BCRX - Rezolute: Negative EV Opportunity Initiating A Phase 3 Ultra-Orphan Pediatric Study

2023-11-09 18:57:06 ET

Summary

- Rezolute is a clinical-stage biotechnology company focused on metabolic diseases related to glucose control.

- Their lead asset, RZ358, is a monoclonal antibody being developed as a treatment for hyperinsulinism, a condition characterized by excessive insulin production.

- The Company is trading for 50% of cash, about to initiate a phase 3 study in an ultra-orphan indication, with significant potential upside on a valuation basis.

Rezolute - Overview

Rezolute ( RZLT ) is a clinical-stage biotechnology company focused on metabolic diseases relating to the control of glucose. The lead asset, RZ358, is a human monoclonal antibody that binds to an allosteric site on the insulin receptor and down-regulates the activity of the receptor. The down-regulation of the insulin receptor reduces the consumption of glucose. RZ358 is being developed as a treatment for patients whose pancreas generates too much insulin, creating a constant state of hyperinsulinism (“HI”). Patients with HI suffer from extreme hypoglycemia, which increases the risks of neurological and developmental issues in children. HI is currently treated with glucagon, diazoxide, somatostatin analogues and/or partial pancreatectomy

The Company’s second asset is RZ402, an oral inhibitor of the kallikrein pathway, which has the potential to reduce inflammation and cell damage in the vasculature. RZ402 is specifically being developed to prevent the progression of diabetic macular edema (“DME”).DME is currently treated with anti-VEGF injections into the eye, or with laser surgery.

Rezolute’s original form was AntriaBio, which become public through a reverse merger in January 2013. The original program, AB101, was focused on creating a pegylated form of insulin to allow for once-weekly dosing for insulin. The original plan was to file an IND in 2015. The Company made the decision to build its own manufacturing facility, which delayed the IND filing to mid-2017.

As of late 2017, the Company shifted its strategic focus. It in-licensed RZ358 and RZ402, and halted its AB101 program. Additionally, the Company changed its name form AntriBio to Rezolute. In early 2019, the Company received approximately $48M from a private placement and subsequent option exercise from Handock, Inc. and Genexine, Inc., two Korean companies. In Fall 2020, the Company raised another $38M through a private placement, and effected a 50:1 reverse stock split, as a step toward an uplist to NASDAQ. In May 2022 on the heels of good phase 2 data, the Company raised $117M through a registered direct offering and concurrent private placement.

As of June 30, 2023, the Company had $118M in cash, which funds the Company until mid-2025 at the current burn rate. The Company lists 36.6M common shares outstanding as of June 30, 2023, but also has approximately 14.6M prefunded warrants outstanding, which means that there are effectively 51.5M shares outstanding.

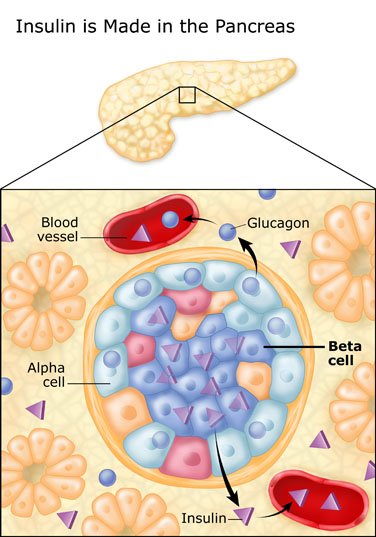

Hyperinsulinism

HI is a disease that occurs because of a mutation in one or more genes related to the control of insulin secretion from the beta cells inside of an islet cluster in the pancreas. In the US, it occurs in between 1:28,000, or approximately 3,500 children. There are over 10,000 patients worldwide.

UCSF

Figure 1: Islet Cell Cluster – Insulin and Glucagon Production Source - UCSF

{kind=link}

Normally, insulin production is high when the blood sugar levels are high, and is low when blood sugar levels are low. People with HI produce high levels of insulin all the time. In infants, symptoms can include poor feeding, discoloration of the skin, fast breathing and, in worst case scenarios, a seizure or a coma. In older children, symptoms can include hunger, sweating, agitation, a seizure or a coma. The child’s neurological and physical development is negatively impacted.

Screening for HI includes a genetic test to identify a mutation in one of the genes known to induce HI. Additionally, the child can undergo an assessment of the control of their blood sugar and insulin, and a glucagon tolerance challenge.

