ROIC - Retail Opportunity Investments: ROIC Is A Perfect Name For This West Coast Gem

2023-11-23 08:10:00 ET

Summary

- Retail Opportunity Investments Corp. stock has underperformed the Vanguard Real Estate Index ETF in the past year.

- It owns shopping center properties along the West Coast with a high leased rate, and the majority of tenants are e-commerce resistant.

- ROIC is materially undervalued compared to both its historical valuation as well as that of its peers.

REITs in general have seen a decent bounce as of late, as fears around higher interest rates have subsided , with the market now anticipating the potential for lower rates next year and beyond. However, the recovery has been rather uneven, as some REITs are still down well below the market average.

This brings me to Retail Opportunity Investments Corp. ( ROIC ), which I last covered here back in September 2021 with a 'Buy' rating, noting its mixed-use potential and quality portfolio along the West Coast. That seems like a long time ago, back when interest rates were near historic lows, and the stock has declined by 31% since my last piece (-23% total return including dividends).

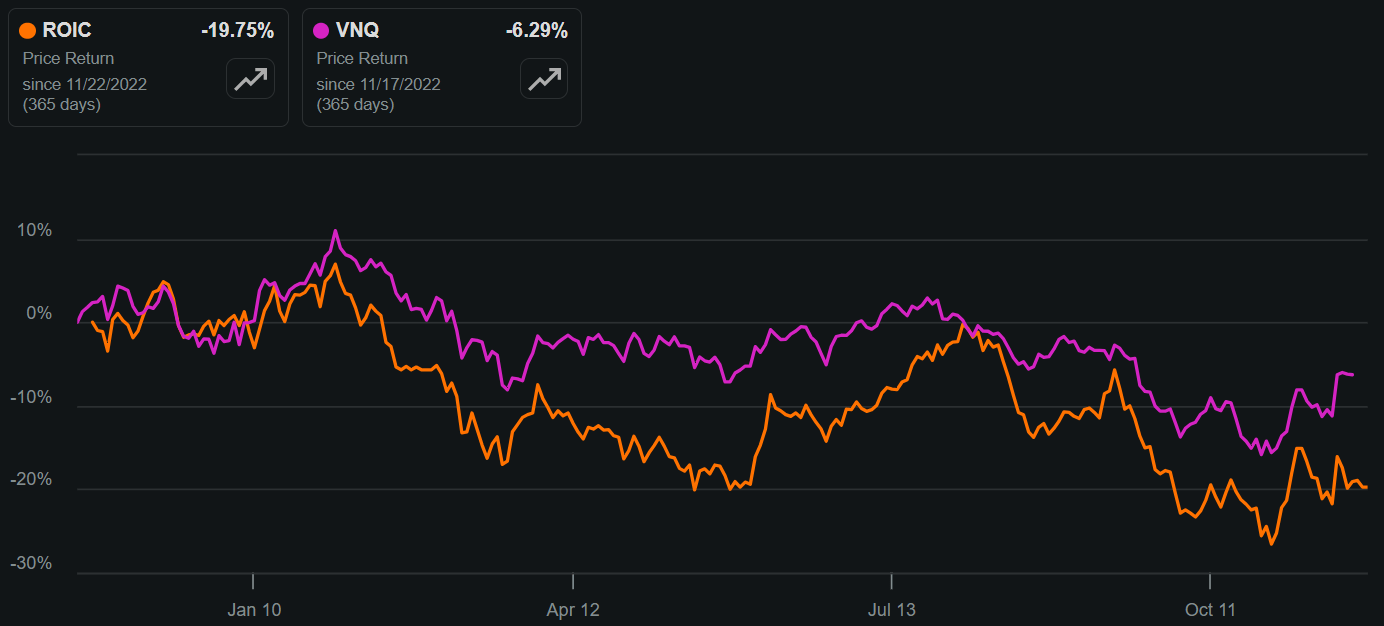

ROIC has also underperformed the Vanguard Real Estate Index ETF ( VNQ ) with a 20% price decline compared to VNQ's 6% decline over the past 12 months, as shown below. In this piece, I discuss income and value investors may be interested in ROIC at the currently discounted price for potentially strong returns from here, so let's get started!

