AGRIP - Reviewing Preferred Security Recommendations And Strategies From 3-6 Years Ago

2023-07-08 00:17:28 ET

Summary

- We discuss the challenges of generating income in a low to zero interest rate environment and review the effectiveness of strategies suggested in previous articles.

- We also review the performance of preferred securities issued pre-financial crisis and note that they have outperformed the overall preferred market, particularly those issued by Goldman Sachs and Morgan Stanley.

- Our suggestion is that variable rate preferred securities have been a successful strategy but with a warning that if rates decrease, fixed rate low coupon issues would be a better strategy.

Introduction:

One of the greatest challenges an investor has faced in the last decade plus, has been how to manage the need to generate income in a low to zero interest rate environment. Anyone with an historical view knew there was great convexity risk embedded in the market for income investors , but managing the risk versus the need was a significant challenge. Over the last 3-6 years, I wrote a number of articles mostly targeted towards unique types of available preferred securities in the market with the goal of trying to thread that needle between income and principal risk from a rising rate environment. While we've certainly not reached a definitive point in time where the Federal Reserve will change their interest rate policy, with the most recent meeting behind us providing the first pause in rising short term rates, I thought this would make a good point in time to review how effective those recommendations and strategies I provided turned out until now. I find the process of reviewing long term strategies a very useful learning process, and can help one make better decisions in the future. Let's take a look at the different articles I wrote back then, what they hoped to provide in terms of strategy, and how that has worked in the most recent experience of the rising rate environment we've endured.

Free-Floating Preferreds: 11/21/2018

Almost five years ago I wrote this article that reviewed a group of preferred securities issued in the pre-financial crisis period of 2006-2007. Right in the title I suggested these could be used as a hedge against a rising inflation environment. These securities featured minimum coupon floors with an ability to switch to variable rates once the combination of 3-Month LIBOR + a certain stub coupon exceeded the minimum coupon. I focused on the ones that were closest to becoming variable rates as LIBOR was moving higher, but we can review the group as a whole to see how they performed relative to the preferred market as well.

Another interesting aspect of this group of securities is they were primarily issued by large wall street banks. Considering the recent swoon financials in general have suffered due to the bank runs, were these securities still able to produce a return as desired? Let's take a look.