Medications for treatment include diazoxide and octreotide to reduce insulin production, and glucagon to increase blood sugar. Monitoring the disease has improved with continuous blood glucose monitors.

Once diagnosed, the child’s pancreas could also be assessed under PET-MRI to determine if the HI stems from a small section of the pancreas, or from the whole pancreas. If the issue comes from a particular area of the pancreas, a partial pancreatectomy could treat the condition. Source – Texas Children’s Hospital .

RZ358

Licensed from XOMA in 2017, RZ358 is a monoclonal antibody that binds allosterically to the insulin receptor on cells throughout the body, the highest density being in the liver, in fat cells and in muscle tissue. When insulin binds to the insulin receptor on a cell surface, it opens a channel on the cell that allows glucose to be absorbed by the cell. RZ358 does not interfere with the binding of insulin to the insulin receptor – it appears to attenuate the effect, reducing the amount of glucose a cell absorbs.

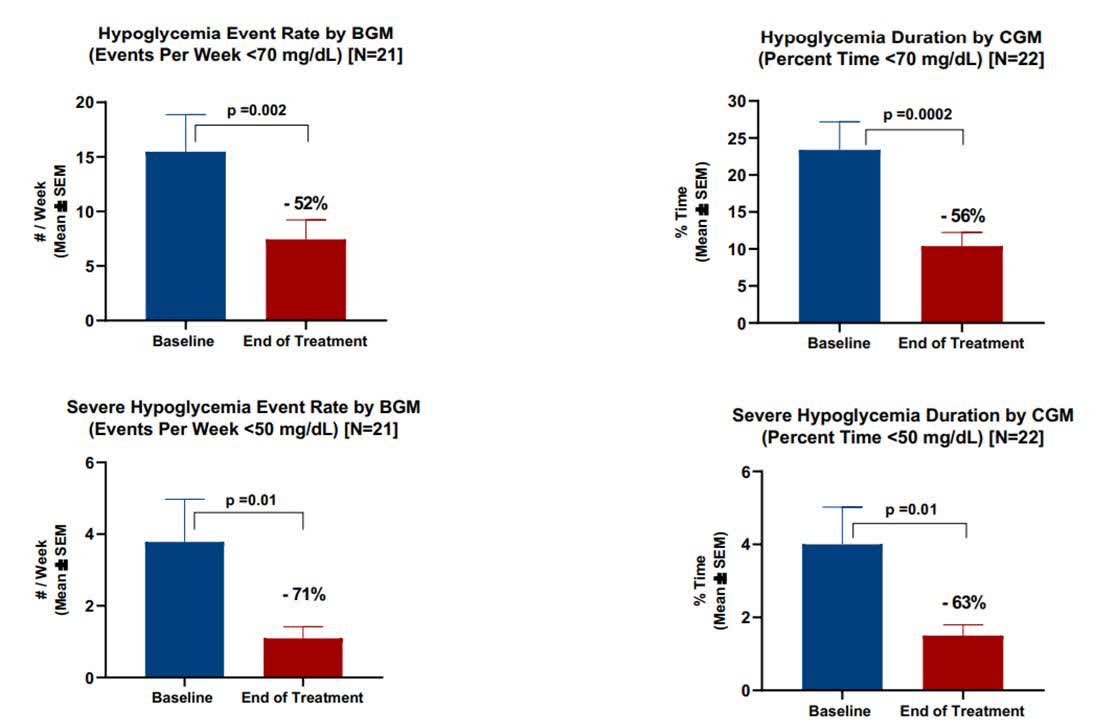

In HI, cells constantly absorb insulin, reducing blood glucose levels. RZ358 has been shown a Phase 2b study in 23 children with average age of 6.5 years, to statistically reduce the number of hypoglycemic events per week and reduce the duration of time in hypoglycemia (< 70 mg/dL blood glucose).

{kind=link}

Figure 2: Results from RIZE Study Source – Company Presentation

In Figure 2, the data from all cohorts are clustered together. In certain dose levels, the effect appeared to be stronger, although the numbers in each cohort are small. The Company provided multiple samples of data from the continuous glucose monitoring system – a day in the life.

{kind=link}

Figure 3: Day in the Life – Glucose Levels, Pre-dose Source – Company Presentation

{kind=link}

Figure 4: Day in the Life – Glucose Levels, Post-dose Source – Company Presentation

It is clear from the pre-dose and post-dose glucose levels that the glucose levels are in the ideal range a much greater percentage of time. The child was below the threshold level for most of the time during sleep, and RZ358 appeared to solve the issue. The Company likely chose the most ideal charts to publish in their presentation – but the overall data is quite compelling.

