JOAN - Retailer JOANN May Not Go Bankrupt But It Is Still Not A Buy

2023-08-16 16:17:27 ET

Summary

- Retailer JOANN continues to burn cash as sales keep declining.

- They carry way too much debt compared to their operating results.

- There is a risk that the stock might be delisted.

- They are still operating without a CEO.

- Leonard Green & Partners, their largest shareholder, might be able to keep them out of bankruptcy court.

Sewing, arts and crafts retailer JOANN Inc. ( JOAN ) might already be in Ch.11 if it were not for the positive impact the pandemic had on this financially distressed retailer. The surge in demand for their products by consumers who were forced to stay at home resulted in a short-lived turnaround that allowed them to have an IPO in March 2021 at $12 per share. Their CEO left in May. While their recent results are very weak, I don't think they will file for bankruptcy and just "bounce around" on the bottom for a while until there is a severe recession and/or vendors force them into Ch.11.

Very Highly Leveraged

An interesting metric when looking at financial leverage is comparing current equity capitalization to total long-term debt. JOAN has a current equity capitalization of only about $47 million compared to total gross long-term debt of $1.053 billion. That is a ratio of over 22 to 1. That is a lot of leverage. This of course is using the carrying value of their debt and not the market/fair value. According to their 10-Q the "fair value" of their 2028 $655.7 million term loan is only $353.3 million as of April 29, 2023, for example.

Long-Term Debt

{kind=link}

Another related metric I like to look at when considering high financial leverage is pre-tax interest expense per share. JOANN had $25.3 million interest expense in the last quarter with a weighted average interest rate of 8.74%, which is up from 4.62% in the prior year, so it is fairly likely their annual interest expense could be at $100 million this fiscal year, especially since interest rates have gone up since earlier this year. (Their loans are all variable rates.) Using that $100 million number, their pre-tax interest expense per share is $2.42. This compares to a current JOAN share price of only $1.13.

Their total debt to adjusted EBITDA was 4.8x to at the end of 1Q. There were also a number of changes made in March to their amended credit facility.

Retail Operations

JOANN was struggling before the pandemic but got a major shot in the arm because people who were forced to stay home needed some new activities to alleviate their boredom. They also were making their own masks with sewing machines and fabric bought at JOANN stores. In many jurisdictions their stores were allowed to stay open because what they sold was considered "essential". If their stores would have been closed, I believe JOANN most likely would have gone into Ch.11 bankruptcy in 2020.

The stores are filled with a huge selection of products with females as their primary target consumer. Below is the recent revenue breakdown:

{kind=link}

Part of their problem going forward might be their product mix. It seems, based on comments made during prior conference calls, they are reducing seasonal items, which often need to be drastically marked-down postseason. In addition, they are focusing more on their own brand names. (I also wonder if vendors get much stricter with their terms if JOANN will buy from vendors based on their terms and not primarily what the consumer wants.) This could be a risky change - just ask Bed Bath & Beyond ( BBBYQ ) who changed their product mix to more store brands and away from brands consumers actually want. While this is a typical method used by retailers to reduce costs, it reverses the business model. Instead of focusing on what the consumer wants/demands it becomes what the retailer wants to sell mostly because of cost/mark-up factors.

Recent Results

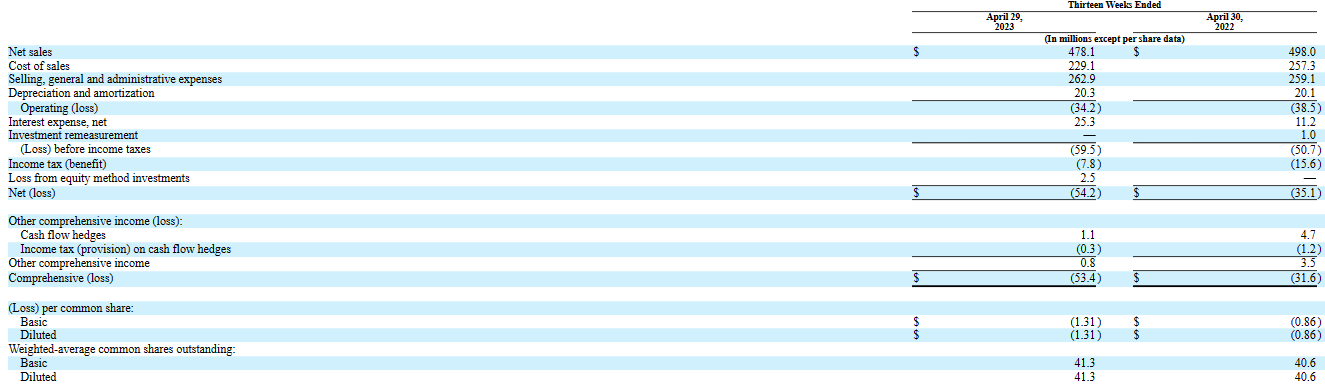

Their 1Q results continued to weaken. The reduction in operating loss was because of the recent sharp decline in ocean freight rates and not because of some internal operational improvement. They also continue to burn cash of $33.8 million from operating activities in 1Q.

