FRBK - Republic First: High Failure Risk

2023-04-04 17:58:15 ET

Summary

- Republic First's unrealized losses on held-to-maturity securities exceeded shareholders' equity as of the end of the year.

- The company's uninsured deposit ratio of 64% is equal to - or higher - than those of many regional institutions considered at risk.

- The consummation of the recently announced equity raise is questionable in our view and insufficient to materially change the trajectory.

- The risk of failure is significant, making the shares highly speculative.

Republic First Bancorp ( FRBK ) is the bank holding company for Republic Bank, a $6 billion community bank operating in the region around Philadelphia including regions of Pennsylvania, Delaware, and New Jersey. The company has struggled for some time due to a variety of factors but the company's condition has deteriorated further in the context of the current banking turmoil.

Republic First is, in our view, highly susceptible to failure as unrealized losses on investment securities exceed the company's stated shareholders' equity. This will likely remain the case even if the bank successfully consummates the recently announced capital infusion via private placement of equity securities. The bank's shareholders' equity, including unrealized losses on held-to-maturity investment securities, is currently negative and with the proposed capital infusion would result in, at best, a marginally positive position, very similar to the condition of Silicon Valley Bank (SIVBQ) shortly before a withdrawal exodus caused that institution's failure. Moreover, we believe Republic First is at significant risk of a similar outcome due to the high proportion of uninsured deposits at risk in a potential failure. In any event, we consider Republic First's future highly uncertain given the institution's current financial condition and would avoid the company's shares.

Auditor Questions

Republic First has been operating under a cloud of uncertainty for nearly a year since the company's auditor requested an independent review of certain relationships and previously disclosed transactions with related parties . The result of the independent review has been significantly delayed securities filings , including the company's last annual report (for 2021) and quarterly reports for 2022, the last of which was recently filed with the Securities and Exchange Commission. The company's annual report for 2022, which should have been filed in March, is currently not expected to be filed until May. However, the bank's financial condition beyond any questions about related party transactions can be assessed through the bank's separate filings with banking regulatory authorities. The filings, which are available through December 31, 2022, paint a bleak picture of the institution's financial position.

Negative Shareholders' Equity and Withdrawal Risk

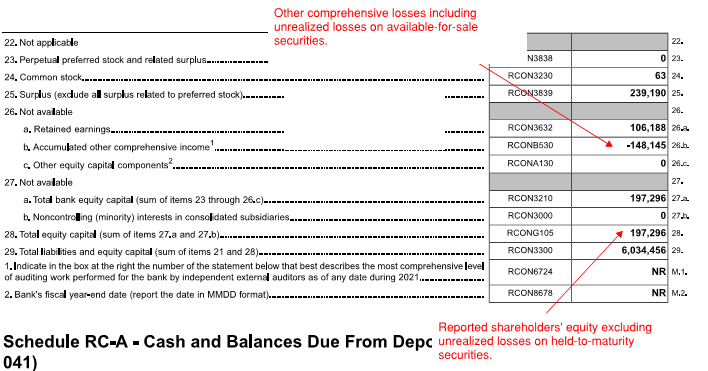

Republic First's bank equity capital as of December 31, 2022, stood at $197.3 million including significant unrealized losses on available-for-sale securities of approximately $167.3 million.

Republic First Shareholders' Equity (FFEIC)

