RENT - Rent the Runway: Still Not A Great Play

Summary

- Rent the Runway continues to post strong sales growth, thanks to a rise in the number of subscribers year-over-year.

- Bottom line results are also improving, but they are far away from where they need to be.

- For now, I believe there are better prospects to be had, but the firm could eventually grow into its valuation.

Buying into speculative investments is a double-edged sword. On the one hand, they do offer significant upside potential. But on the other hand, they can also result in material downside, even in the event that they continue to grow. One example of a speculative play moving much more wildly than I anticipated involves a firm called Rent the Runway ( RENT ). At its core, the company operates as a shared designer closet that permits its customers to gain access to thousands of fashion styles spread across hundreds of different brands. Customers are able to use the online platform that the company set up to pick out clothing and have it mailed to them, either to wear temporarily or to acquire permanently. Recently, top line growth achieved by the company has been impressive. Its bottom line results have also been improving nicely. Unfortunately, none of this has stopped the company from experiencing significant downside. But that's the way that it goes sometimes with speculative firms. Although the company is looking better from a fundamental perspective and the drop in price may offer a buying opportunity, I do still think that this is a rather risky prospect that investors should weigh carefully before trying on for their own portfolios.

A divergence

In April of 2022, I wrote an article discussing the investment worthiness of Rent the Runway. In that article, I found myself impressed by the unique business model that the company functioned from. Over the years, the firm had succeeded in accumulating a large user base, but top and bottom line performance had been rather mixed. This was further complicated by the COVID-19 pandemic. But even without that factored in, the firm was a rather speculative play that could offer significant upside or downside moving forward. The bottom line troubles that the company exhibited caused me to take a more cautious approach to evaluating the firm. And as such, I ended up rating it a 'hold'. Since then, the firm has demonstrated just how volatile it can be. While the S&P 500 is down 9.6% since the publication of the article, shares of Rent the Runway have seen downside of 34.9%.

