RVLV - Revolve's Growth Story Still Stands

2023-09-06 15:28:27 ET

Summary

- Revolve Group operates two online clothing retailers in the United States as well as internationally.

- The company has experienced financial challenges in 2022 and 2023, including falling gross margins and trailing revenues.

- Despite these challenges, I believe the stock is worthy of a buy-rating as the stock has fallen into a reasonable valuation and the long-term growth story should still stand.

Revolve Group ( RVLV ) operates as an online clothing retailer. As online retailing takes share of the clothing industry, I believe the company still has a great path of growth ahead of itself. Although Revolve has had a bad recent financial history with falling gross margins and trailing revenues, I believe the stock is worthy of a buy rating as the company's long-term growth story still stands in my opinion.

The Company

Revolve Group operates two online clothing retailers, Revolve and FWRD. The company has presence internationally, but the company's main geographic market is still the United States, as in Q2 of 2023 81% of the company's revenues came from the country. The company mostly sells clothing to young customers, as younger generations are more likely to purchase items online. The company also sells its in-house brands through Revolve, as in 2022 the company's owned brands contributed 22% to Revolve's revenues.

The company has a large focus on more expensive clothing - the company has many quite expensive brands on its Revolve website, and the FWRD website is based basically solely on designer brands - I believe this sets the company up for highly cyclical operations.

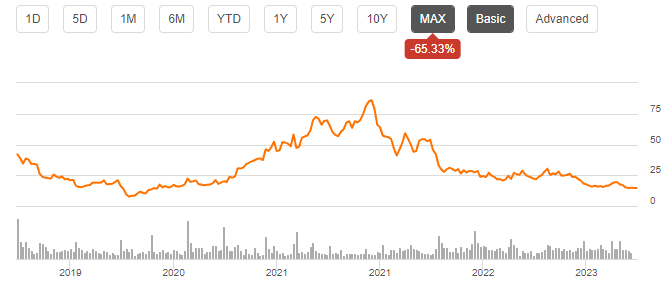

The stock of Revolve has seen its fair share of turbulence, as the stock started its journey with a significant price decrease after the company's IPO in 2019. As the pandemic began, online retailers saw increases in earnings and as the stock market rose in general, Revolve's stock rocketed up from a low of $7.17 into a high of $89.60. After the highs, the company has faced a challenging period, resulting in the stock's fall back to pre-pandemic levels:

{kind=link}

Financials

Overview

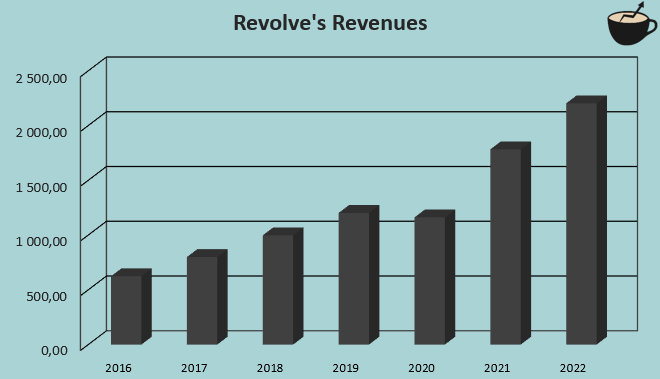

Revolve has achieved a good amount of growth in its history - from 2016 to 2022 the company's compounded annual growth has been 23.4%:

{kind=link}

As the company seems to have no acquisitions in the period, the achieved growth is organic - as online clothing retailers rise in popularity at the expense of brick and mortar retailers, I believe the company is poised for even more growth in the future.

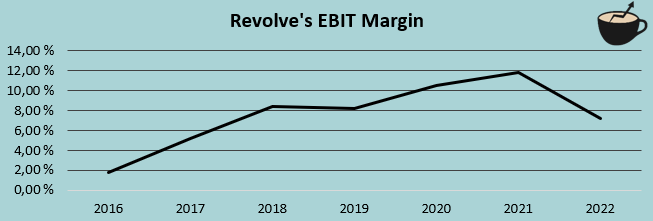

Revolve has had a growing margin for most of its history, as the company has achieved benefits from a growing scale in their operations:

{kind=link}

The company had issues regarding their margin in 2022, though, as Revolve's gross margin fell from 55.0% to 53.8% and as the company's SG&A expenses grew quicker than the company's revenues.

