REX - REX American Resources: Sell On Strong Q3 Results Q4 Won't Be Nearly As Good

2023-12-05 16:55:59 ET

Summary

- REX American Resources Corporation's stock rose 33% after strong Q3 results, despite flat revenue.

- The company's macro environment has deteriorated since the end of Q3. Q4 numbers are likely to be far weaker than Q3, creating an opportunity for shorts.

- Mitigating factors to a heavy decline in stock price include REX's strong balance sheet, capable management team and stock buyback program.

- There is a gap in the chart above $41.63 that is highly likely to get filled.

- Price target of $35-$40 for the near term.

REX American Resources Corporation ( REX ) rose 33% last Thursday to $49.02 after outstanding Q3 results that saw profitability skyrocket despite flat revenue. It has since pulled back to the mid-$40's, but I don't view this pullback is a buying opportunity. I believe that the bullish reaction on its stock price will be short-lived and likely represents a top for the foreseeable future. I don't wish to say anything bad about how this company operates and its management. Based on my research, it's quite well run with a strong balance sheet and responsible growth. I like the carbon capture initiative it is undertaking, which aligns with my views on how humans can realistically tackle climate change.

My bearishness stems from the fact that the macro environment that made its Q3 so strong has suddenly and drastically deteriorated. Almost immediately after Q3 ended and Q4 began, the price of ethanol has taken a steep dive. While the price of corn and natural gas remain contained, so that the company will likely remain profitable, margins will be considerably thinner than in Q3. I believe that this is an ideal time for longs to take profits and shorts to open up bearish positions.

Favorable conditions lead to a $1.49 EPS in Q3

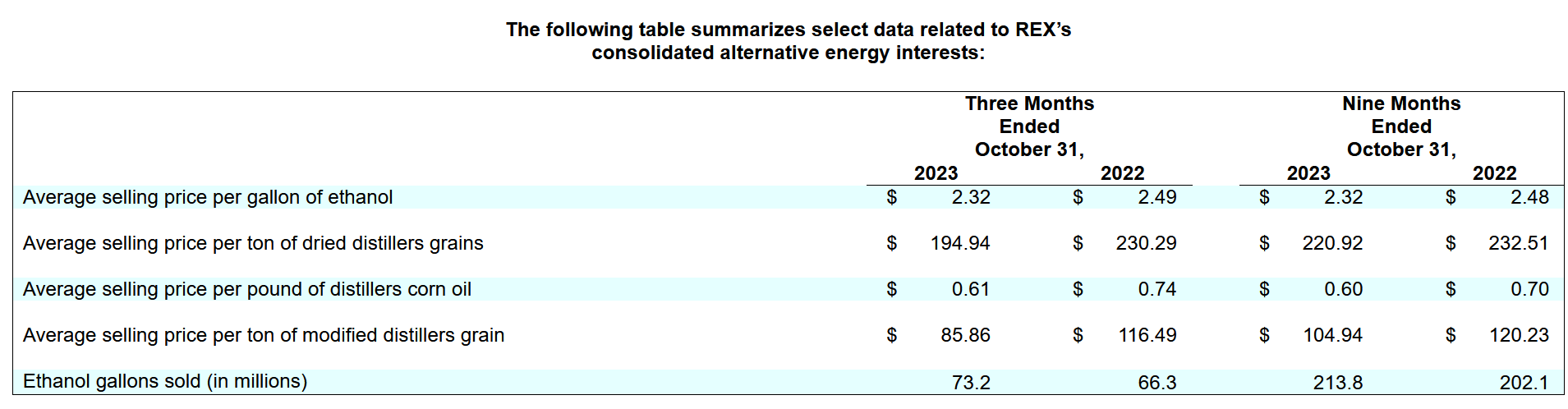

REX announced $221 million in revenue, essentially flat to Q3 2022. It sold 73.2 million gallons of ethanol in the quarter, a 10.4% increase over Q3 2022's result of 66.3 million, but that was offset by a lower selling price of ethanol, distillers grains and corn oil. A summary of the price and volume data is shown in the release:

{kind=link}

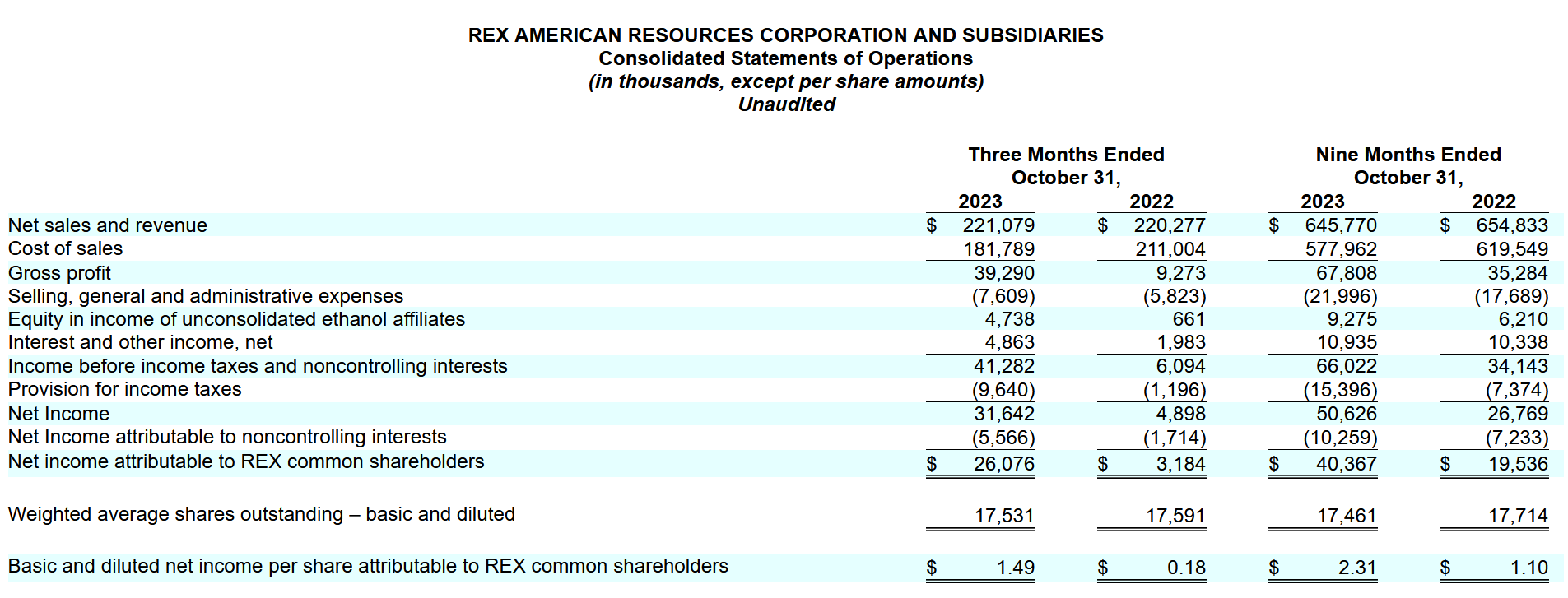

However, the general decline in commodity prices is what actually helped the company as its cost inputs - namely corn and natural gas - declined faster than the prices of the goods it was selling. This resulted in a 14% decline in cost of goods sold compared to Q3 2022. Gross profit increased from $9.3 million to $39.3 million and gross margin improved from 4.2% to 17.8%. This is what drove EPS to increase from $0.18 in Q3 2022 to $1.49 in Q3 2023:

REX's Q3 Earnings Press Release

{kind=link}

On the earnings call , management stated that margins have declined in Q4 compared to Q3, but that Q4 will have significantly better results than last year's Q4. That leaves a fairly wide range of an EPS that will be lower than Q3's $1.49 but higher than Q4 2022's $0.47 EPS. However, one can reasonably surmise that it will be much closer to the latter than to the former by having a look at recent commodity prices.

