RPAY - Repay Holdings: Sticky Partnerships Power Recurring Revenues And Growth

2023-05-23 07:29:50 ET

Summary

- Once integrated with Repay Holdings' payment solution, the partnership tends to become long-lasting.

- The recurring nature of the Consumer Payments segment seems to indicate to have an average tenure of approximately seven years.

- The current boom in auto loans within Credit Union remains a near-term catalyst for RPAY.

- Growth in the B2B segment remains a major uncertainty at this point in time.

- RPAY stands as a wonderful company at a fair price.

Investment Thesis

I have been researching Repay Holdings Corporation ( RPAY ) for some time now and fully understanding the company has been difficult. While RPAY's products and business model interest me, the industry is highly competitive, making me cautious. However, a Dec 2021 video interview with the RPAY's CEO on Seeking Alpha helped clarify how RPAY differentiates itself - by finding a niche within this crowded space that remains underserved and providing the clients, a SaaS model based on transaction volume, rather than a fixed fee.

Please note that for this article, I will refer to RPAY clients as partners instead, as RPAY's business model focuses on transaction volume where it grows as its partners grow and generates less revenue when partners' businesses are impacted. RPAY's success is thus tied to the success of its partners.

What Does RPAY Do?

RPAY is a technology-enabled payment processing business that integrates its technology stack into partner platforms. Revenue comes from a take rate based on the volume of transactions processed.

The company focuses on providing payment solutions to two segments:

- To consumers to pay their financial liabilities through a B2B2C model

- Payment solutions for partners seeking to pay receivables and payables

RPAY May 2023 Presentation

While RPAY has grown through acquisitions of transaction processing companies, its future lies in organic growth. As stated per its 10-K:

From January 1, 2016 through December 31, 2022, we have successfully acquired eleven businesses. Given the large size and attractive growth trends of our current addressable market, we are primarily focused on growing our business organically.

By targeting both consumers and business partners, RPAY hopes to scale its payment solutions rapidly. Further acquisitions may supplement growth initially, but the real opportunity lies in expanding its relationship with existing partners and adding new partners organically over time.

Competitive Advantage of RPAY

Sticky SaaS Model that grows with partner

Once RPAY's technology stack is integrated, the relationship becomes very sticky. To integrate RPAY technology stack is a major infrastructure decision for the partners, and once that is completed, they are unlikely to change unless undergoing an acquisition or major restructuring. After all, infrastructure changes take time and effort, eventually impacting the partner's own revenue and profitability.

This was illustrated in the recent Q1 FY2023 earnings call transcript, where the CEO and CFO stated that Business Payments revenue declined due to:

Our net new growth was impacted from lapping political media spending, implementation time line delays and a large client being acquired… Business Payments net new growth was offset from lapping political media spending during the '22 election cycle, delays in implementation on the client side and lower volumes from a large client who started consolidating payment providers after being acquired… We think it's unique. It's -- obviously, it's an account that got acquired, so kind of out of our control. And so we really think that's unique.

RPAY's revenue model differs from traditional SaaS, where fees are fixed. RPAY earns more as partners' transaction volumes grow. But RPAY also earns less when volumes decline.

This combination of a SaaS and volume-based model may appeal to partners compared to fixed SaaS fees, especially during economic uncertainty. As volumes fluctuate, fixed fees remain constant while RPAY's revenue adjusts accordingly.

However, if a partner's business drops significantly, RPAY's revenue may decline sharply. To mitigate this risk, RPAY is continually adding partners to diversify its revenue base.

Diversification was highlighted in the FY2022 10-K, it states that:

As of December 31, 2022, we had over 23,000 clients. Our top 10 clients, with an average tenure of approximately seven years, contributed to approximately 15% and 14% of total gross profit during the year ended December 31, 2022 and the year ended December 31, 2021, respectively….The Company is highly diversified, and no single client represents greater than 10% of the business on a volume or profit basis.

Overall, RPAY's stickiness, variable revenue model, and efforts to expand the number of partner position the company favorably. Once integrated, partners are unlikely to change service providers. And growing the partner base reduces concentration risk.

The Recurring Nature of Consumer Payments

The consumer payments segment is highly competitive with banks, Visa, and Mastercard also vying for market share. However, RPAY has carved out a niche in underserved segments that larger players ignore.

Specifically, RPAY focuses on three verticals:

- The personal loans vertical is predominately characterized by installment loans, which are typically utilized by consumers to finance everyday expenses.

- The automotive loans vertical predominantly includes subprime automotive loans, automotive title loans and automotive buy-here-pay-here loans and also includes near-prime and prime automotive loans.

- Our receivables management vertical relates to consumer loan collections, which typically enter the receivables management process due to delinquency on credit card bills or as a result of major life events, such as job loss or major medical issues.

By integrating its technology, RPAY enables partners' customers to pay through various methods. This improved convenience reduces payment friction and facilitates partners collecting repayments. The faster collections allow partners to lend more, driving higher RPAY revenue.

