ICE - Retail Investors' Markets Must Be Simple To Succeed

2023-07-11 05:25:05 ET

Summary

- The current National Market System is too complex for retail investors, who need a simpler system.

- The NMS, created by the SEC, is more suited to computer-driven arbitrageurs, leaving retail investors with limited options.

- The article suggests creating a new system that is both simple and significantly improved for retail investors, which would require a private initiative rather than regulatory intervention.

Introduction

Retail investors make decisions infrequently and with little time to consider the complex ins and outs of our very complicated SEC-created National Market System ((NMS)). Retail investors rightly crave simplicity. Market structure expert, Larry Tabb, points out that in a complex world, simplicity is not always your friend. I agree but with a proviso. When an important decision must be made, yet there is little time to make it, a simple choice is far more useful than a complicated one.

On the other hand, creating a simple effective system for retail use is anything but simple. While the alternative considered here would be simple for investors to use, it is complicated itself. Modifying the NMS to meet investor needs is simply complicated.

What will it take to combine simplicity with a better deal for retail investors? The retail system must evaluate retail needs and build pro-retail properties into the market structure so that retail can improve on an OTC fill from a wholesaler within the NMS with a few words to a retail broker.

The current securities market structure, the NMS, provides retail investors with one choice - an afterthought in a system designed to meet the needs of computer-driven arbitrageurs. A worthy objective is to provide investors with a choice built for them only.

This series of articles, beginning with my earlier analysis of the stock market, wends its way through the global financial markets from a retail investor's perspective. The articles identify financial markets' failure to address their fundamental purpose, sending savings inexpensively and efficiently to their most productive investment use. A symptom of Wall Street's untoward preoccupation with self is that the key savings engine, retail investment, has become an afterthought in the structure of today's financial markets.

Following the earlier article that addresses the problems of the NMS, this article outlines a way to create efficient alternatives to the NMS that meet the requirement that markets for retail investors must be both simple and significant improvements on the NMS from a retail investor's point of view.

Implications for securities prices

The important implication for winners and losers among the major exchange management firms (ICE, CME Group, NASDAQ, CBOE) are:

- These firms are less risky now than their market values suggest. Their prices should be higher.

- A better financial market structure will raise the combined market values of the exchange managers substantially but all the increased value will go to the innovator.

- When the innovator appears, risk will return to more appropriate higher levels and the rewards increase as well. Bottom line -- a better market structure will reward the winner more than it punishes the losers.

The current retail market structure

The universe of market participants may be divided into two parts, full-time and occasional investors. If investing is your full-time job, you don't mind a little complication. Armed with a fast computer loaded with proprietary algorithms, you probably welcome complications. But if, like most of us, investing is something you do infrequently, then simplicity is the route for you.

Thus, we need two systems - one for computerized algorithm-driven firms (algo traders) and another for retail investors. We have the perfect system for algo traders - the SEC's NMS. But we should be doing a whole lot better for retail investors.

