REPYY - Repsol: Capital Return Story Remains Intact

2023-11-02 06:37:57 ET

Summary

- Repsol's capital return story remains attractive, with potential for further valuation re-rating and total returns.

- The company's Q3 2023 financial report showed strong performance in the Upstream sector and improved refining margins.

- Management announced increased dividends and a successful share buyback program, with potential for at least 8.1% in total capital returns.

Overview

My recommendation for Repsol (REPYY) is a buy rating as the capital return story remains very attractive and management is committed to continuing doing so. The market is recognizing this fact, and this shows potential for further valuation re-rating and further juicing total returns. Note that I previously rated a buy rating for REPYY as I believe the FCF/P yield was too attractive to ignore, and the valuation relative to REPYY history does not make sense given that it is a much better business.

Recent results & updates

Repsol has released a robust financial report for the third quarter of 2023, which aligns with the capital return thesis I have discussed previously. Although the adjusted income of €1.045 billion fell 5% below the consensus, the adjusted net income of €1.082 billion was in accordance with the consensus estimate of €1.09 billion. At a fundamental level, I think the focus was the effective implementation in the Upstream sector and the significant improvement in refining margins in 3Q23, following a decline in 2Q23 in the Downstream sector. In terms of earnings, 3Q23 Refining experienced a recovery as benchmark refining margins saw a significant increase, more than doubling in comparison to the previous quarter. This growth was primarily driven by robust demand for middle distillates and a decrease in inventories. The occurrence of middle distillate cracking was facilitated by the combination of limited supply and depleted inventories, which coincided with an upsurge in demand during the summer travel period. More specifically, in 3Q23, Repsol experienced a 9% increase in hydrocarbon production, reaching 596 kbpd. This growth can be attributed to the successful initiation of new wells in the Eagle Ford and Marcellus shale assets, as well as the acquisition of Inpex assets in the Eagle Ford region. Additionally, reduced maintenance activities in Peru, increased gas demand in Venezuela, and improved performance of the YME project in Norway contributed to this positive outcome. In relation to Venezuela, my sentiment has become more optimistic subsequent to this outcome, as Repsol has acquired an additional four shipments, amounting to a cumulative total of 3 million barrels of oil. The underlying idea is that the increased production of heavy oil from Venezuela has positive implications, not only for the exploration and production sector in terms of financial remuneration for the extracted resources in Venezuela. This is also great news for Repsol because it will allow them to better optimize their refining system for their particular slate of crudes.

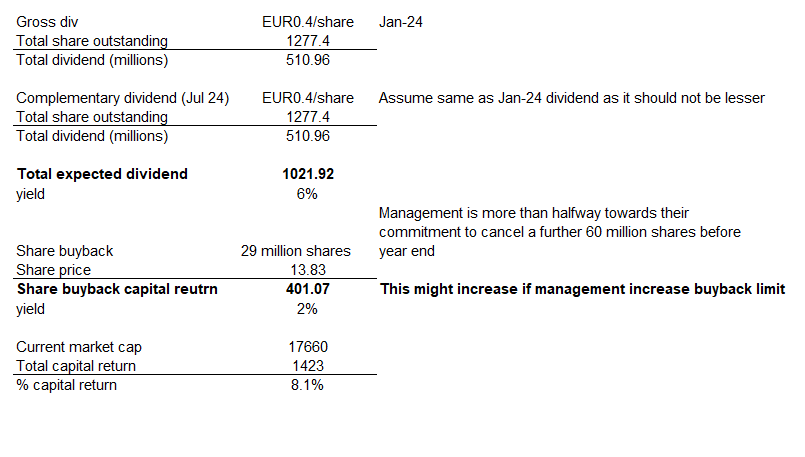

The focal point of the earnings report, in my perspective, revolved around the narrative of capital return. Management announced the dividend for January 2024, which will be an increase to €0.40 gross per share, which represents a 14% growth in comparison to the dividend amount for January 2023. Importantly, the management has indicated that the forthcoming complementary dividend, scheduled for disbursement in July 2024, will not be less than the interim dividend slated for payment in January 2024. The strong dividend policy is accompanied by a strong share buyback program. Throughout the quarter, Repsol successfully procured a total of 24.6 million shares via its ongoing buyback program, which has been in effect since the conclusion of July. Furthermore, an additional 10 million shares were acquired through the settlement of derivatives. As a result, the company has currently achieved over 50% progress towards fulfilling their pledge to eliminate an additional 60 million shares by the conclusion of the current year, thereby reaching a total of 110 million shares cancelled by 2023. As such, if we do the math for capital returns ahead, the total capital returns expected should be at least 8.1% based on my calculation. The yield could be higher if the complementary dividend on July 24 is higher and the buyback limit increases.

