RGT - RGT: Disappointing Small Cap Equity CEF

Summary

- Royce Global Value Trust is an equities CEF.

- The fund focuses on international small capitalization stocks.

- The vehicle has a managed distribution plan, but has failed to beat simple ETFs in the space on 5- and 10-year lookback periods.

- The CEF is trading with a discount to NAV, but has done so in the past 10 years due to its chronic laggard total return.

- This article covers CEFs and related analytics.

Thesis

Royce Global Value Trust ( RGT ) is an equities CEF. As per its literature, the fund is:

• A closed-end fund dedicated to investing in both U.S. and non-U.S. small-cap stocks.

• Core approach that offers wide exposure to both U.S. and non-U.S. small/mid-cap stocks (generally market caps up to $10 billion).

• A fundamentally rooted approach that emphasizes valuation and company quality

The vehicle therefore aims to extract dividends from small and mid-cap stocks, both in the U.S. and internationally. Currently the fund is overweight U.S. names which comprise 43% of the portfolio. Canadian and UK stocks are the next largest concentrations. The fund has a granular build, with a diversified portfolio, dominated by Industrials and Financials.

From a performance standpoint this is where the fund disappoints - the vehicle is unable to outperform simple ETFs in the sector, and ultimately does not coherently justify its existence. The market is punishing the name by trading it at a -14% discount to net asset value, and we can see that historically it has always done so. Expect the discount to persist until the CEF can consistently outperform simple instruments in the international small cap space.

There is not much to like about this fund currently. It does have a managed distribution plan which consistently pays out cash, but without a performance behind it the cash can sometimes be just overwhelmingly ROC. There are much better alternatives in the international small cap arena currently, so new money should steer away from this name.

Holdings

The fund is overweight U.S. stocks:

Country Distribution (Fund Fact Sheet)

We can see that the CEF is currently overweight U.S. names, followed by only two jurisdictions with buckets above 10%, namely Canada and the U.K.

The fund is heavily concentrated in Industrials:

Sectors (Fund Fact Sheet)

Financials and Information Technology are the next largest sectors in this name. From a single name perspective, below are the fund's top exposures:

Top Holdings (Fund fact sheet)

We can note that the fund is fairly granular, without any name representing more than 5% of the portfolio. In effect most stocks do not pass the 3% holding threshold.

Performance

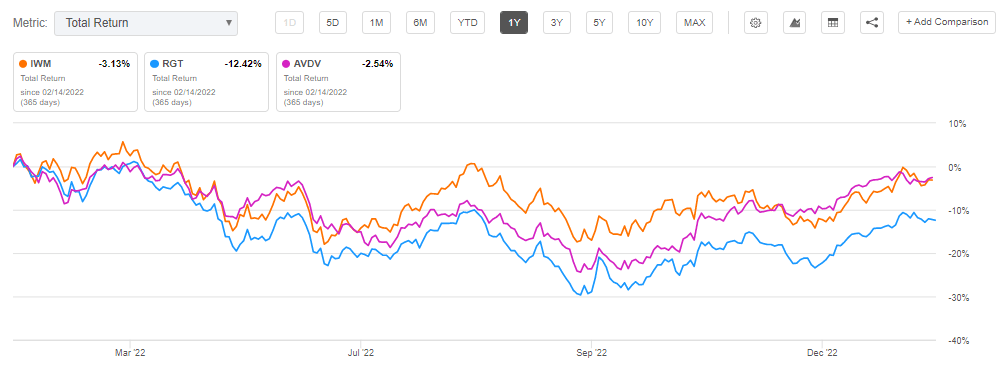

The fund is down over -12% in the past year:

{kind=link}

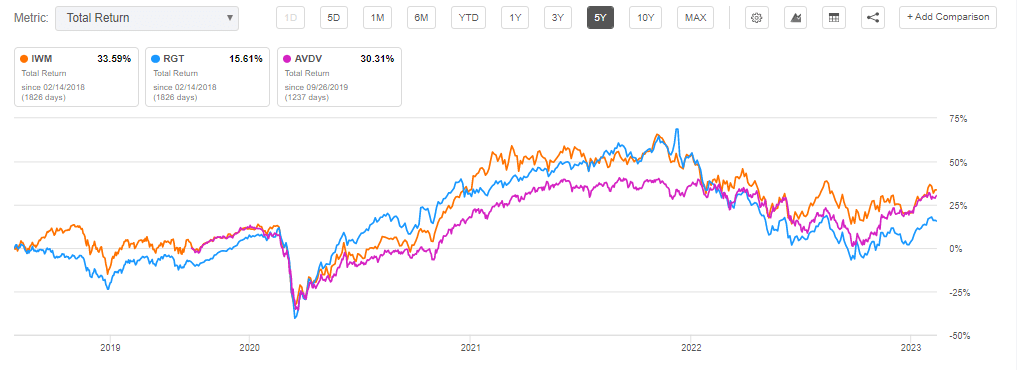

The fund is a laggard on a 5-year time frame as well:

