RVLV - Revolve Is Held Back By Selling And Distribution Expenses

2023-04-17 23:18:33 ET

Summary

- If Revolve can lower its shipping costs, its net income will jump considerably. The stock price should follow suit.

- Revolve continues to grow thanks to its merchandising algorithms and large addressable market.

- Revolve's asset-light economic model is highly profitable.

Revolve is One Step From Achieving Exceptional Profits

I have long admired Revolve ( RVLV ) and its management team. As a shareholder, it comforts me to know that millions of dollars of merchandise are leaving Revolve's warehouse on a daily basis. Humans have always been enthralled by fashion, and Revolve offers a trendy curation and seamless online apparel shopping experience. I am confident Revolve's management team will continue to deliver a strong offering and shopping experience to customers and create value for shareholders. However, shipping costs have been restricting the latter. In this article, I address this issue and explain what needs to happen for it to alleviate.

Background on the Business

Revolve is a fashion and cosmetics retailer for Millennial and Generation Z consumers. It does not operate retail stores. All its sales are online. To date, Revolve is worth ~$1.9 billion. In 2022, Revolve achieved revenue of $1.1 billion against $59 million in earnings. It employs 1,384 people worldwide.

Revolve differentiates itself from competitors by employing mass social media marketing. In its 10-K, Revolve claims it works with celebrities and thousands of social media influencers. Revolve’s social media accounts can achieve billions of impressions per day during its largest marketing event, Revolve Festival.

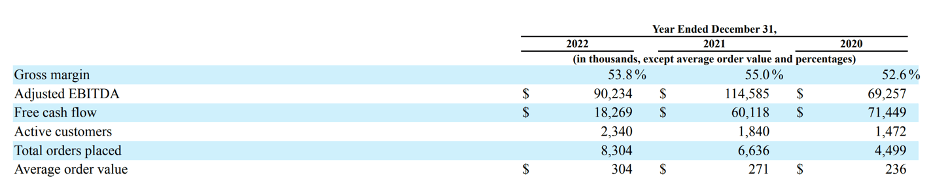

Revolve also differentiates from competitors by taking a data/technology-driven approach to running the business. Revolve built a custom, proprietary technology platform that delivers automated inventory management, pricing, and trend-forecasting algorithms. The management team claims in its 10-K, “Our proprietary technology leverages data from a vast net of styles, attributes, and customer interactions to create a strategic asset of hundreds of millions of data points.” The two founders who still run the company have a background in computer engineering and business. The two were “quick to realize early the importance of relying on data and analytics." They claim their approach facilitates what they refer to as “constant newness,” with over 1,500 new styles launched per week on average in 2022. One metric that the management team at Revolve refers to when analyzing the efficacy of the algorithms is its full-price mix of net sales. The figure was in the high 70s from 2018 to 2020 and was 85% in 2022, as shown in the recent earnings presentation. These figures are well above industry standards and contribute to Revolve’s strong gross margins, which are also above many retail peers.

Quantitative Attribution: Long-Term Growth ~15%, Projected Gross Margins of ~55%

Growth Prospects

Management's goal is to grow revenue by 20% annually. My models forecast a more conservative growth rate of 15%, with growth coming from a combination of customer adds, an increase in orders placed, and an increase in average order value; slowing economic growth will be a headwind.

Firstly, Revolve should be able to achieve a 15% annual revenue growth rate because its addressable market is large and growing, and therefore it has ample opportunity to add new customers. During 2022, active customers grew 27% to 2.3 million. I believe Revolve will add customers at a similar, albeit muted, rate over the next few years. As of Q321, it claims it has penetrated less than 3% of its addressable market. The figure was calculated assuming 58 million women ages 18 to 44 are in the US. The overall growth of the addressable market is attributable to "significant growth in digital channels" and increasing e-commerce sales. Digital Commerce 360, with the help of data from the Department of Commerce, determined, " Ecommerce helped US apparel sales stay afloat in 2020 . Online apparel sales accounted for 46.0% of total US apparel sales in 2020… US online apparel sales grew 21.8% year over year and reached $110.68 billion, Digital Commerce 360 estimates." The large and growing addressable market and Revolve's relatively low penetration should enable it to maintain double-digit growth for the foreseeable future.

