GLPI - Rewarding You: 7 REITs Yielding High Goldilocks-Zone Dividends

2023-12-15 08:30:00 ET

Summary

- Identifying potentially habitable planets in the Goldilocks Zone is a primary focus in the search for extraterrestrial intelligence.

- Similarly, in dividend investing, there is a Goldilocks Zone where companies take just the right amount of risk with their dividend payouts.

- The Seeking Alpha Premium Quant Ratings system assigns Dividend Safety grades to predict the likelihood of a dividend cut for a given company.

- This article presents a list of 13 REITs yielding from 5.25% to 12.05%, with Dividend Safety Grades in the Goldilocks Zone.

- Then the author zeroes in on the 7 REITs with the highest yield, from that list.

In the search for extraterrestrial intelligence, the star-gazing scientists are most interested in identifying potentially habitable planets. To support life, the planet must not be too near the star it orbits, because surface temperatures would be too hot, nor too far away, because they would be too cold. The range of orbits where the distance from the star is just right, is called the Goldilocks Zone.

I would like to propose that there is a Goldilocks Zone in dividend investing also.

Regardless whether you are a COWhand or a FROG hunter , the safety of the dividend is of great importance to your return on investment. Different companies take different levels of risk with their dividend payouts. Some take too big a risk of a dividend cut, putting them in the Hot Zone. Holding them becomes very risky, because if the dividend is cut, not only does your income as an investor take a hit, but the underlying share price usually dives, as COWhand investors dump their shares, usually leaving you with the uncomfortable dilemma of selling at a sizable loss and reallocating, or holding for a very long time, waiting for the stock price to recover.

Other companies take too small a risk, doling out dividends very cautiously, keeping them in the too-safe Cold Zone. Sure, your income stream is safe and predictable, but it is smaller than it could be, if the company would only take on a little more (manageable) risk.

Then there are those companies that take just the right amount of risk, rewarding investors as richly as possible, without running a high risk of a cut. Those are the Goldilocks dividends.

Dividend Safety: How to read the scores

The Seeking Alpha Premium Quant Ratings system assigns Dividend Safety grades to most dividend-paying stocks, including REITs. These are intended to predict the likelihood of a dividend cut.

If a stock earns a Dividend Safety grade of F, the odds are 2-to-1 they will cut their dividends, and the odds are 50-50 the cut will happen within the next 12 months , according to Steven Cress , who pioneered the Seeking Alpha Quant Ratings system.

Some companies operate in an environment that more or less requires them to retain more earnings for expansion and reinvestment. However, for all other companies, a Dividend Safety grade of A+ generally means they could safely pay out significantly more cash income to their shareholders.

Thus, the graphic below portrays the way I view the meaning of the Dividend Safety grade, in most cases.

| Grade |

| B+ |

| B |

| B- |

| C+ |

| C |

| C- |

| D+ |

| D |

| D- |

| F |

| Braemar Hotels & Resorts |

| ( BHR ) |

| Hotel |

| 8.00 |

| C+ |

| LXP Industrial |

| ( LXP ) |

| Industrial |

| 5.46 |

| C+ |

| NNN |

| ( NNN ) |

| Net Lease |

| 5.43 |

| C+ |

| Medical Properties Trust |

| ( MPW ) |

| Healthcare |

| 12.05 |

| C |

| Highwoods Properties |

| ( HIW ) |

| Office |

| 8.96 |

| C |

| Alpine Income Property Trust |

| ( PINE ) |

| Net Lease |

| 6.37 |

| C |

| Getty Realty |

| ( GTY ) |

| Net Lease |

| 6.10 |

| C |

| Healthpeak Properties |

| ( PEAK ) |

| Healthcare |

| 6.25 |

| C- |

| Gaming and Leisure Properties |

| ( GLPI ) |

| Casino |

| 6.15 |

| C- |

| American Assets Trust |

| ( AAT ) |

| Office |

| 5.86 |

| C- |

| Boston Properties |

| ( BXP ) |

| Office |

| 5.76 |

| C- |

| Simon Property Group |

| ( SPG ) |

| Regional Mall |

| 5.46 |

| C- |

| W. P. Carey |

| ( WPC ) |

| Net Lease |

| 5.31 |

| C- |

Source: Seeking Alpha Premium

If you take a step down in Dividend Safety, you should get a significant step up in Yield, so for the sake of argument, the remainder of this article will take a quick look at the 7 REITs on this list that yield 6.00% or higher.

Braemar Hotels and Resorts

Braemar Hotels & Resorts ((BHR)) is crushably small, at a mere $0.15 billion market cap. The yield is high, mostly because the price is low. BHR shares sell at an estimated (-56.8)% discount to NAV (net asset value), and a very low Price/FFO '23 of 4.5.

