RNR - RenaissanceRe: Benefits From A Light Hurricane Season Are Likely Already In The Price

2023-11-22 19:45:26 ET

Summary

- RenaissanceRe shares have rebounded from Hurricane Ian losses and benefited from rising interest rates, but their true earnings power may be less than 2023 results suggest.

- The company reported strong Q3 earnings, with a stellar combined ratio of 78% and underwriting income of $386 million given the light catastrophe environment.

- The volatility of hurricane risk makes RenaissanceRe's earnings more unpredictable, and investors may be better off in companies with lower hurricane risk at its current valuation.

Shares of RenaissanceRe ( RNR ) have been a solid performer over the past year, rising about 14% as the company has rebounded from last year’s Hurricane Ian losses while also benefitting from rising interest rates. While shares have a less than 7x earnings multiple, I do think this likely overstates RNR’s true run-rate earnings power. Shares may have modest upside, but I believe investors are better off in companies without quite as much hurricane risk, given low multiples in names like Chubb ( CB ) and Arch Capital ( ACGL ).

Seeking Alpha

In the company’s third quarter , RenRe earned $8.33, beating consensus by $2.21, and rebounding strongly from last year’s $9.27 operating loss. The company reported a stellar combined ratio of 78%--this means that for every $1 in insurance premiums it wrote, it earned $0.22 in underwriting profits. RNR is a reinsurer, and it takes on meaningful catastrophe risk, which can make third quarter earnings, in particular, quite volatile. In Q3 2023, there were less than 6 points of catastrophe losses, significantly boosting earnings. As such, underwriting income of $386 million was up from a $683 million loss last year.

This normal volatility is because Q3 is the peak of the US hurricane season. Some types of insurance provide fairly steady losses while others are very “lumpy.” For instance, health insurance is perhaps the steadiest. Tens of millions are covered; there is always a share of the population getting ill, but there is never a year where everyone gets cancer or where no one does. Conversely, the number of hurricanes, and where they hit, is much more random. That makes RNR’s earnings far more volatile on a year by year basis, and it is a reason why the market is structurally likely to pay a lower multiple on those earnings.

This volatility showed itself in the property segment of RNR’s business. Property net premiums declined by $252 million, driven by a $208 million decline in reinstatement premiums. When certain catastrophes meet pre-determined benchmarks, policies can be brought back into force, increasing a reinsurer’s premiums and exposures. Given a lighter hurricane season, premiums returned to a more normal level. The impact was most notable in RNR’s underwriting profits as the combined ratio was just 53% from 186%, as large loss events were just 14.5%.

This quarter, RNR suffered just $78 million in catastrophe property losses, $57 million of which were from the Hawaii wildfires and Hurricane Idalia. By contrast, last year, Hurricane Ian caused $540 million in losses. This variance speaks to the natural volatility of the company’s business. Typically, I expect to see RNR’s combined ratio look worst in Q3 because it collects premiums all year but typically only sees hurricane losses in one quarter. Instead, the company’s 78% total combined ratio is below the full year’s 78.8% level.