{kind=link}

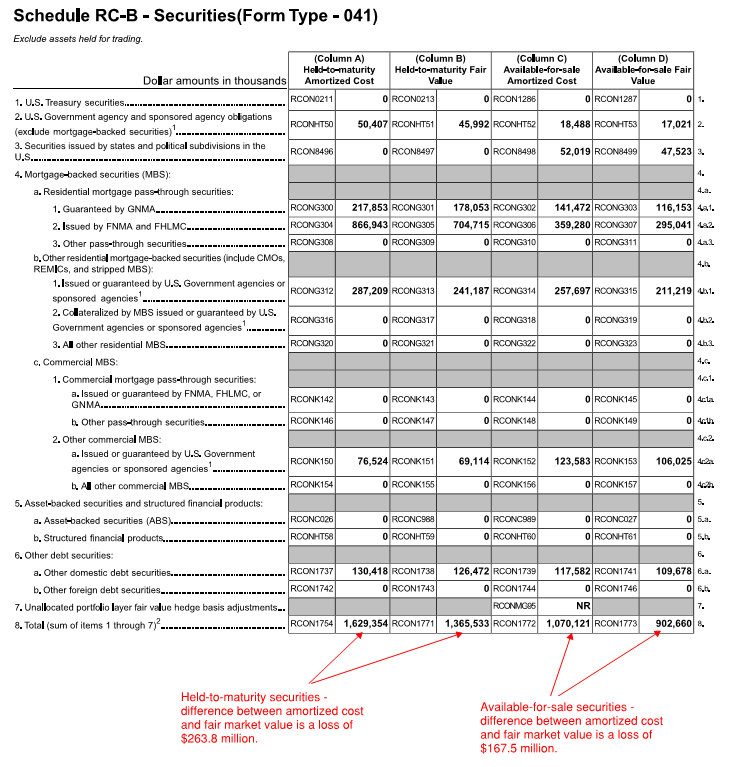

However, this figure excluded an additional $263.9 million in unrealized losses on held-to-maturity securities which, if included in the bank's shareholders' equity, would result in negative shareholders' equity of ($66.6 million).

Republic First Investment Securities (FFEIC)

{kind=link}

Granted, the after-tax unrealized losses would be somewhat less - perhaps in the range of $233.1 million - but this would still yield a negative value for shareholders' equity. The situation in this regard is arguably worse than the conditions present at Silicon Valley Bank at the end of the calendar year just months before that institution's failure. In Silicon Valley Bank's case, unrealized investment securities losses on held-to-maturity securities were roughly equivalent to the bank's shareholders' equity. Republic First's unrealized investment securities losses exceed shareholders' equity by more than $1.33 for every $1.00 in reported shareholders' equity, materially worse than the year-end situation at Silicon Valley Bank and a condition which we would argue makes Republic First effectively insolvent particularly given the clear insolvency and failure of Silicon Valley Bank under comparatively better conditions.

This wide differential places the company's depositors at risk particularly given the company's notably high proportion of uninsured deposits compared to other community banks we have assessed of smaller or comparable size. Republic First's financial reports, as of December 31, 2022, state that estimated uninsured deposits were $3.2 billion against total deposits of $5.0 billion resulting in uninsured deposits comprising some 64% of total deposits.

Republic First Total Deposits (FFEIC) Republic First Estimated Uninsured Deposits (FFEIC)

{kind=link}

{kind=link}

This ratio is actually comparable to or even higher than the uninsured deposit ratios at community and regional banks that have been in the news recently as having an elevated risk of failure, including PacWest Bancorp ( PACW ), Western Alliance Bancorporation ( WAL ), and Comerica ( CMA ), and not different by that significant a margin from the uninsured deposit ratio of the presently much discussed First Republic Bank ( FRC ) as of the end of the calendar year.

The bank's current financial position, and whether there has been a significant exodus of withdrawals in the last quarter, will not be known until the bank's next financial report which will be due in the next few weeks. However, as with Silicon Valley Bank, it's clear in our view that any material movement by depositors to withdraw deposits from the bank would result in significant pressure on the company's regulatory capital ratios and push regulators to seriously consider closing Republic First. The potential for depositor unease even in the face of lending programs sponsored by government agencies to support weak institutions exists as reflected by the flow of deposits from similarly positioned institutions. The potential for a concerted or coordinated withdrawal of uninsured deposits by depositors is perhaps less than was the case at Silicon Valley Bank, where depositors were highly concentrated and correlated by business line, and Republic First's smaller size makes a full depositor backstop, if not guaranteed, certainly much more feasible. However, these factors do not change the fact that Republic First's financial position places the bank's uninsured depositors at an elevated risk of loss as compared to the broader industry and it's difficult to see how any material loss of confidence by depositors would not precipitate a crisis similar to that faced by Silicon Valley Bank and, to a lesser extent, First Republic Bank.

Interest Rate Sensitive Portfolio

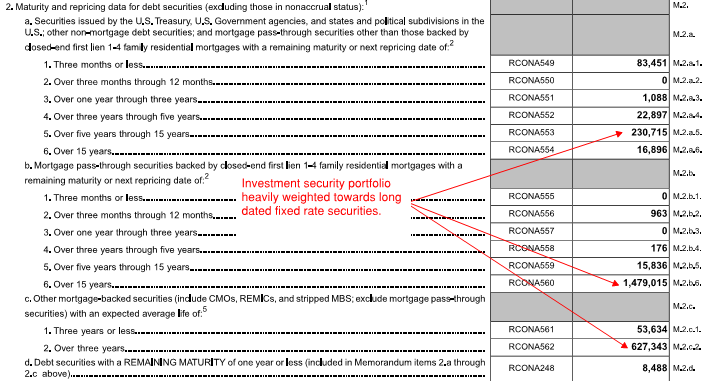

Republic First's financial position is due to the composition of the investment portfolio which is weighted towards long-duration securities that are particularly susceptible to changes in interest rates. A full $1.5 billion of the company's $2.7 billion in investment securities (at amortized cost) have the maturity or repricing scheduled exceeding 15 years.

