RPAY - Repay Holdings: Too Many Uncertainties In The Macro Environment

Summary

- Repay Holdings Corporation operates in verticals with large total addressable markets and low card penetration.

- M&A is unlikely to occur in the near term, but is always an option for Repay Holdings to juice EBITDA growth.

- There are too many uncertainties in the macro environment, which I believe are going to weigh on Repay Holdings Corporation stock performance in the near term.

Recommendation

My recommended rating for Repay Holdings Corporation ( RPAY ) is hold. While RPAY stock is likely undervalued at current levels, I believe it is better to stay neutral. I think a stabilization in the macro is needed for RPAY to materially re-rate.

Business

Repay Holdings Corporation is a payments technology company that offers integrated payment processing solutions for important vertical markets like personal loans, auto loans, mortgage servicing, accounts receivable management, and business-to-business transactions.

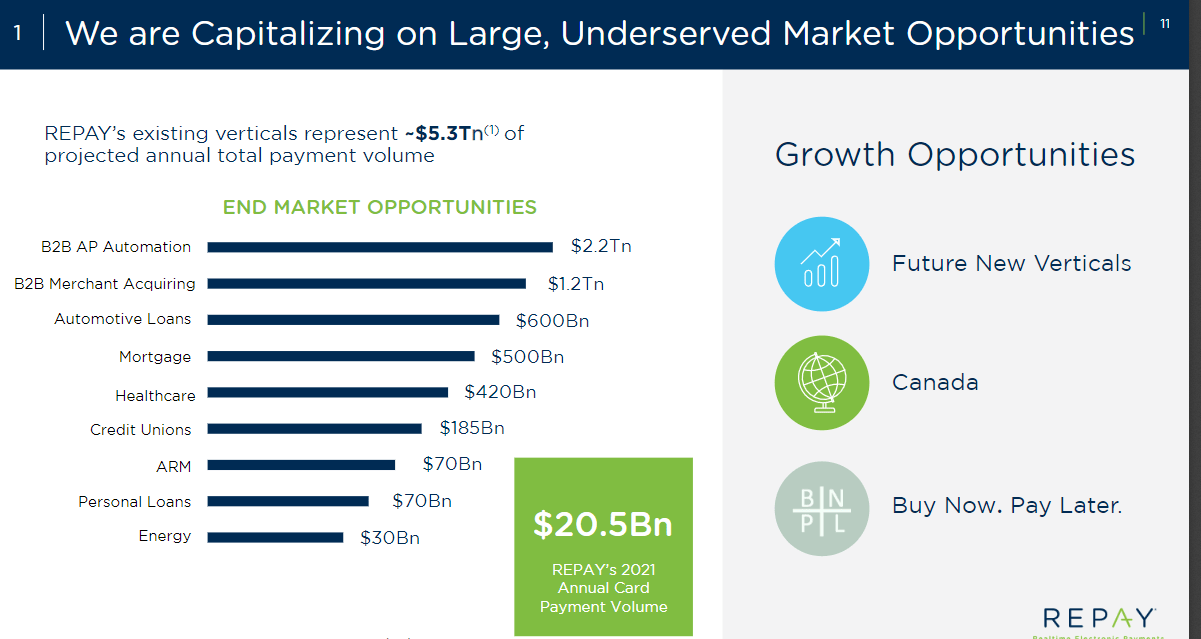

Large TAM with low card penetration

Repay Holdings Corporation has found success in niche markets, particularly the automotive and business-to-business sectors. Loan repayment, business-to-business, and supplementary payments are the three main use cases for RPAY. Mortgage servicing is a subset of the larger loan repayment market, which also includes consumer loans, vehicle financing, accounts receivable management, and so on. Management believes that the firm's total addressable market ("TAM") is easily over trillions of dollar, where the auto industry contributes $600 billion and the mortgage servicing vertical contributing another $500 billion., and the B2B segment easily over $2 trillion.