Revolve's balance sheet seems to be very strong; the company has a cash balance of $269 million and has no outstanding interest-bearing debt. As the company already generates free cash flow on a quite consistent basis, I believe a moderate amount of debt would leverage the company's financing in a healthy way.

Recent Issues

Even more than in 2022, Revolve has had issues in the company's operating margin in the first two quarters of 2023 - the company's operating margins were 4.4% and 2.7% in Q1 and Q2 of 2023 respectively, significantly below the previous year's margins of 10.0% and 6.6%. The company's Co-CEO Michael Karanikolas relates the decrease to multiple factors in Revolve's Q2 earnings call :

"Our profitability was significantly lower than last year's second quarter primarily due to the decline in net sales, the lower gross profit year-over-year and continued pressure on operating expenses in large part due to a higher return rate."

Moreover, the lower margin is coupled with slightly decreasing revenues - in H1 of 2023, the company's revenues fell by 3.5% year-over-year. As the company should still be in a growing phase, a decrease of 3.5% is significantly worse than what is likely expected from the company in a normal operational climate.

The stock market has priced Revolve's challenges significantly into the stock's price in the recent years - I on the other hand believe the long-term growth story still stands. For example, the company's active customers have still continued to climb, even in the challenging operational environment:

Active Customer Growth (Revolve Q2 Earnings Presentation)

The company also did still emphasize Revolve's long-term revenue growth and margin potential and relates the performance to a poor macroeconomic climate. As many other retailers have seen decreases in revenues and margins in the most recent quarters as well, in my opinion, the long-term growth prospect still stands.

Valuation

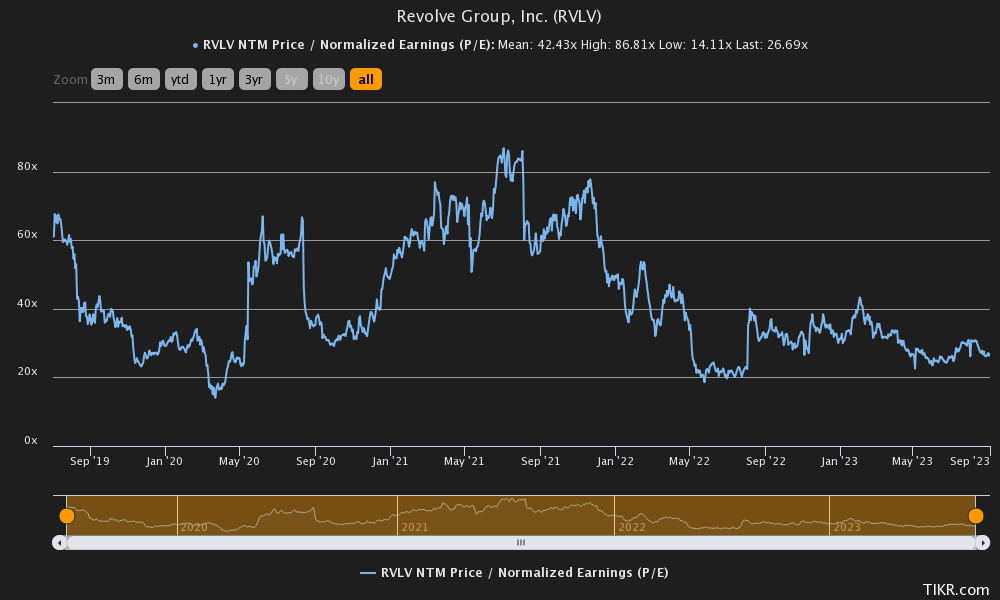

Revolve currently trades at a forward price-to-earnings ratio of 26.69. Although the ratio seems high, it is already significantly below the stock's historical average of 42.43:

{kind=link}

Also, when compared to other online clothing retailers such as Boozt and Zalando, mostly present in Europe, the company doesn't seem too expensive - Boozt currently trades at a forward ratio of 27.20, and Zalando at a ratio of 35.20. The comparisons are made with European companies, as I couldn't find profitable online clothing retailing platforms - companies such as Farfetch (FTCH) and the RealReal (REAL) operate at heavy losses.

