RVLV - Revolve: Growth Potential Is Limited

Summary

- Despite a significant decline, Revolve is still trading at high multiples.

- The market expects the company to continue to post robust double-digit sales growth and improved margins.

- Before the pandemic, many brands did not even think about developing an online sales channel.

- Today, Revolve is facing stiff competition from both fast-growing marketplaces and famous Maisons.

- In our opinion, the future growth rate will be lower rather than higher. The operating leverage potential is also quite limited.

Investment Thesis

Over the years, Revolve ( RVLV ) has demonstrated an impressive growth rate and a permanent improvement in profitability. However, prospects and potential have always been reflected in the price. While the stock is down significantly from its highs, current multiples suggest that Revolve still has a significant runway ahead, or that the company will improve its operating leverage. However, in our opinion, the company's potential is significantly limited. According to our estimate, the current price is slightly below the fair market value. The margin of safety is insufficient. We rate shares as a Hold .

Company Profile

Out of work after the dot-com crash back in 2003, two young tech co-workers Michael Mente and Mike Karanikolas founded a fashion company based on a patented technology platform and big data analytics to work efficiently. Revolve was one of the e-commerce pioneers in the premium apparel market. Only the emerging and rapidly growing industry provided the company with a significant tailwind.

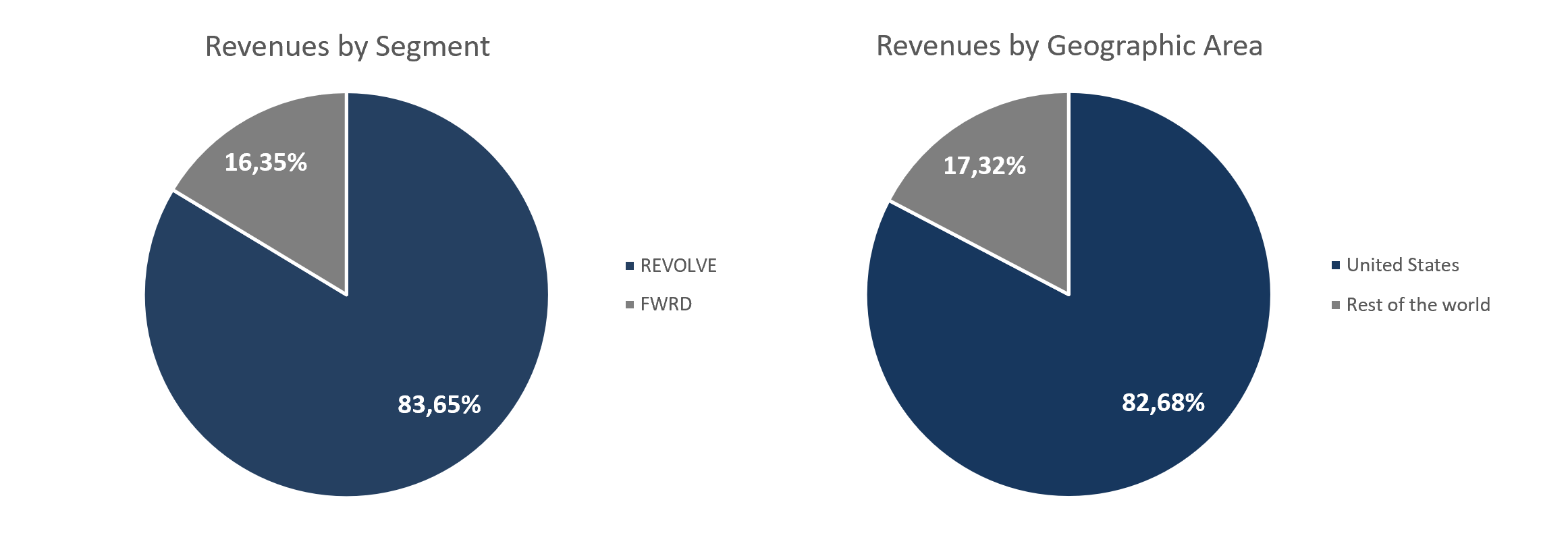

Today, Revolve is a premium fashion retailer offering more than 70,000 clothing, footwear, accessories, and beauty products through its Revolve and FWRD platforms. The first one specializes in upper-middle/high buyers, while the second caters to high-end clients. Over 83% of revenue comes from Revolve. Despite active international development, the US remains the key market with a share of 82.7% of total sales.