{kind=link}

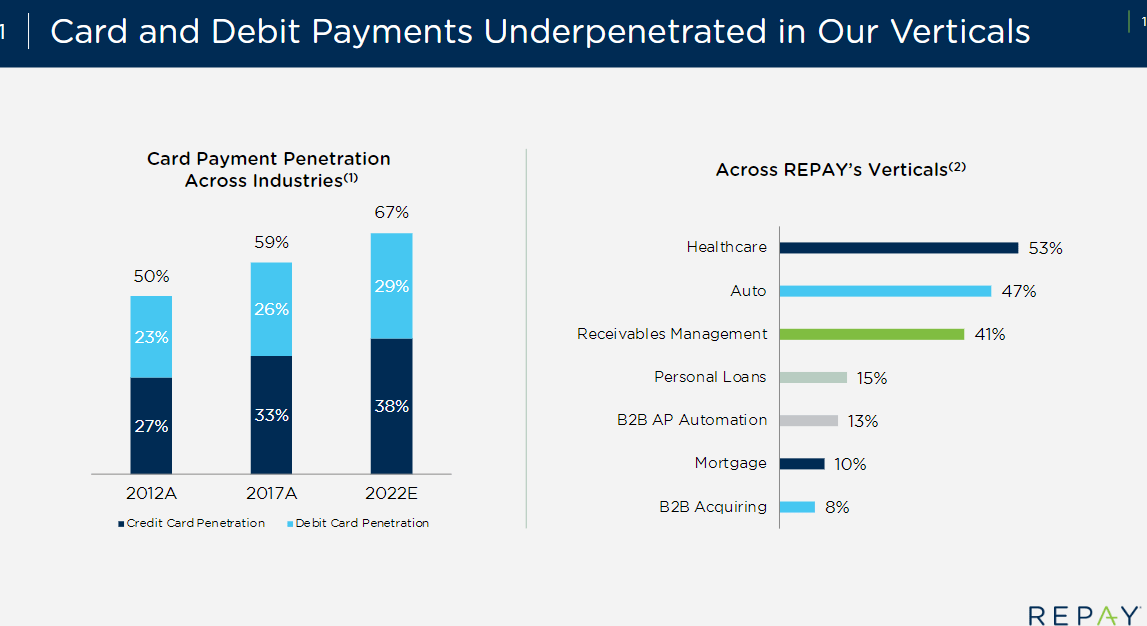

Given its size, it's clear that this TAM won't expand quickly. That said, in my opinion, RPAY's key markets where card penetration is low present a secular growth opportunity. For strategic purposes, RPAY has zeroed in on regions with low card penetration, betting that there will be a demand for its debit and virtual card services in those regions. In 2022, credit card use accounted for 89% of all purchases made by U.S. consumers. However, in some industries, such as business-to-business transactions and unsecured loans, card use was only around 22%. As the RPAY market with the highest card adoption, the auto vertical is still 20% behind the rest of the market. I believe RPAY has a lot of room to grow in the industry as a whole because it only has a small share of the market at the moment.

{kind=link}

Paying by card makes more sense, and stakeholders are agreeing

Currently, card processing accounts for the vast majority of RPAY business, with ACH accounting for only a small percentage of the remainder (around 10% based on the transcript from Wells Fargo's TMT conference in December 2020). The company charges merchants 160bps (Jan'20 Needham Growth Conference call), whereas the fee for an ACH transaction is much lower (less than $0.50). In response to consumer demand and friction points in traditional payment processing, businesses have progressively embraced digital payment methods despite their generally higher transaction costs. These data indicate that the impetus to switch to digital payment methods is substantial, and that RPAY is set up to capitalize on this trend.

Sales model different from peers

RPAY's method of reaching potential customers is twofold: direct sales and integrations with major platforms prevalent in the verticals of interest. I think it's smart that RPAY has integrated its tech with major software vendors in the industries it serves. As a result, RPAY is able to integrate its technology into the mission-critical applications of its clients, guaranteeing the smooth functioning of its payment processing technology within their back-end systems. Furthermore, these integrations make it easier for the RPAY sales team to obtain new client prospects or react to inbound leads, as many businesses will opt for a solution provider who is currently embedded or is capable of integrating its solutions with the business's primary back-end system. With this in mind, Repay Holdings Corporation's successful integration with a wide variety of widely adopted enterprise management systems in the industries it serves makes its platform an even more attractive option for those companies.

When compared to competitors, RPAY's sales model stands out because it prioritizes its own direct sales force and uses software partners as a referral channel. Half of its new merchant leads come from software partners' recommendations (source: Jan'20 Needham Growth Conference), with the other half coming directly from the merchant themselves.

However, even if a software partner refers a merchant to Repay Holdings Corporation, RPAY is the one who does the underwriting and onboarding, and thus retains ownership of the relationship. Because of this, RPAY's software partners receive a smaller percentage of the company's total revenue than the industry average. Owning the customer relationship is a risky strategy, but I see both pros and cons to RPAY taking that step. As a plus, they'll have complete control over future interactions with the customer, making upsells and cross-sells simple. On the other hand, because of its own sales force's limitations, it cannot expand as rapidly.