{kind=link}

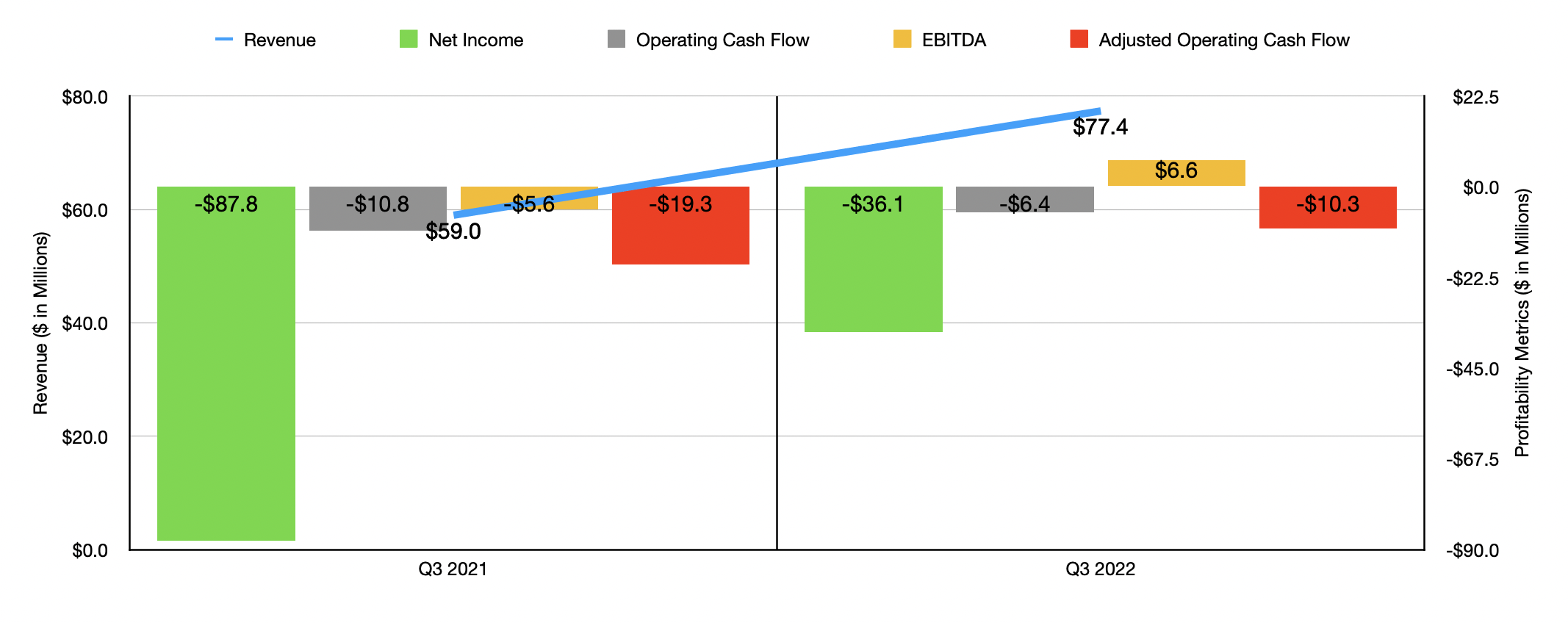

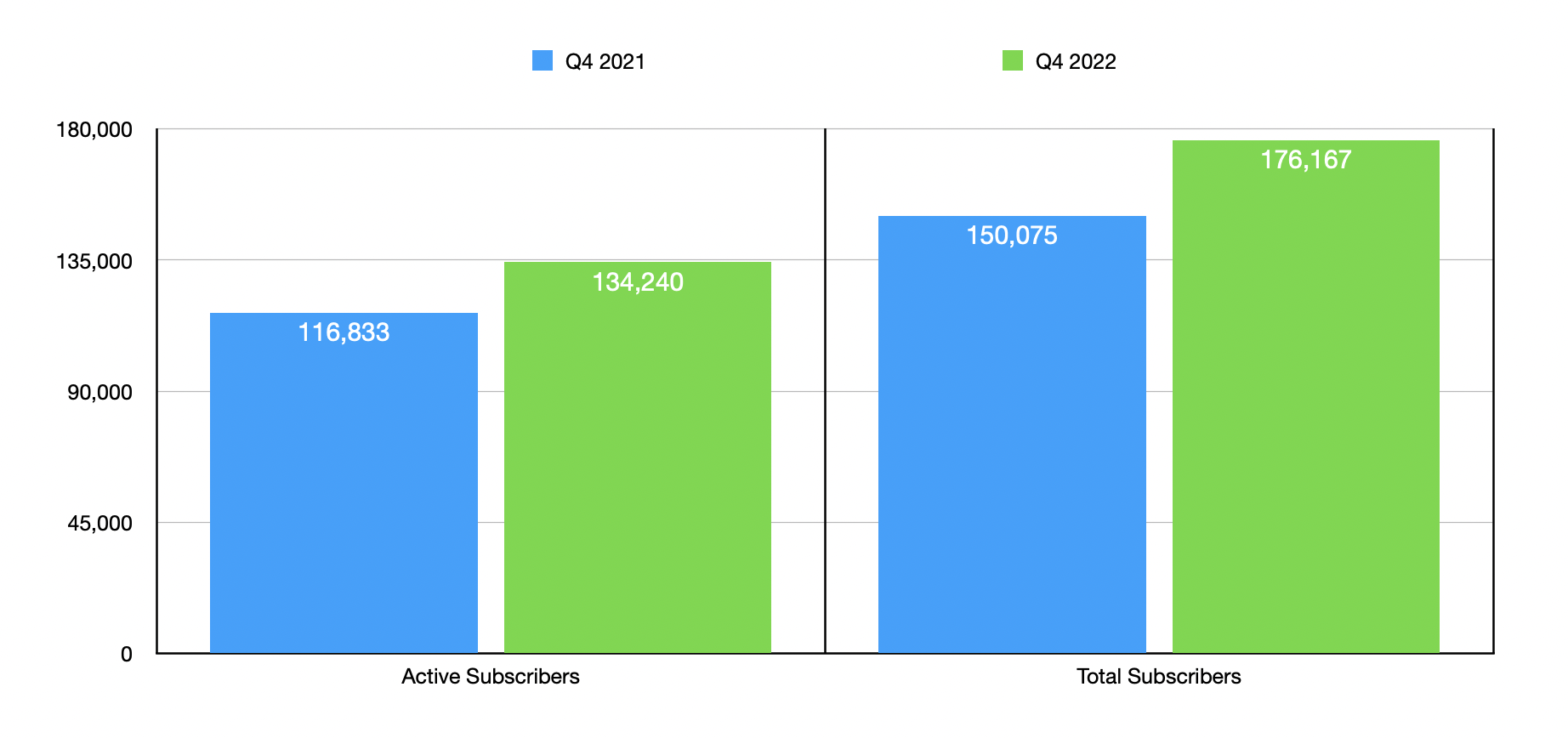

This massive drop came about even at a time when fundamental performance for the business showed signs of improvement. To see what I mean, we should first touch on how the business performed for the third quarter of its 2022 fiscal year. Sales for that time came in at $77.4 million. That represents an increase of 31.2% over the $59 million the company generated only one year earlier. This increase, management said, was driven in large part by a surge in the number of active subscribers on its platform. This number jumped from 116,833 at the end of the third quarter of 2021 to 134,240 by the end of the third quarter of 2022. The total subscriber base for the company, over the same window of time, expanded from 150,075 to 176,167. This is great to see, but it's also important to note that the number of active subscribers only just passed the number that the company reported for the end of the 2019 fiscal year. That came out to 133,572. But because of the COVID-19 pandemic, the number of active subscribers had temporarily plunged, ending the 2020 fiscal year, for instance, at 54,797. It is nice to see such a significant recovery. But it's also important to understand that the extreme variation it saw during that time is indicative of a business model that is inherently unstable.

Recent revenue for the company brought with it a significant improvement in the company's bottom line. The firm went from generating a net loss of $87.8 million in the third quarter of 2021 to generating a loss of only $36.1 million the same time of the 2022 fiscal year. Operating cash flow went from negative $10.8 million to negative $6.4 million. If we adjust for changes in working capital, it still would have improved from negative $19.3 million to negative $10.3 million. And finally, EBITDA for the business went from negative $5.6 million to positive $6.6 million.

