WSR - Retail Real Estate Is Entering A Golden Age

2023-08-07 19:56:21 ET

Summary

- Retail REITs have been undervalued due to past weaknesses, but the environment has changed in favor of retail real estate.

- Negative net supply growth and increasing retail sales create a significant runway for rental rate growth.

- Within the sector, we identify individual REITs with superior growth potential, superior locations, and superior management.

Most people, including professional investors, tend to underperform the market. I think much of the error comes from extrapolation of history - Looking at what was in favor rather than looking at the future. We should know the history and learn from it, but it is far from the best estimate of the future.

I propose a different approach – looking at forward fundamentals to ascertain what is about to be in favor.

Retail REITs (real estate investment trusts) trade very cheaply at 12.6X FFO (funds from operations) because they have been out of favor for the greater part of a decade. Retail was oversupplied and lost substantial market share to e-commerce which exacerbated the supply issue. Tenants had all the negotiating power resulting in rent as a percentage of retail sales dropping across all retail property types, in many cases getting to the mid-single digits.

That 12.6X FFO multiple reflects the bout of weakness, but it is often darkest before the dawn and the environment has drastically changed in favor of retail real estate. Specifically, there are 3 changes of note.

- Negative supply growth

- Retail sales growth

- Valuation is at a highly opportunistic level.

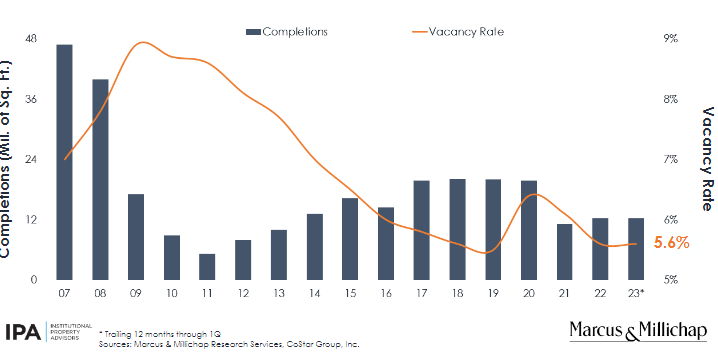

Negative net supply for 15 years

According to Cushman and Wakefield, there are 14.2B square feet of retail in the U.S., 5.4 billion of which is shopping centers. Real estate generally needs 1%-2% of existing supply to be built each year to maintain the same amount of square footage.

However, over the past 15 years, construction completions of retail real estate have averaged around 12 million square feet.

{kind=link}

That is just a fraction of a percent of existing inventory.

