SITC - Retail M&A Heats Up With Kimco/RPT Merger

2023-08-31 15:07:22 ET

Summary

- M&A activity in the shopping center space is increasing due to the mispricing of the market, creating opportunities for stock-for-stock transactions.

- Kimco's acquisition of RPT Realty is seen as a beneficial deal for both parties, with immediate gains for RPT shareholders and growth for Kimco.

- The next potential targets for M&A in the shopping center sector include Whitestone, KRG, BRX, and SITC, which are trading at attractive implied cap rates.

M&A is on fire in the shopping center space and it is entirely rational. The wildly mispriced market has created spreads which make stock-for-stock transactions obviously accretive. The latest chapter of shopping center M&A is Kimco (KIM) buying RPT (RPT) announced on August 28, 2023.

{kind=link}

One could spot transactions of this nature coming a mile away if they were paying attention to the valuation in the sector.

At the risk of tooting our own horn, we at Portfolio Income Solutions did see it coming.

On May 19 I wrote :

“So long as they are buying other REITs with higher implied cap rates, it is fairly straightforward to make the transactions immediately accretive to AFFO/share.

Thus, the most likely targets are the shopping center REITs trading at the highest implied cap rates.

Ross Bowler also saw it coming and had a prescient article on August 23 discussing the extreme discount at which RPT traded.

In this article, we will discuss two topics:

- The merits of the KIM/RPT deal

- Which companies are next in line to get bought out.

The KIM/RPT deal

Kimco is using all stock to finance the transaction with an exchange ratio of 0.6049 shares of KIM per RPT share. This sort of stock-for-stock buyout makes it a direct comparison between the valuations of the two companies. Since KIM is more expensive than RPT at the agreed upon ratio, it is immediately accretive to KIM on an FFO, AFFO and NAV basis.

The merger price represents a cap rate of just over 8% which is clearly beneficial to both parties. RPT shareholders get the immediate ~20% gain and KIM shareholders get to buy a bunch of properties that should trade at 7% cap rates, at an 8% cap rate.

There is a good amount of property overlap which will yield significant operating efficiencies. KIM already has operations in place for most of RPTs regions which will allow trimming of excess staff and less travel time per property.

RPT’s portfolio had over 20% mark to market and signed-but-not-operating leases which build in some NOI growth in the coming years.

How to play it as a KIM shareholder

There really isn’t anything objectionable about this deal. It will grow FFO/share, AFFO/share and NAV, so if you liked KIM before the announcement, it is even better now.

How to play it as an RPT shareholder

A viable choice might be to just take the gains and move on with RPT up nearly 20% on the announcement. It may also be viable to retain the position and allow shares to become KIM shares. KIM is a solid company, and in my estimation, will slightly outperform the market going forward.

There is a slight arbitrage in the stub period until estimated closing in 1Q24. At current pricing, RPT shares are about 0.8% cheaper than their converted value in KIM.

{kind=link}

That is a fairly small arbitrage spread so I think it is only worth playing if you want to own the KIM shares on a continuing basis after. That said, this merger looks highly likely to go through given the clear benefits to both parties.

The next targets of shopping center M&A

In negotiations there is something called a ZOPA or Zone Of Potential Agreement which is the pricing range in which a deal is beneficial to both parties. Given the extreme variance in cap rates at which the various REITs trade, there is a very wide ZOPA which makes it a fertile landscape for M&A.