The balance sheet is a mess, with a very heavy 94% debt ratio and 33% of the company's debt is held at variable (therefore high) interest, but Debt/EBITDA is very reasonable, at 7.0. However, shares are up 31.6% over the past 31 days, so the worst may be in the rearview mirror.

{kind=link}

Seeking Alpha Premium

Medical Properties Trust

Medical Properties Trust ((MPW)) is a lower mid-cap ($2.79 billion) international hospital owner that has been ruthlessly shorted this year. With a short ratio of 14.05%, it is still among the top 10 most-shorted U.S. equity REITs. As a result, despite a recent dividend cut (Q3 2023), the company still offers an extraordinary yield of 12.05%, as of this writing. However, its share price is up 41% in one month, which could cool the short-sellers' ardor, and suggests the company's woes may have bottomed.

The company excels at turning revenue into FFO, and its TTM (trailing 12 month) FFO payout ratio of 53% is quite conservative. However, due to problems with some of its largest tenants, MPW now faces some debt and interest coverage problems. The company's debt ratio is heavy at 62%, and Debt/EBITDA stands at a cumbersome 12.2, with 6.8% of the company's debt held at variable (therefore high) interest rates.

{kind=link}

Seeking Alpha Premium

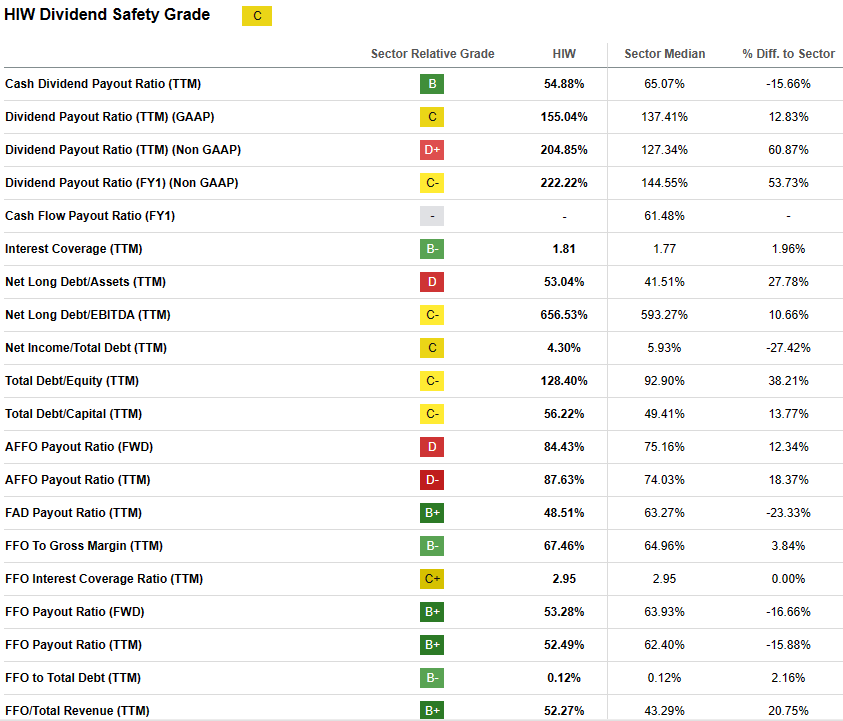

Highwoods Properties

Highwoods Properties ((HIW)) is a Sunbelt-focused Class A office REIT headquartered in Raleigh, North Carolina. The company has benefited from the post-pandemic population shift and the flight to quality in Office rentals. Nevertheless, like all REITs, and Office REITs in particular, its share prices have taken a beating. As of this writing, the Yield is at or near 9%, and unlike the vast majority of Office REITs, this company has not cut its dividend in 20 years, not even during the pandemic.

Its balance sheet is slightly shaky, with a 51% debt ratio and 15% of debt held at variable interest. However, HIW sports a sturdy Debt/EBITDA ratio of 6.0.

However, HIW excels at converting revenue to FFO, resulting in relatively comfortable FFO payout ratios, and its interest coverage ratio of 1.81 is pretty sturdy.

HIW is selling at a steep (-31.6)% discount to estimated NAV, and a Price/FFO ratio of 6.3, low even by Office REIT standards.