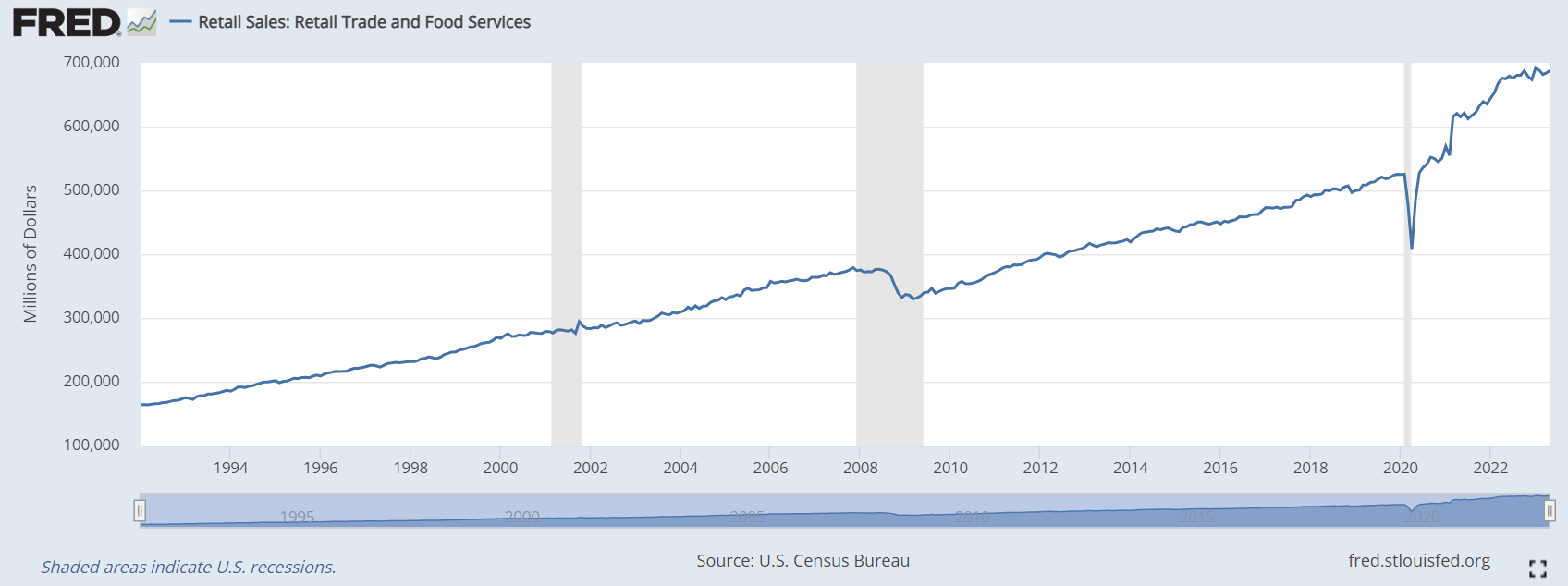

Inclusive of demolitions and repurposing, net supply growth has been significantly negative. At the same time, retail sales have been growing significantly.

{kind=link}

As a result, the sales per square foot is a multiple of what it used to be. The ratio of sales to rent is referred to among retail REITs as occupancy cost.

It used to be in the mid-teens, as in rent was somewhere in the vicinity of 15% of sales. It varies by property type and location of course, but it was somewhere around that number.

Today, it is much lower. Retail rents have only minimally increased while retail sales have doubled in the last 15 years. Many shopping centers now have rent as a percentage of sales in the mid-single digits.

That is far below equilibrium and creates a significant runway for rental rate growth.

So far, the landlords have not been able to push rents up to the equilibrant level because low occupancy made it more important to keep as many tenants as possible rather than to chase higher rent.

Today, however, occupancy for the shopping center REIT sector has reached a mean of 94.25% which is at a key threshold.

With an occupancy above 94%, negotiating power starts to shift in favor of landlords. Rather than landlords competing for the good tenants, the scarcity of good retail space forces the tenants to fight over the good locations. Landlords get to raise rents and we are starting to see hints of this in the retail REIT 2Q23 earnings reports

- Kimco Realty Corporation ( KIM ) new leases sighed at 25.3% increase with renewals up 7.6%

- Whitestone REIT ( WSR ) had GAAP leasing spreads of 32.2% on new leases and 16.2% on renewal leases

- Kite Realty Group Trust ( KRG ) reports that it “ Leased over 1.3 million square feet at 14.8% comparable blended cash leasing spreads”

- Brixmor Property Group ( BRX ) reports that it “Executed 1.4 million square feet of new and renewal leases, with rent spreads on comparable space of 15.4%, including 0.6 million square feet of new leases, with rent spreads on comparable space of 22.4%.”

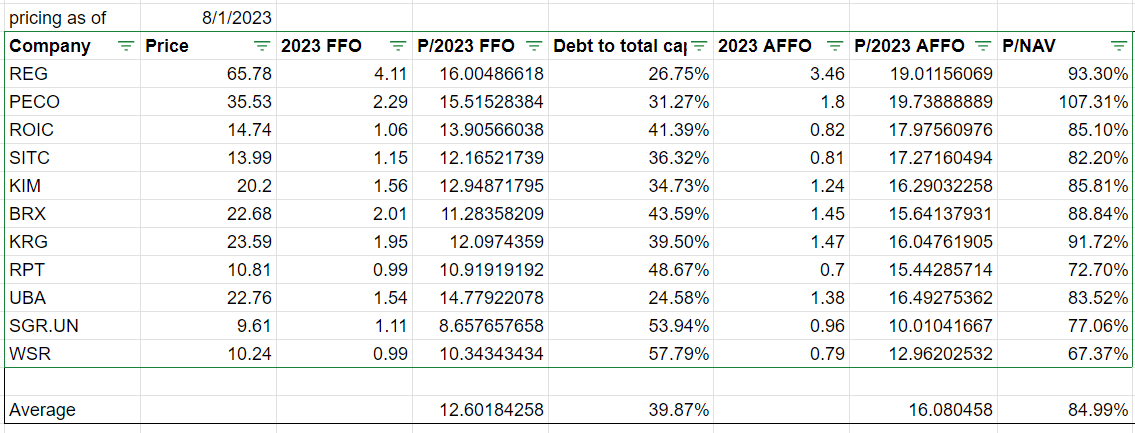

These are excellent numbers that are not often observable in a sector that trades at 12.6X 2023 estimate FFO and 16.1X 2023 AFFO.

