RVP - Retractable Technologies: What Are We Buying In This Niche Operator?

Summary

- Retractable Technologies continues to realize negative distribution of returns, with price action and volatility skewed to the downside.

- Chief investment debate is the company's revenue recognition ex-US Government looking ahead.

- The question then turns to exactly what are we buying in RVP.

- Here we dive deeper into this relatively opaque company that saw tremendous upside on the chart in FY20.

- We rate shares neutral until further clarity can be obtained on the above.

Investment Summary

Safety syringe company Retractable Technologies, Inc. ( RVP ) has been somewhat of an uncompelling story over the past 12 months on the chart. With a series of structural headwinds in situ, investors continue to seek clarity on this relatively opaque name. Here we give investors insight into what they are buying in RVP, and note shares look to offer a lack of upside/downside capture without further clarification on its revenue recognition ex-US Government. These points in mind, we rate RVP neutral.

RVP 6-month price action

{kind=link}

Data: Refinitiv Eikon

Risks to investment thesis

Investment in small-cap equities carries with it inherent risks due to the volatility and magnitude of potential moves to the upside/downside. Holding a neutral stance, our thesis is at risk of both upside and downside risk, if there is heavy buying or selling activity respectively. Price sensitive news in this space is likely to cause swings in price that may nullify our investment thesis, as fundamentals may become dislocated from market technicals. This must be kept front of mind for investors reading this analysis.

Q2 earnings recap

Sales of $14.3 million ("mm") were down 66% YoY from $42.5mm the year prior. COGS margin was up 21 percentage points to 68% on the lower revenue volume at $9.78mm, and gross profit was down similar amounts YoY to $3.7mm when factoring in royalty expenses as well.

Geographically, domestic sales made up ~67% of sales, down from 94.4% the year prior, driven by reduced revenue volume from the US government agreement. This remains a key risk to the company looking ahead. As a bright spot, domestic unit sales still increased ~80% YoY and made up 51% of domestic sales, whereas overall unit sales were up 64% in volume. Meanwhile, on a YTD basis, international revenues were up c.97.5% YoY to $904,000 from increased vaccination turnover despite narrowing by more than 50% YoY.

Meanwhile, net loss came in at $3.6mm from a $10.6mm profit last year at the bottom line, narrowing earnings from $0.31/share to a loss of $0.11/share. This stemmed from a loss from operations of $2.1mm as revenues dwindled and per-unit cost has increased YoY.

Meanwhile, the company also announced it will trim its headcount by ~16% following the completion of recent facility expansion efforts. The haircut is estimated to result in annualized savings of a~$2.1 million or 13% in annual payroll expense of $16mm. Hence, new labor costs should be ~$14mm. The reduction in labour cost will also reduce capital intensity and brings the capital intensity ratio down from 1.82 to 1.59; meaning it will need to spend ~12% less to generate $1 of revenue looking ahead.

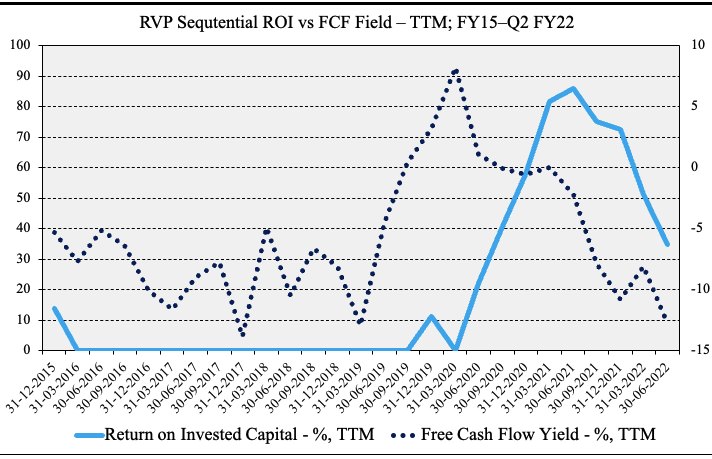

As seen below, the company's capital intensity has changed over time. From Q2 FY19–FY20, FCF yields gained as and turned course thereafter amid rapid reinvestment into the company. It maintained double-digit return on investment whilst FCF yields were declining, suggesting the capital budgeting initiatives were successful along with growth of the company. However, since late FY21, return on investment has shifted back to range [albeit still ~35%]. Nevertheless, the downtrends in both [combined with factors above] are not to be ignored.

Exhibit 1. ROIC and FCF yields have been shifting down since FY20 and FY21 respectively along with narrowing contract revenue

{kind=link}

Data: HB Insights, RVP SEC Filings

US Government contract update

The key overhang in the RVP investment debate remains its contract with the United States Government Department of Defense, U.S. Army Contracting Command-Aberdeen Proving Ground, Natick Contracting Division & Edgewood Contracting Division [ACC-APG, NCD & ECD] on behalf of the Biomedical Advanced Research and Development Authority [BARDA]. It accounts for this as the Technology Investment Agreement ("TIA"). Back in FY21, RVP was a growth story and saw tremendous upside on the chart following material orders under this agreement to supply syringes for Covid-19 vaccinations.

However, whilst this contract has been extended, and the company continues to work with the US Government, additional orders are unknown. The salient points detailing the bridge of this contract from FY20–date are outlined below:

- Effective July FY20, the company started the TIA for $81mm in government funding to expand its domestic production of needles and syringes. RVP books this as a deferred liability that is amortizes as a gain over the life of the PP&E increase.

- From May FY21, the TIA was amended for an additional ~$27.5mm in funding to add 12,500 square feet of controlled environment, plus 2 additional assembly lines, to further increase existing domestic manufacturing capacity.

