WU - Remitly Global Hits An Air Pocket

2023-12-11 07:48:08 ET

Summary

- Today, we take a look at fast-growing Remitly Global whose shares hit an air pocket following Q3 results.

- Remitly is a Seattle-based provider of cross-border remittance and financial services to immigrants in over 170 countries.

- The company has doubled its market share to 2% in the past two years and is focused on the global migrant opportunity.

- Is the recent pullback a buying opportunity? A full investment analysis follows in the paragraphs below.

All Americans have something lonely about them. I don't know what the reason might be, except maybe that they're all descended from immigrants ."? Ry? Murakami, In the Miso Soup

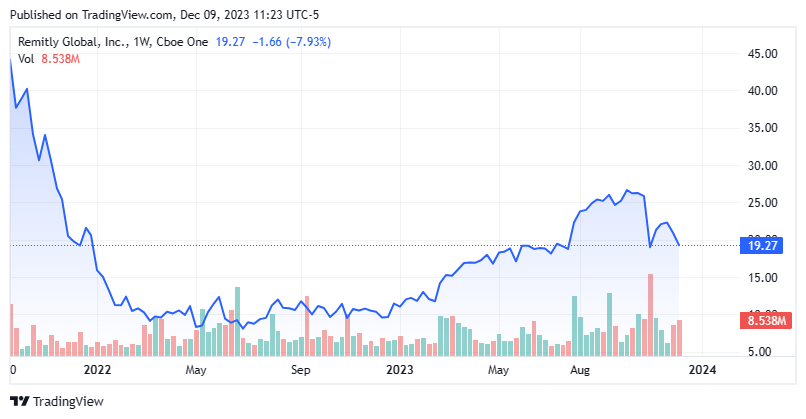

Shares of migrant money transfer concern Remitly Global ( RELY ) cratered 32% after an in-line quarter on November 1st that featured upward revisions to its FY23 Adj. EBITDA and revenue estimates. Profit-taking after a 314% 18-month surge and concerns regarding its plan to increase marketing spend to further drive customer acquisition after growing revenue 43% in 3Q23 were to blame. Having doubled its share of the global money transfer market to 2% in the past two years but still expensive on traditional metrics, the recent insider buying merited further investigation. A full investment analysis follows below.

{kind=link}

Company Overview

August Company Presentation

Remitly Global, Inc. is a Seattle based provider of cross-border remittance and complimentary financial services to immigrants and their families in over 170 countries, 33 of which are remitters - the balance recipients. The company boasted 5.4 million active customers on its platform as of September 30, 2023. Remitly was founded as BeamIt Mobile in 2011, changed to its current moniker in 2012, and went public in 2021, raising net proceeds of $305.2 million at $43 per share. Its stock trades just above $19.00 share, translating to an approximate market cap of $3.6 billion.

August Company Presentation

Business Model

To initiate digital transfers, customers of Remitly simply download its app, permitting the transfer of money in ~4,900 corridors, defined as a unique originating country-receiving country combination. The company's disbursement network encompasses ~4.0 billion bank accounts, ~1.2 billion mobile wallets, and ~460,000 cash pickup locations. Approximately 92% of all transactions are disbursed in less than one hour.

Remitly generates two revenue streams from these transfers. The first is a transaction fee, which is a function of the corridor employed, currency of the funds delivered, choice of 13 funding methods (e.g., ACH, credit card, debit card, etc.), disbursement method (e.g., bank deposit, digital wallet, physical location, etc.), and transfer amount. The second is a foreign exchange spread between Remitly's cost of currency and what it charges its customer. To engender customer acquisition, promotions are employed, which are treated as a reduction in revenue (as opposed to an expense item). The algebra generally works out to revenue equaling 2.4% of total funds transferred (a.k.a. send volume).

Remittances to Mexico, India, and the Philippines accounted for 65% of its total revenue in FY22.

Global Remittance Market

The global money transfer market is significant, estimated at between $19.65 billion and $26.5 billion in 2022 (depending on the research firm's definition) and is expected to grow at a 15%-16% CAGR over the subsequent ten years. In 2022, over $1.6 trillion was transferred by 280 million immigrants (predominantly) to their families. Remitly, with a 2% share of the overall global migrant opportunity, currently estimates its core serviceable market at $626 billion. The market is very fragmented, consisting of other global and regional money transfer providers, digital channels, banks, post offices, and alternative channels (e.g., through DHL). Unlike most of its competitors, such as Western Union ( WU ) with ~9 million digital customers, Remitly is solely focused on the migrant opportunity.

The company attempts to grow market share through new customer acquisition (partly by branding itself as the migrant money transfer company), geographic expansion - which increased through its $77.9 million buyout of Israeli based concern Rewire in January 2023 - frictionless remittances engendering extremely high customer satisfaction (4.9 iOS App Store rating from ~1.2 million reviews), and complementary products. The branding has evolved into a very real network effect, with eight of every ten customers saying that they have recommended Remitly to someone else.

