REYN - Reynolds: Margin Expansion Could Signal Upside

2023-12-06 03:22:06 ET

Summary

- Reynolds Consumer Products focuses on products for the kitchen with the offering including products such as aluminium foil, plastic wrap, and waste bags.

- The company has a current focus on improving margins through initiatives such as the Reynolds Cooking & Baking Recovery Plan and the Reyvolution, which seem successful in the Q3 report.

- REYN stock seems to be priced with a favorable price, as my DCF model estimates the stock to have a modest undervaluation.

Reynolds Consumer Products ( REYN ) manufactures and sells consumer products with a focus on products used in the kitchen - for example, the company sells aluminium foil, freezer paper, plastic wrap, baking cups, waste bags, and plastic food containers under brands such as Reynolds, Hefty, Diamond, and Presto. The company divides its operations into four segments - Reynolds Cooking & Baking, Hefty Waste & Storage, Hefty Tableware, and Presto Products:

Reynolds Q3 Earnings Presentation

After an IPO in early 2020 as the Covid pandemic started to arise, Reynolds' stock price has stayed mostly quite flat with some turbulence. The company pays out a dividend with a current yield of 3.47% , making the stock return near flat from the IPO:

{kind=link}

Financials

A Long-Term View

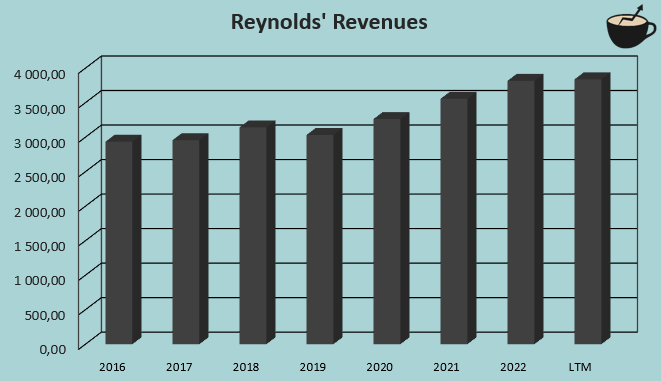

Historically, Reynolds has been able to achieve a very modest amount of growth. From 2016 to LTM figures, the company's revenues have grown at a CAGR of 4.1% through organic initiatives, building on the company's well-known brands.

{kind=link}

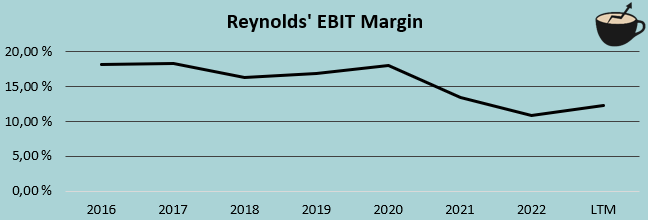

Margins don't seem as stable as the achieved revenues - Reynolds achieved an average EBIT margin of 16.0% from 2016 to 2022, but the current LTM figure is quite significantly below at 12.3% after the margin dropped in 2021 and 2022. Reynolds does have initiatives to improve the margin, though - the company has named a Reynolds Cooking & Baking Recovery Plan, working on selling volumes, gross margins, and operational efficiency.

{kind=link}

A Current Focus on Margins

Including the Reynolds Cooking & Baking Recovery Plan, Reynolds seems to have a large focus on improving margins. The company seems confident in margin expansion in coming quarters in the Q3 earnings call held on the 8th of November - the mentioned recovery plan, a favorable sales mix, and a prior Reyvolution - named operations improvement plan seem to have had an effect on Reynolds' margins. The company has already achieved a good amount of margin expansion, most notably in the reported Q3 result and in the Q4 outlook - in Q3, Reynolds' EBIT margin expanded impressively by 5.7 percentage points year-over-year, and analysts are expecting an EBIT margin expansion of 4.6 percentage points for Q4, in line with Reynolds' guidance for the quarter from a net income perspective.

It would seem that the margin expansion is largely a result of pricing increases; as margins have expanded, Reynolds' revenues decreased by 3.3% in Q3, and the company is expecting revenues to fall by 7% to 9% in Q4. Rising margins coupled with falling revenues should indicate raised consumer pricing. Reynolds' margin expansion so far has been mostly a result of rising gross margins instead of improved SG&A efficiency, pointing in the same direction. Still, Reynolds mostly points the good margin performance to cost initiatives in the Q3 earnings call, and the company's pricing increases are guided to only provide a 2% growth to revenues in 2023 according to CFO Michael Graham - the gross margin expansion is still mostly achieved through COGS improvements.