{kind=link}

ROIC vs. VNQ Price Return (Seeking Alpha)

Why ROIC?

ROIC in the finance world is an acronym for 'return on invested capital, and is perhaps a fitting ticker symbol for this internally-managed REIT, which owns shopping enter properties in densely populated regions along the West Coast of the U.S. At present, ROIC owns 93 properties covering 10.5 million square feet in California, Oregon, and Washington State.

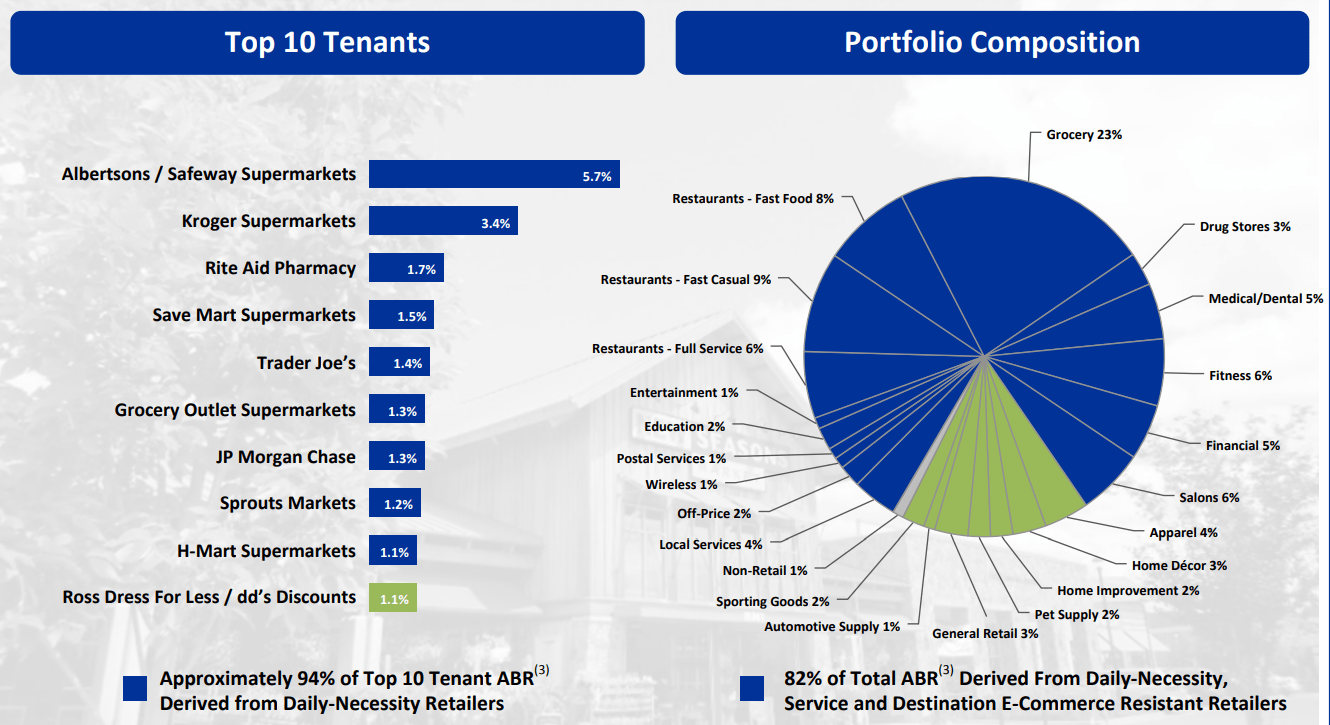

ROIC's portfolio quality is demonstrated by its ability to maintain a high leased rate of 96%+ over the past 10 years including during the pandemic, a feat that's unmatched by its peers. In addition to having properties being in close proximity to high income population bases, the majority (82%) of ROIC's annual base rent stems from daily necessity based tenants that are e-commerce resistant. As shown below, Grocery, Restaurants, Medical/Dental, Fitness, and Financial (banks) make up over half (54%) of ROIC's total ABR.