{kind=link}

Seeking Alpha Premium

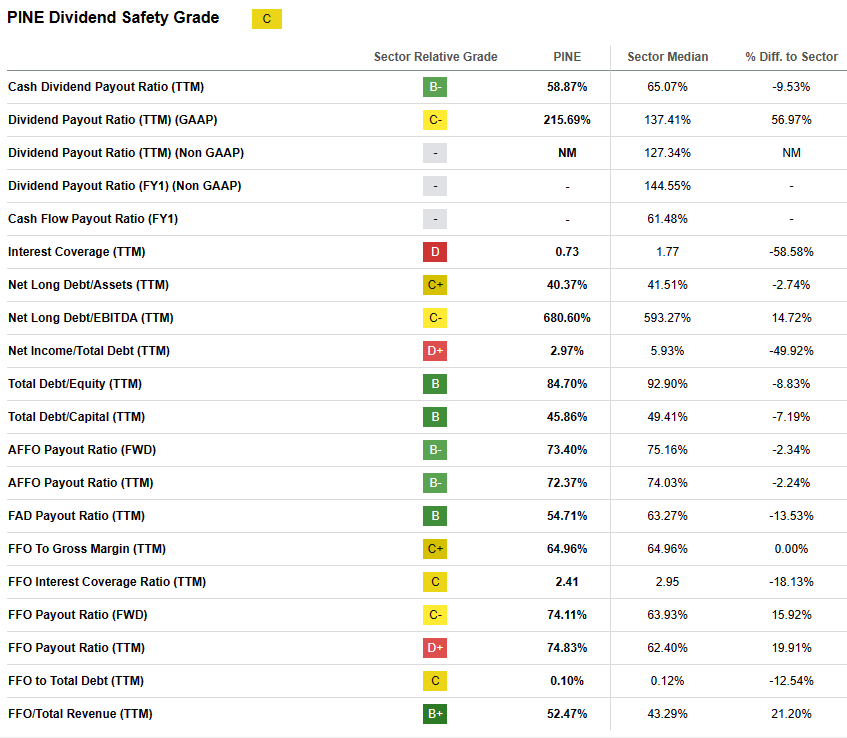

Alpine Income Property Trust

Alpine Income Property Trust ((PINE)) is externally managed by CTO Realty. Despite the name, this company is Sunbelt-heavy, and rents mostly to nationally-known retail brands. As of this writing, the Yield is well over 6%, and unlike the vast majority of REITs, this company has not ever cut its dividend, not even during the pandemic.

There is good news and bad news in its balance sheet metrics. PINE carries a 52% debt ratio and 0% of debt is held at variable interest. However, PINE sports a cumbersome Debt/EBITDA ratio of 17.0, so earning its way out of debt does not appear feasible.

However, like Highwoods, PINE excels at converting revenue to FFO, resulting in relatively comfortable FFO payout ratios. However, PINE's significant FFO decline in 2023, which is expected to come in at (-15.0)%, has driven its interest coverage ratio down to a perilous 0.73.

PINE is selling at a REIT-average (-17.3)% discount to estimated NAV, and a Price/FFO ratio of 11.8, which is a little lower than the Net Lease REIT average.

{kind=link}

Seeking Alpha Premium

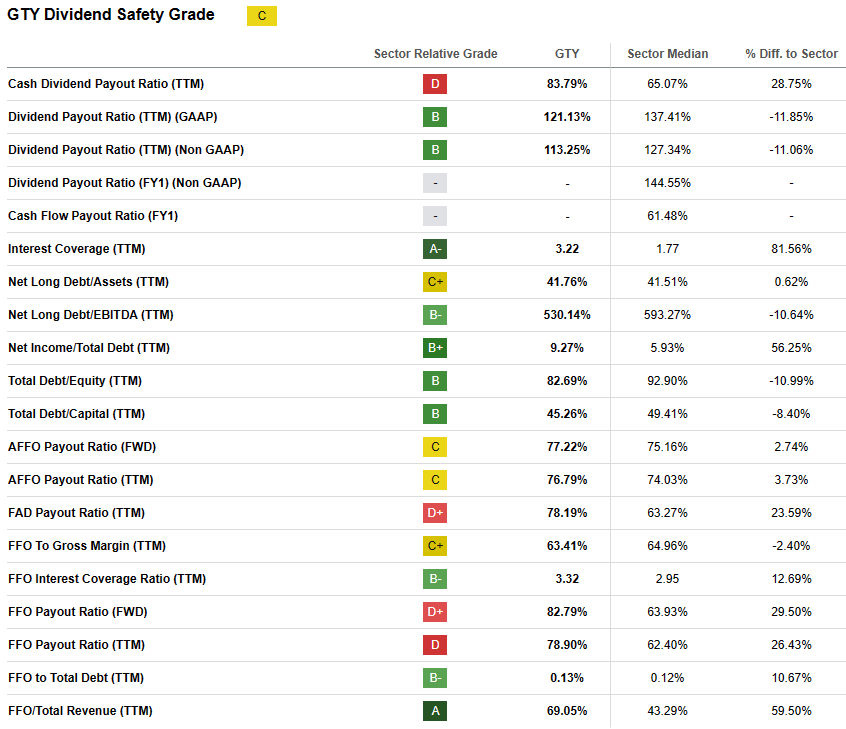

Getty Realty

Getty Realty ((GTY)) is the largest pure-play net lease REIT that focuses on automotive company tenants, heavy on gas stations and car washes.