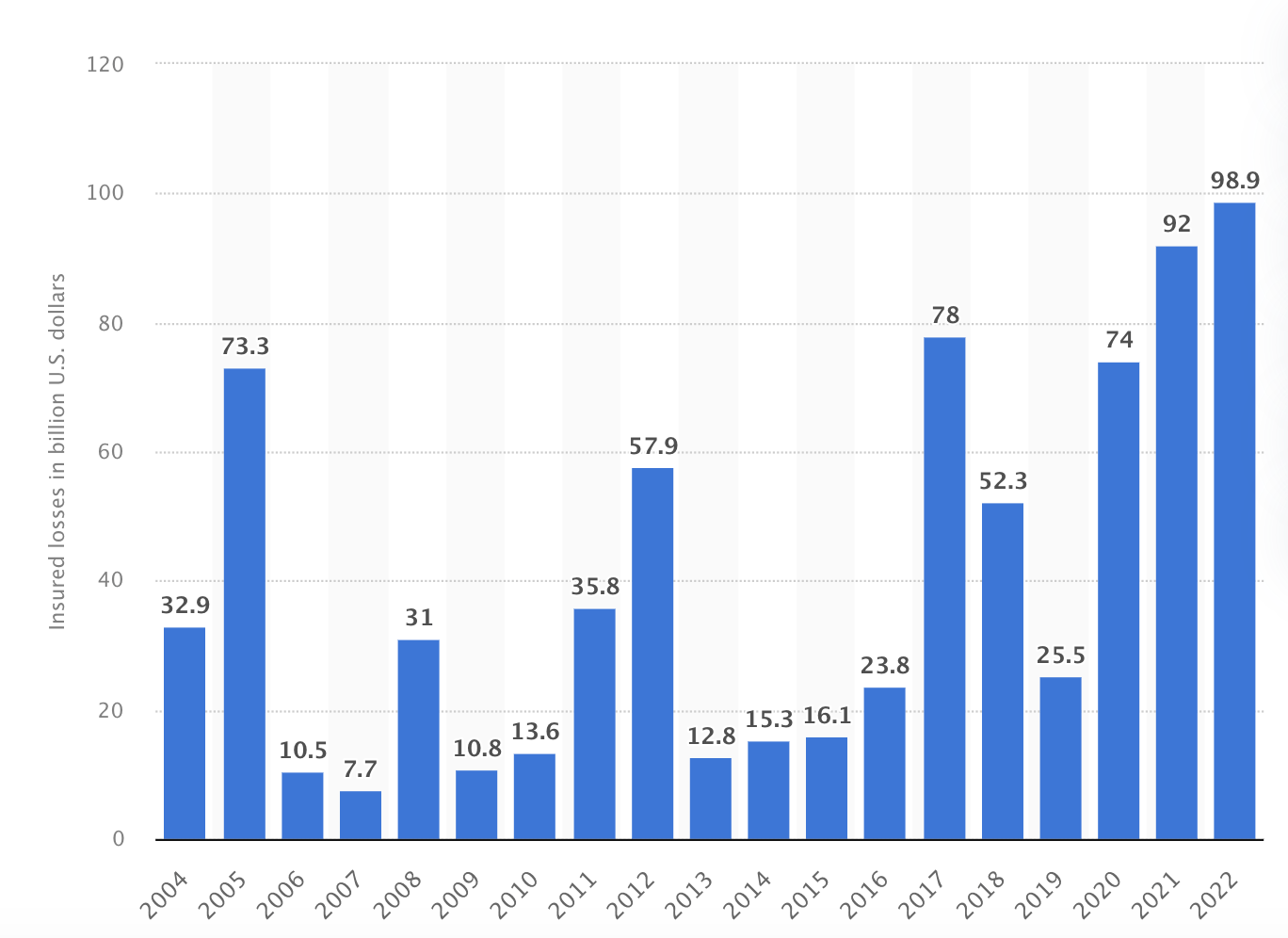

Now, on the conference call, management noted that industry cat losses were nearly $20 billion , which exceeds the 10 year median. This would argue that the 2023 level of cat losses is a reasonable base case and that 2022 was the outlier. I find this view to be somewhat over-optimistic. As you can see below, the statement is true in that the median year for catastrophe losses is about $20 billion. However, when it is above $20 billion, it tends to be substantially higher.

{kind=link}

As such, the average year has a much higher pay out than the median year, at about $50 billion, or 2.5x the median, given the skew in how much damage a large storm can cause. Additionally, given inflation, construction costs have been rising, meaning a storm that caused $10 billion in 2014 damage would cause ~$13-15 billion today. In the past few years prior to 2023, losses also seemed to be trending higher. Now, perhaps this is an aberration; climate and weather are difficult to predict. Still, given climate change, investors should be at least cognizant to the potential that hurricanes will be more problematic over the next 10-20 years than they have been the past 10-20 years.

