RPTX - Repare Therapeutics: A Compelling Bet On Synthetic Lethality

2023-10-03 09:00:00 ET

Summary

- Repare Therapeutics shows clinical and financial strength, with diverse cancer therapies and a robust balance sheet.

- Despite promising Q2 results, elevated put activity and 7.32% short interest warrant investor caution.

- "Buy" recommendation based on strong clinical pipeline and financial footing; monitor clinical milestones and spending closely.

At a Glance

Repare Therapeutics ( RPTX ) stands at an intriguing intersection of clinical innovation and financial viability. The company’s fiscal prudence, as evidenced by a strong balance sheet, offers a counterbalance to the inherent risks in oncology-focused R&D. With milestone payments from its Roche ( RHHBY ) collaboration serving as a financial backstop, the firm appears well-capitalized for its near-term objectives. Market sentiment, however, shows a mixed bag; elevated put activity and 7.32% short interest require vigilance. The performance of lead assets like camonsertib and their influence on milestone payments will be pivotal in the near term. Therefore, understanding the subtleties in both clinical progress and financial metrics is paramount for investors assessing Repare’s long-term outlook.

Q2 Earnings

To begin my analysis, looking at Repare Therapeutics' most recent earnings report for Q2 2023, there are notable improvements. Revenue from collaboration agreements surged to $30.2M from a mere $0.679M in Q2 2022, representing a staggering YoY increase. However, R&D and G&A expenses have also crept up, at $33.8M and $8.7M respectively, contributing to a net loss of $11.9M. The net loss per share has improved to $-0.28 from $-0.91 YoY. Share dilution is minimal, with weighted-average common shares outstanding increasing only marginally to 42.1M from 41.9M.

Financial Health

Turning to Repare Therapeutics' balance sheet , as of June 30, 2023, the company has $115.5M in 'Cash and cash equivalents' and $165.1M in 'Marketable securities,' resulting in a total liquid asset pool of $280.6M. Total current liabilities stand at $53.3M, yielding a current ratio of 5.3. Over the past six months, the net cash used in operating activities was $66.1M, indicating a monthly cash burn rate of approximately $11M. Dividing the total liquid assets of $280.6M by the monthly cash burn gives a cash runway of about 25 months. It's crucial to understand that these numbers are historical and may not be indicative of future performance.

Given the strong current ratio and a substantial cash runway, the likelihood of Repare seeking additional equity financing in the near-term appears low. Nonetheless, these are my personal observations, and other analysts might interpret the data differently. An unforeseen ramp-up in R&D or operational expenses could still necessitate capital raising, but based on current financials, the company appears well-capitalized for the next two years.

Equity Analysis

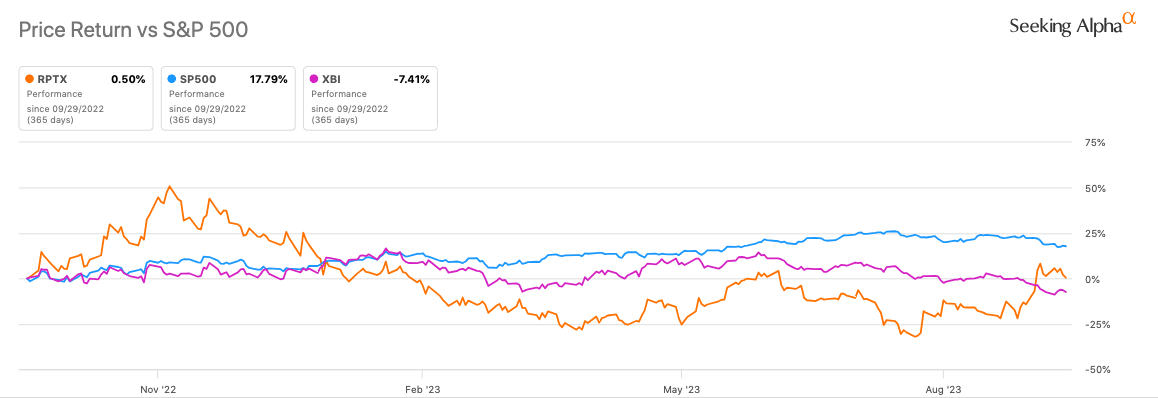

According to Seeking Alpha data, Repare Therapeutics has a $508.5M market cap, suggesting moderate market confidence given its promising Q2 earnings and clinical progress. Analysts project FY 2023 revenues of $62.77M, reflecting significant growth prospects. In momentum, RPTX has outperformed SPY in 3M and 6M timeframes but lags on a 1Y basis. The 24-month beta of 0.89 indicates less volatility than the broader market.