{kind=link}

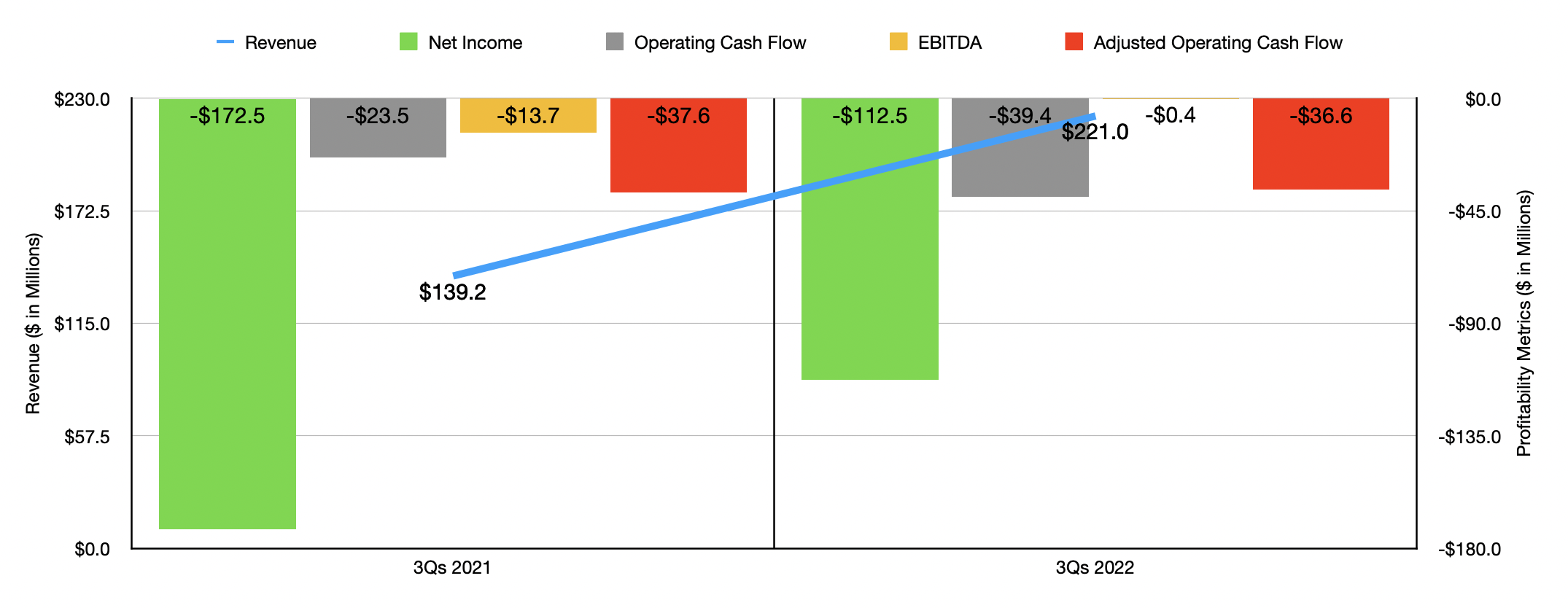

The results seen in the third quarter of 2022 are very similar to what the results were for the first nine months of that year relative to the same nine months one year earlier. Revenue of $221 million beat out the $139.2 million reported for the first nine months of 2021. The firm's net loss went from negative $172.5 million to negative $112.5 million. Operating cash flow actually worsened, going from negative $23.5 million to negative $39.4 million. But if we adjust for changes in working capital, it would have improved modestly from negative $37.6 million to negative $36.6 million. And finally, EBITDA improved from negative $13.7 million to negative $0.4 million.

When it comes to the 2022 fiscal year in its entirety, management said for investors to expect revenue of between $293 million and $295 million. This would be the greatest revenue in the company's history. However, profits are still going to be a problem. After all, the company said that its EBITDA margin for the year will be around 1%. At the midpoint, that would translate to a reading of $2.9 million. If EBITDA is barely turning positive, that means that operating cash flow and certainly net profits will be in the red.

Clearly, Rent the Runway does have some issues. Although the company is growing nicely, and its bottom line results are showing signs of improvement, it does have a lot of work to do if it's to be a viable operation in the long run. One really great thing about this is that management acknowledges the challenges they face. That's why, on January 31st of this year, the firm announced some corporate debt restructuring. In addition to extending the maturity date of its credit facility from October of 2024 to October of 2026, it also rearranged how interest is paid. The current interest rate on its debt is 12%. 7% is paid out in the form of cash, with 5% paid out with in-kind debt. Instead of this, from now through the end of July of 2024, the amount that will be paid out in the form of cash will be reduced to 2%.

After that, it will eventually be increased to 5% per annum. The rest up to the 12% limit will be paid in kind. In the short run, this is a positive because, according to management, the change will allow the company to save around $20 million in interest payments over a two-year window. But the increase in in-kind payments will set up the company for higher interest expense in the future. In addition, effective January 2024, the interest rate will rise 1% per year thereafter. In order to get this deal, the company had to also issue warrants giving the debt holders the right to buy up to 2 million shares of stock at $5 per share. Given that shares are currently under that limit, this could bring in some capital for the firm. But in the event that shares rise materially, it could mean costly dilution for investors.

{kind=link}

Truth be told, you can't really value a company that's generating negative cash flows and profits. At least you can't value one like this. But what you can do is see what kind of cash flow would be necessary in order for the company to be at least fairly valued. In the table below, you can see three different scenarios. The first calculates what kind of operating cash flow and EBITDA the company would need to generate each year to be fairly valued if it is to trade at a price to operating cash flow multiple or an EV to EBITDA multiple of 10. The second uses a multiple of 20, while the third uses a multiple of 30. It's difficult to imagine shares justifying evaluation near the high end of that range unless bottom line results improved drastically and growth continues as it has been. Having said that, using data from the 2022 fiscal year, we would need an EBITDA margin for the company of only 3.8%. For the fourth quarter of 2022 as a whole, management expected an EBITDA margin of between 4% and 5%. With the multiple at 20, the required margin would be about 5.7%. So it's not unrealistic that the company could grow into its valuation, especially if revenue growth continues.

{kind=link}

Takeaway

Conceptually, I like the business model that Rent the Runway has. I think it is an interesting firm that does have long-term potential. I like the revenue growth and user growth data that we have seen recently, though it's unclear how long it will continue to expand at a rapid pace. The fact that the number of subscribers has varied significantly from year to year during the pandemic era is indicative of a company that many of its users can live without. So that on its own is a negative. But, especially when factoring in the debt restructuring the company announced, it's not unthinkable that the firm could grow into its valuation. All of this creates a rather risky and volatile situation that makes me hesitant to rate the company either bullishly or bearishly. As such, my only recourse is to assign RENT stock a 'hold' rating with the caveat that it's still very much a speculative prospect.

For further details see:

Rent the Runway: Still Not A Great Play