{kind=link}

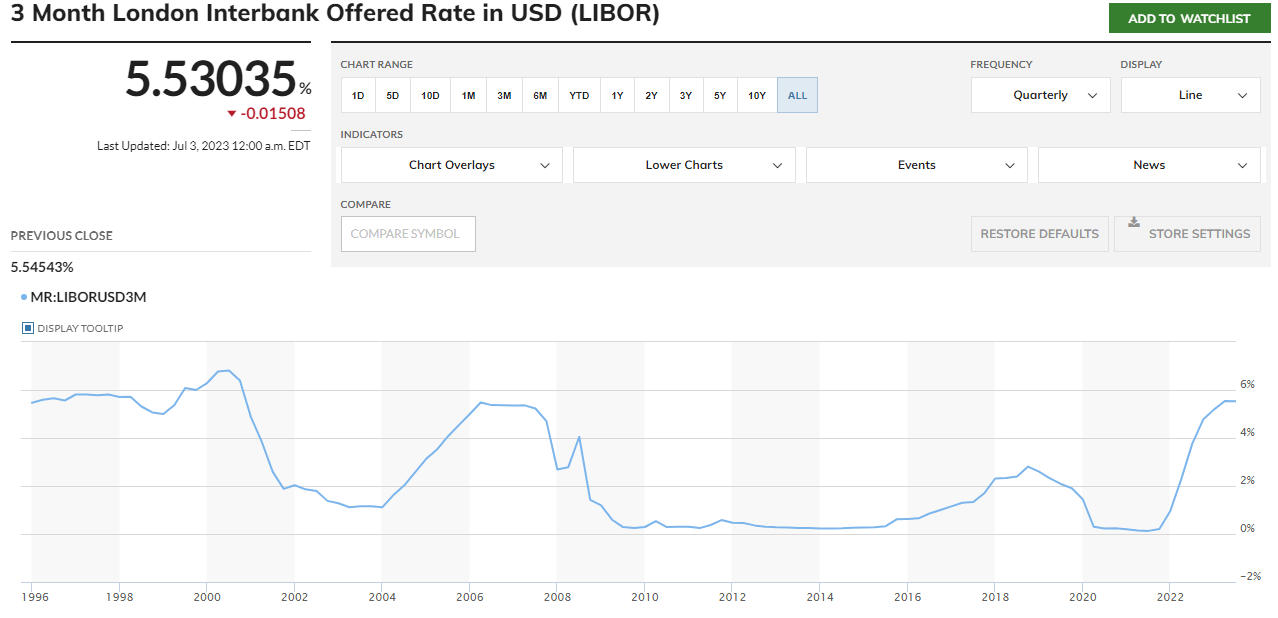

MarketWatch 3-Month Libor

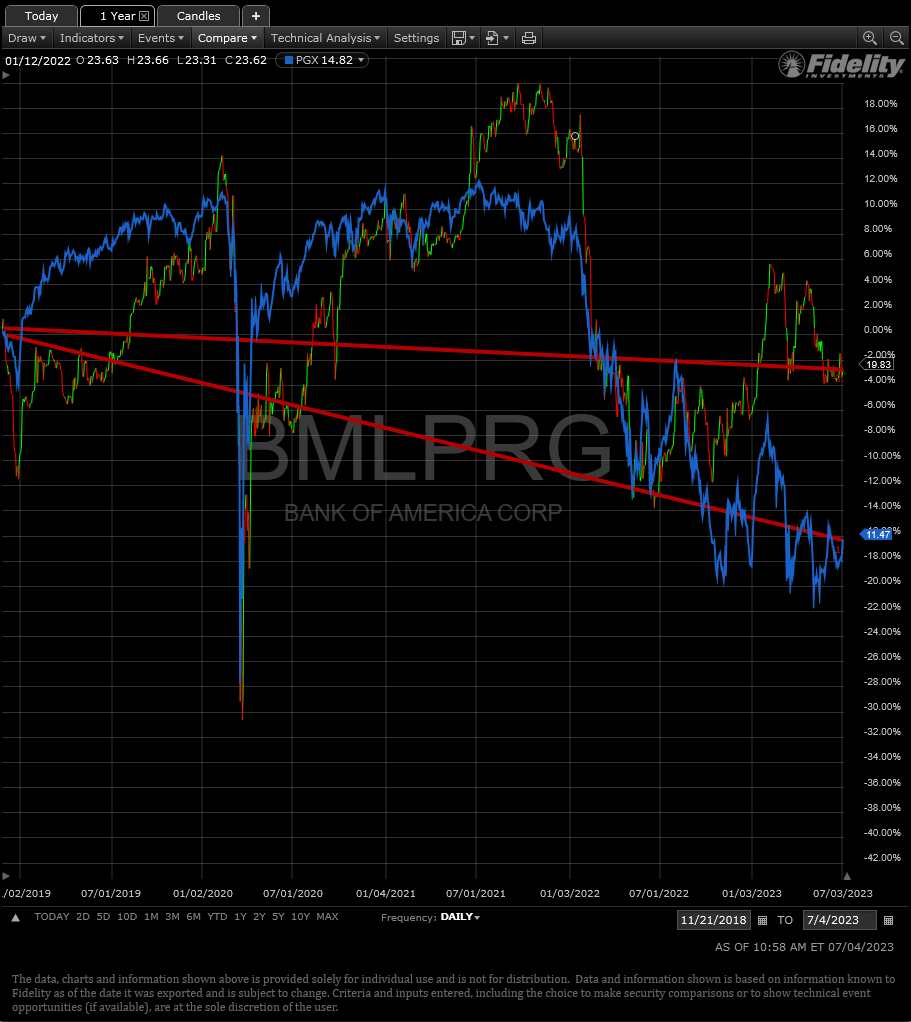

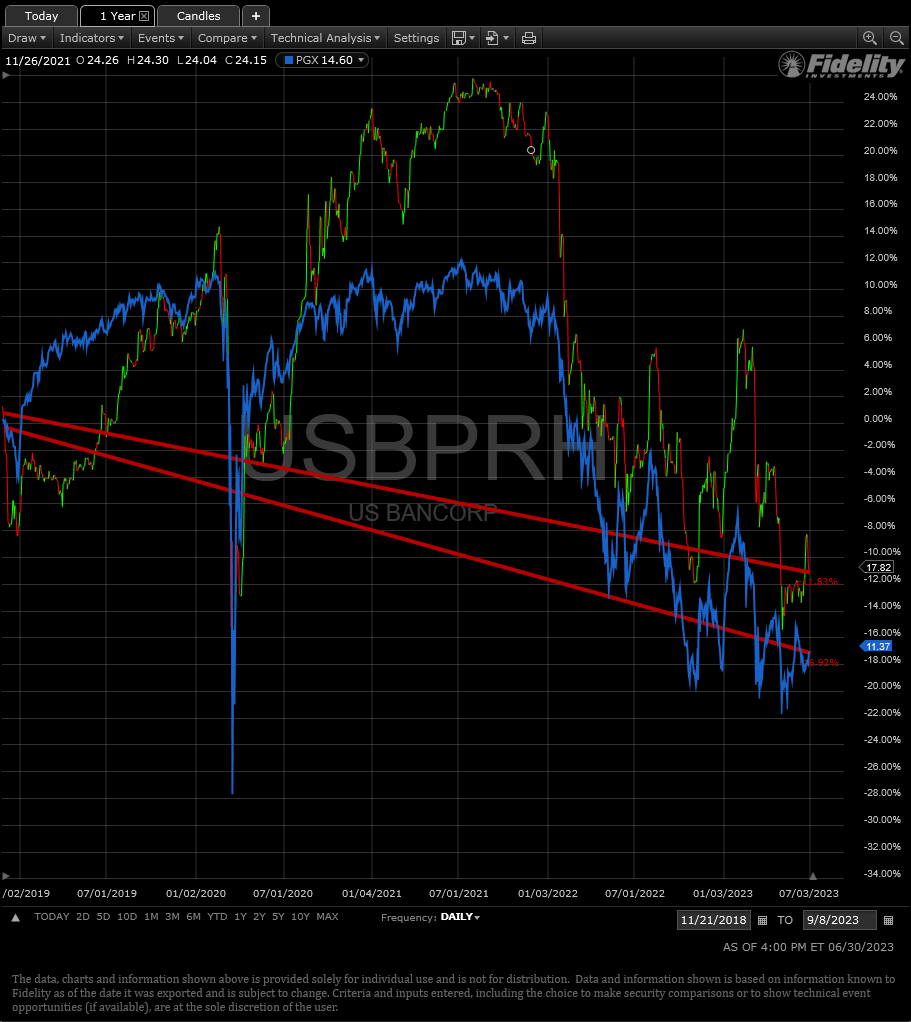

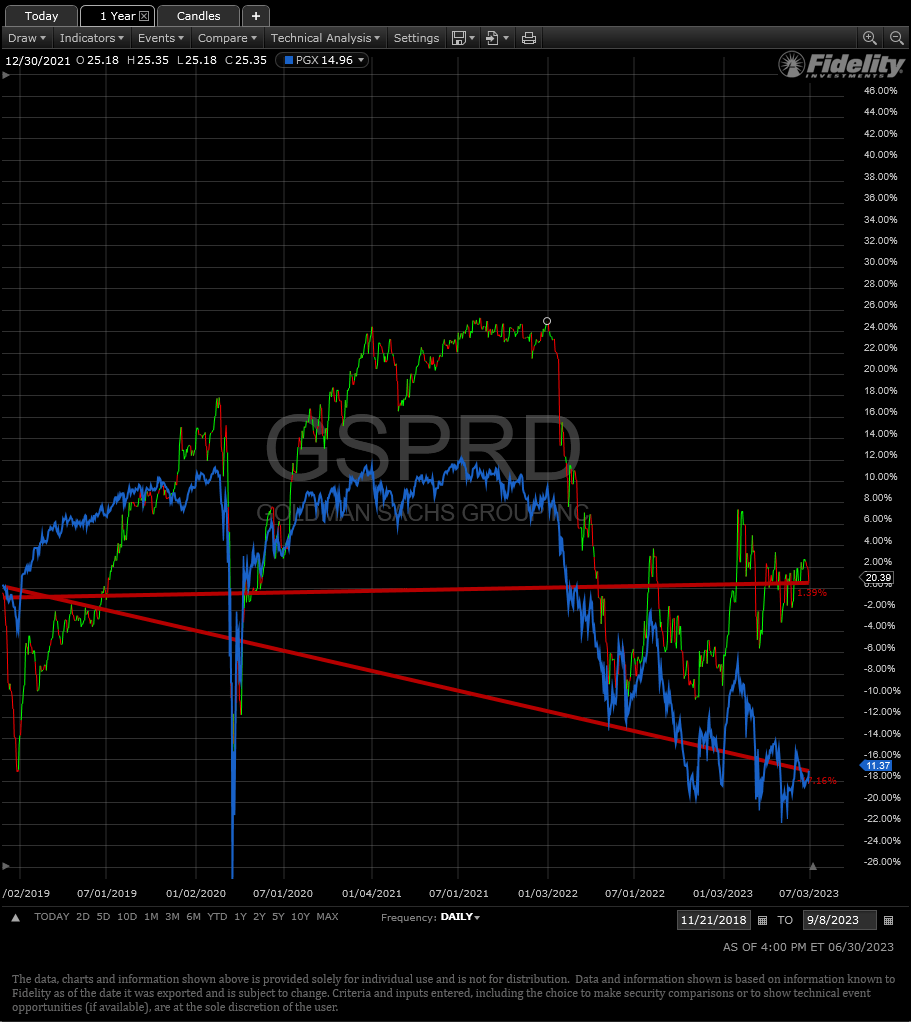

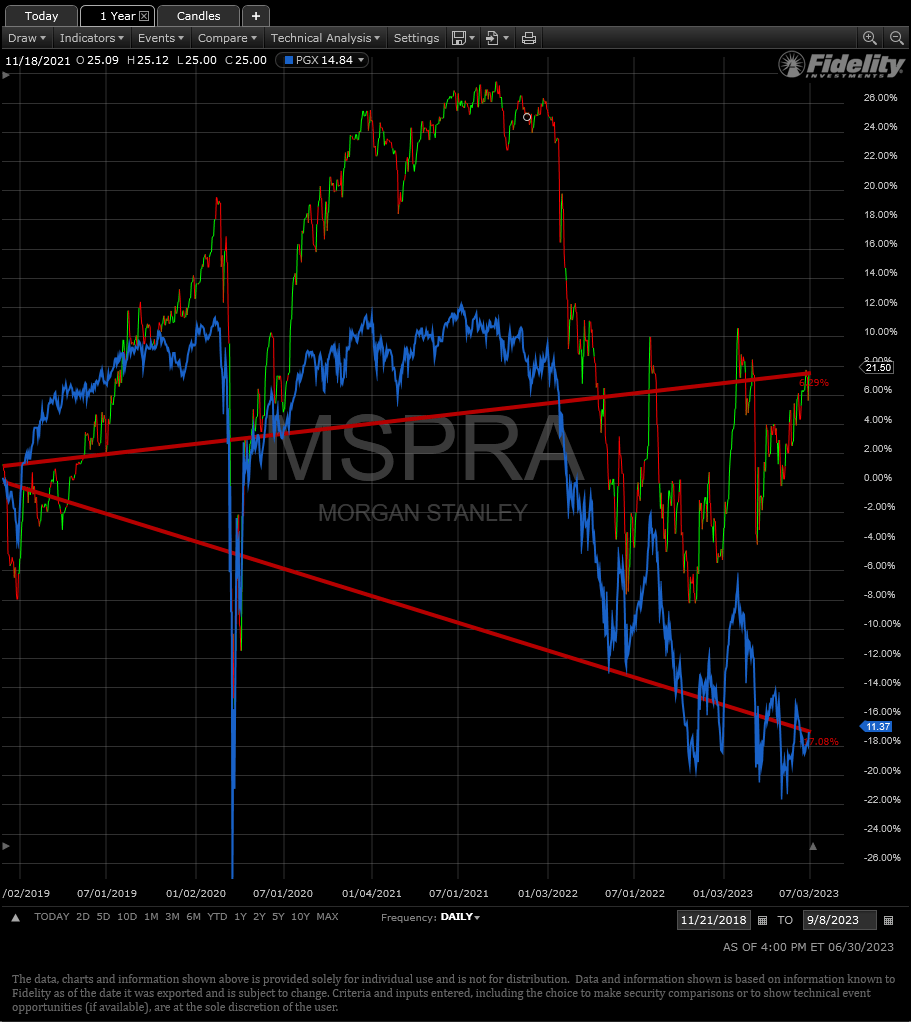

When this article was published, I had a chart in it showing the current rate of 3-Month LIBOR at 2.6445%. With it just over 5.53% currently, this portion of the thesis clearly worked out, and in fact all of these types of securities are now well above their minimum coupon floors and freely floating. At that time I shared I had exposure already to Bank of America's ( BML.PG ), and U.S. Bancorp's (USB.PH). As rates continued to rise, I swapped out of those and into Goldman Sachs ( GS.PD ), and Morgan Stanley's ( MS.PA ). Here's how those issues have performed in terms of principal relative to the Invesco Preferred ETF ( PGX ). In these charts, the blue line is always PGX for ease of comparison.

{kind=link}

Fidelity Active Trader Pro

{kind=link}

Fidelity Active Trader Pro

{kind=link}

Fidelity Active Trader Pro

{kind=link}

Fidelity Active Trader Pro

First, all of these securities outperformed the overall preferred market on a relative basis by a considerable amount. The Goldman and Morgan Stanley issues have actually increased in principal value while the PGX ETF is down a little over (17%). The weakest performer is the USB.PH issue which is down about (11%). This analysis lacks as it is not a total return view. If I had easy access to a chart providing that analysis, then I would have used it. However, it does convey the necessary point: the general thesis has played out and worked over the last three years. I.e., this is something to consider in the future if a similar market environment arises making this a worthy strategy.