{kind=link}

Investor Presentation

Meanwhile, ROIC currently enjoys a historically high portfolio leased rate of 98.2% and the end of Q3 this year, which is 40 basis points higher than that of the prior year period. Market demand for ROIC's properties is also high, helping to drive 8.2% YoY growth in same store net operating income. This represents an acceleration from the first half of the year, considering that ROIC's 9-month same-center NOI growth is 3.6%. Q3's higher SS NOI growth was driven by impressive 36% cash rent growth on new leases and 7.2% growth on renewal leases.

While higher interest rates have pressured the real estate industry in general, those who are better capitalized are positioned to benefit from higher leveraged owners seeking to liquidate their holdings. This dynamic is reflected by management seeing several opportunities in private sellers seeking to transact, including one in Los Angeles in a densely populated mature community with a nationally-recognized grocery anchor tenant.

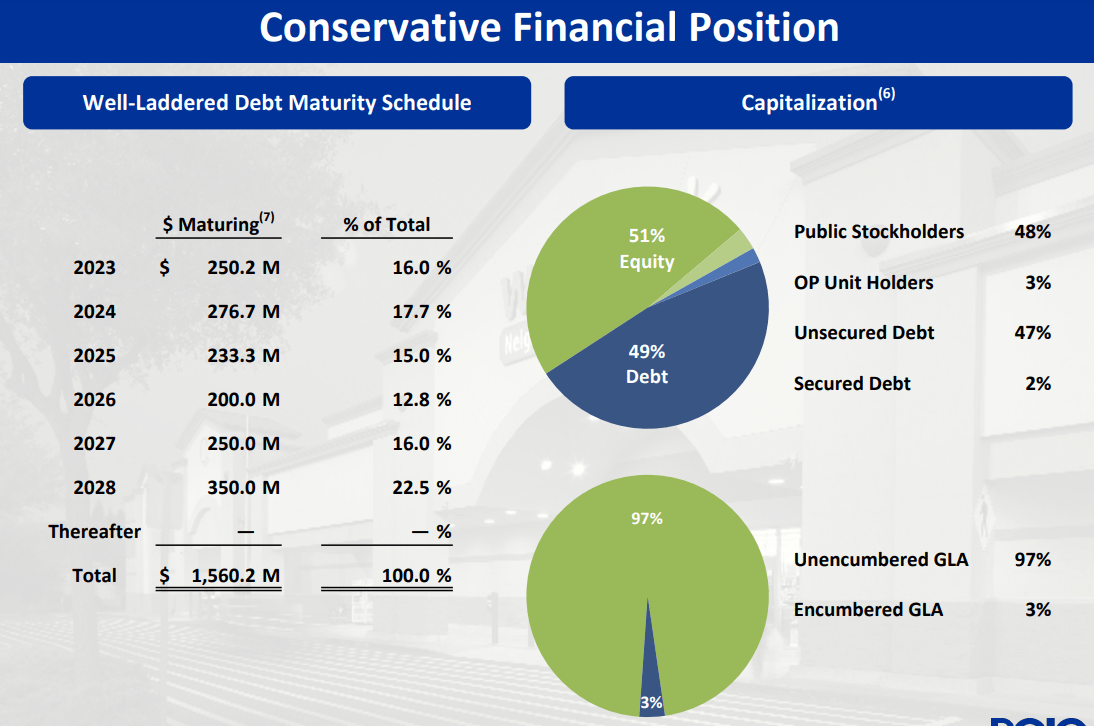

Acquisitions in the near term could be supported by ROIC's recent raising of $350 million in debt in September due in October of 2028, with a 6.75% interest rate. ROIC is also modestly leveraged, with a net debt to EBITDA ratio of 6.4x, sitting slightly above the 6.0x generally considered safe by ratings agencies, and carries a BBB investment grade credit rating from Fitch (BBB- from S&P).

ROIC's recent debt capital raise is also more than sufficient to repay $250M worth of debt maturing this year. While ROIC has more debt maturing next year, its annual debt maturities are well balanced and staggered, thereby reducing material interest rate risk in single given year.

{kind=link}

Investor Presentation

Risks to ROIC include higher interest rates, which would increase its cost of debt when it comes time to refinance. However, as noted earlier, market fears around higher interest rates have now subsided and investment banks UBS ( UBS ) and Goldman Sachs ( GS ) both predict the Federal Reserve will cut rates next year, with UBS believing this will happen in the first half of next year, and Goldman believing that cuts will happen in Q4 next year.