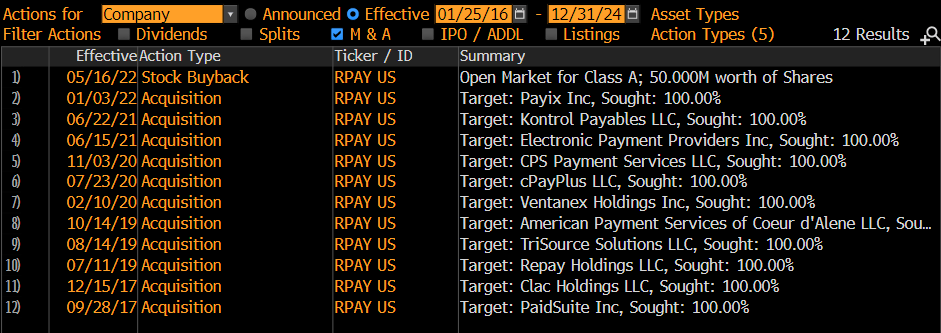

M&A growth

RPAY has a history of buying up payment companies in low-card-penetration markets, and then utilizing those firms' relationships and capabilities to convert more non-card transactions to card/digital. As the market is changing so rapidly, I believe this is the correct strategy as it shortens the time it takes to get to market. That aside, I believe this M&A tactic will be used to deepen penetration into RPAY existing markets, penetrate adjacent markets, enhance payment processing tech, and possibly attract a broader customer base. Looking at their previous work, I think RPAY is also fairly strategic. Nine of RPAY's eleven acquisitions since 2016 have occurred after the company's 2019 IPO. Many of these buyouts have helped RPAY extend its reach in the B2B market and into new industries.

{kind=link}

Following the 3Q22 earnings report , management once again reaffirmed their capital allocation strategy, focusing on growth initiatives and share repurchases. Given that RPAY's valuation has slid quite a bit and funding is difficult to come by in the current market, I think this is a sensible course of action. Although, looking ahead to FY24, if RPAY keeps its leverage ratio at 4x net debt to EBITDA (after debt paydown between FY22 and FY24), I believe RPAY can get access to an additional $150 million to $200 million (net debt after debt paydown between FY22 and FY24) funding, based on consensus FY24 EBITDA estimates of $150 million. Management has shown a willingness to pay 9-12x EBITDA for assets in the past, which suggests they could add $12-22 million of EBITDA, or 10%-15% to FY24 EBITDA estimates.

Strong quarter performance has cleared investors’ concerns

Some investor anxiety about the effects of the deteriorating credit environment may have been allayed by the strong performance in the third quarter, in my opinion. Given the commentary around the tightening origination market in the prior quarter, RPAY's 3Q beat and reiterated guide stood out because investors were likely expecting continued softness due to associated credit market pressures. In more detail, Consumer Revenue slowed to high single digit growth in the quarter, while Business-to-Business Revenue soared by 30%. That said, I believe a key metric to track is the Consumer segment, which is likely to be a lot more correlated with underlying credit performance.

Since there is uncertainty about how a deteriorating credit environment will affect RPAY's results in FY23, I believe that investor confidence in the company's earnings power is low. To put this into perspective, RPAY is primarily compensated by the volume of consumer loan repayments; thus, a deterioration in consumer credit would cause lenders to tighten their appetite for loans and reduce the volume of new loan originations. In terms of its outlook for 2023, management seems to be rather confident in their ability to execute as they anticipates growth in the low to mid-teens even in a mild recession scenario,. All is good in the guide, but I believe it would be safer to jump onto the bandwagon when I see evidence of this crystalizing. While the third quarter was encouraging, the consumer lending environment is only just weakening and there is still a wide range of possible outcomes if it continues to deteriorate.

Valuation & model

Using consensus estimates, I believe Repay Holdings Corporation is worth $10.20 in FY23, an 11% upside. While there is upside, I believe the range of outcomes if wide here given the uncertainties in the macro environment. As such, I think a wide margin of safety in terms of valuation/stock price is required before RPAY becomes an attractive investment. I note that my model does not reflect any positive change in the environment in the short-term. If it does, RPAY could see higher growth and valuation rerating, which could lead to higher share price.

Author’s own calculations

Risk

Sensitive to macro movements

The Repay Holdings Corporation business model, like that of other merchant acquirers, is sensitive to changes in consumer spending habits and the well-being of its merchants. The company stands to lose more money and see lower future volumes if the business failure rate in any of its verticals increases. As a result of its involvement in so many different industries, it is especially attuned to broader economic shifts.

Summary

Although I think Repay Holdings Corporation stock is undervalued at current prices, I would advise remaining neutral until such time as the macroeconomic environment becomes more stable and RPAY can undergo a meaningful re-rating.

For further details see:

Repay Holdings: Too Many Uncertainties In The Macro Environment