To be clear, I am not arguing that investors should assume a large-loss making storm like Ian occurs every year. It seems likely that was a uniquely painful event. I would argue that assuming a ~$20 billion loss rate is likely to be lighter than the average the insurance industry will experience. I roughly assume the average will be halfway between the two years, or about $300 million in losses. That would be about a $4 per share headwind relative to reported results. When valuing RNR and determining an appropriate valuation, I believe it best to use a normalized earnings run-rate, rather than having an EPS distorted by how severe one year’s weather is.

Outside of property, casualty and specialty net premiums were down by 13% to $976 million. Here, the combined ratio rose to 97% from 95.7% slightly disappointing. Increased loss in energy and marine drove the deterioration; these categories can be volatile on a year-by-year basis. Premiums fell largely due to a large multiyear mortgage transaction last year; these policies are lumpy, not annual activities, which can distort year over year premium growth.

Aside from underwriting activity, RNR is benefitting significantly from the increase in interest rates. Net investment income more than doubled to $329 million with a return of 5.7% from 3.2% last year. Renaissance has a $26 billion investment portfolio; $22.6 billion of it is in fixed and short-term assets with $3.3 billion of other investments. The fixed income portfolio has a 6.3% average yield to maturity, up from 5.7% at year end with a 2.1 year duration. Excluding cash, the portfolio has a 2.6 year duration from 3.2 years at year end.

Given its short duration, RNR has been able to reinvest much of this portfolio already into higher-yielding securities in today’s right environment. Still, there is likely to be modest further tailwinds over the next 3-4 quarters from reinvestments, by which point the investment tailwind will be complete, absent further increases in the Fed funds rate. Right now, the market is pricing in four rate cuts next year, so given its short duration, by the end of 2024, or more likely in 2025, investment yields could begin to decline.

For the year so far, earnings are $25.32 from -$0.16 in 2022 as the combined ratio of 78.8% has fallen from 103.3% last year. Assuming a similar underwriting environment in Q4, RNR should earn about $33 this year, for just a 6.1x P/E. Now, as noted above, RNR has, in my view, over-earned by about $4 from the light catastrophe season, bringing run-rate earnings to $29. RNR also enjoyed a 9% benefit to its combined ratio from “favorable developments” on prior reserves, meaning its losses were not as high as previously estimated. This is a positive item, but not a recurring one. Excluding this, RNR is set to earn about $25-26 on a run-rate basis, giving shares an 8x multiple.

This is still cheap, but not quite as cheap as 6x, with other insurance like Chubb around 10x but with less volatile earnings, or ACGL , which has some catastrophe exposure but a bit more business diversification.

Now subsequent to quarter end, RNR completed its acquisition of Validus Re. Validus deepens the ties with AIG and provides $4.8 billion of investment assets. RNR paid a $900 million premium or about 40% to book equity.

RNR has a $134 book value, so at the same premium it just paid for a reinsurer, its shares would be worth $187. A major rationale for the deal, as reiterated on the last conference call, is that RNR can reduce the capital intensity of Validus by 30%, given its integration onto the larger platform. Giving a full credit for being able to do 30% more earnings on the capital basis would get shares to $243 value. That is an ambitious target, and it does bear reminding that Validus holders were happy to sell at that price, given those assumptions.

M&A also usually occurs at a premium to stand-alone value, and so public markets are unlikely to provide the same valuation, especially given the uncertainty around execution. I believe it to be prudent to assume a 10% discount to M&A-implied prices, or about $219 in fair value for RNR. Incremental income from the new acquired operations should boost run-rate earnings to about $28, so at $219, shares have a just-under 8x multiple.

Considering the volatility in RNR’s earnings, that valuation strikes me as fair, providing about 7% upside from the current share price. As such, I do not believe investors need to rush out and sell RNR. With limited upside and volatile earnings though, I would use its rally this year to rotate out of RNR. I prefer to invest in name like this if shares sell-off following a bad hurricane season if investors panic about losses. But when results are this pristine, there is likely to be more downside than upside risk to results, and there are better alternative for investors now.

For further details see:

RenaissanceRe: Benefits From A Light Hurricane Season Are Likely Already In The Price