{kind=link}

Revolve's focus on millennials and Gen Z is reflected in its once-innovative approach to influencer marketing and active social media advertising. Today, the store's ambassadors are more than 30,000 microbloggers with a small but loyal audience.

Growth Potential is Limited

We like haute couture for its low price elasticity, relative resistance to macro headwinds, and simple business model. In addition, fashion firms have a deep competitive moat, provided with recognition and exclusivity. We also like growth companies for the potential returns they can generate at a reasonable entry price.

Revolve is one of the rare growth companies in the fashion industry that is also operationally efficient and doesn't burn shareholder value. Of course, Revolve's prospects have not gone unnoticed by Mr. Market. Since the public listing, investors have been avidly gobbling up shares even at premium prices; in November 2021, the stock traded for more than 60x Forward EBITDA.

Since then, Revolve's capitalization has declined by 76.8% to 2022 lows; the stock is currently trading over 65% below its November 2021 high. However, the market is still asking for 19.40x Forward EBITDA for the company. Obviously, this is a more reasonable estimate than it was before. However, it does imply that Revolve still has a significant runway, or that the company is able to substantially improve its operating leverage.

Over the past five years, Revolve has grown at an impressive CAGR of 24.82%. In the first nine months of 2022, the company's revenue reached $842.26 million, up 29.3% year-on-year. The number of active clients grew by 34%, average order value by 16% YoY. However, in physical terms, the number of active customers increased by only 84 QoQ - a significant slowdown and a return to pre-pandemic levels. The average growth from Q3 2018 to Q4 2019 was 82 active customers per quarter.

The number of returns also increased significantly, resulting in a 17.85% decrease in revenue per active customer to $119. It is worth noting that revenue per active customer has been declining for several quarters, which is also in line with the trend observed in 2019.

{kind=link}

We think the future growth rate will be lower rather than higher. Revolve needs to be seen in the context of the development of the e-commerce market. The company was one of the pioneers of a promising market.

It was a new world and a new opportunity with the internet and online commerce starting to change things.

There was a large and growing interest in apparel online. But there weren't really that many players doing it or doing it well. We felt like we could come out of the gates with a better approach and then continue to build on that."

- Co-CEO Mike Karanikolas in an interview for Los Angeles Times

Before the pandemic, many brands did not even think about developing an online sales channel. Today, Revolve is facing stiff competition from both fast-growing marketplaces and famous Maisons.

Marketplaces are just an infrastructure for sellers, due to which they can offer buyers a much wider choice. In addition, they become the beneficiaries of the network effect: the more sellers on the marketplace, the more buyers; and the more buyers, the more new sellers. Revolve can only offer a limited range of products.

Revolve lacks pricing power as third-party brands account for most of its revenue. With the owners of these brands, Revolve has to compete for the buyer, as many fashion houses have significantly expanded direct-to-customer online sales in recent years.

Of course, Revolve can bet on the development of its own brands, but it takes years to form a recognizable name in the high fashion industry. Customer reviews on the Trustpilot are indicative. Most of the negative reviews point to the poor quality of goods from little-known brands. Probably many of the names belong to the company. It is worth noting that the share of own brands in the sales structure is steadily declining: they are represented by 20.1%, 26.7%, and 36.1% of Revolve segment total revenues for 2021, 2020, and 2019, respectively.

As Revolve grew, it steadily improved its operating leverage. In 2017, the operating margin was 5.14%, and for the last twelve months, it was 9.25%.