The next step for RZ358 is a Phase 3 study. The Company is expected to announce a final protocol and initiate the Phase 3 study by the end of 2023. The study is expected to take 1.25-1.5 years, which suggests a top-line read-out around Q2 2025. Unless it occurs sooner, this data should create an outsized inflection point for the value of the Company.

The Hair - FDA Partial Clinical Hold

One of the potential culprits of the stock’s drift down could be the interactions with the FDA regarding a safety signal in a rat model performed by XOMA well before the Company licensed the drug. In the preclinical package, microvascular liver injury was seen in a rat toxicology study. In a similar study performed in monkeys, there was no safety signal in doses 10 times higher than those of the rats, and 4 times the highest dose seen thus far by a human. In all of the human trials to date, the has been no sign of liver injury.

The Company is continuing to interact with the FDA to resolve their concerns. Concurrently, the European regulatory agencies have reached agreement with the Company to dose patients as young as 3 months old. The Company is expected to initiate the Phase 3 study before the end of 2023.

Having spoken with management on this issue, and having been the recipient of a clinical hold from an ultraconservative FDA in the past, I fully appreciate and understand the predicament. I applaud the Company for moving forward in the jurisdictions that have weighed the benefit to patients versus the potential risk with a different scale. With additional data, the FDA would likely release the clinical hold and allow enrollment at US sites.

HI Caused by Cancer

In rare cases, HI can also be caused by a tumor in the pancreas that over produces insulin, or by a tumor that secretes IGF-2, which stimulates insulin production. In these scenarios, RZ358’s mechanism of action suggests it could be effective in mitigating the effects of HI in these patients as well.

A New England Journal of Medicine article was just published regarding the use of RZ358 in a patient with a pancreatic tumor who was experiencing HI. The patient was in the ICU and was in need of continuous glucose IV. After eight treatments over 75 days, the patient’s glucose levels stabilized in the range of normal and the patient was able to go home. A single patient does not make a drug, but it does provide a signal of potential efficacy in a new indication. If the Company is able to prove efficacy in a small proof of concept study in this indication, then I believe it would add substantial potential upside.

Diabetic Macular Edema

Left untreated for a long time, DME can lead to reduced vision, and potentially blindness. Excessive blood sugar causes inflammation in the capillaries. In the area behind the retina called the macula, inflation can cause leaky vessels from microaneurysms, creating edema. This edema can reduce visual acuity, and eventually cause blindness if not corrected.

A common treatment for DME is an anti-VEGF, which helps to prevent the growth of new blood vessels. Anti-VEGF is also a very common treatment for many types of cancer. For DME, the drug is injected into the eye monthly. Long term studies are sparse, but it appears that visual acuity improves initially, for up to 2 years; and then the patient’s vision deteriorates by year 9 .

Mayo Clinic

Figure 5: DME Visualization Source – Mayo Clinic

RZ402

Licensed from Active Site Pharmaceuticals in 2017, RZ402 is a small molecule plasma kallikrein inhibitor (“PKI”). While the PKI pathway has a number of potential indications, the Company is first focused on DME. The theory is that, by inhibiting the formulation of kallikrein, RZ402 can reduce levels of bradykinin, which is a pro-inflammatory, pro-coagulant peptide implicated in process of creating the vascular leakage.

In Q1 2024, the Company will have Phase 2 data on RZ402 . The trial is expected to enroll 100 patients, who will be randomized to one of 3 doses and placebo for 3 months. The primary endpoints are safety and change in central subfield thickness, which is a measurement of the level of edema. A reduction in thickness can be correlated to improvement in vision .

To date, the best data the Company has on the potential efficacy of RZ402 is in a rat study . While supportive of the thesis, animal models are not real until the effect translates into humans. The Company’s trial appears well designed to validate RZ402’s potential for efficacy in DME. A reduction in retinal thickness in DME patients is highly correlated to the treatment of the disease. The Company will know what is possible with RZ402 in Q1 2024.

If there are significant differences in central subfield thickness after the 3 months, with no safety signals, then the Company’s next step is likely a Phase 2b where they test for visual acuity improvement after 1-2 years, to validate that improvements in retinal thickness with this mechanism does indeed change visual acuity. Perhaps they would include an arm where RZ402 is co-administered with an anti-VEGF therapy to understand the potential for synergies. Additionally, if successful in DME, there are other indications that the Company, or a strategic partner, could pursue. Damage from inflammation is not limited to the back of the eye.