{kind=link}

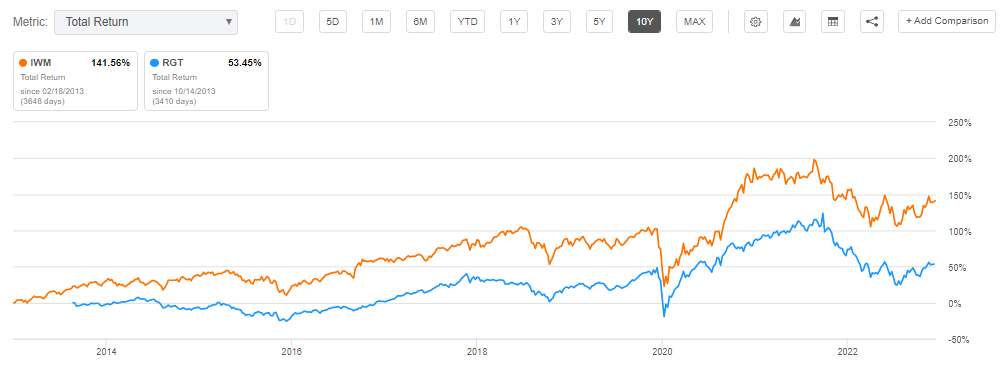

When looking at total returns on a 10-year look-back period we can clearly notice a substantial underperformance in the fund:

{kind=link}

Premium/Discount to NAV

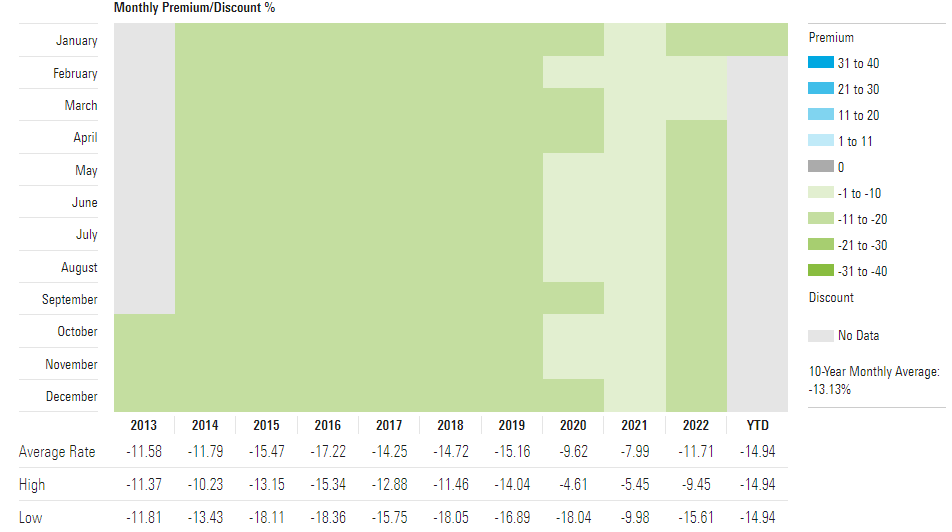

The market has rewarded this CEF's underperformance with a healthy discount to net asset value:

{kind=link}

We can see that in the past decade we do not have any premiums to net asset value when looking on a monthly basis. The average discount has gyrated around -15%, with wide levels seen around -18%. Do not expect anything to change in the future either, unless somehow the fund starts to outperform its benchmark or the simple unleveraged sector ETF.

Distribution

The CEF has a managed distribution plan in place:

The Board of Directors of each of Royce Micro-Cap Trust and Royce Value Trust has authorized a managed distribution policy (MDP). Under the MDP, Royce Micro-Cap Trust and Royce Value Trust pay quarterly distributions at an annual rate of 7% of the average of the prior four quarter-end net asset values, with the fourth quarter being the greater of these annualized rates or the distribution required by IRS regulations. With each distribution, the Fund will issue a notice to its stockholders and an accompanying press release that provides detailed information regarding the amount and composition of the distribution (including whether any portion of the distribution represents a return of capital) and other information required by a Fund's MDP

This basically means that the vehicle is going to pay 7% either via capital gains or by returning your own cash. Managed distribution plans are common in the CEF space, and they are in place to ensure a smooth management of dividends even when the underlying asset class is not performing up to par.

Conclusion

RGT is an equities CEF. The fund focuses on domestic and international small cap names. The vehicle has a granular build and is concentrated in the Industrials and Financials sub-sectors. With a managed distribution plan, the fund aims to pay 7% of the average of the prior four quarter-end NAVs. RGT fails to excite and to perform. The fund underperforms simple ETFs in the space, and that is why the market is punishing the fund, trading it at a -14% discount to net asset value. We expect this to persist until the CEF can establish a clear outperformance track-record. We do not expect that to be any time soon. There is not much to like here in respect to RGT when compared to simple alternatives in the space.

For further details see:

RGT: Disappointing Small Cap Equity CEF