{kind=link}

Personal Spreadsheet, SEC filings, Yahoo Finance

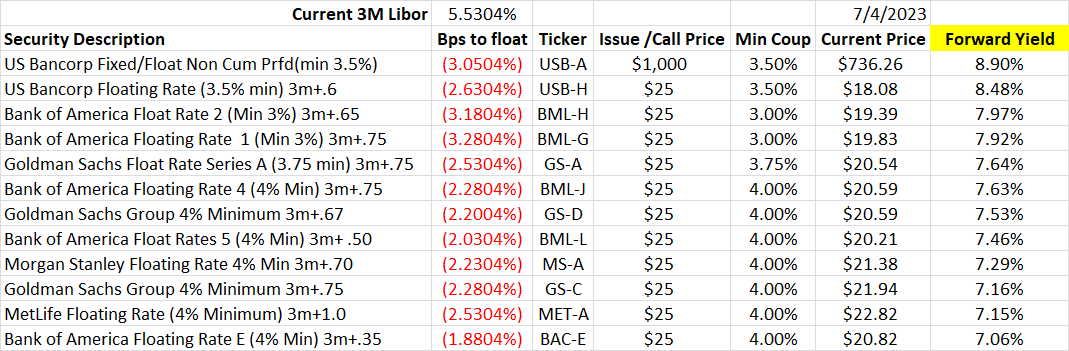

The second thing to note is there's separation between the regional banks and the investment houses. In fact, writing these articles is also a process I hope to gain something from. In this case, I admit that I decided to rotate into the U.S. Bancorp ( USB ) issues. The above chart is sorted by the forward yield of these now all variable rate preferred issues. There's 100+ bps of greater yield potential from the USB issues versus my current holdings. ( Note : the above chart I've labeled and calculated using 3-Month LIBOR. However, some of these issues have changed their calculation methodology as of June 30th. The USB issues, for example, have switched to using the 3-Month SOFR +0.26161% spread adjustment feature . Please do your own due diligence for each issue if you're interested in investing. Don't take my above chart as gospel!). Clearly, the market is reflecting concern for these USB issues relatively. Is this warranted? I actually purchased some USB equity in the most recent downdraft while it was trading well below book value, so clearly I'm biased in my comfort for these issues. Part of that comfort though was how the fixed coupon preferred USB issues were trading relative to the market.

{kind=link}

Quantum Online, Yahoo Finance, Personal Spreadsheet

The above shows all of the current fixed coupon preferred issues from USB with their current yields highlighted at the close of trading on July 3rd. Note that they all trade fairly similarly despite sizable variances in their coupons, and they are all less than 6% yield. That's particularly interesting because the diversified PGX ETF yields over 6.4% currently. So the fixed low coupon USB preferred issues are yielding less than the overall preferred market, while the variable floating rate USB issues are above their other comparable securities. The risk here is more likely the same for what I will discuss frequently throughout this review: while owning these variable rate preferred securities has worked to this point, if rates turn around and head lower for whatever reason, (recession etc...), then the opposite strategy would be better employed. Meaning, you'll want to own the fixed rate low coupon issues out there instead, as they will appreciate in principal value to a greater extent. Next, let's review what happened to Post-Call Utility Preferred securities after an article I wrote earlier in 2020.