{kind=link}

Early innings of growth

Due to the long lease terms in real estate, leasing spreads such as the ones discussed above are not reflective of a year over year change in market rates, but rather a comparison of the now current market rate to that of the weighted average of the vintage of leases coming due.

Thus, when prevailing rental rates move, it can take 5 to 15 years to fully filter in to the rental revenue.

For retail, the positive move in rental rates is a new thing which implies they will have favorable roll-ups on leases for the next decade.

Beyond the market rates taking a while to roll into the leases, I anticipate market rates to rise substantially over the coming years based on the dynamics we discussed above.

- Occupancy hitting a critical threshold which shifts power to landlords.

- Current rent as a percent of sales is below equilibrium.

- Lack of new supply.

It is the 3 rd factor that differentiates retail from the other REIT sectors.

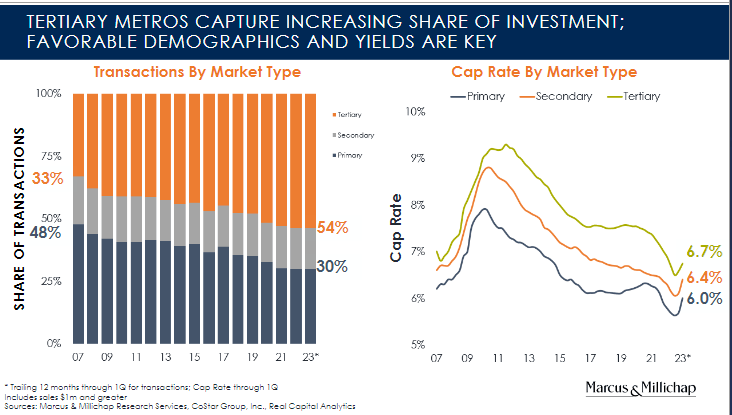

Industrial, apartments and self-storage have been hot for a while now (not necessarily in market price of the stocks, but in terms of actual fundamentals).

This fundamental success enticed significant development of new supply. You can see on the curves below that each of these sectors has had a significant upward curl to vacancy as this supply started to really get delivered in 22 and 23.

Marcus and Millichap

Retail, however, has not had the same supply boom. It is experiencing similar demand trends but because its fundamental resurgence is more recent the supply has not started yet. I also believe it will be many years before material construction begins due to construction costs being higher than public market valuations. In a recent article we dove into this further as the REITs are trading at higher implied cap rates than you can get by developing.

Thus any capital that would normally go to development is better suited buying the REITs. It will be a few more years before retail supply starts to catch up with the demand wave.

That suggests that retail market rental rates will continue to tick up. The gap between current rents and market rents will grow resulting in increasing leasing spreads as time goes on. That is the kind of fundamental momentum investors want to see and I think it will lead to significantly higher FFO multiples for the sector.

In my opinion, it is a great sector in which to invest presently, so let us dig into which REITs are the best positioned within retail.