Retail investors

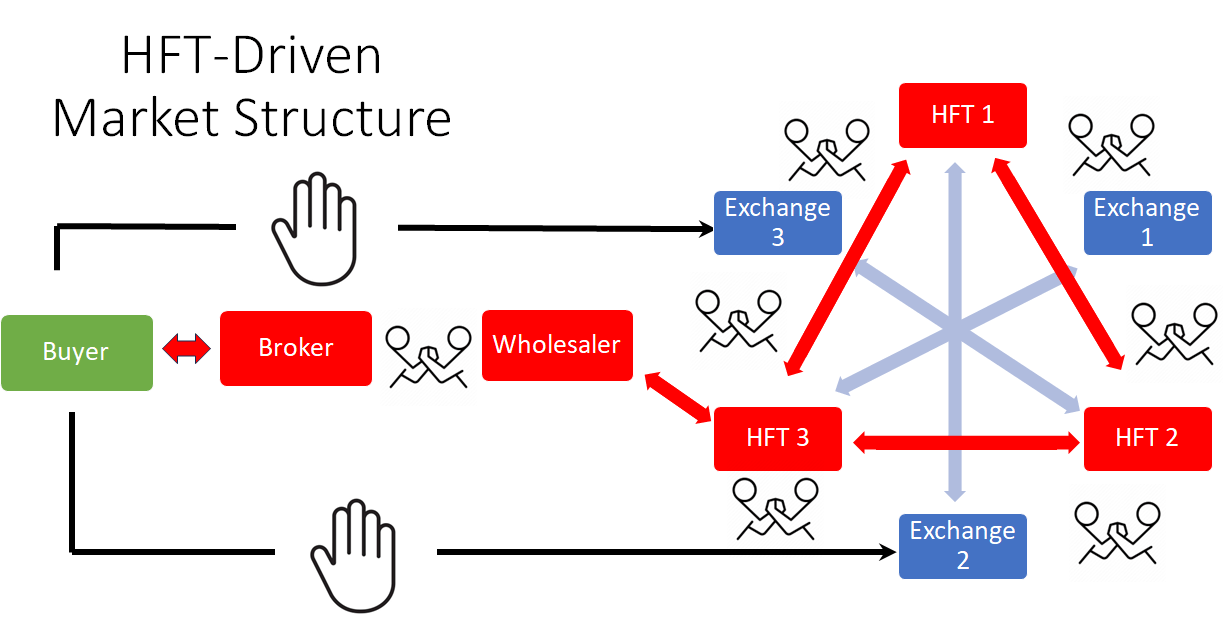

Right now, the retail version of the NMS is so simple that it insults intelligence. An investor places an order with her broker. Her broker hands it off to one of the dominant wholesalers (broker-dealers that specialize in filling retail orders OTC). The wholesaler fills the order at a below-market outsider's price. Then the wholesaler lays off the order for its own account at a better price. Finally, the wholesaler pays the retail broker for giving up the order. The payments to brokers are called Payments for Order Flow (PFOF). No system could be simpler or more abusive to retail.

Computer-driven high-frequency traders (HFTs)

The second group served by the NMS is wholesalers/HFTs. As the markets adapted to electronic trading, the participants most invested in a market structure favorable to themselves were the computerized HFTs. They realized electronic trading created a profitable race to gain a speed advantage. Armed with computer algorithms, HFTs co-located their machines with exchange transaction engines and created a market environment that rewarded the many small-margin arbitrage trades that were their specialty.

{kind=link}

Their network of computers located next to (co-located with) the exchange transaction engines produced a market structure that looked like the system described by the graphic below.

Exchanges

The rise of the HFTs presented the exchanges with a decision. Should they pursue the HFTs, retail traders, or both? Driven by the much higher transaction volume of HFTs the exchanges focused first on HFT needs. Since HFTs conduct arbitrage, that meant adding arbitrage alternatives. So, the exchanges added more exchanges and created new complex orders, both actions intended to generate more arbitrage.

But there was a downside to creating multiple exchanges, complicated orders, and speed-of-light trading. Retail investors and their brokers could not find their way through the resulting chaos safely (in a way that would assure that the retail brokers met their SEC requirement to execute at the best price available). Chaos like this is anathema to retail. Nonetheless, the exchanges decided to cater to the HFTs, leaving retail investors to find another way to complete transactions.

HFTs/Wholesalers

At first, HFT was a bonanza for participating broker-dealers. But as the HFT-generated profits rolled in, the exchange management firms saw an opportunity to capture a share of the HFTs' profits through higher exchange fees. So, arm-wrestling for a share of the arbitrage profit began. Exchanges increased their share of the haul from arbitrage by increasing exchange fees, to the HFTs' dismay.

Meanwhile, the HFTs, always alert to opportunity, saw that they could be the bird dogs of retail, chasing trades through the NMS thicket for retail brokers. So, now a broker passes its retail orders to an HFT in the HFTs' new function, wholesaler retail order execution. The wholesaler fills retail orders at a below-market price - yet not so low as to draw the SEC's attention. A share of wholesalers' profit from off-market prices is passed back to retail brokers to encourage brokers to keep the good times rolling.

But as always with payments not reached at market prices, wholesalers and retail brokers also arm-wrestled for their share of the outsider-insider price spread.

There is the NMS in a nutshell. Retail investors receive outsider prices. Insiders - retail brokers, wholesalers/HFTs, and exchanges - dicker over their respective shares of the difference between the insider prices wholesalers receive and the outsider prices retail receives.

Requirements to build a system for retail traders

According to SEC chair Gary Gensler, the SEC's objectives are to "strengthen competition and ensure individual investors are fairly treated." The SEC must be incredibly uncomfortable with the current system that serves retail investors as an afterthought.

But it would not be difficult to greatly improve retail investor service, technically. The difficult part is finding the will to take this dramatic step. That step won't be taken by the SEC or another regulator. Only a private initiative will work. In what follows I will describe the process from the initial issuance of corporate securities until investors tuck the investment into their holdings.