Additionally, recurring payments from loan amortization and late fees benefit RPAY. For example, an auto loan customer makes monthly and occasional late payments, generating a consistent take rate for RPAY.

This recurring revenue yields more predictable guidance and visibility for investors. Essentially, RPAY earns a percentage of each dollar partners originate and subsequent collection from customers. As stated previously, partners' average loan tenures of seven years facilitate long-term RPAY income.

Near Term Catalyst - Growth in Credit Union

In the consumer payments segment, ACI Worldwide ( ACIW ) and SoFi's subsidiary Galileo/Technisys ( SOFI ) compete mainly for bank and fintech clients. In contrast, RPAY focuses on credit unions, an underserved market.

Credit unions represent an interesting growth opportunity for RPAY. In the following earnings calls, management highlighted credit unions as a key growth driver.

As of Q4 FY2022 Earnings Transcript , Jack Moore, the Executive Vice President of Consumer Payments stated:

Additionally, we now serve over 240 credit unions up from 200 in 2021 and have a great opportunity just within those customers. Further, there are thousands of other credit unions across the United States that represent a significant opportunity going forward. We recently signed multiple deals with several large credit unions, each of which have over $1 billion in assets.

As of Q1 FY2023 Earning Transcript, the CEO also noted:

Credit unions also remain a focus of ours. We signed 11 new credit union clients this quarter, bringing our total credit union customers to over 250. We continue to enhance and upgrade our integrations with partners such as MeridianLink and Jack Henry Symitar in order to facilitate accelerated distribution within this key vertical. The underlying trends have not changed from last quarter. We are still seeing demand for our clients' products and our clients are looking to us for more ways to engage and interact with the borrower from a payment perspective.

The CFO also answered one of the analyst questions and stated:

Yes. So I think that comment was related to some of the auto lending moving out of the traditional auto space into credit unions, just credit unions having generally lower rates they were benefiting from rates rising and then being able to provide competitive financing. So I think that we still see that happening. We're winning some auto financing business away from traditional lenders because of that dynamic. And credit unions have generally been strong. I think even through the last 6 weeks or so as we've seen issues with regional banks. We've seen real strength in credit unions because of their member deposit base and because of the loyalty the members have to them, which I would help with the originations for new loans to those members as well. So I think the biggest tie-in is probably between credit unions and auto.

In my opinion, credit unions remain a key growth driver for RPAY, for these 3 reasons:

Lower Interest Rate leading to higher demand for Loan Facilities

Given the Federal Reserve's significant interest rate hikes, credit union loan rates are typically lower than banks since profits from members are reinvested. This will likely drive higher demand for credit union loans during this high-rate environment. As the Fed continues raising rates, borrowers will increasingly turn to credit unions for more affordable loans.

Per Experian's Q4 2022 Automotive Finance Report, credit unions have a 29.12% auto loan market share, leading all segments. Credit unions offer the 2nd lowest new vehicle rates at 5.49% (captives are lower at 5.45%) compared to 7% at banks, and the lowest for used car financing rates at 7.03% versus over 9% at banks.

Auto loans remain a key vertical for RPAY. With credit unions' strong auto loan market share, this positions RPAY for increased recurring revenue potential.

More Deposit leading to more Loans

With the bank run crisis in regional bank runs, depositors are also shifting funds into credit unions. Like banks, the more deposits a credit union has, the more it can lend at lower interest rates.

Per the National Credit Union Administration , credit union shares and deposits rose $61.3 billion or 3.4% year-over-year to $1.85 trillion in Q4 2022.

The increase in credit union deposits positions them to expand lending. As a credit union partner, RPAY stands to benefit from this growth.

As credit unions originate more loans, the transaction volumes RPAY processes and its resulting take rate will rise. Credit unions' loan growth will also translate directly into higher recurring revenue for RPAY.

Huge Total Addressable Market

As per National Credit Union Administration, USA has 4,760 credit unions currently while RPAY has integrated with only 250, or about 5%, as of Q1 2023. This indicates a massive untapped market potential.

By focusing on expanding within the credit union vertical, RPAY could achieve exponential revenue growth.

In summary, RPAY has penetrated just a small fraction of the sizable U.S. credit union market. The addressable market remains vast and underserved. As credit unions expand their loan books and payment processing needs grow, RPAY is well positioned to facilitate that growth through its integrated solutions and large partner network.

Risk

A Potential Recession

Due to the fact that RPAY revenue is dependent on volume, a recession can cause a decrease in volume, and also downgrade prime deals to subprime ones.

However, this can be mitigated simply adding more partners to the equation which can help to compensate for the decrease in volume.

Competition in B2B business payment

As per FY2022 10-K:

The business-to-business vertical relates to transactions occurring between a wide variety of enterprise clients, many of which operate in the automotive, field services, healthcare, homeowner association ("HOA") management and hospitality industries, as well as educational institutions and governments and municipalities.