International growth prospects are abundant. Currently, 17% of sales are shipped to international customers. International sales increased by 13% during 2022. Revolve's management team has clarified that it will be patient during its expansion to countries outside the US because it strives to maintain the same high quality of service provided to customers in the US. Certain customs and border control policies can make shipping to international customers difficult.

Revolve also has an opportunity to expand its curation into new product categories, which should lead to an increase in total orders placed. It saw success selling more athleisure apparel and cosmetics during the pandemic. It is also stepping into the luxury business, which will increase the average order value. Revolve's luxury sister website, FWRD, is seeing tremendous success. Sales in this business segment grew by 23% during 2022.

Return Metrics

I believe Revolve's management team has demonstrated superior capital allocation abilities. Its ROE is 15%. The business can pursue a growth strategy while remaining debt-free and profitable. This is generally a favorable combination, demonstrating to investors that the capital-light business model enjoys strong brand loyalty. During earnings calls, I've heard analysts complain that the balance sheet is not "optimized," meaning the company should take on debt. I'm not overly concerned with Revolve's capital allocation and balance sheet optimization. If RVLV stock remains near the current price, I want the management team to buy back stock quickly. I would probably be against taking on debt to issue a dividend. Suppose the company takes on debt and distributes a dividend. In this case, I'm not confident I could invest the proceeds from the dividend into an asset that generates higher returns than Revolve's management team. The cash deployed by Revolve's management generates returns at 15%, which is above the cost of capital. Combine the ROE with 15% top-line year-over-year growth, and the earnings/equity/share price should compound at a desirable rate. Further, Revolve is unequivocally conservatively financed, which should bode well if economic pessimism continues to rise throughout 2022.

Revolve stewardship, marketing, and customer loyalty give me confidence it will be able to fend off competition. Revolve claims its customers are loyal because it constantly engages them through the digital platforms they use daily. Currently, Revolve has 2.3 million active customers. The name and brand continue to grow stronger.

Other Risks, Key Metrics, and the Balance Sheet

Sales fell only 3.4% during Covid, but net income grew 59.2% as the net profit margin nearly doubled. I consider the sales figures achieved during Covid respectable, given Revolve sells going-out clothing.

Revolve would likely experience decelerating sales growth during a recession. Usually, consumer discretionary businesses fare worse than consumer staples during recessions. Revolve's customers might be unable to allocate as much of their wallets toward clothing as they might during an economic expansion.

I look to buy companies that sell nondurable goods so that I can accurately discount future cash flows. I do not consider apparel, Revolve's offering, a nondurable good. However, one can make the argument Revolve enjoys a recurring revenue stream. As I previously mentioned, during 2022, active customers grew 27% to 2.3 million. To clarify, Revolve states, "We define an active customer as a unique customer account from which a purchase was made across our platform at least once in the preceding 12-month period." I'm pleased that the figure is growing, and I recommend shareholders pay attention to it going forward.

Revolve uses some customer data points to assess progress and make decisions.

{kind=link}

Revolve maintains a fantastic balance sheet. Its current assets of $518 million cover its current liabilities of $181 million. The company has no debt.

What's Holding Revolve Back? Shipping Costs

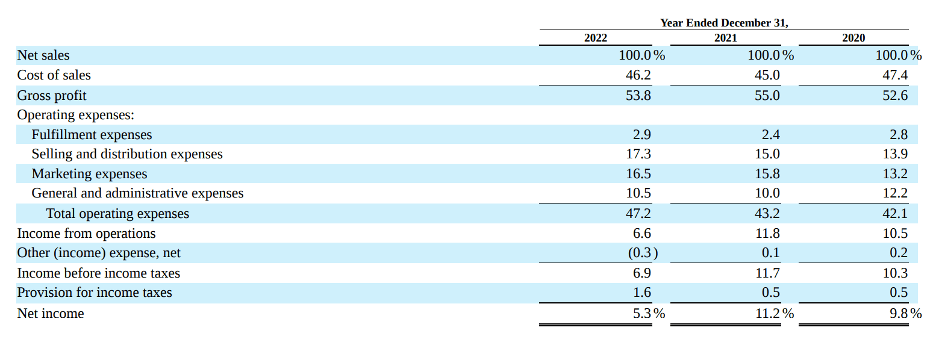

Revolve enjoys a relatively high gross margin of 54%. In my opinion, the relatively low net profit margin of 5% has weighed on the business. More specifically, the "Selling and Distribution" expense item has increased as a percentage of sales over the past three years. The increase is attributable to elevated return rates and fuel surcharges.

