RFI - RFI: The Unleveraged CEF From Cohen&Steers

Summary

- RFI is a REIT equity focused CEF from the Cohen & Steers suite.

- The fund has an 80/20 allocation between REIT equity and financials preferred shares.

- The vehicle runs virtually no leverage and has a 5-year standard deviation lower than the S&P 500.

- The fund has been in the market for almost three decades and has been able to consistently generate annualized total returns in excess of 7%.

- This article covers CEFs from our suite of products - we focus on macro portfolio allocation, CEFs, and yield-generating options strategies, targeting overall yearly portfolio returns of 9%+.

Thesis

We have recently started a review of a number of Cohen & Steers funds, having had a look at ( RLTY ) here , and at ( RNP ) here . This article will focus on the Cohen & Steers Total Return Realty Fund ( RFI ), the unleveraged CEF from the suite (technically the leverage ratio is 1.5%, but that is done for regulatory purposes rather than anything else). The vehicle has been around for almost three decades, having IPO-ed in 1993.

The fund has robust long-term results, that are best to be thought of as around the current dividend yield of 7.9%:

Annualized TR (Morningstar)

While the three-year number has been significantly dragged down by this year's negative performance, the 5- and 10-year figures are closer to what a retail investor should expect. The fund has achieved its 5-year performance with a 16 standard deviation, versus 17 for the S&P 500. Quite impressive.

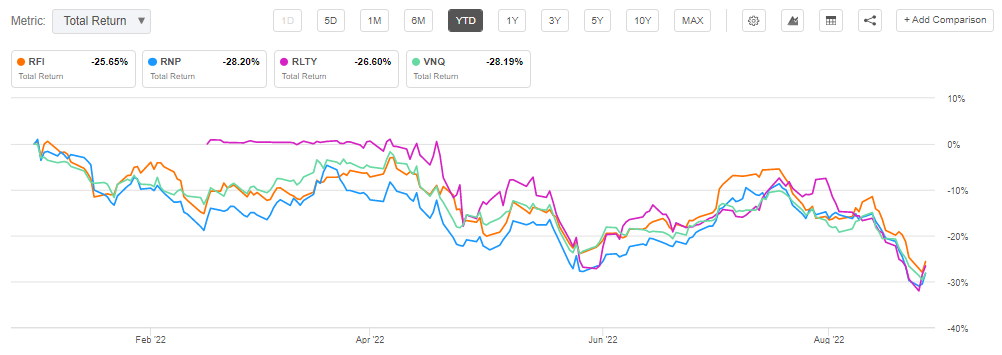

What is surprising though is that RFI has not outperformed its leveraged peers in 2022. All three funds have total return levels close to -30% in 2022. With RLTY and RNP having leverage ratios close to 30%, how is this possible? We believe the answer lies in the collateral allocation. RFI is overweight REIT equity with an 80% allocation, while only 20% is invested in preferred shares. RLTY and RNP have 35%+ allocations to preferred shares, which in these portfolios are many times floating, hence experienced less of a price decrease due to higher rates.

RFI has alternated historically between premiums and discounts. We believe higher risk-free rates translate into a lower premium to NAV for this name, so going forward expect a flat premium to NAV as a fair value here. RFI is a robust CEF that has been in the market for almost three decades and generated consistent results with a low standard deviation and high Sharpe ratio. The fund is to be revisited as soon as the Fed is done raising rates.