DME Kallikrein Competition

Recently, BioCryst ( BCRX ) announced a collaboration with Clearside Biomedical to develop their kallikrein inhibitor, avoralstat, for DME. Avoralstat would be injected into the suprachoroidal (layer between the choroid and the sclera) space in the eye with Clearside’s SCS Microinjector. Avoralstat failed a phase 3 study in hereditary angioedema. The low dose was effective, but the higher doses had gastrointestinal (“GI”) adverse events. The direct injection of avoralstat into the suprachoroidal layer would mitigate any potential for systemic adverse events.

The launch of this collaboration supports the thesis behind RZ402. If they both get to market, assuming there is no black box warning for GI risk with RZ402, then one might assume that RZ402 as a daily pill would be more palatable to patients than routine injections into the eye with avoralstat. That competitive positioning falls into the nice-problem-to-have bucket for the RZLT.

Management Team

The Company has a very experienced management team.

| CEO & Acting Chairman |

| Nevan Elam, JD

|

| Chief Medical Officer |

| Brian Roberts, MD

|

Only Mr. Elam and Dr. Roberts are Form 4 filers. Mr. Elam currently also serves as the CFO, supported by an experienced finance professional from Fibrogen and Gilead. The senior management team all come from top bay area biotech companies. From the pedigrees, the team appears quite capable of executing.

Proforma Model

When modeling the Company, I have made the following assumptions:

- Consistent R&D and G&A expenses until mid-2025, when RZ402 Phase 3 begins.

- In FY 2026, begin Sales and Marketing expenses for expected launch of RZ358 in FY 2027.

- Peak penetration of 25% for RZ358 and 5% for RZ402.

- Starting @ $250K per year gross revenue for RZ358 in the US, and $100k per year outside the US; and starting @ $20K per-year gross revenue for RZ402, with 5% COGS for both products.

- $50M raise in FY 2025, and $100M raise in FY 2026.

{kind=link}

While the Company currently has a large cash balance, it also burns around $50M per year. Note that the company is on a June 30 year end, so FY 2023 ended in June 2023. To get to being cash flow positive from commercial sales, assuming both products obtain FDA approval and RZLT does the commercial launch themselves, I estimate that the Company will need to raise ~$150M by the end of FY 2026 to commercially launch their programs (odds are low that the would not be taken out prior to a commercial launch).

By the end of FY 2024, assuming a 20% cost of capital and a 20% probability of success across both programs (being very conservative), I ascribe a NPV of approximately $240M, which converts to a stock price of approximately $4.5.

After the Phase 2 read-out from the RZ402 study, and the FDA sign-off on the protocol for the Phase 3 of RZ358, I would incrementally increase the probability of success ascribed to the model. In 2026 with a successful study and the estimated dilution, the model suggests a $18 stock price. If NPV valuations were important, then a stock price today between $3 and $5 would not be unreasonable.

Analyst Coverage

The Company is covered by Cantor ($5 target), JMP ($8 target), HCW ($14 target), Cannaccord ($17 target) and Jefferies ($4 target). The price targets suggest substantial upside, assuming people believe in the valuations that set price targets.

Insider Buying Activity

The CMO purchased shares in May 2022 (21,052 @ $3.80) and July 2023 (5,000 @ $1.89). A few directors also purchased shares in May 2022. At the current levels, assuming they are not in possession of material, non-public information, it would be nice to see the whole board and management team belly up to the bar. That could clear out the seller(s) who have been happy to sell down to ~$1 over the last few months.

Major Holders

The schedule 13 filers are as follows:

| Fund |

| Beneficial Ownership |

| % of Common & Prefunded Warrants |

| Date Reported |

| Federated Hermes, Inc. |

| 7,550,274 |

| 14.8% |

| Jun 30, 2023 |

| Handok |

| 5,942,617 |

| 11.6% |

| Jun 30, 2023 |

| First Manhattan Co. LLC |

| 3,623,078 |

| 7.1% |

| Jun 30, 2023 |

| Vivo Opportunity LLC |

| 3,242,842 |

| 6.3% |

| Oct 5, 2023 |

| Stonepine Capital, LP |

| 3,072,476 |

| 6.0% |

| Jun 30, 2023 |

| Blackstone Inc. |

| 1,537,684 |

| 3.0% |

| Jun 30, 2023 |

| Vanguard Group |

| 1,407,652 |

| 2.8% |

| Jun 30, 2023 |

| Caxton Corp |

| 1,318,967 |

| 2.6% |

| Jun 30, 2023 |

| Sphera Funds |

| 1,155,897 |

| 2.3% |

| Jun 30, 2023 |

| Nantahala Capital |

| 769,606 |

| 1.5% |

| Jun 30, 2023 |

All and all, the list of institutions is impressive. Federated Hermes filed their acquisition statement for ~15% of the company as of October 31, 2020. By October 2021, Federated owned ~21%. Caxton, a well known biotech investor, owned 6.6% of the Company as of October 8, 2020, then was up to 8.6% by the end of 2021 . By the end of 2022, Caxton’s % dropped to 4.99% . Stonepine crossed the reporting line in December 2021 @ 5.1%. , and was up to 8.2% by the end of 2022 . First Manhattan crossed the 5% line near the end of 2022, hitting 8.5%. A new entrant into the 5% plus pool jumped in to the stock in October of this year- Vivo Opportunity owned 8.8% as of October 5, 2023 . Nantahala has been in a number of well-timed deals in the biotech space this year – great one to see on the list. In total, 24M shares are held by reporting institutions, and 8M are held by the board and management (including Handok). Given there are only 36M common shares outstanding, and many other shares are likely in the hands of smaller, long term holders, less than 10% of the float is probably available for trading on any given day.

Potential Risks and Potential Surprises

1) Generic CMC Disclaimer: FENC , PTLA , and many others have had CRLs issued by the FDA based on manufacturing issues. Manufacturing antibodies has become relatively routine. As long as the Company uses an experienced CMO and keeps vigilant on the controls and procedures, then there are low odds of a manufacturing-related CRL when the time comes. That being said, more than a few companies have had issues because they did not prioritize their CMC efforts. The risk will be mitigated after their initial manufacturing site passes its FDA inspection without being issued a Form 483.

2) Financing: The Company burns approximately $50M per year, and that may rise as the Company embarks on the RZ358 phase 3 and decides to progress RZ402 into phase 3. Depending on the outcome of the RZ402, and the Company’s desire to accelerate RZ358 into tumor associated HI, the Company may need more money in early 2025. Given the quality of its investors, it would likely be easy to top-up if needed by passing around the hat. It is doubtful, however, that they would dilute at levels below cash and there would be no need for financing in the near term. .

3) Valuation: Since the start of the pandemic, classical NPV valuation methodologies have been disconnected from public company market caps. This is especially true in the small cap space. In June 2022, 20% of biotech companies were trading for less than the cash on their balance sheet. This disconnect may persist for a long time. Therefore, the models used to generate the stock price estimates in this report should be seen as directional. Financing risk out-weighs biology risk right now.

4) FDA / Regulatory Risk: Given the clinical hold placed on the program by the FDA, one could assume that the worst-case scenario has already played out. However, as the Company proceeds with clinical trials in other regulatory jurisdictions, the Company will be watching out for this safety risk. If the phase 3 trial enrolls with no liver injury, then the risk will be fully mitigated. Perhaps safety data from an interim DSMB meeting would check the box with the FDA and release the clinical hold in time to enroll a few US patients. If the Company performs a study that shows why the issue occurs in rat model, but not in monkeys or humans, then the risk will be mitigated. Until the risk is mitigated, it will likely be an overhang on the Company.

Conclusion

RZLT has one question mark with its lead program with the FDA. That question is a non-issue with the EMEA. RZ358 has proven that it is safe and effective in a phase 2 study in HI. Some well regarded funds wrote big checks to fund the company through its phase 3 program, which is expected to start before the end of 2023, and read out in early 2025. RZ402 will have phase 2 data in Q1 2024. If it shows reduced retinal thickness in the drug arms, then RZ402 has a path to approval on DME, as well as many other diseases enhanced by microvascular inflammation, like diabetic nephropathy.

With $120M in cash and cash equivalents, the Company has no need to raise money in the near term. The RZ402 phase 2 could be a potential catalyst in early 2024. The announcement of enrolling the first patient in the RZ358 phase 3, the FDA’s decision to release the clinical hold for US sites, or adding another well-known biotech investor’s name to the list would also be catalysts. One never knows what will get the stock back to a stock price more in line with a DCF model, but I believe patience will benefit any investor in this name. Ultimately, data will drive approval, and potentially an acquisition. Once approved, RZ358 would benefit patients with this rare condition, and provide substantial return to patient shareholders.

For further details see:

Rezolute: Negative EV Opportunity Initiating A Phase 3 Ultra-Orphan Pediatric Study