MMTOF - Renault: Significant Upside From Spin-Off And Improving Financials

2023-06-18 23:15:15 ET

Summary

- Renault's transition to electric vehicles is going well, with investments in autonomous vehicles and the Mobilize brand offering future growth opportunities.

- The company is trading at a discount to its historical average multiple, with further upside potential due to its ownership of Nissan and the spin off of its EV business.

- Margins trail its peers but we are seeing gradual improvement. Further, deliveries are strong on April 23, despite weaker economic conditions.

Investment thesis

Our current investment thesis is:

- Renault is a strong business that is transitioning to an EV fleet well. Vehicle deliveries are impressive in spite of weaker economic conditions, margins are improving, and revenue growth looks to be returning.

- Investments in autonomous vehicles and its Mobilize brand represent opportunities for future growth.

- Renault is trading at a discount to its historical average multiple, implying upside given the strong commercial position.

- Further upside comes when factoring in the company's P/TBV is 0.4x, in large part due to its ownership of Nissan. Further, the company is looking to spin off its EV business for a rumored valuation of exactly Renault's market cap.

Company description

Renault SA ( OTCPK:RNSDF ) is a global automotive company.

The company operates in three segments:

- Automotive segment focuses on producing, selling, and distributing passenger cars and light commercial vehicles. They also invest in automotive associates and joint ventures, primarily Nissan.

- Sale Financing segment offers financing, leasing, and service contracts under the Mobilize Financial Services brand.

- Mobility Services segment provides mobility and energy solutions for electric vehicle users under the Mobilize brand.

Renault is known for its passenger cars and light commercial vehicles sold under the Renault, Dacia, Alpine, and Mobilize brands.

Share price

Renault's share price has underperformed in the last decade, losing c.50% of its value during this time. This reflects a once-in-a-lifetime change to the automotive industry, which Renault is on the back foot responding to.

Financial analysis

{kind=link}

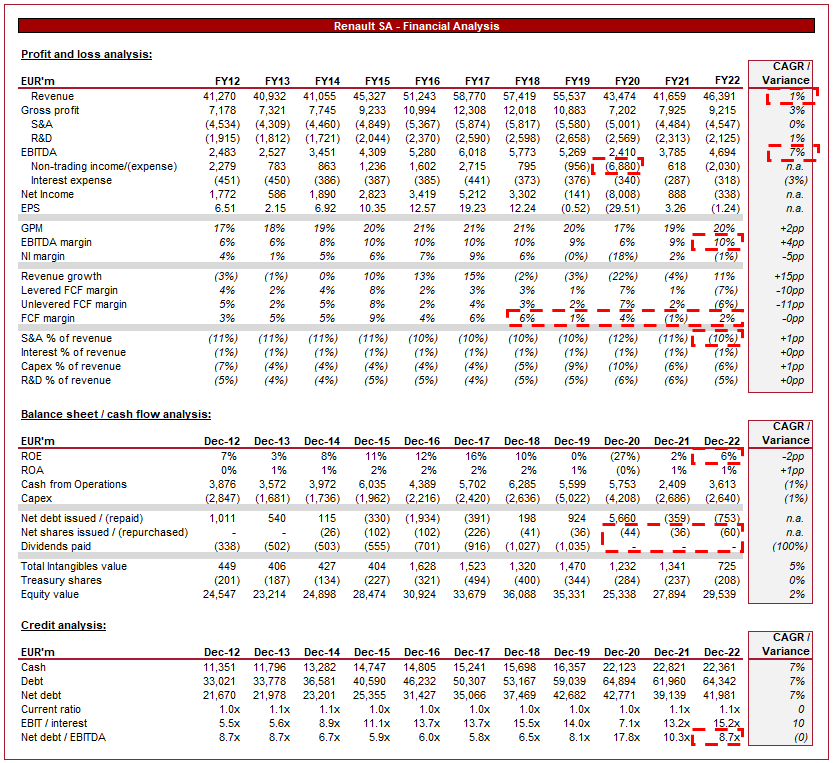

Presented above is Renault's financial performance for the last decade.