Other risks include potential for a recession, which may inhibit ROIC's ability to raise rents, and ROIC low share price, which means that equity raises are not a viable option to fund external growth. At the current price of $12.21 with forward P/FFO of 11.5, ROIC's cost of equity is 8.7%, which represents a high hurdle rate for initial cash yields on acquisitions. As such, external growth may be muted in the near term so long as the share price remains low.

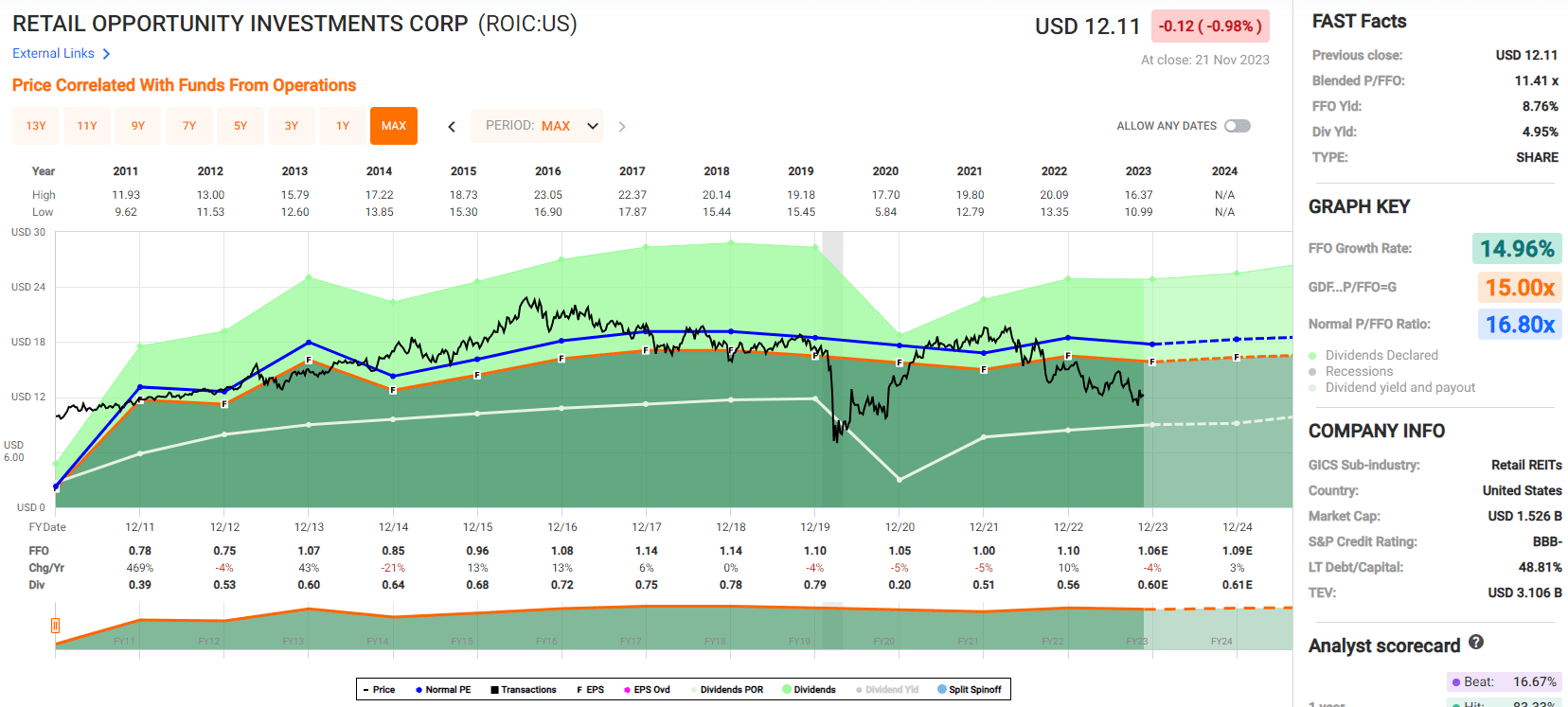

Nonetheless, investors buying into ROIC at the present valuation get to take advantage of the low price while getting paid to wait, with a 4.9% dividend yield that's well-covered by a 57% payout ratio, setting up ROIC for dividend raises down the line should interest rates stabilize or go down. As shown below, ROIC's blended P/FFO of 11.4 sits materially below its historical P/FFO of 16.8.