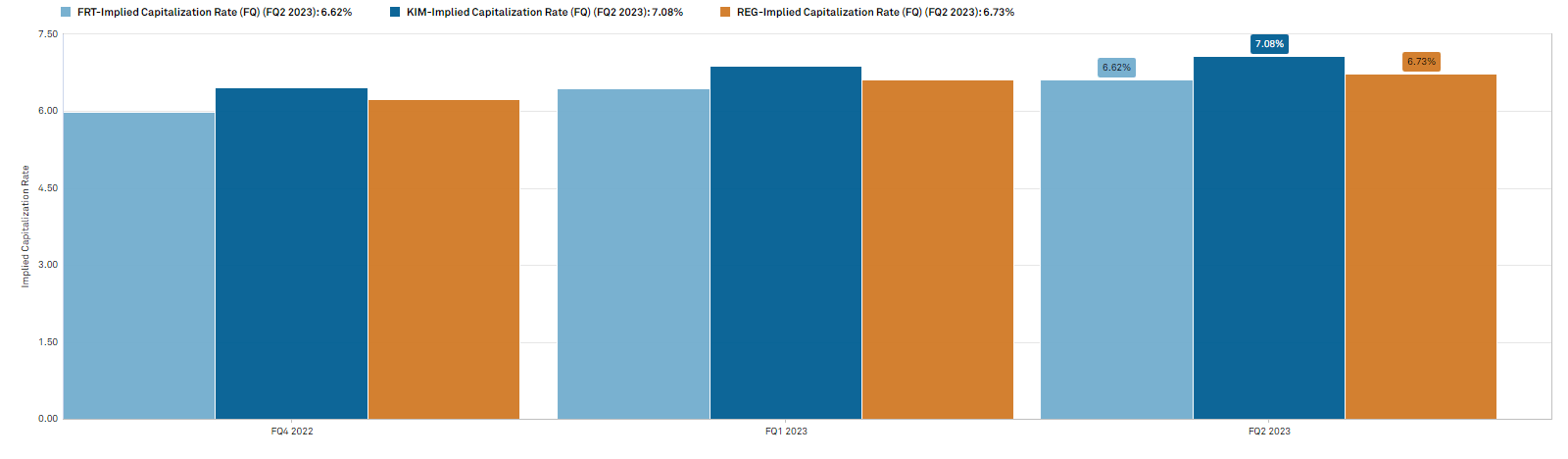

There are three correctly priced shopping center REITs.

- Kimco ((KIM)) - 14.9X 2024 AFFO (FFO may be distorted by Albertson’s stock)

- Federal Realty ( FRT ) - 14.4X 2024 FFO

- Regency Centers ( REG ) 14.5X 2024 FFO

One could even argue that they are somewhat attractively priced as their FFO multiples are not that high given the growth ahead.

However, on a relative basis, their prices are very high compared to the cheap cohort of shopping center REITs.