A mono-dimensional pricing schema

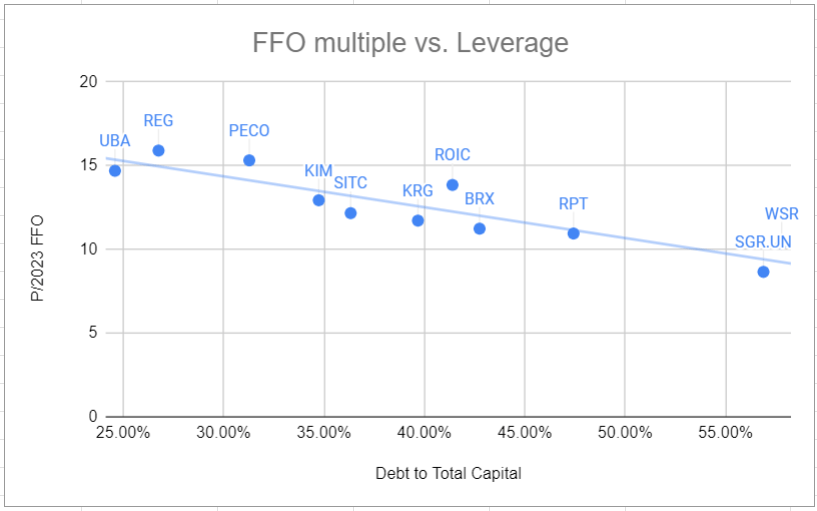

Right now, the market is so terrified of what it terms “commercial real estate debt” that debt seems to be the only metric it cares about.

I frequently plot FFO multiples against leverage ratios as a means of viewing valuations in a leverage neutral fashion, but this is the first time I have seen valuations fit on the trend line so neatly.

{kind=link}

With FFO multiple on the Y axis and leverage on the X axis the market is precisely valuing the REITs based on their leverage level - The higher the leverage the lower the multiple.

While that is the correct mathematical relationship, it just strikes me as strange that this is the ONLY factor influencing market pricing.

The market is valuing these REITs in a fashion that is agnostic to:

- Property location

- Property quality

- Forward growth

- Management integrity and skill.

That means we can buy any of the retail REITs without having to pay for the quality. One can upgrade from poor quality to high quality on equal leverage neutral valuation.

We can get extra growth without paying for it.

Superior Growth

Kite Realty is experiencing strong growth driven by hitting its key occupancy level in the mid-90s, which is translating to rental rate growth. From 2021-2024 FFO is expected to go from $1.50 to $2.03 and AFFO from $1.34 to $1.59

{kind=link}

Note that this is over the course of time in which interest expenses shot up. KRG’s growth was sufficient to have about 35% net FFO growth despite the increased expense. I think it will grow the bottom line faster than peers for the next few years.

Superior locations

Whitestone REIT has the best located retail portfolio in my opinion.

{kind=link}

Not only are its submarkets high household income, but the population growth and job growth in these cities is phenomenal.

These submarkets have similarly strong demand drivers for apartments and industrial but the incumbent real estate of those types is not necessarily benefitting because these markets are also being flooded by development. So for industrial and multifamily Phoenix and the Texas triangle are only okay whereas retail gets to enjoy the same demand boom but without the supply.

More people and more money divided across the same amount of retail square footage. Sales per square foot is rising rapidly and I think rents will as well.

Superior management

In my opinion, Brixmor has the best management in the shopping center space. They consistently position intelligently based on what is opportunistic at the moment.

BRX bought a bunch of secondary market locations when the spreads between primary and secondary markets were huge. Since that time, the spread has narrowed to only 40 basis points.

{kind=link}

Properties across the board appreciated, but Brixmor’s appreciated significantly more due to greater compression between purchase cap rate and current cap rate.

For the last few years BRX has been playing defense with heavy disposition volume. This took advantage of the dislocation in which private market property values were high and the REIT prices were low.

In 2023, BRX is going back on offense because acquisitions once again make sense. Sellers have come to terms with moderately higher cap rates in the higher interest rate environment and the spread is now big enough to make it accretive on a per share basis.

I just really admire the discipline they have to grow only when it makes sense.

Additionally, BRX has a bit more occupancy upside than the rest of the sector. Anchor occupancy is 96.2% while small shop occupancy is 89.4%. That is a great mismatch because it is the anchors that drive the traffic while the small shops bring in a bigger rent per foot. With grocery anchors already in place it should be fairly easy to bump occupancy on small shops up to 93%-95%. So that is about 400 basis points of occupancy gains on top of the rental rate growth.

Wrapping it up

I still like all 3 of these REITs (KRG, WSR, and BRX). Urstadt Biddle Properties Inc. (UBA) no longer looks attractive to me simply due to it being bid up to its buyout price with only a tiny arbitrage spread remaining.

The sector is likely heading for a long upswing as healthy demand coincides with a dearth of new supply. Valuations are opportunistically low as investors are still focused on retail’s former weakness rather than looking ahead.

For further details see:

Retail Real Estate Is Entering A Golden Age