First Quarter Income Statement

{kind=link}

Many of their new consumers during the pandemic have returned to their pre-pandemic areas of interest and stopped sewing. (It is too boring and requires too much focus.) Management in their 2021 S-1 IPO registration statement had high hopes for these new customers, but that has not happened. For fiscal year 2024 management stated during their conference call they expect revenue to be down 1%-4% for the 53 week period compared to 52 weeks in the 2023 fiscal year. This implies an effective decline of 3%-6%. With many of their customers now being required to start paying again in October on their student loans this could hurt their sales more than they project, in my opinion.

The disappointing results over the last two years has resulted in the stock dropping sharply from the $12 March 2021 IPO price. Actually, there was a certain amount of weakness already prior to the IPO because the original indicated price was from $15-$17. Leonard Green & Partners sold some of their shares and the company also raised $77 million of cash used to pay down debt. Leonard Green is currently way under water on their JOANN investment because they bought the retailer for about $1.6 billion in early 2011.

Short Squeeze - Unlikely

Meme traders often target low-priced distressed companies for their irrational trading. While the current short interest of about 19.8% of the float seems to make JOANN a potential short squeeze target there is a massive number of potential shares to be sold overhanging the market. The latest short interest compared to the total number of shares outstanding is a modest 5.3%, which is not enough to trigger any short squeeze, and the current borrow rate is about 20%. Leonard Green owns 27,886,637 shares according to their latest proxy (28,344,623 according to a June 29 13D ) of the 41,176,486 shares currently outstanding. Leonard Green could, in theory, sell a modest amount under Rule 144 and potentially could sell all of that large holding under a more traditional underwriting. If they sold any, however, the idea that the major insider is selling could cause a sharp stock price drop. In addition, the company itself could sell shares because 200 million shares are authorized. I was actually expecting a new stock offering in late 2022 to raise needed cash to pay off debt, but it never happened. Now with the stock at only $1.13 that opportunity may have slipped away.

Net Operating Loss Value

There is not really any significant "value" in their net operating losses - NOLs. They have $122.3 million NOLs, which is about $3 per share. Using the 21% tax rate that gives a "value" of $0.63 per share. You need, however, to use the present value of that amount and that is where this gets tricky. It could be a long time before those can be used because they currently do not have taxable profits. While their NOLs should be considered, they are not a major factor in determining a valuation for JOAN stock.

Potential Delisting

Another problem that could impact JOAN stock price is a potential delisting from the Nasdaq Global Market. The market value needs to trade above $50 million for at least 10 consecutive days and the publicly owned amount of JOAN needs to be over $15 million for 10 consecutive days before January 16, 2024 or it will be delisted. By my calculations JOAN needs to be above $1.214 for 10 days and I don't think they achieved that during the last two weeks. It does not seem, by my calculations, that they got the full 10 consecutive days. They still have until January 16.

Long-Term Outlook

JOANN operates a niche retail chain store operation that could be very viable without their massive interest rate payments and with proper management. If they did not have to pay the $25.3 million interest expense in 1Q their negative operating cash flow would have been reduced to $8.5 million. With dynamic management, they should have been able to have positive cash flow. Without a CEO at the present time, this is not going to happen in the near term. JOANN has had a number of "less than dynamic" CEOs over the years. Jill Soltau, for example, was CEO before she went over to be CEO at JC Penney and "drove" JCP into Ch.11 bankruptcy court.

Conclusion

The stock price could see a nice "pop" if they are able to recruit a top-rated CEO, but that rise could be short-lived because the reality is that they are carrying way too much debt on their books compared to their operations. While I think Leonard Green might become "creative" in trying to keep JOANN out of bankruptcy court in order to protect their investment, they need to drastically reduce debt/interest expenses to stay out of court.

I don't think a short squeeze by meme traders is a realistic expectation because of the massive amount of new stock that could come on to the market. With sales declining and their very high debt amount, I rate JOAN stock a sell. There are other more attractive trades than buying JOAN stock.

For further details see:

Retailer JOANN May Not Go Bankrupt, But It Is Still Not A Buy