SPG - RFI: A Sell Setup

Summary

- RFI has done remarkably well over the long haul.

- We are more interested in what the next 12 months will bring.

- Downside risks outweigh upside potential.

The Cohen & Steers family has plenty of closed end funds that allow you to capitalize on their real estate expertise. Many of these have a legion of admirers and the funds have in general done well for their investors. The one we want to look at today is Cohen & Steers Total Return Realty Fund ( RFI ), a fund we argue is a sell today.

The Fund

According to its website, RFI's primary focus lines up well with our own.

The investment objective of the Fund is to seek to achieve a high total return through investment in real estate securities. Real estate securities include common stocks, preferred stocks and other equity securities of any market capitalization issued by real estate companies, including real estate investment trusts (REITs) and similar REIT-like entities.

Source: Cohen & Steers- RFI

The art of total return investing has taken a back seat in all this yield chasing we got as a result of low rates. But it is nice to see funds, even ones that pay a high distribution, making it their primary priority. The fund has been around for a long, long time and was started in September 1993. It has about $308 million in assets, which is a good size for a closed end fund. The moderate size allows expense ratios to be contained while giving the fund enough room to generate alpha.

Holdings

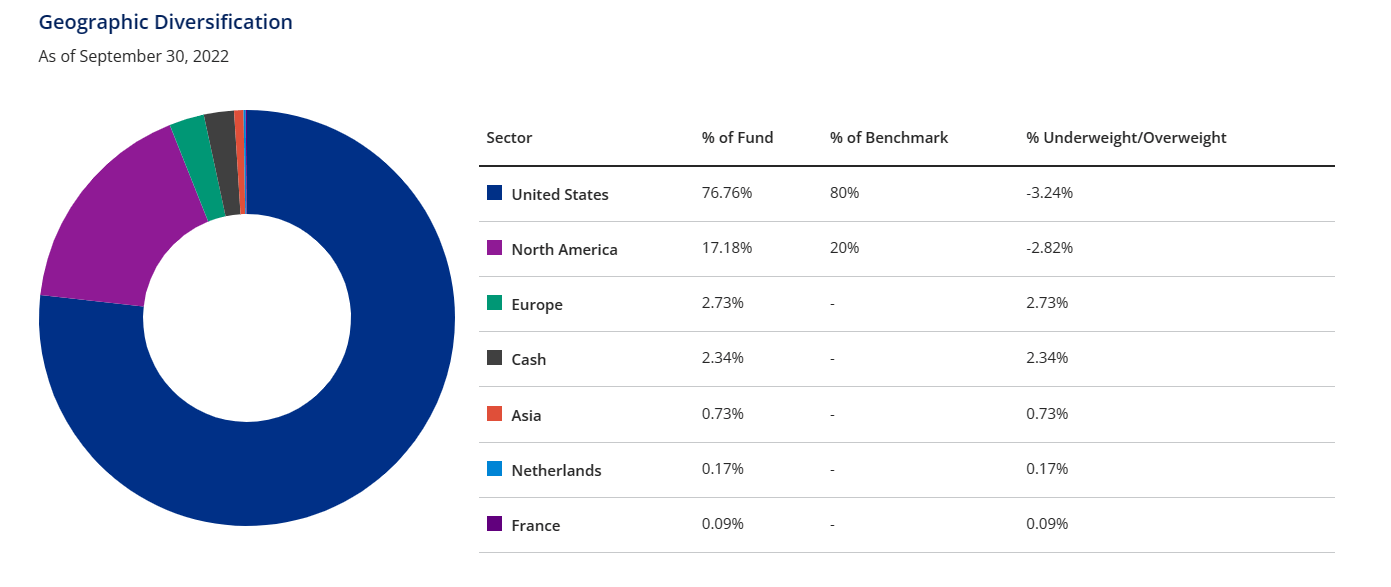

The fund stays primarily in the US, and that has offered it some advantages over others like Aberdeen Global Premier Properties Fund ( AWP ) over the last 12 months.