However, the potential for profitability growth is also limited. First, Revolve's gross margin will always be constrained by the pricing policies of third-party brands. Second, while management emphasizes the uniqueness of its marketing strategy, marketing efficiency, defined as revenue per dollar of marketing expense, is steadily declining (excluding an abnormal 2021). If the trend continues, Revolve will be forced to increase spending to maintain double-digit sales growth.

{kind=link}

Perhaps expanding the logistics infrastructure will provide some economies of scale. In any case, management believes that the Fulfillment expense as a percentage of revenue will decline in the long term. However, it is unlikely that operating margins will reach the mid-teens. The potential for profitability growth due to asset turnover is also limited as the ratio is already high and given the expected slowdown in growth, it is unlikely that Revolve will be able to increase sales significantly faster than the assets.

RVLV Stock Valuation

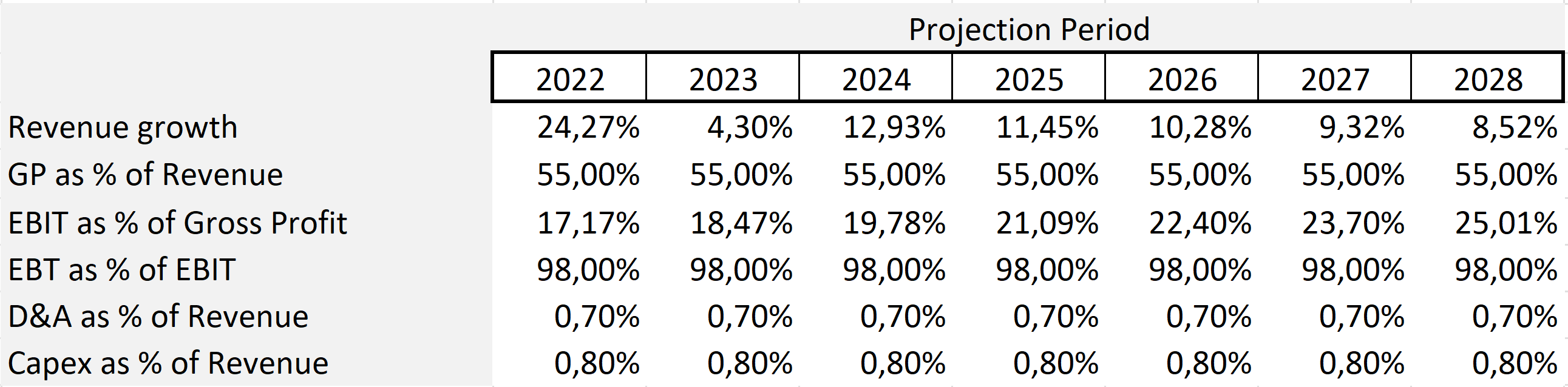

Our estimate is based on some assumptions. The revenue is projected as follows:

- From Q3 2018 to Q4 2019 plus Q3 2022, Revolve grew its active customer base by an average of 82K per quarter. We expect the company to continue growing its customer base at the same rate until the end of the forecast period.

- The average revenue per active customer from Q2 2018 to Q4 2019 plus Q3 2022 is $114. We assume that revenue per customer will remain at the same level. We do not take into account inflation, as our forecast seems quite optimistic given the downward trend in the indicator.

{kind=link}

We assume that Revolve's gross margin will remain at 55% until the end of the forecast period, in line with the trailing twelve months.

Over the past five years, Revolve has improved operating margins by an average of 0.7 percentage points per year. Given that the company is still in its growth phase, we assume that operating leverage will continue to improve at a comparable pace.

We expect DD&A expenses as a percentage of revenue to be at 0.7%, in line with the average over the past five years. The capital expenditure forecast is also based on a five-year average of 0.8%.

