NIMC - RGC Resources: Underfollowed With A Nice Dividend But A High Price

2023-03-09 14:15:12 ET

Summary

- RGC Resources is a fairly small natural gas utility that serves the town of Roanoke, Virginia.

- RGC Resources is seeing some customer growth, although it is not a rapid-growth company.

- The company recently applied to regulators to raise its rates, which could grow its earnings over the next year.

- The recent dividend increase was meager, but the company appears able to sustain it.

- RGC Resources stock is quite expensive relative to peers and the market today.

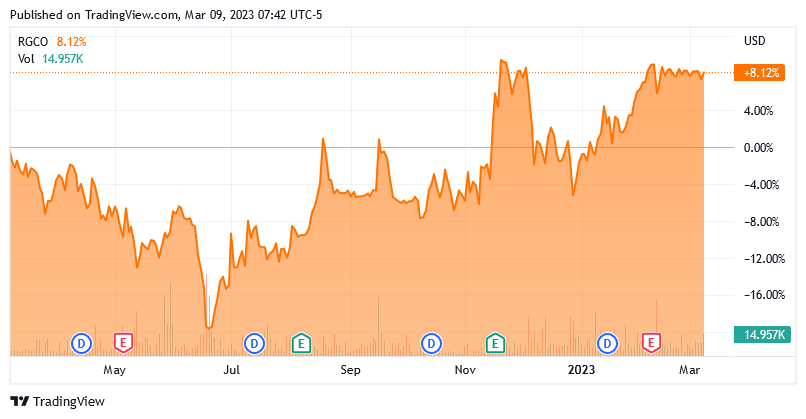

RGC Resources, Inc. ( RGCO ) is a natural gas utility that primarily operates in Roanoke, Virginia, and the surrounding area. This company is admittedly very underfollowed in the investment community and by investors themselves, likely due to its comparatively small service territory and relatively tiny customer base. However, it still has many of the characteristics that we have come to appreciate over the years. The most important of these is the company's relatively stable revenue base which results in highly reliable cash flows and allows the company to pay out a respectable 3.26% dividend yield. The company's stock price has also been one of the better performers in the market recently, as it is up 8.12% over the past twelve months:

{kind=link}

Obviously, this is much better than the loss that many other assets have handed us over the same time period. Unfortunately, the downside of this strong market performance is that the company's stock appears to be overvalued today. This is similar to the stock's overvaluation the last time that we discussed it. Thus, it may make sense to watch the stock until a more opportune buying price comes along.

About RGC Resources

As stated in the introduction, RGC Resources is a regulated natural gas utility that operates in Roanoke, Virginia, and the surrounding area. This is not an especially large service area and the company only counted 62,900 residents and businesses as customers at the end of the most recent quarter. However, this does not mean that the company does not have the same characteristics that we have come to appreciate in utility companies over the years. The most important of these is that the company has remarkably stable cash flow over time. We can see that quite clearly by looking at its operating cash flow over time:

{kind=link}

There might be some readers that point out that the above chart shows the company's operating cash flows during each of the trailing twelve-month periods as opposed to quarter by quarter. There is a good reason for that in the case of this company. As already mentioned, RGC Resources is a natural gas utility that distributes natural gas to homes and businesses. Natural gas is primarily used for space heating, so naturally, it would be much more heavily consumed in the winter than during the summer months. This causes a natural gas utility to generally receive most of its revenue, and by extension most of its cash flow, during the October to March period. This is the reason why some of these companies, such as RGC Resources, actually have a fiscal year that runs from October to September. Here are the company's quarterly operating cash flows, which illustrate this fact:

{kind=link}

As we can see, the company's operating cash flows vary quite a bit from quarter to quarter, although it does tend to have its highest figures during the January to March quarter of a given year. As we saw earlier, though, the cash flow is fairly stable when we look at it during any given twelve-month period.

The reason for this stability over time is that natural gas service to a home is generally considered to be a necessity. After all, heating during the winter months is actually protected by habitation laws and the government even provides assistance to help people pay their heating bills during the coldest months of the year. As such, people generally prioritize paying their natural gas bills ahead of other expenses during times when money is tight. This is something that could be very important today considering that consumers are showing signs of running out of discretionary income. In addition, the Federal Reserve has stated that it is actively trying to push the economy into a recession and recessions usually have an adverse impact on the finances of people at the lower end of the income scale. Thus, it may make sense to have some exposure to a utility like RGC Resources in such an environment.

