knowledge, where a company does better and where it does worse than its peers. It goes hand in hand with investing in "quality" companies, as I try to do. I look for sector or industry leaders at good prices - and RELX is an industry leader, to be sure.

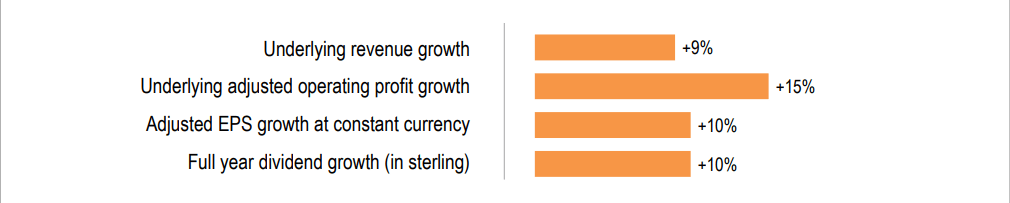

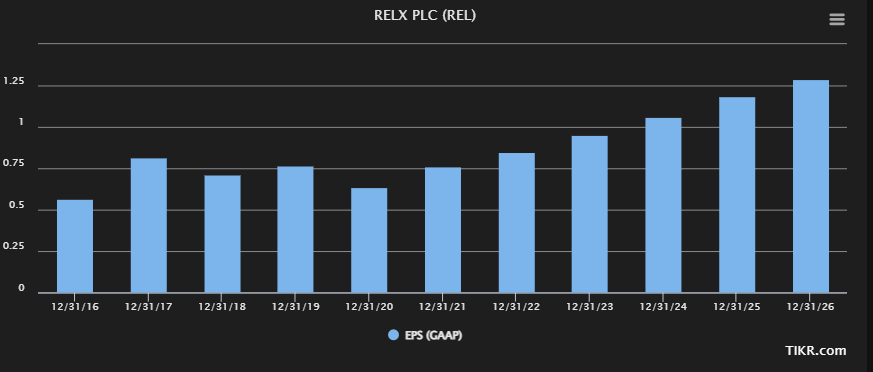

The outlook for this industry leader is actually positive. For 2023, we have a mix of expecting a double-digit EPS increase. I invest in/follow the native share for RELX, trading on the LSE, and I expect a 12.5% growth in company EPS for the year, to around a £0.95/share level for the full 2023E. This is then followed by more growth. Overall, I believe the following trajectory to be realistic.

{kind=link}

Challenges and risks for RELX? Parts of the indicators we want to look at include the number of published articles, to make sure that the company's volumes are intact. For 2022, this was comparable. Because the company operates in part a subscription-based business, renewal figures are crucial - and the customer has a lot of power here. For instance, RELX hasn't pushed any real inflationary price increases for the year, and this might start to be visible in the next few quarters on the margin side. The company considers its services to be value-add and increasing value over time, because the service data sets/content sets improve.

We think of what we sell to our customers as something that is of increasing value to them over time, both because we have broader data sets or the broader content sets, we have increasing and sophisticated analytics and higher-value decision tools, and therefore, we sell on their value and their perceived value.

(Source: RELX earnings call 1Q23)

The main risk I would be looking at in 1Q or forward is margins. If we see any meaningful decline here, then we should be re-evaluating this company's value. For now, that is not the case - margins are stable - and therefore, valuation going into 2Q is going to be similar.

RELX Valuation - And its upside

RELX is a tricky proposition here. In order to expect a market-beating upside from the company at this time, even with my relatively positive expectations going forward, you would have to work with a 24-25x P/E, as much as 26x P/E in some cases. That is exuberant, and a level the company has only reached during a very short time.

We're currently at a P/E of around 26x - so the forward thesis for a "BUY" is based on maintaining that premium. In an environment such as this one, with growing costs and potentially lower margins, I don't put much credence in any type of premium. Not just for this company, but for any company that isn't typically at that type of premium.

And RELX isn't.

RELX is currently valued at PTs of £20-£31 for the native, with an average PT of £27.5/share. That means the 13 analysts following the company believe this, on average, to still be a "BUY" at this time. However, only 4 analysts are at "BUY" - 7 have a mix of "Underperform" and "HOLD" at this time.

If you look at a mix of NAV, book values, FCF potential, and DCF, there's not a massive upside to this company. Most analysts and most methods you typically would look at would rate this company a "HOLD" at this price, or consider it fair-value.

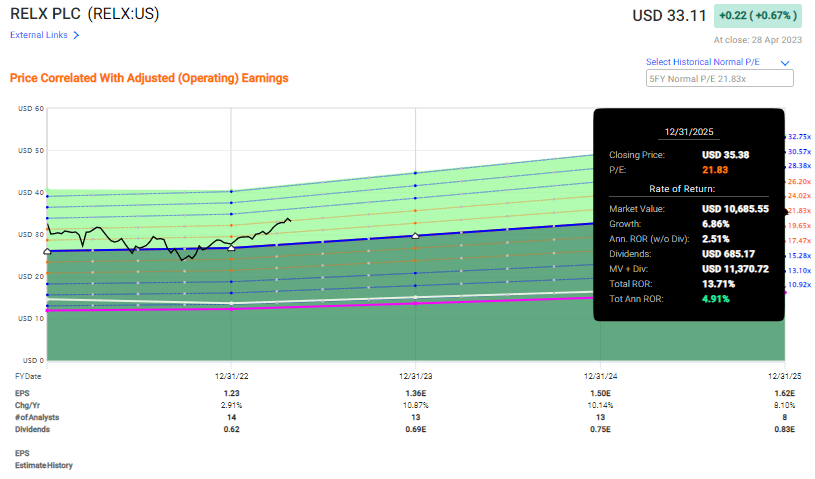

These are the returns if the company maintains a 21.8x P/E premium, which is the level that's been historically accurate on a 5-year basis.

{kind=link}

This is not a scenario or a potential that I invest in. I'm perfectly willing to pay a premium for a great business, and RELX is a great business. But I'm not willing to pay this premium.

My previous share price for an attractive buy for the ADR was $24/share - I'm not shifting from this target at this time. So, as before, RELX is a company I want to own - but not at that price. As of this time, I don't see a reason for shifting my target, making the following thesis relevant going into 2Q23.

Thesis

- RELX is a class-leading company in research and consulting - and it's a convincing investment at a good price. My ambition is to own RELX in my portfolio once the price drops down. I view the company as a relatively simple and stable play on attractive business segments. That is still my ambition, but for the time being, it's less than likely in the near-term.

- If bought at below 20x P/E, and trimmed at above 25-26x P/E, this company has the potential to give you excellent returns over time while paying you a relatively attractive and well-covered dividend of above 2%.

- I would consider RELX a "BUY" at around $24/share for the ADR. The ADR is relatively liquid, meaning you can either go native or buy the RELX US ticker here.

- I'm at a "HOLD" for RELX here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company is excellent but does not fulfill my valuation-based criteria, making it a "HOLD" here.

For further details see:

RELX: Substantially Overvalued, Be Careful