Getty investor presentation

As of this writing, the Yield is well over 6%, and unlike the vast majority of REITs, not only did this company not ever cut its dividend in the past 8 years, it actually hiked the divvy significantly during the pandemic.

It's all good news where the balance sheet is concerned. GTY carries a typical 31% debt ratio and only 3.1% of its debt is held at variable interest. The company's Debt/EBITDA ratio is excellent at 5.0, so earning out of its debt appears entirely possible, and interest coverage is superb, at 3.22. This comes despite GTY's significant 2023 decline in FFO, which is expected to come in at (-14.0)%.

Like others on this list, GTY excels at converting revenue to FFO, resulting in a continued ability to cover their relatively aggressive FFO payout ratios. GTY is selling at a relatively rich +1.6% premium to estimated NAV, and a Price/FFO ratio of 14.0, typical for a Net Lease REIT .

{kind=link}

Seeking Alpha Premium

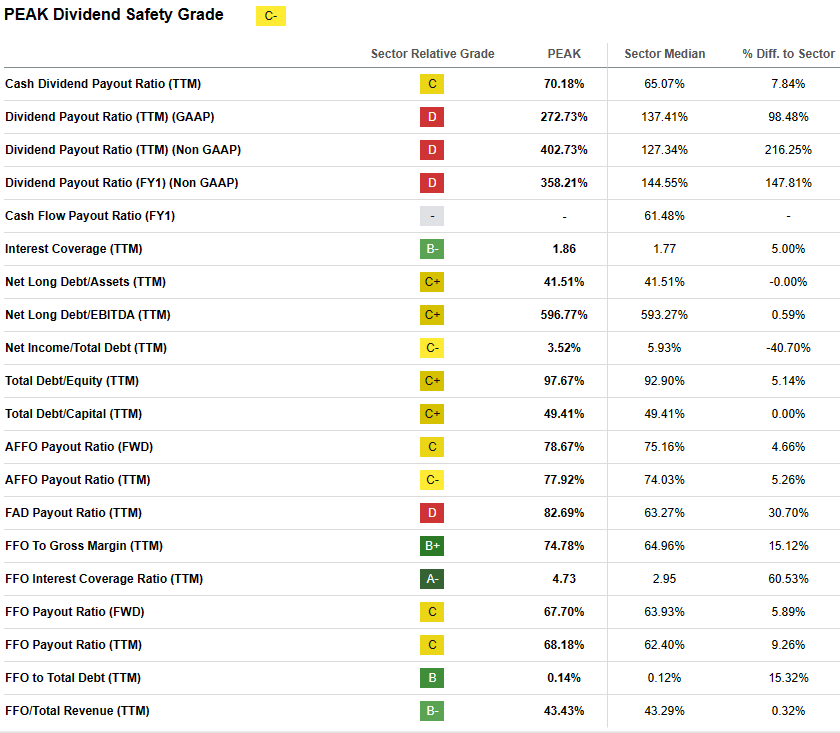

Healthpeak Properties

Healthpeak Properties ((PEAK)) owns a portfolio of well-selected senior housing, medical office, and life science lab facilities. The company is a little too dependent on its top tenant, HCA Healthcare, which contributes about 12% of annual base rent. As of this writing, the Yield is exactly 6.25%. PEAK did better than most REITs during the pandemic, resisting a dividend cut until Q1 2021, and cutting only from $0.37 to $0.30, where it remains today.

The balance sheet metrics are strong. PEAK carries a typical 32% debt ratio, with just 4.8% of its debt held at variable interest. However, PEAK sports a solid Debt/EBITDA ratio of 6.0, so earning out of its debt seems plausible. PEAK does well at converting revenue to FFO, supporting relatively aggressive FFO payout ratios. The company's FFO per share held essentially even at +1.7% in 2023, so interest coverage remains solid at 1.86.

PEAK is selling at a REIT-average (-17.3)% discount to estimated NAV, and a cheap Price/FFO ratio of 11.4, which is well below the Healthcare REIT average.