you could expect complementary in July that is not going to be, in any case, lower than the interim dividend we are anticipating this January 2024 related to the interim dividend. From: 3Q2023 earnings call

{kind=link}

Valuation and risk

{kind=link}

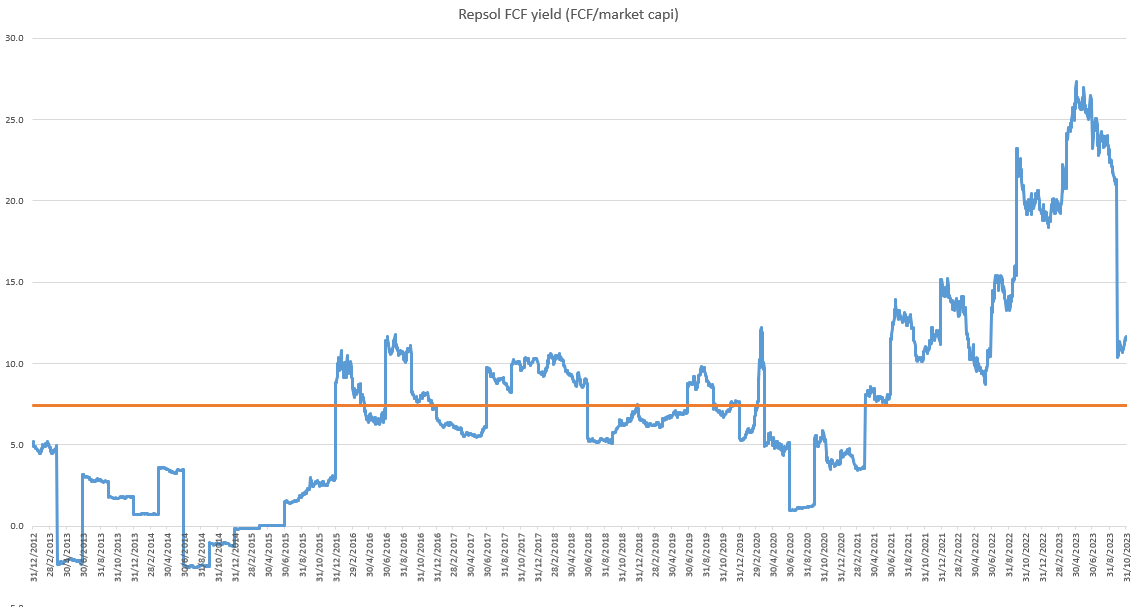

At the rate that the stock is trading, the capital return story remains very attractive, as investors can continue to yield at least 8% returns based on FCF allocation. The additional upside here is if the stock P/FCF valuation compresses back to the historical average of 7.4%. Repsol current trades at 11.7x P/FCF (which equates to ~8.5% FCF yield); if that compresses to 7.4% (which equates to 13.5x P/FCF), this implies an upside of 15%. Adding this 15% to the minimum of 8% in capital returns equates to a potential total return of more than 20% at this level. I believe there is a good chance of P/FCF rerating as the business fundamentals continue to perform well and the market is clearly recognizing the Repsol capital return story, as evident by the compression in FCF yield (as seen from the chart).

One of the risk is that Repsol's financial performance is highly sensitive to fluctuations in oil prices. As a significant player in the oil and gas industry, the company is exposed to the risk of adverse movements in global oil prices. These fluctuations can be influenced by geopolitical tensions, supply and demand dynamics, and other external factors beyond Repsol's control. The company's revenue and profitability are vulnerable to such price volatility.

Summary

REPYY continues to present an attractive capital return story, making it a compelling investment. The company's management is committed to delivering on this promise, and the market's recognition of this fact suggests potential for further valuation re-rating and enhanced total returns. The core of the earnings report centers around capital return, with a substantial increase in dividends and a robust share buyback program. This commitment to returning capital to shareholders is expected to yield at least 8.1% in total capital returns, with the potential for even higher returns based on future dividends and buybacks.

In terms of valuation, Repsol's capital return story remains highly attractive, offering the potential for significant returns, with a potential total return of more than 20% at current levels. The market's growing recognition of Repsol's capital return story is evident, further supporting the positive outlook. However, it's essential to note that Repsol's business is highly sensitive to fluctuations in oil prices, which remain a significant risk factor. Geopolitical tensions and supply-demand dynamics can impact oil prices and, subsequently, Repsol's revenue and profitability.

For further details see:

Repsol: Capital Return Story Remains Intact