Revenue & Commercial Factors

Renault's revenue has grown at a CAGR of 1% across the last 10 years, reflecting a period of soft performance. The company had been on a positive growth trajectory, but the impact of Covid-19 looks to have derailed this. In line with many automotive businesses, Renault has yet to return to its pre-Covid level levels.

Business model

Similarly to its European Automotive peers, Renault operates across the price spectrum within the industry. Dacia is a strong brand in the affordable segment, Renault operates in the highly contested mid-range market, and Alpine is the luxury offering.

Renault has a strong history in the world of sports car racing, most recently in Formula 1, having won numerous championships in partnership with Red Bull as their Engine manufacturer, and now under the Alpine brand as a works manufacturer (dedicated team). Further, the Alpine intends to enter WEC in the Hypercar division, seeking to win Le Man. Racing represents a key marketing exercise for Renault that we believe is financially justified (F1 especially is incredibly expensive), although we are unsure about the switch to Alpine branding (Which we will explore later).

Automotive industry

The transition toward electric vehicles is the most significant factor impacting the automotive industry. Renault has embraced this shift by investing in EV technology and expanding its electric vehicle lineup. This involves the launch of new models such as the Austral, as well as the creation of electric variants such as the Clio hybrid. Our view is that the traditional automakers have been on the back foot, primarily as they have a core market to service (Traditional ICE vehicles), while also investing in EV development. This is compared to the EV specialists who are happily loss-making as they invest heavily in development. Our view is that Renault has done well in this transition, with the Dacia Spring, Renault Zoe, Renault Twingo E-Tech, and Renault Megane selling particularly well in Europe currently. Further, the pipeline looks extremely positive, with Renault, Nissan ( OTCPK:NSANY ), and Mitsubishi ( OTCPK:MMTOF ) jointly announcing they would spend c.$23bn on development, creating 30 new EVs. The 3 businesses are currently in an alliance (Masterminded in part by the infamous former CEO Carlos Ghosn), which involves a c.43% ownership of Nissan by Renault.

The EV transition is complicated by the fact Renault currently intends to spin the business off, creating " Ampere ". This business is touted to list in Paris later this year, with Nissan purchasing a portion of the business, thus protecting the alliance (and the IP concerns that come with it), while Renault will retain ownership. The valuation sought is rumored to be €10bn. This would create a Polestar / Volvo ( OTCPK:VLVLY ) situation where the two businesses operate partially independently. We will explore the valuation consideration of this later.

Autonomous driving technology is a development that is occurring in conjunction with the EV transition. Renault is actively investing in research and development to enhance its autonomous driving capabilities. There has yet to be a clear winner in this space and represents the natural progression post-adoption of EVs. Renault's development looks to be positive, with its SYMBIOZ concept car looking impressive .

Renault's Mobilize brand is an interesting foray into what the future could be. Renault is banking on two particular trends causing a significant increase in demand for the products it is developing. Firstly, with the growth of urban areas and the concept of smart cities, Renault is exploring mobility solutions tailored to urban environments, including compact electric vehicles, shared mobility services, and infrastructure integration to support sustainable urban transportation. This is essentially a risk that continued population growth in conjunction with migration toward big cities will render traditional vehicles obsolete. Secondly (and less dramatically), there is increasing interest in autonomous delivery and logistics solutions. This would allow businesses to significantly reduce costs, increase efficiency and reduce constraints that come with human operations (working hours, sleep, etc). Renault is developing autonomous delivery vehicles and collaborating with logistics companies to streamline last-mile delivery operations. How influential the Mobilize business will become is yet to be seen but we are impressed by the development thus far and the use case is clear. The importance (as with all things) is whether this will be commercially viable and supported by legislation.

Our only concern with Renault in terms of industry positioning is its Alpine brand. It just does not stand up well against other vehicles in its price bracket. The cars are very niche and there is almost no mainstream interest in the brand. The sportscar brand strategy makes sense from this perspective, as Renault is attempting to improve interest. Renault head De Meo stated he would like to create a " mini-Ferrari ". The issue is that Alpines look and drive like Alpines, not Ferraris; they are just not interesting enough.