Analytics

AUM: $0.3 bil

Yield: 7.9%

Premium/Discount: 1.5%

Z-Stat: -1.03

Sharpe: 0.46

St Dev: 16

Leverage: 1.5%

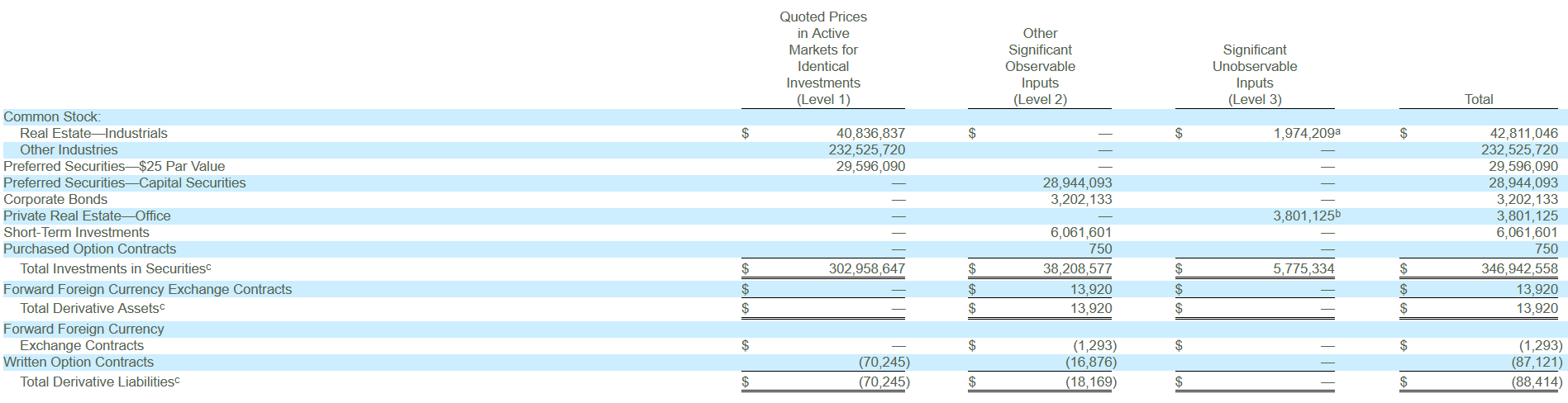

Holdings

The fund has an 80/20 split between REIT equity and preferred shares:

{kind=link}

The above table from the semi-annual report details the asset split, which for unknown reasons is not done in the fund's fact sheet.

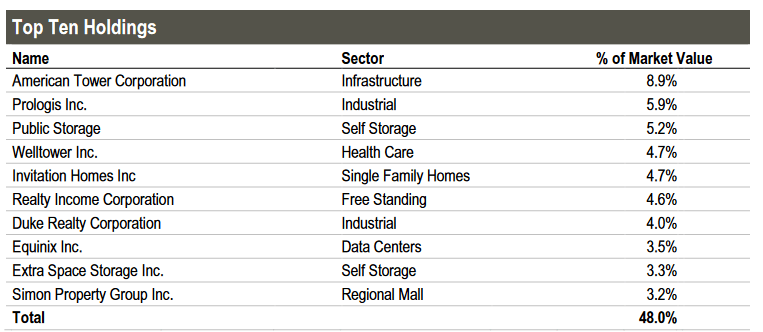

Just like the other Cohen funds, RFI exhibits the same top names in its holdings:

{kind=link}

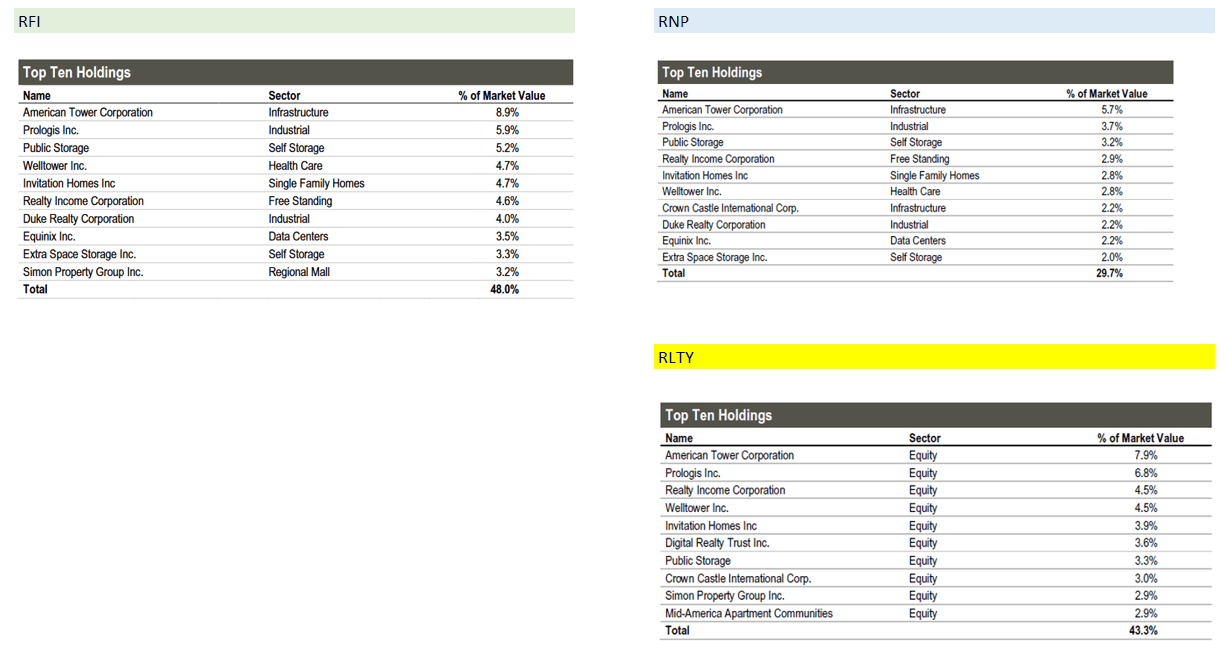

Let us have a quick look at how the fund benchmarks versus the other peers from Cohen:

{kind=link}

We can see that all three funds have almost identical top-10 holdings, albeit with different weighting. The common thread - American Tower Corporation (AMT) and Prologis (PLD) are the top two holdings in each fund.

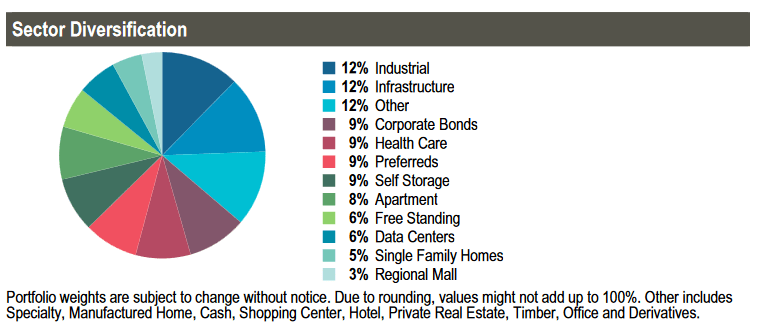

What is particular about RFI is that it does not have a large bucket dedicated to preferred shares, and most of the allocation is in pure REIT equities. The sub-sector allocation is as follows:

{kind=link}

There are no outliers here in terms of sectors with extreme concentrations. All sub-sector bucketing is done under a 15% sectoral threshold. Moreover, the very significant track record exhibited by the manager indicates their ability to correctly evaluate and pick names in the space.

Performance

What is surprising is that RFI has not outperformed its leveraged peers in 2022:

{kind=link}

We can see the fund has a very similar total return profile in 2022 as the leveraged RNP and RLTY. We surmise this is occurring due to the larger allocation to pure REIT Equity, which has taken a pounding. Floating rate preferred shares, which are present with a larger weighting in the other funds, have been less affected by the increase in rates (on a relative value basis).

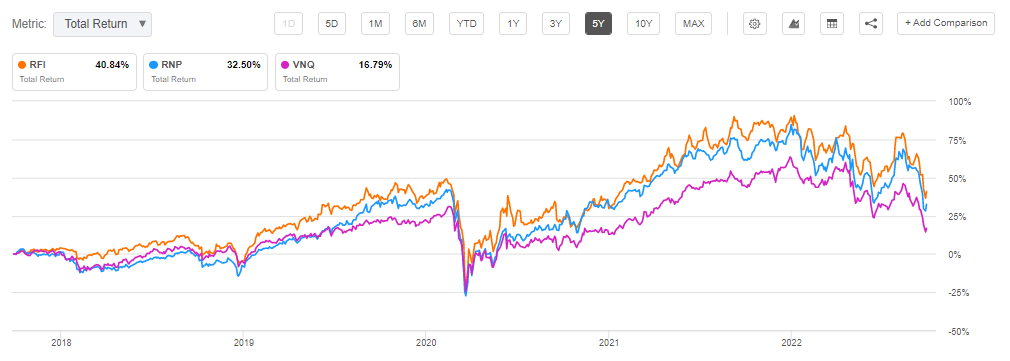

On a 5-year basis, RFI does outperform, albeit with a very slight margin:

{kind=link}

Both Cohen funds exhibit better performance metrics and total returns than the generic ETF in the space ( VNQ ).