Operating and Share Price Performance

With this focused approach, the company has doubled its market share to the aforementioned 2% over the past two years. This result is reflected in its top line, which grew 78% FY21 vs FY20 and 43% FY22 vs FY21. However, that growth was fueled by a robust marketing and R&D effort. The former rose 64% and 41% (respectively), while the technology spend grew 57% and 116% (respectively). Factor in higher processing and customer support expenses, and it is easy to see why profitability had been elusive, with the company posting negative Adj. EBITDA each year FY20 through FY22 (-$19.9 million, -$10.5 million, and -$13.6 million, respectively). And given the market's aversion to high-growth, unprofitable concerns since shortly after Remitly went public (September 2021), it is easy to see why a hot IPO floundered.

Prior to its IPO, its last round of private funding (July 2020) valued the company at $1.5 billion. After initial IPO valuation talk of ~$5 billion, Remitly was priced at a valuation of $7.1 billion and ran to $8.8 billion on its first day of trading, as all things fintech were en vogue. The corresponding top tick of $53.65 a share proved to be an all-time high, soon plummeting 88% to $6.66 by May 2022, as the market eschewed growth-at-all-cost concerns. That said, Remitly eventually beat its initial FY22 outlook soundly, with Adj. EBITDA of negative $13.6 million on revenue of $653.6 million easily besting its first forecast of negative $35 million on revenue of $610 million. Because of this result and an excellent 1H23 - during which management upwardly revised its FY23 outlook twice, from an initial Adj. EBITDA forecast of negative $5 million on revenue of $870 million to positive $36.5 million on revenue of $920 million - shares of RELY rebounded 314% to a 2023 closing high of $27.59 on November 1st.

3Q23 Financials

However, after that close, the company reported its 3Q23 financials, posting a gain of $0.03 a share (non-GAAP) and positive Adj. EBITDA of $10.5 million on revenue of $241.6 million versus a loss of $0.04 a share (non-GAAP) and Adj. EBITDA of negative $3.7 million on revenue of $169.3 million in 2Q23. The bottom-line matched Street expectations, while the top line was $2.4 million better. The 43% year-over-year surge in revenue was bolstered by a 36% increase in send volume to $10.2 billion and a 42% rise in active customers, representing 1.6 million net adds year-over-year. Certain operating metrics improved considerably year-over-year, such as customer support as a percentage of revenue, which fell 230 basis points to 8.3% and transaction expense, which dropped 580 basis points to 35.5%. The first improvement was attributed to the increasingly frictionless nature of its app, while the second was a function of scale.

Owing to its continued top-line momentum, management raised its Adj. EBITDA and revenue forecasts for a third time to $38.5 million and $939 million (respectively), based on range midpoints. However, the disconnect between the magnitude of increase in FY23E revenue (larger at $19 million) versus Adj. EBITDA (smaller at $2 million) was a function of management making a conscious decision to spend additional dollars on customer acquisition to set up a successful FY24. With a 314% gain over the past year and a half, investors viewed management's move to further press the marketing lever as an opportunity to take profits. That said, the reaction was exceedingly severe, with shares of RELY trading 32% lower in the subsequent trading session to $18.80.

Balance Sheet & Analyst Commentary

It was also surprising in the context of the company's pristine balance sheet, which reflected cash and equivalents of $223.3 million versus debt of only $2.4 million as of the end of the third quarter.

Since Q3 results were posted, four analyst firms including Citigroup and Barclays have reissued Buy ratings on the stock. Price targets proffered range from $25 to $32 a share. BMO Capital initiated the shares as a Market Perform with a $25 price target while Wolfe Research downgraded to Peer Perform this week.

On average, they expect the company to earn $0.15 a share (non-GAAP) on revenue of $940.9 million in FY23, followed by $0.38 a share (non-GAAP) on revenue of $1.20 billion in FY24, representing gains of 153% and 28% (respectively) in the out year.

Board member Nigel Morris also adjudged the selloff an overreaction, using it as an occasion to purchase 250,000 shares at an average price of $19.27 on November 3, 2023. He then purchased another 50,000 shares on November 6th. Other insiders including the company's CTO and CEO have sold approximately $2.7 million worth of shares collectively since November it should be noted.

Verdict

Mr. Morris is likely noticing that Remitly has done an excellent job building a specifically targeted brand while engendering customer trust with an increasingly frictionless app. Although somewhat a function of the global economic backdrop, these transfers are predominantly non-discretionary as migrant workers need to get money back to their families so they can survive. To build on its excellent performance year-to-date in 2023 by spending additional marketing dollars to drive a larger base for future word-of-mouth marketing does not appear to be the sin that the stock market has adjudicated it to be. That said, Remitly is not cheap at over 50 times FY2024E EPS.

Remitly is an excellent company with an outstanding future that deserves well above average multiples. However, even though the 32% one-day correction on November 2, 2023 seems like an overreaction, it likely has further downside, strictly on overly aggressive valuations. Stay to the sidelines for now, but this company is one we will keep an eye on.

The first generation thinks about survival; the ones that follow tell the stories ."? Hua Hsu, Stay True

For further details see:

Remitly Global Hits An Air Pocket