Our assumptions are presented below:

{kind=link}

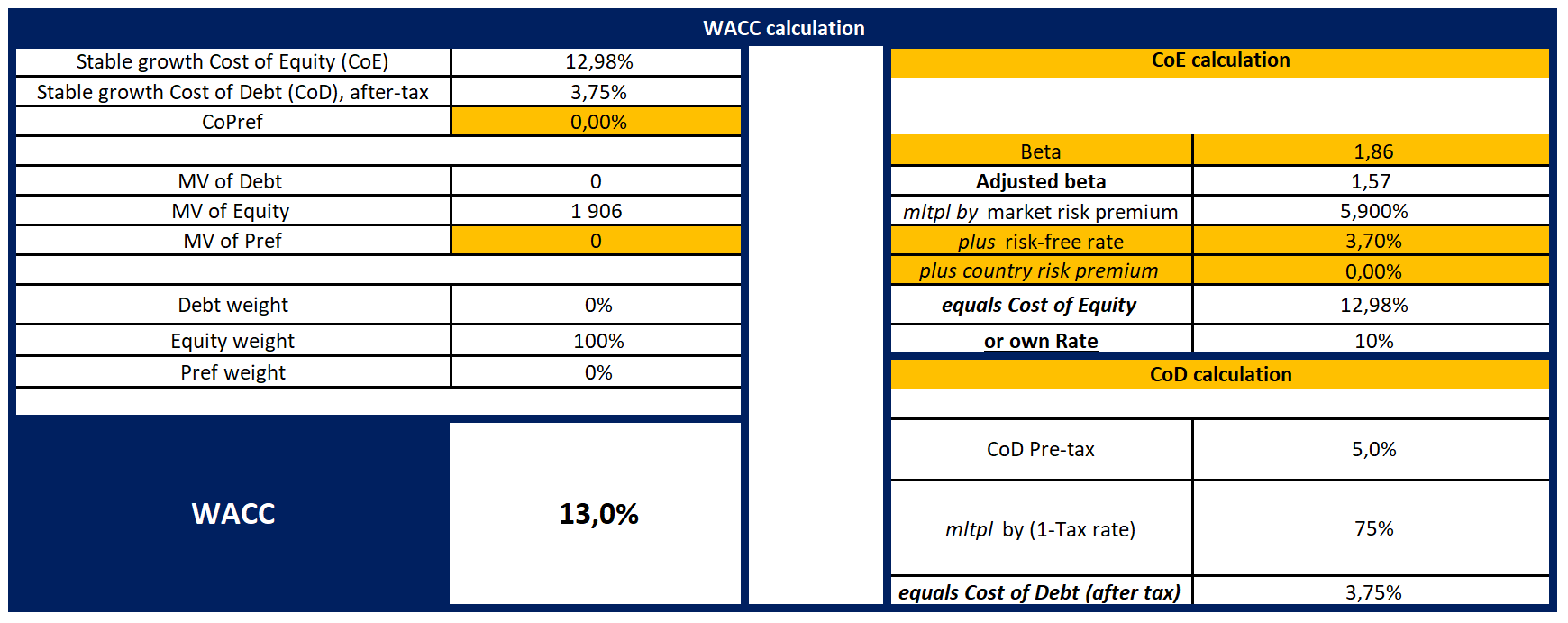

With the cost of equity equal to 12.98%, the Weighted Average Cost of Capital [WACC] is 13.0%.

{kind=link}

With a Terminal EV/EBITDA of 8.87x, our model projects a fair market value of $2.09 billion, or $28.5 per share. The upside potential we see is about 10%.

You can see the model here .

Conclusion

Despite a significant decline, Revolve is still trading at high multiples. The market expects the company to continue to post robust double-digit sales growth and improved margins. However, in our opinion, the future growth rate will be lower rather than higher. The operating leverage potential is also quite limited. According to our estimates, the company is trading near its fair market value. We are neutral on RVLV.

For further details see:

Revolve: Growth Potential Is Limited