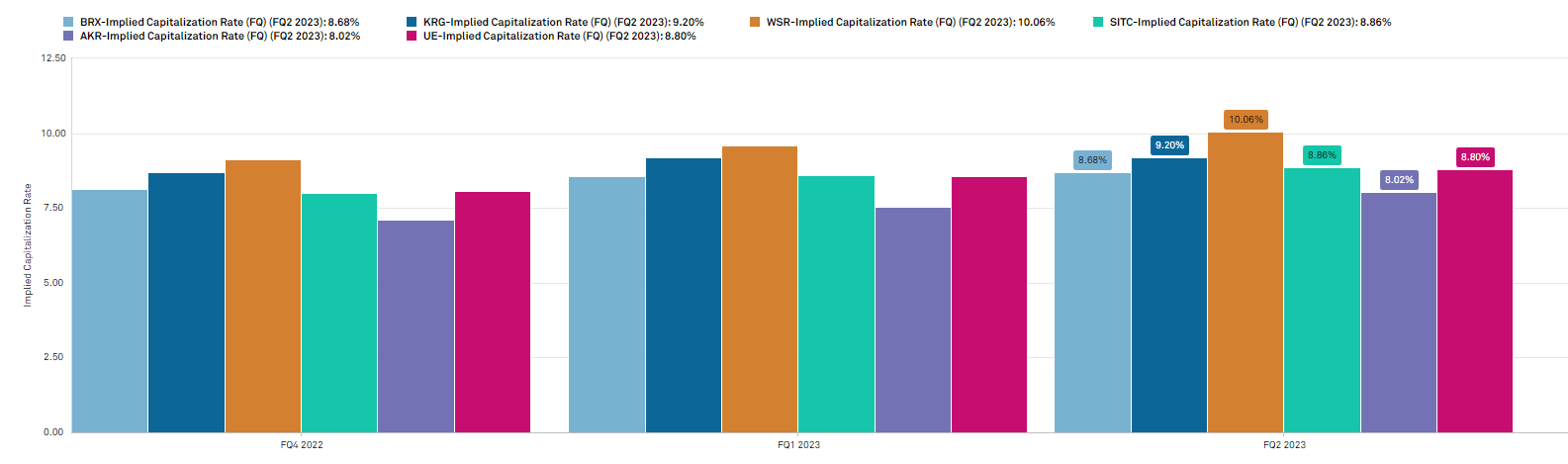

- Brixmor ((BRX)) – 10.2X FFO

- Kite Realty ((KRG)) - 10.6X FFO

- Whitestone REIT ((WSR)) - 9.2X FFO

- SITE Centers ((SITC)) - 10.8x FFO

- Acadia ( AKR ) – 11.5X FFO

- Urban Edge ( UE ) - 12.4X FFO

In general, the cheaper ones are smaller which means the overhead is higher as a percentage of revenues. As such, the property level discount is even larger than the FFO discount. It is the spread in implied cap rates which makes for really easy M&A.

These will be the buyers (KIM and REG already have).

{kind=link}

They are trading at implied cap rates in the 6s and low 7s. For clarity, an implied cap rate is the property Net Operating Income divided by enterprise value.

In other words, the market pricing of these REITs is functionally buying their properties at cap rates from 6.62% to 7.08%.

That strikes me as the correct price. In a lower interest rate environment, these properties should go for 5% cap rates, but there has to be some sort of risk premium over Treasuries.

On the other hand, the growth looks exceptional. Shopping center REITs have 20%+ mark to market which will facilitate rental rate increases for the next five years. Occupancy for the sector should also grow given the paucity of new supply and ample demand with net store openings.

Thus, the growth of the sector makes the 6.5%-7% cap rate range look about right.

The three more expensive shopping center REITs are appropriately priced by the market. The other six are wildly cheap with implied cap rates ranging from 8.02% to 10.06%

{kind=link}

Just as Kimco scooped up RPT at an 8% implied cap rate, any of the three low cap rate REITs could acquire any of these six.

In my opinion, AKR is less likely to get bought out due to the locations and types of its properties being different from those of the buyers. AKR focuses on walk-up shopping centers in high population density areas. In the long run this could be phenomenal real estate, but right now it is disproportionately being hurt by the boom in organized retail theft.

I think the most likely targets of M&A are:

- Whitestone with the highest implied cap rate of 10.06% makes for the widest zone of agreement

- KRG and BRX with their heavy grocery anchored concentration makes their portfolios accretive to the quality of buyers

- SITC has significant property overlap with potential buyers and has similar properties.

Mispricing of the sector

Retail and specifically shopping centers are quickly surpassing industrial as the best real estate type. The market tends to overly focus on demand and not enough on supply.

So the market is seeing the still high demand growth of sectors like industrial and data center and is trading those at higher multiples. Missing in the market’s viewpoint is the supply side of the equation.

Both industrial and data center have heavy development activity. There is enough demand growth to absorb the supply so I think the sectors will be fine, but it is relatively balanced.

In shopping center, there is virtually no net supply so the store openings (net of closures and things like BBBY) will represent true occupancy growth. Occupancy for the sector is already at the highest point in over a decade and it is crossing that dangerous threshold where landlords start to get pricing leverage over tenants.

This is not a sector that should trade anywhere near as cheaply as it does and I think there are two paths to realizing the value.

- The market catches on and starts to trade them at appropriate multiples

- The spread remains and M&A continues at a rapid pace. The buyers are essentially recognizing the value in place of the market.

I find shopping centers to be one of the best opportunities in the market right now and we are significantly overweight the sector at Portfolio Income Solutions.

Why not go even more overweight?

I am a big fan of diversification. Even the best ideas are susceptible to unforeseen risks and there are potential risks on the horizon.

In particular, I think the market is underestimating the risk of student loan interest kicking in. Most are measuring the impact to retail spending as being about equal in magnitude with the interest rate payments which would not be all that big of a deal.

I suspect there will be an additional impact from behavioral change. A sudden realization of debt that inspires a general tightening of purse strings.

Summary

The M&A in the shopping center space has been very clean. Good, honest transactions that are beneficial to all parties involved. If the mispricing persists in the sector there will be more M&A ahead.

For further details see:

Retail M&A Heats Up With Kimco/RPT Merger