RBCAA - Republic Bancorp: An Attractively Valued But Run-Of-The-Mill Bank

Summary

- The declining loan trend will likely reverse soon; however, the loan growth will likely be subdued in the coming quarters.

- Thanks to the recent improvement in the deposit mix, the margin is slightly positively correlated to interest rates.

- The December 2022 target price suggests a high upside from the current market price. Further, RBCAA is offering a decent dividend yield.

Earnings of Republic Bancorp, Inc. ( RBCAA ) will most probably dip this year due to the normalization of provisioning for expected loan losses. On the other hand, subdued loan growth and slight margin expansion will likely offer some support to the bottom line. Overall, I'm expecting earnings to dip by 5% this year to $4.05 per share. For 2023, I'm expecting earnings to remain mostly flattish. The year-end target price suggests a high upside from the current market price. Therefore, I'm adopting a buy rating on Republic Bancorp.

Strong Job Markets To Help Reverse The Declining Loan Trend

Republic Bancorp's loan book declined by 0.5% in the second quarter of 2022. Except for 4Q 2021, the loan portfolio has declined sequentially in every quarter since June 2020. I believe the downtrend will reverse for good in the second half of this year due to the effect of favorable job markets. Republic Bancorp operates in five states, namely Kentucky, Indiana, Florida, Tennessee, and Ohio. All five states currently have strong job markets, with unemployment rates that are near record lows.

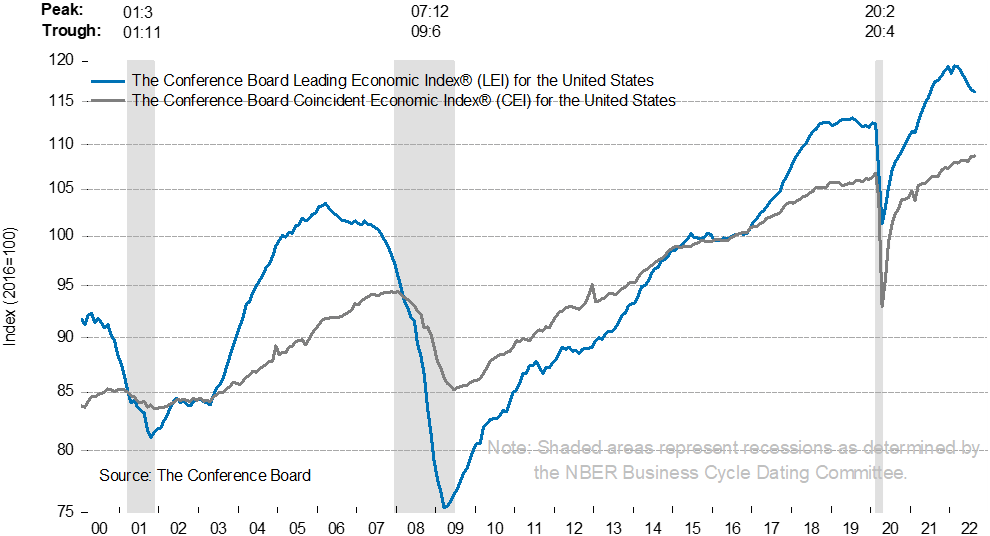

By asset subtype as well, the loan portfolio is well diversified. Loans range from credit cards and residential real estate to aircraft and commercial real estate. Therefore, the broad-based U.S. leading economic index is also a good gauge of credit demand in Republic Bancorp's markets. As shown below, the leading index continues to be on a downtrend, but at least the slope is less steep than before.

{kind=link}

Overall, I'm expecting loan growth to return to the pre-pandemic norm of low to mid-single digits in the coming quarters. I'm expecting the loan portfolio to grow by 0.75% every quarter till the end of 2023. Meanwhile, I'm expecting other balance sheet items to grow mostly in line with loans. The following table shows my balance sheet estimates.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22E |

| FY23E |

| Income Statement |

| Net interest income |

| 226 |

| 236 |

| 232 |

| 221 |

| 222 |

| 238 |

| Provision for loan losses |

| 31 |

| 26 |

| 31 |

| 15 |

| 27 |

| 28 |

| Non-interest income |

| 63 |

| 75 |

| 87 |

| 87 |

| 101 |

| 103 |

| Non-interest expense |

| 164 |

| 172 |

| 185 |

| 182 |

| 193 |

| 207 |

| Net income - Common Sh. |

| 78 |

| 92 |

| 83 |

| 87 |

| 82 |

| 83 |

| EPS - Diluted ($) |

| 3.74 |

| 4.41 |

| 3.99 |

| 4.24 |

| 4.05 |

| 4.11 |

| Source: SEC Filings, Earnings Releases, Author's Estimates(In USD million unless otherwise specified) |

Actual earnings may differ materially from estimates because of the risks and uncertainties related to inflation, and consequently the timing and magnitude of interest rate hikes. Further, a stronger or longer-than-anticipated recession can increase the provisioning for expected loan losses beyond my estimates.

Adopting A Buy Rating

Republic Bancorp has a long-standing tradition of increasing its dividend every year. Therefore, I'm expecting the company to increase its dividend by $0.011 per share to $0.3520 per share in the fourth quarter of 2023. The earnings and dividend estimates suggest a payout ratio of 34% for 2023, which is above the five-year average of 29% but still easily sustainable. Based on my dividend estimate, Republic Bancorp is offering a forward dividend yield of 3.6%.

I'm using the historical price-to-tangible book ("P/TB") and price-to-earnings ("P/E") multiples to value Republic Bancorp. The stock has traded at an average P/TB ratio of 1.17 in the past, as shown below.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| Average |

| TBVPS - Dec 2022 ($) |

| 40.3 |

| 40.3 |

| 40.3 |

| 40.3 |

| 40.3 |

| Target Price ($) |

| 39.2 |

| 43.2 |

| 47.2 |

| 51.2 |

| 55.3 |

| Market Price ($) |

| 38.9 |

| 38.9 |

| 38.9 |

| 38.9 |

| 38.9 |

| Upside/(Downside) |

| 0.7% |

| 11.0% |

| 21.4% |

| 31.7% |

| 42.1% |

| Source: Author's Estimates |

The stock has traded at an average P/E ratio of around 10.4x in the past, as shown below.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| Average |

| EPS - 2022 ($) |

| 4.05 |

| 4.05 |

| 4.05 |

| 4.05 |

| 4.05 |

| Target Price ($) |

| 34.0 |

| 38.0 |

| 42.1 |

| 46.1 |

| 50.2 |

| Market Price ($) |

| 38.9 |

| 38.9 |

| 38.9 |

| 38.9 |

| 38.9 |

| Upside/(Downside) |

| (12.7)% |

| (2.2)% |

| 8.2% |

| 18.6% |

| 29.0% |

| Source: Author's Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $44.6 , which implies a 14.8% upside from the current market price. Adding the forward dividend yield gives a total expected return of 18.4%. Hence, I'm adopting a buy rating on Republic Bancorp.

However, I'm not enthusiastic about this company because it's mediocre in many respects, especially rate sensitivity and organic loan growth. I am most dissuaded by the point that its earnings have been rangebound in the past and are likely to remain rangebound in the future. Unlike most other banks, there is no clear uptrend. Therefore, I wouldn't want to buy and hold this stock for long. My strategy would be to buy and exit whenever its market price gets closer to its fair value.

For further details see:

Republic Bancorp: An Attractively Valued But Run-Of-The-Mill Bank