{kind=link}

Options data show elevated put activity, signaling market expectation of increased volatility and bearish sentiment. Short interest is 7.32%, indicating some skepticism but not alarmingly high. Significant ownership lies with PE/VC firms (33.11%) and hedge fund managers (25.47%), implying strategic and financial acumen backing the company. Institutional holdings slightly favor increased positions over decreased ones. Insider trading trends show net selling over 12 months, but zero activity in the last 3 months.

Repare's Double-Barrel Attack on Cancer

Repare Therapeutics' Q2 updates reveal a nuanced, multi-pronged approach to targeted cancer therapy. Leading the portfolio is camonsertib, a unique ATR inhibitor, whose mechanism disrupts DNA damage repair in tumors with specific genomic alterations. Importantly, its pairing with PARP inhibitors showed a remarkable increase in clinical benefit rate to 48%. This combination strategy sets camonsertib apart in a crowded market of DNA damage repair inhibitors and is further bolstered by Repare's collaboration with Roche, a validating partnership with financial milestones.

On another front, lunresertib emerges as a first-in-class PKMYT1 inhibitor. Unlike most cell cycle inhibitors plagued by toxicities, lunresertib demonstrates low myelotoxicity and diarrhea , presenting itself as a safer option. The drug also secured Fast Track designation from the FDA when combined with camonsertib, hinting at its clinical potential. Various collaborations, including those with Princess Margaret Cancer Center and the Canadian Cancer Trials Group, reflect a broad scope of clinical applications.

The preclinical pipeline shows promise as well, notably RP-3467, which outperformed its predecessor RP-2119 in potency. The termination of the Ono Pharmaceutical collaboration means Repare now wholly owns this asset, giving them strategic flexibility at the cost of bearing all developmental risks.

Financially, the milestone payments from Roche could provide much-needed, non-dilutive capital. In a high-risk sector like biotech, such external validations are crucial. In sum, Repare's recent advancements suggest a strategically diversified portfolio, but key upcoming data releases and partnership dynamics should be carefully watched for long-term viability.

My Analysis & Recommendation

In wrapping up this analysis, Repare Therapeutics occupies a compelling niche in targeted cancer therapy, buoyed by both strong clinical data and robust financials. Investors should remain acutely aware of three factors in the near term:

-

Clinical Milestones: The performance of camonsertib in ongoing trials will be pivotal. A strong showing here could potentially trigger milestone payments from Roche, not to mention bolstering investor sentiment. On the flip side, lackluster data could have a cascading negative impact.

-

Expense Dynamics: While currently well-capitalized, watch for any uptick in R&D or operational expenses. Given the 25-month cash runway, an unexpected acceleration in spending could bring about financing needs earlier than anticipated.

-

Market Sentiment: Elevated put activity and a short interest of 7.32% signal a cautious market. Any negative news could act as a catalyst for downside volatility. Conversely, meeting or exceeding clinical milestones could very likely squeeze out short sellers and provide upward price momentum.

For those looking at Repare as an investment, its clinical program is diverse and aligned with the state-of-the-art cancer therapies, and its partnership with Roche provides both a seal of approval and potential non-dilutive funding streams. Financially, the company appears to be on solid footing, mitigating some of the risks commonly associated with biotech investments. Therefore, after considering both the medical and financial parameters, my investment recommendation for Repare Therapeutics at this juncture would be a "Buy."

Risks to Thesis

While I've issued a "Buy" recommendation for Repare Therapeutics stock, consider these caveats. First, the revenue surge from collaboration agreements could be non-recurring; sustainability is key. Second, the FDA's Fast Track designation raises the stakes for clinical success; failure could lead to an abrupt sentiment shift. Additionally, although low now, a surge in R&D expenses might force the company to tap into equity markets earlier than anticipated. Lastly, Roche's milestone payments are double-edged: while beneficial, they tie Repare to performance metrics that, if not met, could lead to reduced funding. Insider selling over the past 12 months, albeit stale, remains a cautionary indicator. Exercise prudence.

For further details see:

Repare Therapeutics: A Compelling Bet On Synthetic Lethality