{kind=link}

Seeking Alpha Premium

{kind=link}

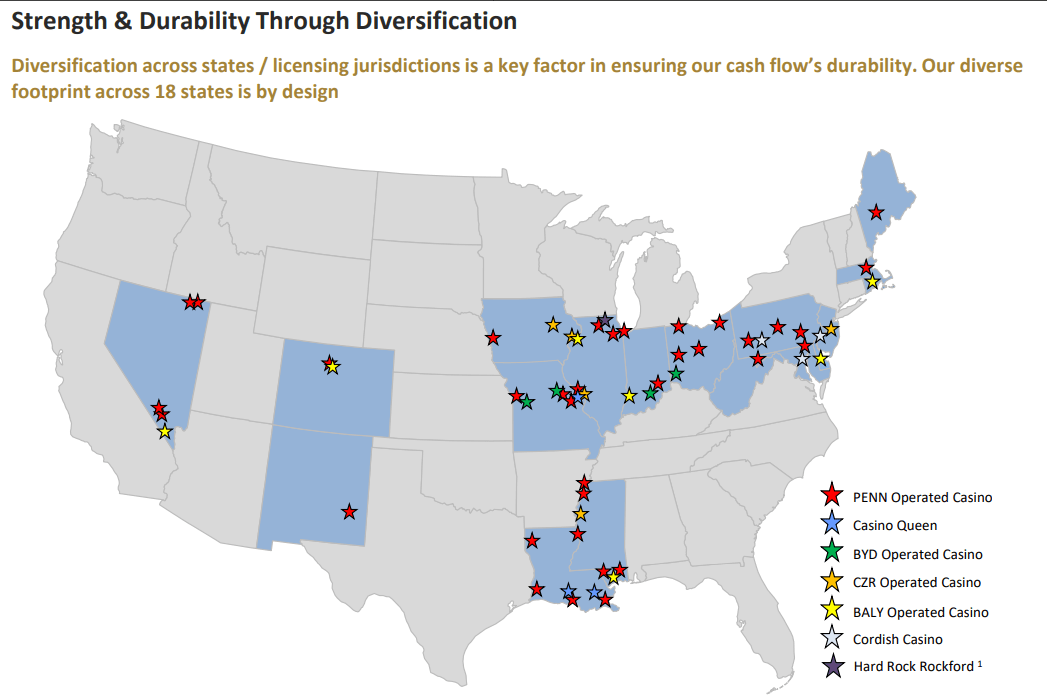

Gaming and Leisure Properties

Gaming and Leisure Properties ((GLPI)) is a casino REIT, going toe-to-toe with much larger VICI Properties ( VICI ). The company has assets in 18 states, mostly in the Eastern half of the country, and 88% of its revenue comes from publicly-listed tenants.

{kind=link}

GLPI investor presentation

As of this writing, the Yield is just over 6%, and unlike the vast majority of REITs, this company continued growing its dividend until Q4 2021. They slashed the dividend briefly, but then restored it 9 months later, at a higher level than before the cut.

There is good news and bad news in its balance sheet metrics. GLPI carries a typical 32% debt ratio, with just 3.0% of debt held at variable interest. This company excels with a Debt/EBITDA ratio of just 4.4, so growing out of its debt appears likely. Like others on this list, GLPI excels at converting revenue to FFO, supporting in aggressive FFO payout ratios. GLPI's handsome 7.1% growth in FFO per share in 2023, has driven its interest coverage ratio up to a rock-solid 3.32.

GLPI is selling almost exactly at estimated NAV (-0.4)%, and a modest Price/FFO ratio of 13.1, which is significantly lower than the overall REIT average.

{kind=link}

Seeking Alpha Premium

Bottom Line

As an investor, you have to decide how much risk of a dividend cut you are willing to run, and how much alpha in Yield makes it worth that risk. The higher the risk of a cut, the smaller the warranted allocation, and the more you need to keep a watchful eye on any of these companies you might choose to buy, particularly at the C- end.

This is still a great time to buy REITs . Yields are much higher than usual after the 2-year sell-off, and operating performance has continued strong , despite the 2-year sell-off. Balance sheets for most companies have been well-maintained, and in my opinion, Charlie Munger's gloom-and-doom forecast for commercial real estate has resulted in a lot of companies getting oversold, particularly outside the Office REIT sector.

Note: just because a company appears on this list, that does not mean I recommend buying shares. There are some on this list that I would not buy right now, and some I would never buy under any circumstances. You will need to do your own due diligence, as always, but hopefully, this list will save you a lot of time, by narrowing the field.

And remember, the opinion that matters most is yours. Because it's your money.

For further details see:

Rewarding You: 7 REITs Yielding High Goldilocks-Zone Dividends