Post-Call Utility Preferreds: 8/10/2020

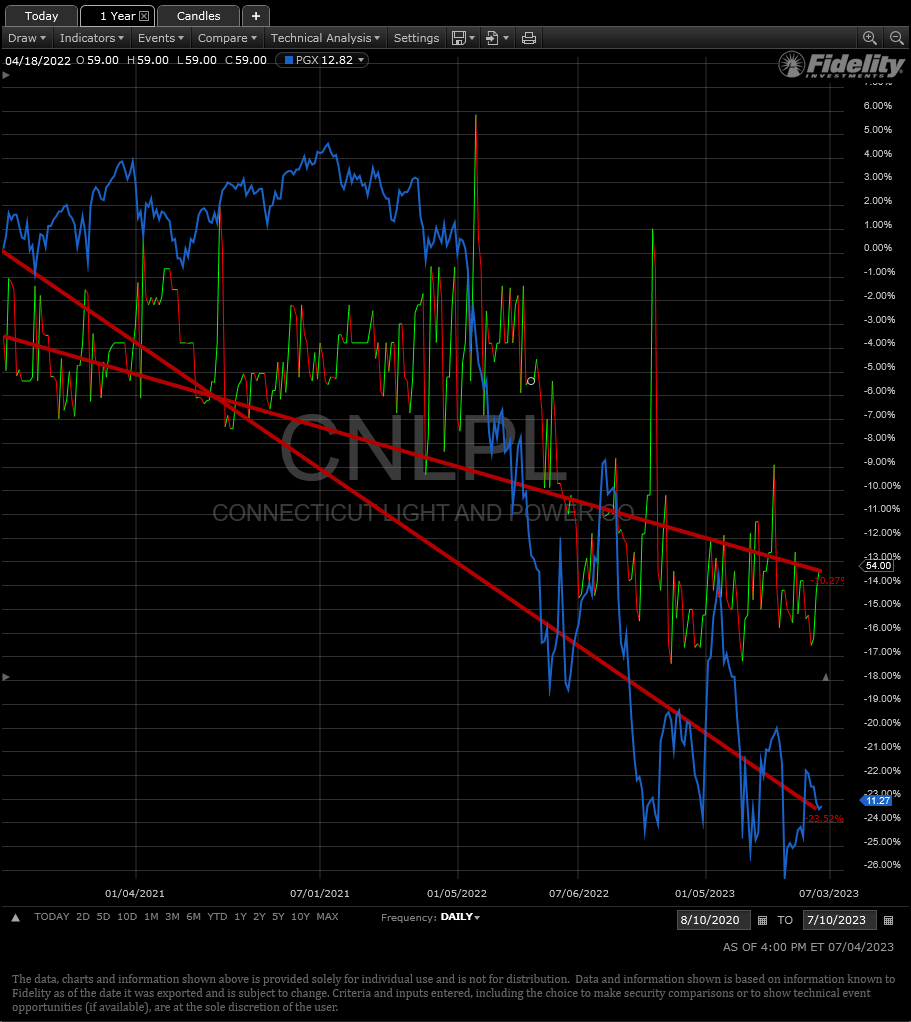

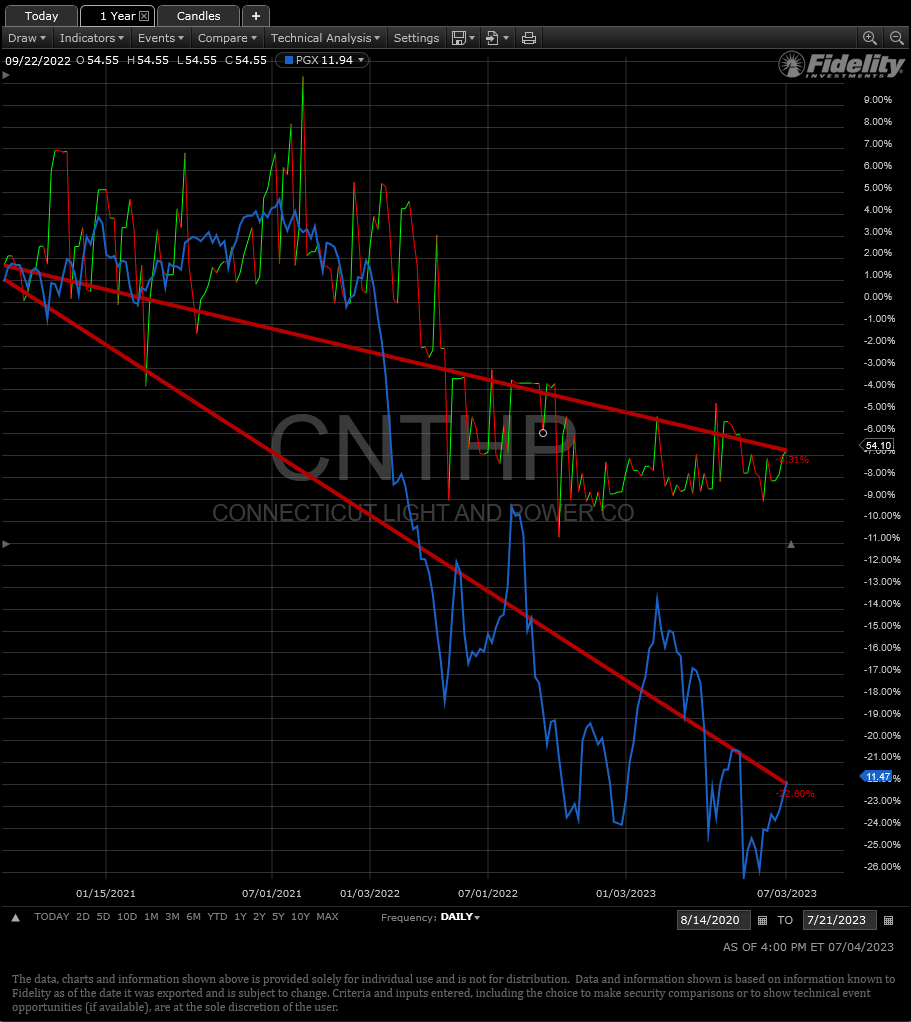

The primary thesis of this article was to own post-call utility preferred securities, because they offered higher yields due to the risk of being called keeping their price tethered closer to par. They also offered lower volatility and less convexity risk than their peer securities. Hence, as a strategy they provided better current yield and less downside risk in a rising rate environment. The primary issue was the risk that they would get called in by the issuing company, which I argued meant you had to be careful and purchase these as close to par when market environments offered the opportunity. This final point proved prescient as two of the four issues I highlighted were indeed called in: AILLL and IPLDP. The Connecticut Light & Power issues ( OTC:CNLPL ) ( OTCPK:CNTHP ), however, are still trading and likely to remain so due to their regulatory requirement. Let's take a look to see what happened in these two cases.

{kind=link}

Fidelity Active Trader Pro

{kind=link}

Fidelity Active Trader Pro

These two issues are tricky for this purpose as they are not liquid and sometimes don't trade at all during a given day. Hence, the charts above are the closest next date of trade after the article publication. Still, you can see again that indeed the lower convexity risk of holding a higher coupon helped to reduce the impact to the principal loss during this rising rate period. Again, the above just shows principal amounts and doesn't include the impact of higher yield on the total return profile of this comparison. Considering these issues were yielding mid-5% at that time which was nearly 3 years ago less one month, the (8%) and (10%) declines in principal were more than covered by the cumulative distributions. Thus, the strategy proved effective to this point for the issues that didn't get called, and display the value of the thesis but also the risk and necessity to buy-right when market opportunities are available closer to par. It's not a slam dunk though since some of these issues did in fact get called in generating small losses, but one could argue that still might have been a good thing relative to what happened to the overall preferred market.