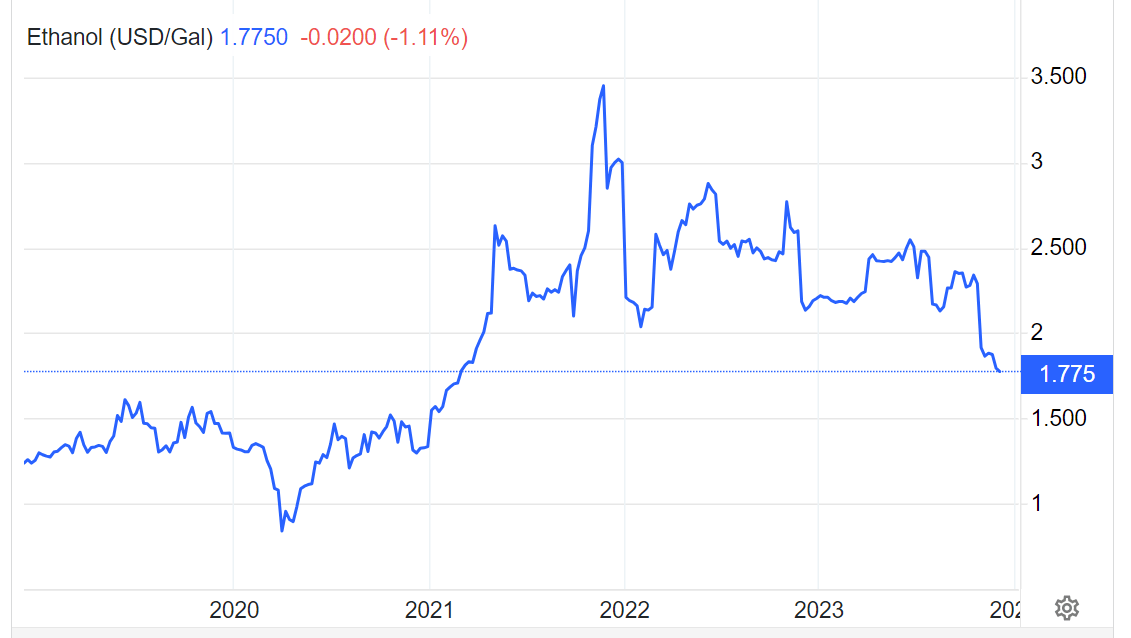

The price of ethanol has drastically declined in Q4; the price of inputs has stabilized

Since the beginning of November - right at the start of REX's Q4 - the price of ethanol has taken a plunge , dropping 22% from $2.28 to $1.78:

tradingeconomics.com/commodity/ethanol

{kind=link}

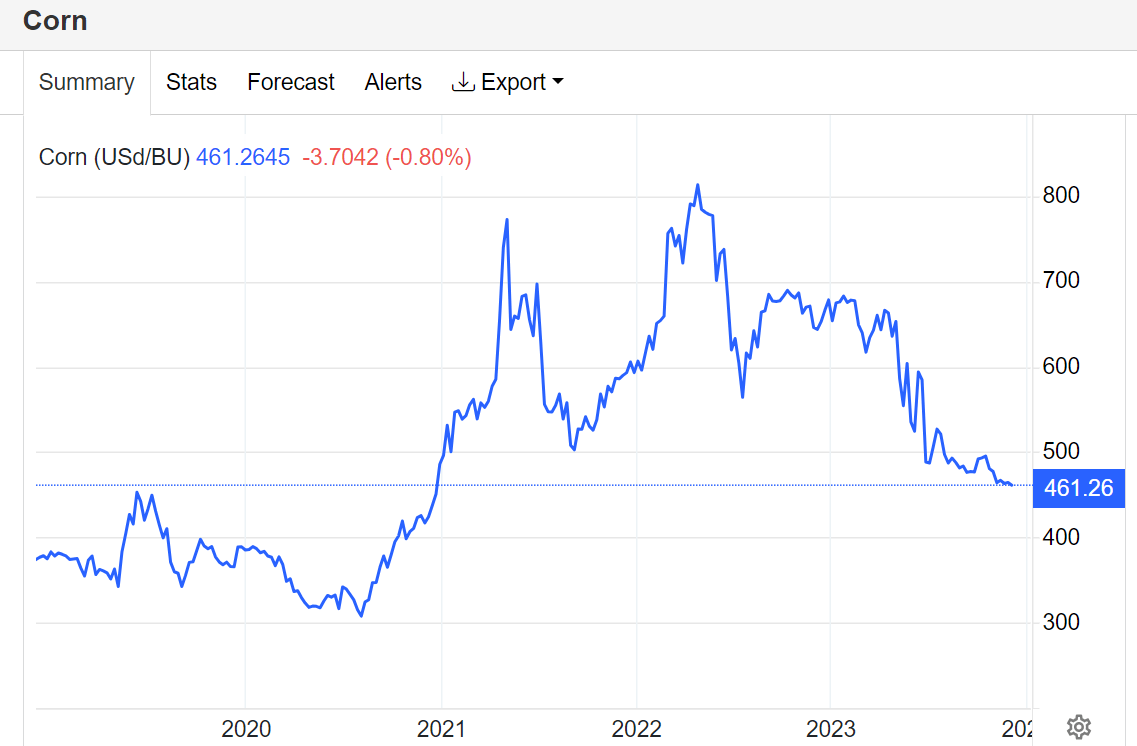

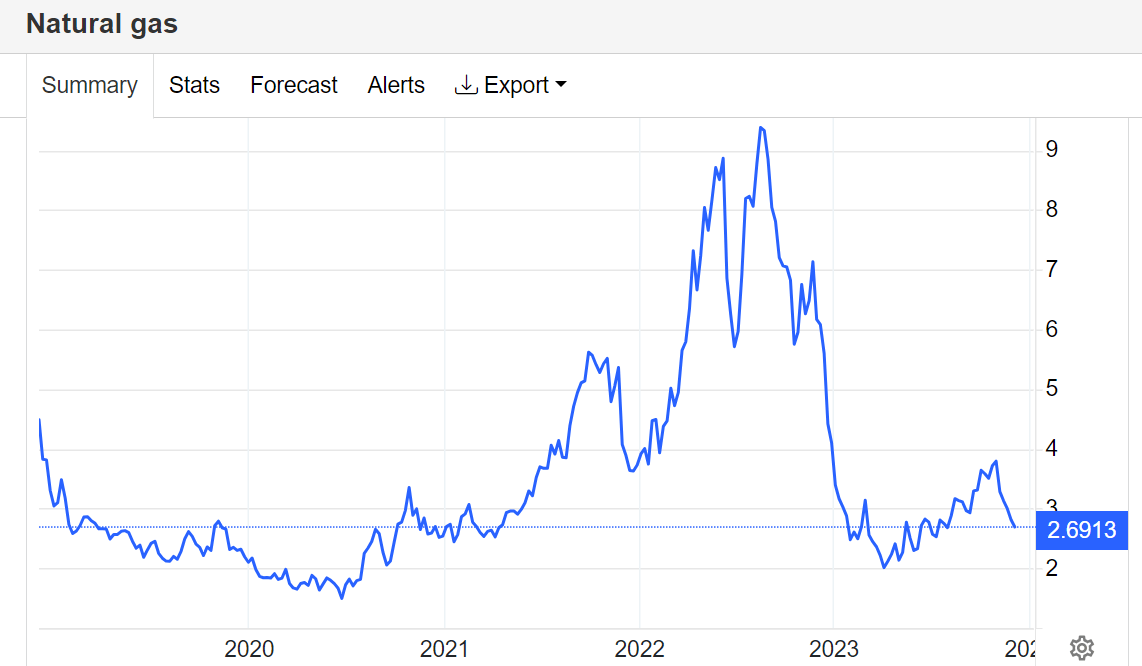

The price of corn has dropped 10% since then while natural gas has fluctuated wildly but so far remains at a price we saw for most of Q3. A 5-year chart of all three commodities paints a clearer picture why I believe that Q3 2023 was a fluke event that won't be repeated in Q4 or any time in the near future:

tradingeconomics.com/commodity/ethanol tradingeconomics.com/commodity/corn tradingeconomics.com/commodity/natural-gas

{kind=link}

{kind=link}

{kind=link}

Corn drastically declined in the first half of the year but has since been fairly stable. Natural gas has been weak pretty much all year. However, it started its heavy decline last December. By the end of REX's Q4 in January, the price of natural gas was below where it has been for most of November. That margin improvement caused by cheaper natural gas for the first three quarters won't be nearly as drastic for Q4. Finally, we see that the price of ethanol had more staying power compared to corn and natural gas for the summer and early fall, but has since taken a dive.

All three commodities have returned to prices seen in early 2021. For context, net income for the quarter ended January 2021 was $3.5 million on $126 million in revenue and for the quarter ended April 2021 was $7.8 million on $164 million in revenue. Though the company has since increased its production. At the time, the company's stock price and underlying commodities were increasing, recovering from recessionary pressures related to the COVID measures. It was seen as a good news story. Now the prices of these commodities are headed in the opposite direction on recessionary worries. I don't think it will be too long before the stock price follows.