{kind=link}

FAST Graphs

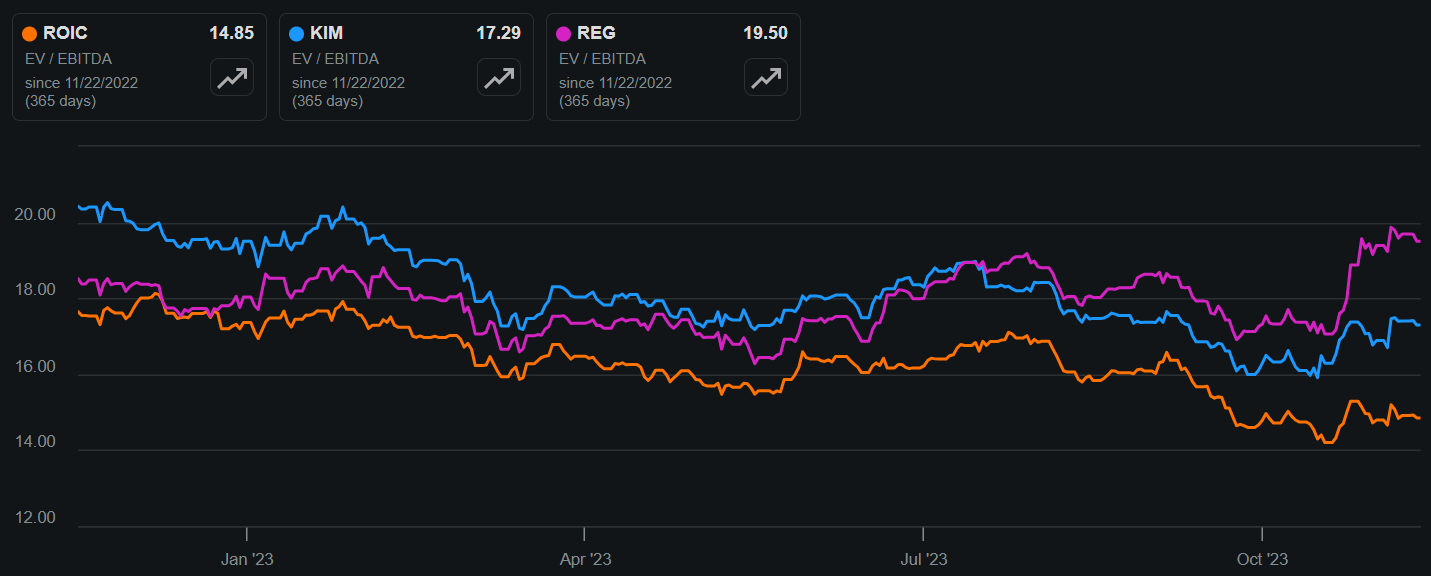

ROIC also carries a materially lower valuation than its larger peers, Kimco Realty ( KIM ) and Regency Centers ( REG ), despite having a similar quality portfolio of grocery-anchored centers in population dense regions and having high cash rent growth. As shown below, ROIC's EV/EBITDA of 14.9 sits below that of these two peers.

{kind=link}

ROIC vs. Peers' EV/EBITDA (Seeking Alpha)

Investor Takeaway

ROIC is a high-quality shopping center REIT that's currently facing short-term headwinds due to market fears around interest rates and an external growth hurdle rate made high due to its low share price. Nonetheless, ROIC makes for a good buy at the current price with investors getting paid nearly 5% while waiting for potential positive catalysts to materialize in the form of meaningful cash rent growth from strong tenant demand and deployment of debt proceeds into new acquisitions. As such, income and value investors seeking an undervalued quality REIT may want to consider ROIC at its current discounted price. Reiterate 'Buy' rating.

For further details see:

Retail Opportunity Investments: ROIC Is A Perfect Name For This West Coast Gem