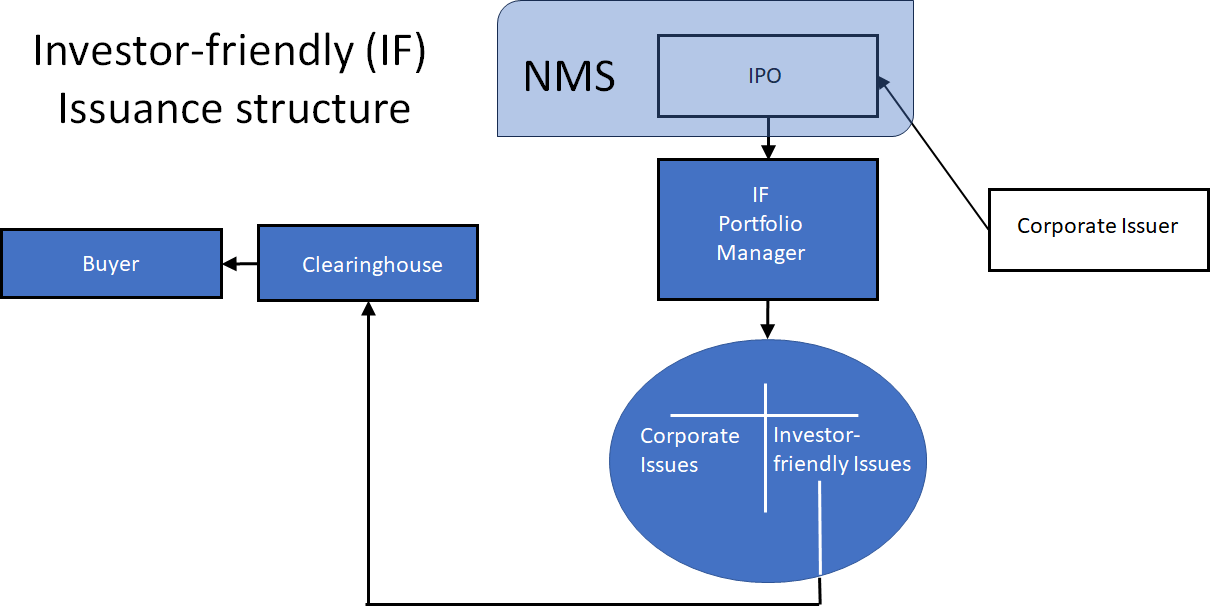

Issuance

Initially, it makes sense to assume that corporate issuance patterns won't change. The dominant IPO providers (NYSE, NASDAQ) will continue in that function. But afterward, it would benefit investors if an investment fund would issue investor-friendly asset-backed securities to be listed by an affiliated exchange.

{kind=link}

The investor-friendly component of market structure

Creation of an investor-friendly market includes devising a way to provide investors with a version of the securities market that includes:

- New securities that are more attractive to investors than corporate original issues.

- A universe of investments less expensive to trade than NMS securities.

- A way of investing that does not exclude investors from insider prices.

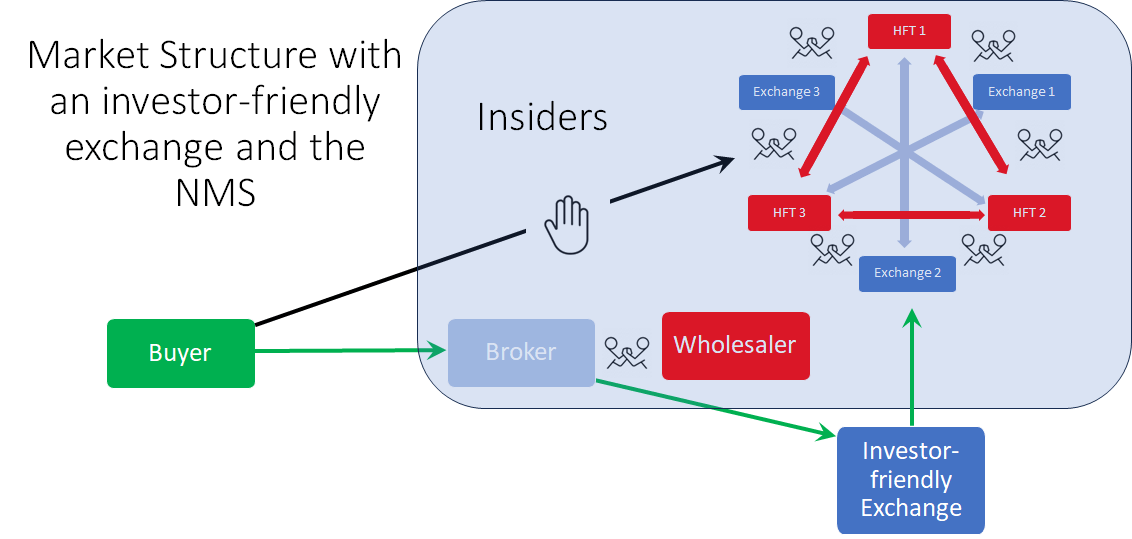

Once a market where every participant faces the same prices is created, and where the market structure is designed to eliminate the expensive aspects of the trading and clearing process that provide value only to broker-dealers and market activists, retail investors need only to specify the retail exchange to avoid the aspects of the NMS designed for other kinds of traders. The retail-friendly market structure is displayed in the graphic below.

{kind=link}

Conclusion

This article builds upon my earlier description of the NMS, the SEC-created market structure that has been co-opted by HFTs and Wholesalers at the expense of retail investors. It summarizes the economic forces that drove the exchanges to cater to the needs of HFT/Wholesalers at the expense of retail investors. It then explains the reasons why the NMS cannot address the needs of retail without innovation from financial market participants. The article outlines some changes that would better meet retail investors' needs. Finally, it names the firms that will be the major winners and losers going forward. The following articles will address retail investment in the market for debt and the likely long-run financial market structure.

For further details see:

Retail Investors' Markets Must Be Simple To Succeed