- As of June 30 FY22, it had negotiated contracts to purchase automated assembly equipment, moulds and tooling, and some auxiliary equipment for $64.9 million.

- The US Government also funds a temporary certificate of occupancy for the $6.7 million 27,800 square foot controlled environment, and the company has received the certificate of occupancy for the new $5.9 million 55,000 square foot warehouse.

Current portions of the contracted facilities are seen below:

Exhibit 2. RVP long-term deferred liability for TIA, Q2 FY22

Data: RVP 10-Q Q2 FY22

Exhibit 3. Current Portion of US Government Sales, down from $12.72mm to $9.56mm

This trend remains the key risk for the company looking ahead, as Covid-19 cases/vaccinations continue to dwindle, so too is the US Government revenue likely to pull back also.

Data: RVP 10-Q Q2 FY22

In this vein, investors must consider this increasingly smaller slice of revenue contribution moving forward. It also reduces the predictability of RVP's future cash flows and therefore impacts measures of corporate value.

Valuation

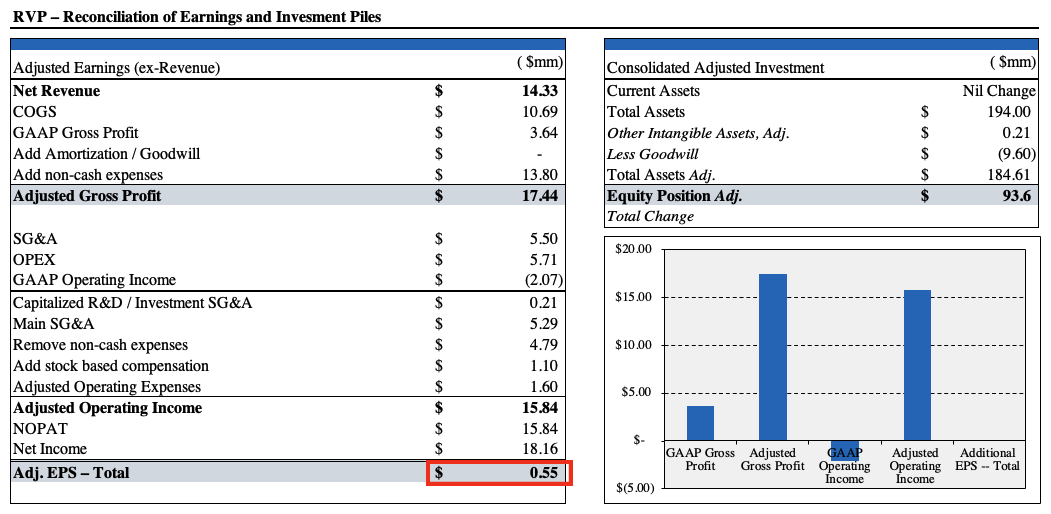

As we've seen a glimpse of RVP's continuing value [historical and forward-looking earnings], we also need to make several adjustments to GAAP earnings to clean up the picture.

First, let's take a look at what we're buying in RVP. We capitalize $206,000 in R&D expenditure onto the balance sheet and back out a $9.6mm deferred tax asset to see equity value adjust down to $93mm from $102.5mm. We do have $45mm in retained earnings as a plus, and adjusted tangible book $76mm. We're also buying into tangible assets of $96.7mm that are depreciated over 39 years and therefore retain strategic value on the balance sheet. As we saw, capital intensity is low.

Exhibit 4. Reconciliations to GAAP earnings to extract true value

{kind=link}

Data: HB Insights

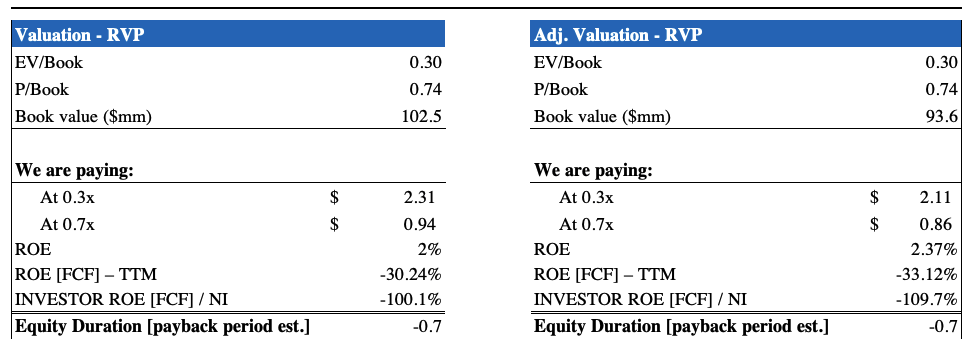

As noted, shares do trade at a respective discount to book value. Question is, does this represent value or are shares fairly priced at this discount? Post adjustment, we'd be paying an implied $0.86–$2.11, each the respective discount to the current market price. Even on unadjusted values, we'd pay a discount.

Exhibit 5. Adjustments to book value see an improvement to the implied cost per share

{kind=link}

Data: HB Insights

In light of the analysis over RVP's investment value above, and in terms of continuing value [earnings], we see shares priced fairly at $2.97, with an adjusted forward EPS of $1.10 [Exhibit 6]. Therefore, we don't see compelling value at these levels, as we are capturing less than $1 per share in upside relative to current market value.

Exhibit 6.

Data: HB Insights

This provides investors a clearer understanding of exactly what it is they are buying in this relatively opaque name. From our analysis, we choose to abstain from being buyers at this point, as we seek further clarification on the company's revenue recognition ex-US Government. In this vein, we rate shares a hold at $2.97.

For further details see:

Retractable Technologies: What Are We Buying In This Niche Operator?