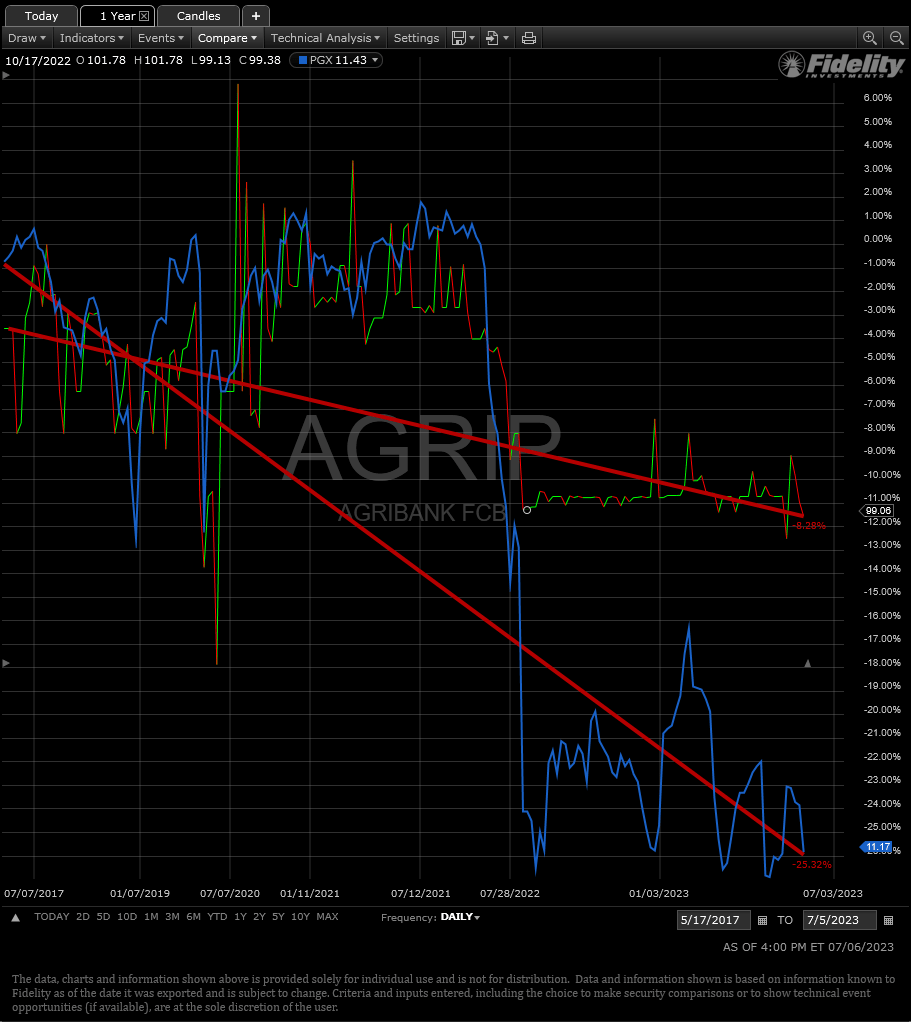

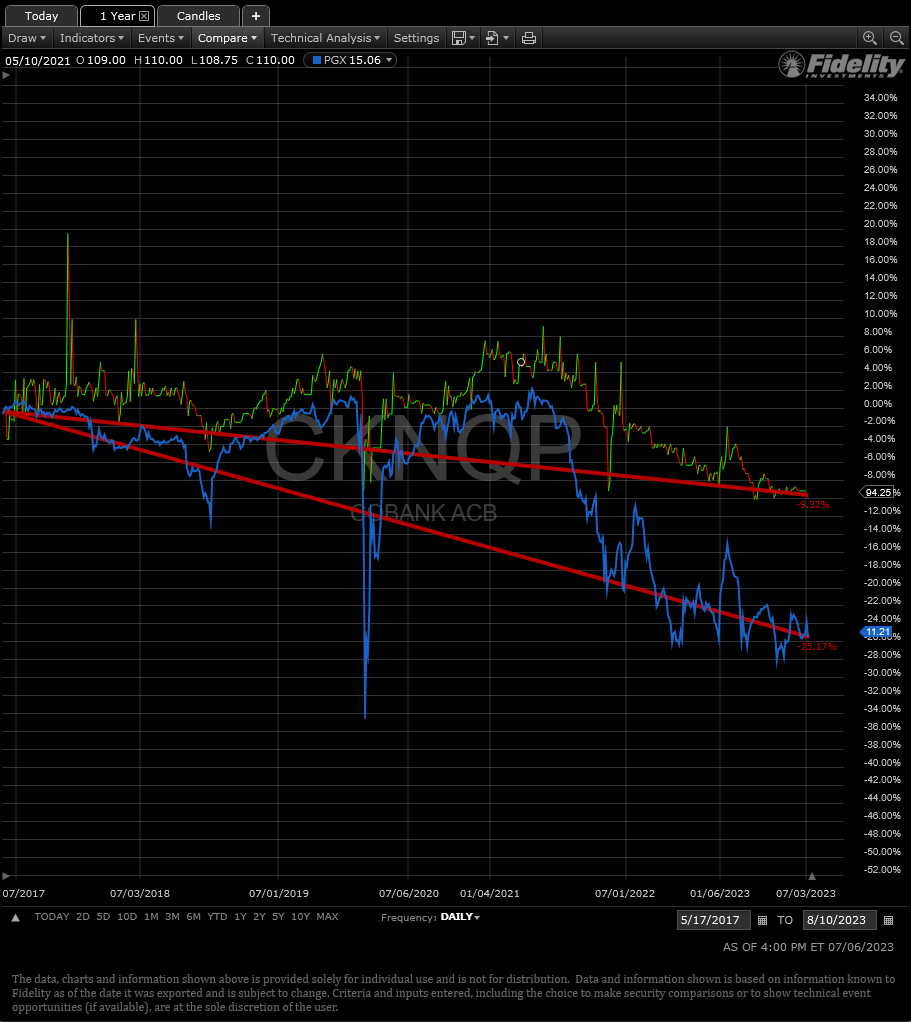

Farm Credit System Bank Preferreds: 5/16/2017

Last, I'd like to review this article from over six years ago . It might be my favorite project as most people I talk with, even on the professional side of the business, know zero about the Farm Credit System and these preferred issues. It's a long piece that goes into the history and structure of the FCS including its GSE status. In the end I highlighted four securities that traded OTC from two of the system banks: ( OTCPK:AGRIP ), ( OTCPK:CKNQP ), ( OTCPK:CBKLP ), ( OTCPK:CBKPP ). The latter two of which sadly were called in recent years. AGRIP can be called on the first of the year in 2024, and CKNQP can be called on the first of 2025. These are illiquid issues which offered higher coupons and significantly higher Yield-To-Call at the time of the article than other banks' offerings. Let's see how the remaining two have done.

{kind=link}

Fidelity Active Trader Pro

{kind=link}

Fidelity Active Trader Pro

The first security one could argue might be resisting declines in its recent performance due to the possibility of getting called in less than six months. The market tends to pin such securities close to par given that risk. However, as we can see there's almost a year and a half left before that same issue crops up for CKNQP, and its relative return is almost identical to AGRIP's over that given time frame. I actually find CKNQP attractive right now given its profile and current trading price below par, and have added to positions in recent months. If interested I encourage the reader to review my original article as a primer for understanding these unique preferred securities before investing.

Overall though, this is another case where the basic strategy of searching for higher coupons and yield, even while sacrificing liquidity, proved very valuable over holding a diversified basket of securities in the form of PGX ETF.

Conclusion:

I find these reviews useful in confirming one's basic strategies employed during different market environments. I'm glad to see that indeed these under-the-radar issues all proved very useful and superior than the overall market alternatives given a very difficult landscape for income investing at that time. Now that we're reaching a more normal market environment for interest rates relative to the last 100 years of market history, we can begin to ponder if a different strategy should be employed moving forward.

This review isn't intended to provide suggestions for what may lie ahead, but you can see how basic strategies around convexity do pay off over time measured in years. If you believe we're heading into recession, then long-term rates are likely to move lower as well as shorter duration. In that scenario a better strategy would be to switch into more liquid fixed coupon securities preferably with low coupons issued in recent years, and trading well below par that would provide significant principal return potential. I will say that I have not employed that strategy as of today. My sentiments tend towards the camp that believes global inflation rates are declining as commodity prices continue to recede, suggesting the Fed is likely to tighten too much watching rear view mirror data. However, the top decile of society continues to carry economic growth through spending, and has not wavered to this point from rising rates. Right now my thought is rates are most likely to plateau here for an extended period, so I'm maintaining a blended portfolio with some current and soon to float rate exposure in case I'm wrong about inflation. I'm also taking advantage of short term rates to deploy in 3-9 month increments of T-Bills in place of capital normally deployed in equities. Chasing frothy tech driven manias is not my cup of tea.

I hope you found this review useful, and at least gives you some ideas about how to deploy your capital given your personal market outlook. Good luck investing to everyone, and have a good summer. -NCSI

For further details see:

Reviewing Preferred Security Recommendations And Strategies From 3-6 Years Ago