Guidance on a company with unpredictable cash flows is fleeting. However, in every quarterly 10-Q, the company provides sensitivity analysis for the prices of the commodities that have the greatest impact on its income statement for the next 12 months, net of any hedging. Q3 was no exception:

{kind=link}

The two biggest drivers of net income variance are the prices of ethanol and corn, with the rest of the commodities having a relatively small impact on a quarter-by-quarter basis. A 10% change in the price of ethanol results in a $12.3 million pre-tax variance in net income per quarter, or about $9.5 million post-tax. A 10% change in the price of corn results in an $11.2 million pre-tax variance in net income per quarter, or about $8.6 million post-tax.

Q3 2023 achieved a $1.49 EPS on $26.1 million in net income. Q4 2022 achieved a $0.47 EPS on $8.2 million in net income. A quick sanity check on my methodology shows that a 22% variance in the price of corn ($500/bu in Q3 2023, $640/bu in Q4 2022) between these two quarters led to an $18 million variance in post-tax net income. And that's the variance we see in the overall number, with marginal impact from the fairly steady price of the other commodities between these two time periods.

If current commodity prices were to hold for the remainder of the quarter, the chart below estimates where Q4 could land based on analysis of the impact of the price of ethanol and corn.

My own estimates based on REX company filings

If ethanol remains around $1.78, its 23% decline in price will have an impact of around $22 million in erosion of post-tax net income when comparing to either quarter. Conversely, the tanking price of corn will have an even bigger positive impact on financials when compared to Q4 2022, resulting in slightly superior financial performance when comparing year-over-year results. However, as most of the win on the dropping corn price has already been banked in 2023, the relatively muted 8% decline in its price from Q3 results in only a $7 million win, resulting in net income that is far below Q3.

Commodity prices could fluctuate wildly between now and the end of January. So my estimate of around $0.60 EPS for Q4 will almost certainly be off. If the ethanol price continues to drop, expect a lower EPS, all other things being equal. However, if the price of corn continues to drop, expect a higher EPS, all other things being equal.

Conclusion and mitigating factors to my analysis

I believe that REX ran to $50 on the idea that it could produce an EPS of $4.00 or more for 2023. It has pulled back materially since Thursday as the market likely sees what I see. A dropping ethanol price pretty much guarantees that won't be the case. A $3.00 EPS for 2023 is much more likely. A 15x multiple leads to a $45 stock price, which is about where REX is right now. However, any prolonged margin crunch from the dropping price of ethanol and relatively stable prices of corn and natural gas will ensure that 2024 will not be as good as 2023. An EPS of $2.00 or less likely results in a stock price of $30.

There are some mitigating factors. Like I said previously, this company appears well managed. On the Q3 call , management mentioned that REX has an open share buyback available, but that it is not currently buying shares and only does so on dips. While that might not be something that traders who want to sell at $100 want to hear, that is astute financial management for the long term health of the company. The cash balance is strong and book value per share is approximately $28. Other than the 2020 COVID-assisted mini-crash, REX tends to bottom out at around 10% to 20% premium to book value. I also did not take into consideration the company's carbon capture project. I like the idea, but at this point in time I still consider it speculative.

One final consideration is on the technical analysis side. REX's 52-week and all-time high prior to Thursday's spike was $41.63. The spike created a gap in the chart above that price. I'm not big on technical analysis and edicts such as "all gaps must fill". But I can't ignore that many people do believe in this. Based on the price action since Thursday and what I find to be spurious reasons behind the spike in the first place, I have to admit that this gap has a very good chance at being filled.

All things considered, I am quite confident that REX will drop below $40 sometime in the near future. $32 is its likely floor, but I wouldn't short it until then. Especially considering the volatility of the commodity prices underlying its business. $35 to $40 seems like a fair price for this stock, with those targets fluctuating along with the prices of ethanol, distilled grains, corn and natural gas.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Top 2024 Long/Short Pick i nvestment competition, which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don’t want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

REX American Resources: Sell On Strong Q3 Results, Q4 Won't Be Nearly As Good