In my view, increased competition in the B2B segment poses a bigger risk to RPAY than a recession. The market appears extremely competitive with over 44 listed competitors, excluding banks, with many targeting healthcare as well.

To scale and differentiate itself, RPAY has actually made six acquisitions within this segment out of its 11 total as per new vertical expansion.

All 11 Acquisition (RPAY May 2023 Presentation)

{kind=link}

However, management's arguments for its competitive positioning are underwhelming. As per Q3 FY2022 earning transcript , from my perspective, the most convincing RPAY claim to differentiate its B2B offering was to offer "2-sided integrations" with Sage and Acumaticu, which allows for both AR and AP payment automation and execution directly within the ERP environment. But this may not provide sustainable differentiation given technology advancements.

RPAY's supplier network of 174k also pales in comparison to competitors like AvidXchange's ( AVDX ) 965k and Shift4 Payments' ( FOUR ) over 500 software partners, compared to RPAY's 248.

RPAY seems to be playing catch-up in the highly fragmented and competitive B2B space. Its scale, network, and technological capabilities currently trail major competitors.

While acquisitions have expanded RPAY's footprint, the company must grow organically faster to truly differentiate its offerings, particularly as large competitors increasingly target RPAY's focus areas.

Scale appears critical to success in this land grab-like environment. RPAY must leverage its integrations more strategically, expand its network at a quicker clip, and innovate more aggressively to truly establish a durable competitive advantage.

Otherwise, RPAY risks losing ground to much larger and better-resourced rivals over time. RPAY shows promise in focused niches but will need to execute flawlessly and identify new opportunities to truly scale and compete at the highest levels of the B2B market.

Valuation

Normally, I will be comparing my companies using EV/EBITDA ((TTM)) or PE Ratio ((TTM)), such as the articles I wrote for Movado ( MOV ) and Liquidity Services ( LQDT ).

However, RPAY continues to operate at a loss. Thus, I will only use EV/EBITDA as a comparison with its peers and as a gauge for valuation.

EV/EBITDA ((TTM)) Across Sector

- RPAY - 15.47

- Industry average - 12.51

Close Peers

- ACIW - 16.50

- FOUR - 22.38

- IIIV - 19.97

- USIO - NM

- FLYW - NM

- AVDX - NM

When compared to the industry average of 44 peers, RPAY appears to be overvalued. However, upon closer inspection of six similar peers, RPAY is actually the least expensive among them.

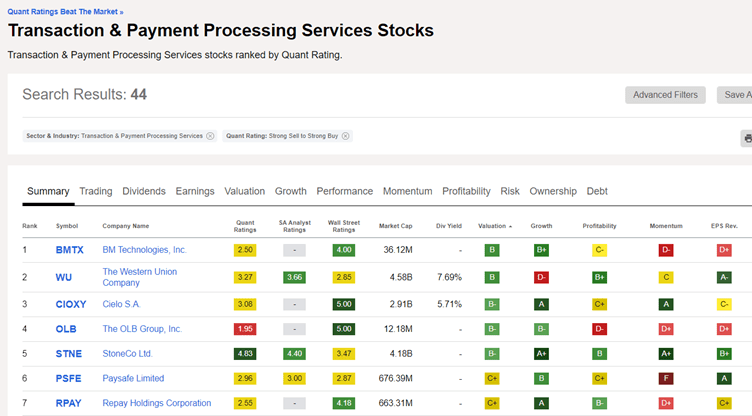

Alternatively, if we use Seeking Alpha's valuation grading for comparison, RPAY is considered undervalued and ranked seventh out of the 44 peers.

RPAY Rank 7th out of 44 Peers for valuation (Seeking Alpha Screener)

{kind=link}

Nevertheless, I think it's reasonable to conclude that RPAY is currently trading near its fair value. However, if the action plan for B2B segment is executed correctly, the company's multiples are likely to increase, resulting in a significant surge in the share price.

Conclusion

RPAY's integration of its payment solution into its partner's platform creates a strong and enduring relationship. Additionally, the recurring nature of these transactions provides greater confidence that RPAY can generate operating cash flow for an extended period, as stated in their last 10-K report.

Although its B2B segment remains uncertain, management have assured in their recent earning call that the B2B pipeline remain strong and they will continue to win businesses in the B2B segment.

Furthermore, RPAY's 11 acquisitions have likely provided them with sufficient growth opportunities, and as indicated in their 10-K report, the focus now is on organic growth.

It's worth noting that RPAY has also approved a share repurchase program that allows them to buy back up to $50 million of their outstanding Class A common stock. In 2022, RPAY already repurchased 1,078,141 shares for around $10.0 million under this program.

Finally, in Warren Buffet words, this remains a "Wonderful Company at a Fair Price."

For further details see:

Repay Holdings: Sticky Partnerships Power Recurring Revenues And Growth