{kind=link}

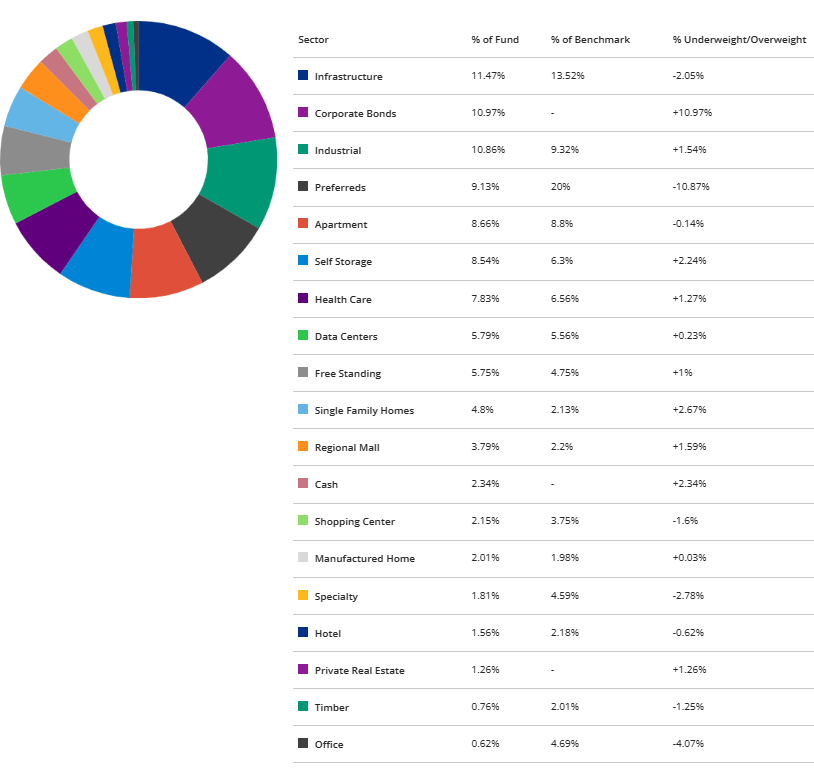

The fund also shows its sector allocations in a rather unique way. The uniqueness comes from the fund showing its percentages in relation to the benchmark and highlighting whether it is underweight or overweight a sector. This may sound like a rather obvious thing to do but it is a rather rare find. Most funds tend to talk about this weightage in their semi-annual or annual reports but it is really rare to see this shown as below.

{kind=link}

RFI's blended index for its benchmark is defined as the following.

Blended Index: The linked blended benchmark consists of 80% FTSE Nareit Equity REITs Index and 20% ICE BofA REIT Preferred Index through 3/31/2019. Thereafter, it consists of 80% FTSE Nareit All Equity REITs Index and 20% ICE BofA REIT Preferred Index

Source: Cohen & Steers- RFI

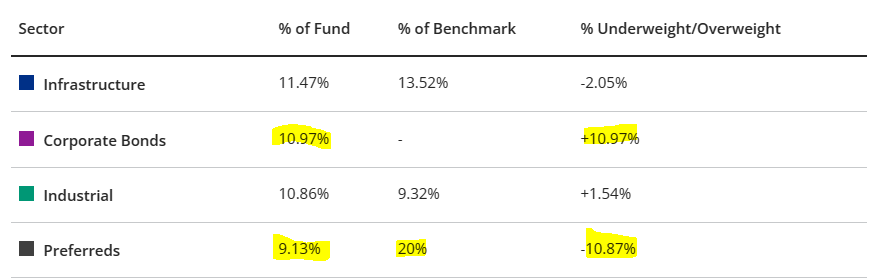

Examining the positioning in relation to the benchmark, a couple of things become clear. The biggest deviations come from having corporate bonds versus preferred shares.

{kind=link}

This is a duration-risk neutralizing move as preferreds tend to get far more damaged in rate hikes than limited duration bonds. Preferreds are also chased more by the retail crowd and hence can often get expensive relative to the bond equivalents. We recently showed how Simon Property Group's ( SPG ) preferred shares ( SPG.PJ ) were hopelessly overvalued and designed for 2% annual returns. That same article also showed how corporate bonds for SPG were far better and offered decent returns. RFI is likely just capitalizing on this theme.

The other notable call is the big underweighting of the office sector. That sector has been the worst performing among REITs and the underweighting there has definitely helped. We also remain bearish on primarily single tenant office REITs, like Orion Office REIT ( ONL ), where we see another 50% downside as possible in 2023.

Yield

RFI pays a strong monthly distribution of 8 cents, which works out to a 7% yield at the current price. This is lower than some of the other closed end funds in the space but quite competitive.