Naturally, as investors, we want to see more than simple stability. We like to see those companies in our portfolio grow and prosper. Fortunately, RGC Resources is positioned to do that. One of the more obvious ways that it can accomplish this is by adding new customers. While Roanoke, Virginia is not an especially large city, it has been experiencing some population growth. During the earnings conference call , Paul Nester, RGC Resources' President and CEO, made reference to a series of new housing developments going up in the Greater Reno Valley. I was not able to find any information about this during an Internet search, but the company states that it should be able to add about 500 to 600 customers over the next twelve months because of it. That is admittedly not a very large growth rate, but it is at least something. This will, of course, result in more customers paying their utility bills and should result in more revenue for the company. The more money that comes in, the more money that RGC Resources has available to cover its fixed expenses, and ultimately the more money makes its way down to the bottom line.

The other method through which RGC Resources can generate growth is by growing its rate base. The rate base is the value of the company's assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase in the rate base allows the company to increase or adjust its prices in order to achieve that specified rate of return. This is usually accomplished by spending money on upgrading, modernizing, or possibly expanding a company's utility-grade infrastructure. RGC Resources, unfortunately, has not put forth any plan to do that at present. The company has mentioned that it will be making some investments and has been growing its rate base, but the most recent conference call, press releases, and even SEC filings give absolutely no specifics. Thus, we cannot estimate how quickly the company intends to grow its rate base. However, it did file for a rate increase in December 2022. It is still waiting for formal approval from regulators, but it did start charging the higher rates on an interim basis back in January, so that could provide a bit of an earnings boost going forward assuming the company does ultimately get final approval from the regulators.

Financial Considerations

It is always important that we review the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt and using the proceeds to repay the existing debt, which can cause a company's interest expenses to increase under certain market conditions. This is something that may be a big concern today considering that the Federal Reserve has been actively raising interest rates over the past year, causing newly issued debt to be more expensive than it was in past years.

In addition to this risk, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company's cash flow to decline could push it into financial distress if it has too much debt. Although utilities like RGC Resources tend to have remarkably stable cash flows over time, this is still a risk that we should not ignore as bankruptcies have happened in the sector.

One metric that we can use to evaluate a company's financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well a company's equity can cover its debt obligations in the event of a bankruptcy or liquidation event, which is arguably more important.

As of December 31, 2022, RGC Resources had a net debt of $142.9 million compared to shareholders' equity of $94.9 million. This gives the company a net debt-to-equity ratio of 1.51 today. Here is how that compares to some of the company's peers:

| Company |

| Net Debt-to-Equity |

| RGC Resources |

| 1.51 |

| New Jersey Resources ( NJR ) |

| 1.76 |

| Northwest Natural Holding ( NWN ) |

| 1.40 |

| Atmos Energy ( ATO ) |

| 0.86 |

| NiSource Inc. ( NI ) |

| 1.43 |

As we can see here, RGC Resources is more levered than most of its peers, but it is not the worst company on this list in that respect. Natural gas utilities as a rule are usually somewhat less levered than electric utilities and RGC Resources certainly does not appear to have a high debt load if it is compared to those companies (see here for comparison). Overall, we probably do not have to worry too much, but it would still be nice to see the company bring down its debt load somewhat so that it is closer to its better-financed peers.

Dividend Analysis

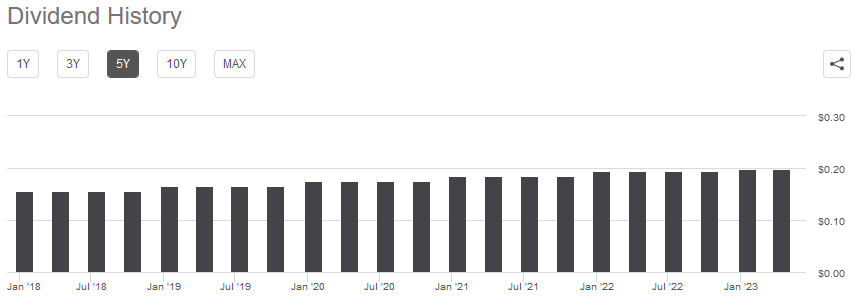

One reason why investors like utilities is that they typically have higher dividend yields than many other things in the market. RGC Resources is no exception to this as the stock yields 3.26% at the current price, which is significantly higher than the 1.58% yield of the S&P 500 Index (SP500). The company also has a long history of raising its dividend annually, although the most recent dividend hike was only $0.0025 per share so it is certainly nothing that we can write home about:

{kind=link}

The fact that the company raises its distribution annually is something that we should find appealing, particularly given today's inflationary environment. This is because inflation is constantly reducing the number of goods and services that we can buy with the dividend that we receive, so it will likely feel as if we are getting poorer and poorer over time. The fact that the company increases its dividend regularly helps to offset this effect and maintains the purchasing power of the dividend. With that said, the most recent increase was far less than the current rate of inflation, so it certainly did not manage to accomplish that task this year. The 1.28% increase that we got was still better than nothing, however.