Premium/Discount to NAV

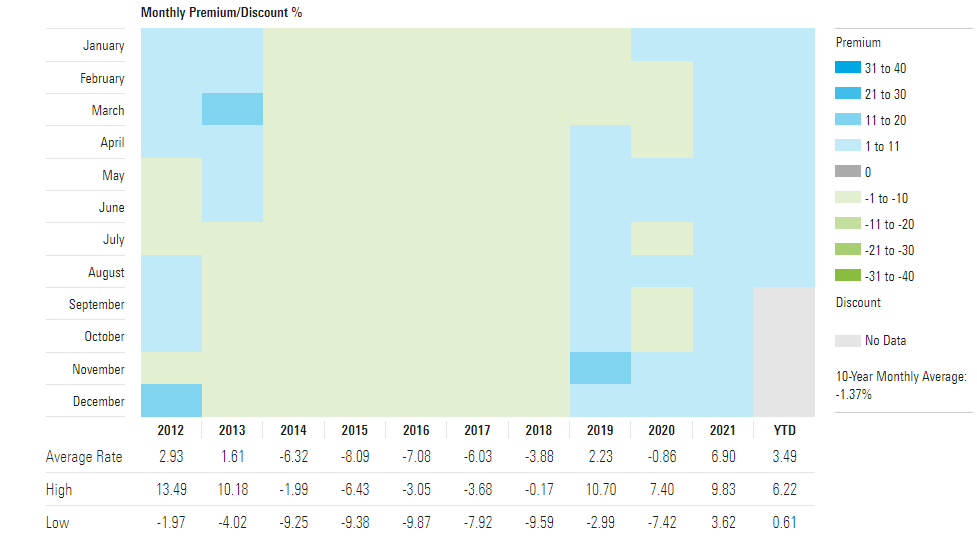

The fund has historically alternated between discounts and premiums to NAV:

{kind=link}

The fund consistently traded at a premium to net asset value during the zero rates environment experienced in 2020 and 2021.

This year, the premium has been driven by risk-on/risk-off periods:

We can see from the above table the fluctuation between 0% to 10% premium to NAV this year for the fund. We feel the higher rates environment should translate into a lower premium for the fund versus historic levels.

Distributions

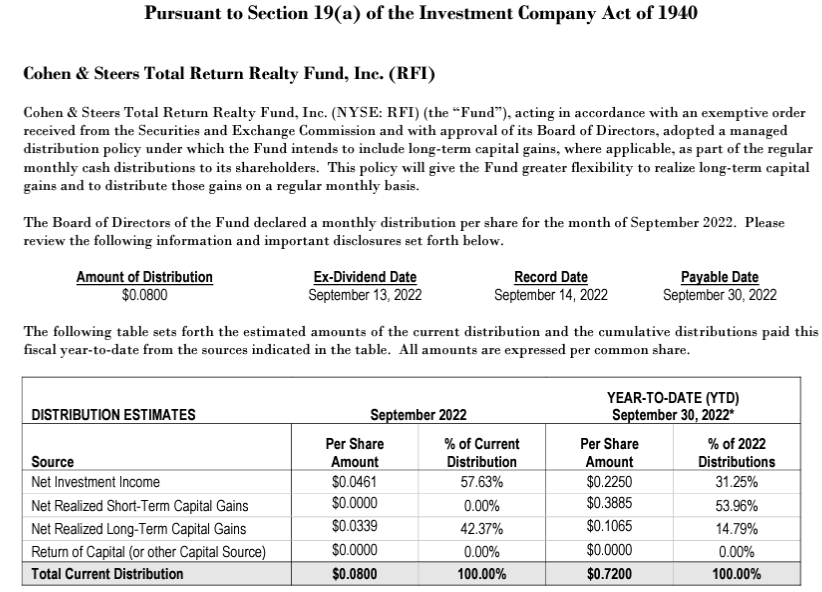

The fund is currently fully supporting its dividend:

{kind=link}

We can see from the latest Section 19.a posted by the fund that the cash utilized for the dividend distribution fully comes from investment income or realized capital gains. No ROC has been used in 2022. Given the assets in the structure and the high underlying yields, we expect full support for the dividend going forward as well.

Conclusion

RFI is a REIT equity CEF from the Cohen & Steers family of funds. Unlike its peers, the fund exhibits no leverage but still manages to pay a dividend yield exceeding 7%, and post annualized total returns close to its dividend yield. Versus its peers, the fund is overweight equities which have an 80% allocation, with only 20% invested in bank's preferred shares. The fund has not been able to outperform its peers in 2022 though, being down almost -30%. We believe this is due to the relative outperformance of many floating rate bank preferred shares, which have a higher weighting in the RNP and RLTY portfolios. RFI fully covers its current dividend yield, and we expect the fund to do so in the future. The fund is a robust vehicle with a very tried and tested management team which has steered the CEF through many market iterations in the past decades with significant success. RFI is a solid choice going forward and is worth revisiting once the Fed is done with rate hikes.

For further details see:

RFI: The Unleveraged CEF From Cohen&Steers