Good Margin Performance Could Signal Upside

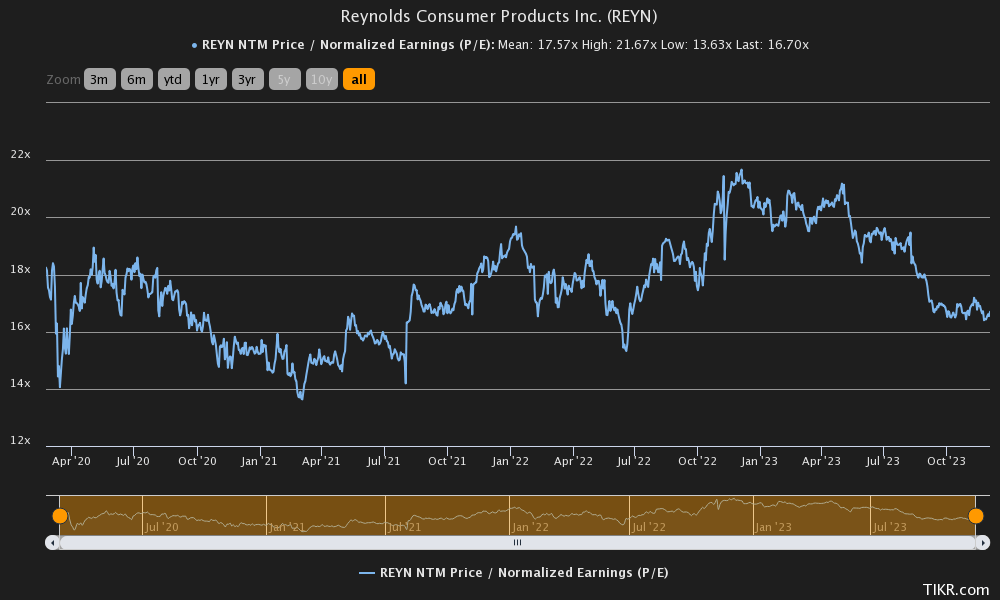

Currently, Reynolds' stock trades at a forward P/E multiple of 16.7. The company's average forward P/E figure of 17.6 from the IPO is close to the current one:

{kind=link}

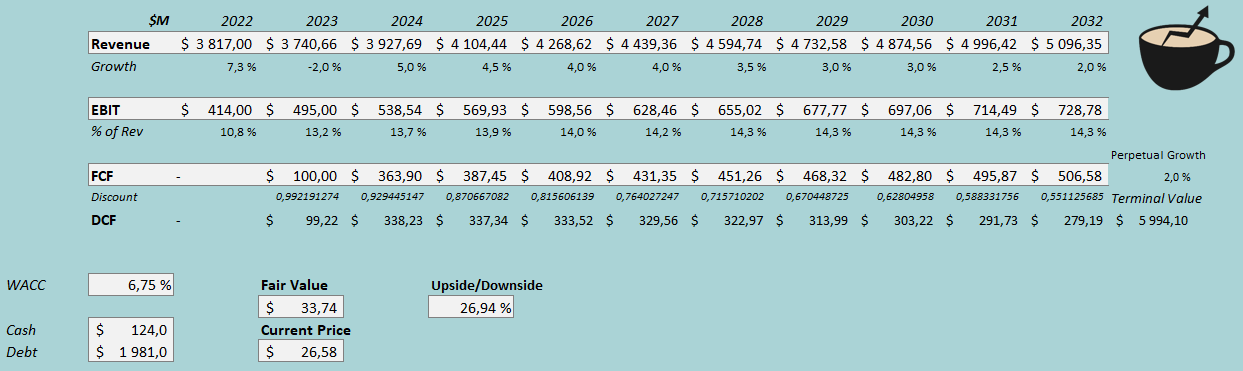

As usual, to estimate a rough fair value for the stock and to contextualize the valuation, I constructed a discounted cash flow model. In the model, I estimate Reynolds' operations to continue on the trajectory that seems to be laid out for the company. After weak revenues in H2 of 2023, I estimate a rebound of 5% in 2024 as volumes recover from the slight slump and Reynolds further grows its brands. After 2024, I estimate the growth to come down slowly into a perpetual growth rate of 2%, representing a revenue CAGR of 2.9% from 2022 to 2032.

My margin estimates in the DCF model represent good cost control in the future through the current initiatives - after a 13.2% EBIT margin estimate for 2023, I estimate the margin to have slight leverage into an eventual EBIT margin of 14.3%, achieved in 2028. The estimated 2028 margin still represents a level below Reynolds' 2016-2022 average, but for the time being, I believe that the estimate is a fair base scenario. Reynolds has a moderately good cash flow conversion, as the company doesn't seem to have excessive needs for further investments with modest growth.

The mentioned estimates along with a cost of capital of 6.75% create the following DCF model with a fair value estimate of $33.74, around 27% above the stock price at the time of writing - if Reynolds is able to execute further on margin expansion, the stock seems to have a good amount of undervaluation.

{kind=link}

The used weighted average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q3, Reynolds had $31 million in interest expenses. With the company's current amount of interest-bearing debt , Reynolds's annualized interest rate comes up to 6.26%. Reynolds leverages a fair amount of debt safely as the company's operations seem stable. I believe that a long-term debt-to-equity ratio estimate of 30% is fair for the company, which I use in the CAPM.

For the risk-free rate on the cost of equity side, I use the United States' 10-year bond yield of 4.29% . The equity risk premium of 5.91% is Professor Aswath Damodaran's latest estimate for the United States, made in July. Yahoo Finance estimates Reynolds's beta at a figure of 0.47 . Finally, I add a small liquidity premium of 0.3%, crafting a cost of equity of 7.37% and a WACC of 6.75%.

Takeaway

Reynolds has initiatives to expand the company's margins back to a level that's more in line with the achieved long-term performance. The reported Q3 results and Q4 outlook seem to suggest the margin expansion plans to be successful, although the quarters have seen decreasing revenues to couple with the margin expansion. A further good performance with margins and a growth near the company's historical rate would seem to estimate upside for the stock, as my DCF model estimates the stock to have an upside of 27% at the time of writing. I see Reynolds' mostly stable performance and the undervaluation as signs of a favorable risk-to-reward - for the time being, I have a buy rating for the stock.

For further details see:

Reynolds: Margin Expansion Could Signal Upside