It does not hurt RFI's case that the two shown above are very likely to cut their distributions in 2023 (in our view) .

Performance

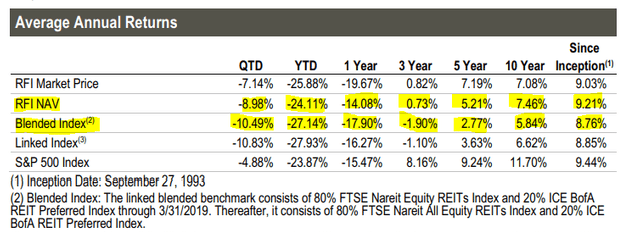

RFI has beaten its benchmark over every single timeframe, at least until September 30, 2022.

{kind=link}

That is an incredibly rare feat. Even strong long term winners will tend to have periods of underperformance. That is the nature of the beast. Keep in mind when you compare RFI to any other REIT fund, that the latter may not be a blended REIT/Preferred mix. RFI should have lower volatility compared to almost any closed end REIT fund simply because of that. It will also have lower volatility as it is one of the rare funds that does not use leverage. RFI's performance is also stellar relative to AWP and CBRE Global Real Estate Income Fund (NYSE: IGR ).

3 Reasons To Sell

While we appreciate the performance and the lack of leverage, the fund has definitely given us some reasons to give it a sell rating.

The first here being that we don't believe that the REIT indices have bottomed. We see more valuation compression ahead for most of RFI's top holdings.

CEF Conect

Some like Digital Realty Trust Inc. ( DLR ) have substantial downside ahead and we completely agree with Jim Chanos' thesis on this one .

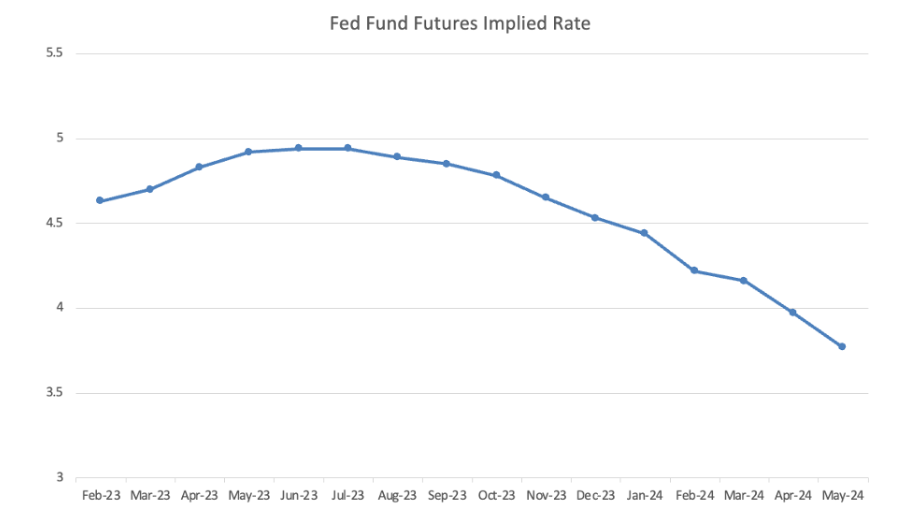

The second reason is that we think the REIT sector's recent rally has made it quite vulnerable to the Federal Reserve not cutting rates in 2023. Fed Fund Futures are pricing in some heavy cutting in the back half of 2023 and we don't see that happening at present.

Fed Fund Futures-Forex analytix

{kind=link}

We believe the Fed will stand pat (as they should) in the face of mild economic weakness as inflation is still too high. If this curve turns out correct, then you really, really would not want to own REITs anyway. The reason is that economic activity will have collapsed and REIT valuation compression will take a whole new dimension.

Finally, the fund has gotten really expensive. 12.46% premium is a ridiculous amount and sets you up for a real disaster if things go south.

We saw this level of premium only 4 times in the fund's history. In January 2013 and then again April 2013. From the January 2013 timeframe you scored a price return of negative 20% 1 year out.

We also saw it in late 2021. What followed was not pleasant.

And here we are with a 12.46% premium. The Z-score also looks scary.

CEF Conect

If we see the fund trade at a 5% discount to NAV (which it often has), alongside a 15% drop in the index, we could see a 30% decline dead ahead. Buyer beware. We rate the fund a Sell.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

RFI: A Sell Setup