As is always the case, though, we need to ensure that the company can actually afford the dividend that it pays out. After all, we do not want to find ourselves the victims of a dividend cut, since that would reduce our incomes and most likely cause the company's stock price to decline.

The usual way that we judge a company's ability to maintain its dividend is by looking at its free cash flow. A company's free cash flow is the amount of money that was generated through its ordinary operations and is left over after it pays all of its bills and makes all necessary capital expenditures. This is the money that is available to do things such as reducing debt, buying back stock, or paying a dividend. During the twelve-month period that ended on December 31, 2022, RGC Resources reported a negative levered free cash flow of $13.7 million. That is obviously not enough to pay any dividend, yet the company still paid out $7.4 million to its shareholders. At first glance, this is likely to be concerning as the company is not generating enough free cash flow to cover its dividend.

However, it is common for utilities to pay their dividends out of operating cash flow while financing their capital expenditures through the issuance of debt and equity. This is because of the extraordinarily high cost of constructing and maintaining utility-grade infrastructure over a wide geographic area. Those costs cause these companies to have negative free cash flow during most quarters so they would essentially be prevented from ever paying a dividend if they had to finance it using free cash flow. As stated earlier, RGC Resources had an operating cash flow of $16.7 million during the twelve-month period that ended on December 31, 2022. This was sufficient to cover the $7.4 million dividend and still leave the company plenty of money available for other purposes. Overall, this distribution is probably reasonably safe.

Valuation

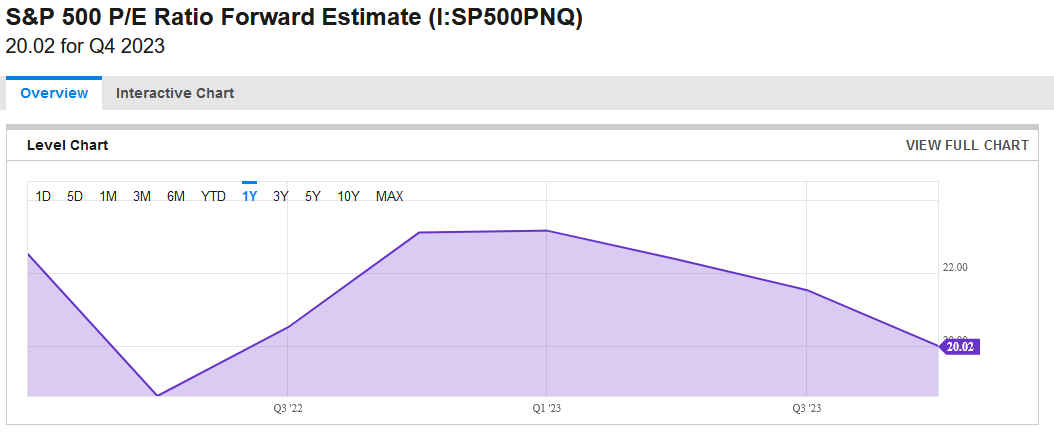

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a utility like RGC Resources, we can value it by looking at the forward price-to-earnings ratio. This ratio basically tells us how much we would have to pay today for each dollar of earnings that the company is expected to generate over the next year.

According to Zacks Investment Research , RGC Resources has a forward price-to-earnings ratio of 26.93 at the current price. This is quite a bit higher than the 20.02 forward price-to-earnings ratio of the S&P 500:

{kind=link}

This is quite surprising since we should expect RGC Resources to trade for less than the index because its forward growth potential is much lower. However, here is how RGC Resources' valuation compares to its peers:

| Company |

| Forward P/E Ratio |

| RGC Resources |

| 26.93 |

| New Jersey Resources |

| 20.16 |

| Northwest Natural Holdings |

| 17.33 |

| Atmos Energy |

| 18.74 |

| NiSource Inc. |

| 17.76 |

(all figures courtesy of Zacks Investment Research.)

This adds further confirmation that RGC Resources stock is quite expensive today. We can see that its peers are all significantly cheaper than RGC Resources today and the majority of them are cheaper than the index, which is exactly what we expect from the utility sector. Thus, it seems that we should probably wait until RGC Resources comes down a bit before building a position.

Conclusion

In conclusion, RGC Resources, Inc. is a small and very underfollowed natural gas utility that serves a fairly small area of Virginia. It still shares many of the same characteristics that investors usually appreciate with a utility though, most importantly its stable cash flows over time. The company may experience somewhat limited growth though, and its recent dividend increase leaves something to be desired. The biggest concern here, however, is that it appears that RGC Resources, Inc. is significantly overpriced at the current market value. It could ultimately be worth buying as a stable dividend-payer, but it would be best to wait until the price drops.

For further details see:

RGC Resources: Underfollowed, With A Nice Dividend But A High Price