Republic First Investment Securities Profile (FFEIC)

{kind=link}

The figure excludes an additional $230.7 million of investment securities that do not mature or reprice for at least five years and $627.3 million of mortgage-backed securities with indefinite maturity dates but with an expected remaining life exceeding three years. It's worth noting that the sale of the bank's entire investment securities portfolio - the bank's most liquid asset which carried a fair value of $2.27 billion at the end of the calendar year - would cover less than 75% of the company's uninsured deposits.

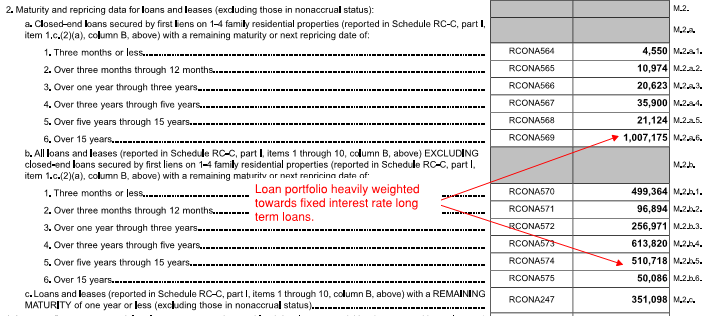

The company's loan portfolio is only in a slightly better position from a duration standpoint with approximately $1.0 billion of the company's $3.1 billion loan portfolio not maturing or repricing for at least 15 years.

Republic First Loan Maturity Profile (FFEIC)

{kind=link}

However, this large tranche of longer-dated loans - with another $613.8 million maturing or repricing within 3-5 years and $510.7 million maturing or repricing within 5-15 years - means that there would likely be a significant valuation discount applied in the event of a sale of a part of the loan portfolio or of the bank limiting any potential recovery for common shareholders. In turn, this limits the potential likelihood of an acquisition which would yield much value for common shareholders. The variability of prepayment potential on loans can make valuation estimates more volatile than fixed-income investment securities but this should not be so significant as to vary widely from comparable securities.

A Potential Equity Raise?

Nonetheless, the company did announce on March 10 an agreement to raise $125 million in equity capital in conjunction with community bank investor Castle Creek Capital and affiliates. The agreement is not entirely surprising although it's not clear that the company has been or will be able to close the transaction as there are a number of conditions including the participation of additional outside accredited investors and a number of regulatory approvals associated with stock ownership, etc.

Notably, however, this capital infusion would still leave the bank in a precarious financial situation even though headline regulatory capital ratios would improve somewhat with the additional financing. The capital infusion - potentially consisting of a mix of convertible preferred stock, common stock, and warrants - was priced at the time at $2.25 per common share equivalent which was above the trading price of approximately $1.75 and well above the market price of $1.30 three weeks later.

We view the ultimate consummation of the equity infusion to be questionable. The market price certainly suggests little enthusiasm for the agreement from current shareholders while we consider the magnitude of the infusion too small to make a material difference in the company's financial condition. The contribution of $125 million (or potentially more if certain additional allocations are exercised) doesn't resolve the company's capital issues or materially alleviate the withdrawal risk of uninsured deposits. The combination of heavy potential equity dilution, new preferred shares, significant unrealized losses on investment securities and the corresponding discount on the company's long-duration loan portfolio in the event of a sale likely means there is essentially no value available to a potential acquirer.

Conclusion

Republic First, in its current condition, is in our view unlikely to survive without significant support from equity investors and government backstops. The company's shares may represent a wild card in the event the company can raise sufficient capital to recapitalize the institution but, even if it manages to close all proposed financing, doing so will come at a significant cost in dilution to the existing shareholders. Still, we view Republic First as a fragile institution in worse financial condition and subject to the same potential loss of confidence which brought down Silicon Valley Bank. The question may not be if, but when, regulators recognize the situation is untenable at Republic First. Ultimately, we do not believe whatever potential for salvaging the company is worth the high corresponding risk of dilution or even survival.

For further details see:

Republic First: High Failure Risk