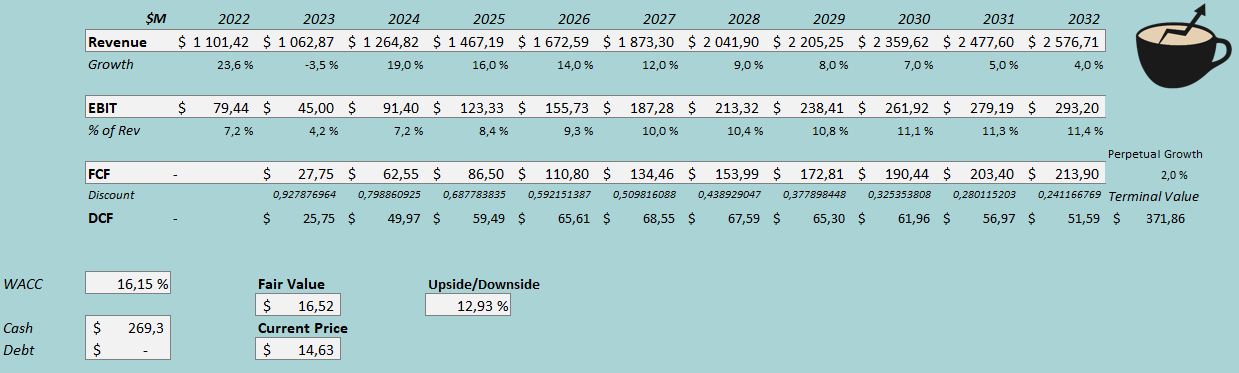

To further analyze the company's valuation, I constructed a discounted cash flow model. In the model, I estimate Revolve to have a revenue decrease of 3.5% in 2023, in line with the first half of the year. Going forward, I expect the company to proceed with its long-term growth story, although with a lower growth than in the company's history - I estimate a growth of 19% in 2024 that slowly fades into a perpetual growth of 2%, representing a CAGR of 12.1% from 2023 to 2030. Compared to the company's historical growth of 23.4%, the growth is significantly lower, but as Revolve is facing current issues I believe investors should have conservative estimates.

As for the company's margin, Revolve seems to be facing issues for 2023 - I estimate an EBIT margin of 4.2% for the year, three percentage points below the 2022 level. Going forward, I expect Revolve to get back control of its margin through a better operational climate as well as efficiencies from scale as the company grows - I expect the retailer to eventually reach an EBIT margin of 11.4%, in line with 2020 and 2021 levels.

These estimates along with a cost of capital of 16.15% crafts the following DCF model with an estimated fair value of $16.52, translating to an upside of around 13%:

{kind=link}

The cost of capital of 16.15% is derived from a capital asset pricing model:

CAPM of Revolve (Author's Calculation)

In the model, I expect Revolve to have an interest rate of 6.5% in the future - as the company currently has no interest-bearing debt, it's impossible to get a current interest rate. The used rate of 6.5% represents a healthy margin of safety, as the rate would be well above the United States bond yields. I expect the company to draw a very modest amount of debt in the future, with a long-term debt-to-equity ratio of 10%.

On the cost of equity side, I use the United States 10-year bond yield of 4.26% as the risk-free rate. The used equity risk premium of 5.91% is Professor Aswath Damodaran's estimate . Tikr estimates Revolve's beta to be a high figure of 2.14 - I believe that the current challenges present quite well as to why the beta is so high. The stock's beta could be lower in the future, though, as the operations mature. Finally, I add a liquidity premium of 0.5%, crafting a very high cost of equity of 17.41% and a WACC of 16.15% which I used in the DCF model.

Takeaway

Although Revolve Group has had turbulent finances in its recent history, I believe the lower stock level represents a possible opportunity. The company's long-term growth story should still stand, and with possible future operating leverage and significantly higher revenues, the company's stock price could have significant potential. Although my DCF model only points towards an upside of 13%, I have a buy rating for the stock, as my model has quite conservative growth estimates and a beta that could well be lower in the future.

For further details see:

Revolve's Growth Story Still Stands