Economic & External Consideration

Current economic conditions represent a near-term risk to the business. With heightened inflation and elevated rates, consumers are experiencing a deterioration in finances. This discourages large purchases. Deliveries remain strong, with the YoY volumes up 22.3% worldwide despite these concerns. This reflects impressive resilience and a strong trajectory for FY23 results.

Looking ahead, we expect rates to remain elevated, and thus economic conditions to be soft, for several more quarters. Inflation is declining but has shown a clear stubbornness.

Margins

Renault's margins have progressively improved across the historical period, with GPM increasing from 17% to 20% and EBITDA-M increasing from 6% to 10%.

Margin improvement is driven by scale benefits, shared competencies with the alliance, a change in product mix, and cost benefits from improved automation. Our view is that further improvement is possible in the coming years.

Renault's non-trading income has a habit of distorting NI, partially due to its various investment holdings, causing unrealized gains and losses.

Balance sheet

Renault's ND/EBITDA ratio is 8.7x, which is slightly deceiving given that this is primarily facilities costs. The company has sufficient interest coverage and a debt rating of BB from S&P .

Distributions have been mild in the last few years, as reduced revenue has forced the business to commit a greater portion of cash flows to Capex. This is the correct decision in our view and suspect full dividends will not be immediately returned.

Cash flows have generally been consistent with no real volatility, which has allowed for consistent capex investment alongside distributions.

Industry analysis

Industry (Seeking Alpha)

Presented above is a comparison of Renault's profitability to the average of its industry, as defined by Seeking Alpha ( 31 companies , of which the bottom 12 have been excluded due to outlier results ).

Renault performs poorly when considering profitability, with the business marginally below average on every metric. The key metrics to consider are EBIT(DA)-M and LFCF-M, all of which Renault is slightly below. This is a reflection of Renault's product weighting toward the affordable segment, where it operates with tighter margins. Improvement in Alpine and further scale benefits has the potential to improve margins, but for now, we consider this disappointing.

Valuation

Renault's valuation is a mess. The company is trading at an EV of c.€10bn, while its stake in Nissan alone is worth €5.9bn, it is rumored to be seeking a €10bn valuation for its EV division, and it has an equity value of €29.5bn.

This implies markets are extremely negative about the business. To an extent, this is understandable, as the company is less profitable than its peers and there is uncertainty around growth. This said, these factors do not imply such a deep discount. The EV transition is going relatively well, the alliance remains intact despite various issues, the Ampere spin-off will unlock value short term, and margins have been improving.

Valuation (Seeking Alpha)

Renault is currently trading at 11.2x LTM EV/EBITDA and 8.2x NTM EV/EBITDA. Both valuations are a discount to the company's historical average, implying an 11.5-25.7% upside.

Based on the factors stated above, we believe Renault's overall trajectory is positive and the company can at least boast parity with its "average" position in the last decade.

When considering the fundamentals, alongside the potential to unlock value from Ampere, Renault looks undervalued.

Key risks with our thesis

The risks to our current thesis are:

- The listing of Ampere. The current bear market is not favorable for an IPO, especially at the size that's being touted. Further, European markets have performed poorly relative to the US in the last decade (as reflected by Renault's valuation). The two factors in culmination could lead to a below-expected valuation, or even worse, a delay.

- Although far less material, poor development from Alpine could cause Management to cancel the F1/WEC projects altogether in order to cut costs.

Final thoughts

Renault is an attractive business in a highly competitive industry. Renault was achieving good growth prior to Covid-19 and margins are improving. The EV transition looks to be going well and investment in other areas represents opportunities for future growth.

Importantly, the stock looks mispricing. Its ownership of Nissan and the upcoming listing of Ampere represents a strong value proposition for near-term price action.

For further details see:

Renault: Significant Upside From Spin-Off And Improving Financials