Expenses as a Percentage of Sales ( Revolve 10-K )

{kind=link}

Fuel surcharges peaked for Revolve in Q2 2022 after the Ukraine conflict.

Revolve's management team mentioned that it is addressing increasing "Selling and Distribution" costs by utilizing the new East Coast warehouse facility to process orders and returns from customers in the Northeast. Also, management is exploring an opportunity to decrease international shipping volume by holding merchandise overseas. Obviously, fuel surchargers are out of management's control and will likely vary based on geopolitical developments.

My current model forecasts that "Selling and Distribution" will be $219 million in 2023, or 17% of sales.

{kind=link}

With good decisions and good fortune concerning fuel surcharges, management could achieve a Selling and Distribution expense of only 16% of revenue, equating to about $15 million more in profit than most of the analyst community is modeling for in 2023. I strongly believe that RVLV stock price would move favorably following the hypothetical scenario.

Valuation

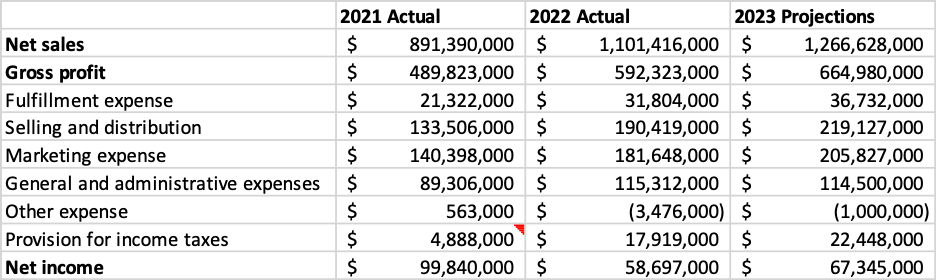

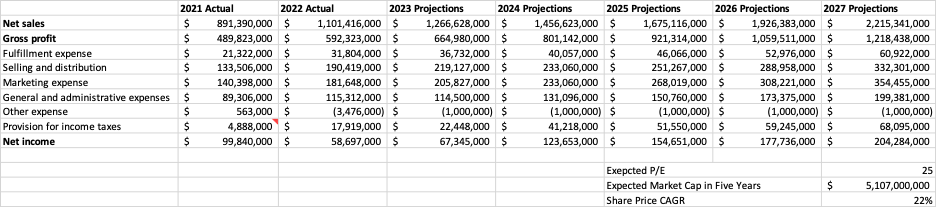

Revolve is worth ~$1.9 billion, or ~$26 per share. In five years, I think a reasonable target price to set would be $5.1 billion, or ~$70.00 per share. I arrived at this target price using management's expectations to model operating figures over the next five years. The inputs for the model below, except the "Expected PE" figure, are all roughly in line with the figures management has presented to analysts in its publicly released materials. This model assumes annual revenue growth of 15%, the gross profit margin reaching 55%, Fulfillment Expenses reaching 2.75% of revenue, Selling and Distribution reaching 15% of revenue, Marketing Expenses reaching 16% of revenue, General and Administrative Expenses reaching 9% of revenue, Other Expenses at $1 million, and a 25% tax rate.

{kind=link}

Conclusion

Revolve has built a powerful economic machine with superior customer loyalty. It can reinvest all of its returns above the cost of capital. It should have the opportunity to do so for years to come, given the ample growth opportunities. Therefore, the earnings and share price should compound at an attractive rate. I consider Revolve a strong buy at its current price.

For further details see:

Revolve Is Held Back By Selling And Distribution Expenses