RYTM - Rhythm Pharmaceuticals: Major Catalysts Due For Weight Loss Specialist

2023-11-21 02:58:46 ET

Summary

- Rhythm Pharmaceuticals' stock has experienced significant volatility, soaring and plunging multiple times since its IPO in 2017.

- The company's lead drug, Imcivree, was approved for chronic weight management in patients with specific genetic deficiencies, but its revenue has been relatively low.

- Rhythm faces competition from GLP-1 agonists, which target a potential $100 billion revenue opportunity in diabetes and weight loss/obesity.

Investment Overview - Rhythm Stock Soars, Plunges, Soars Again On Potential Of Lead Drug Setmelanotide

Rhythm Pharmaceuticals ( RYTM ) stock has been on a rollercoaster rise ever since the company completed an oversubscribed Initial Public Offering ("IPO") in October 2017 raised ~$120m at $17 per share in October 2017, and immediately rose to a value of >$30 per share.

Back then Rhythm's lead candidate was setmelanotide, a melanocortin-4 receptor agonist, and the drug remains absolutely central to the company's fortunes more than 5 years on.

In November 2020, Setmelanotide was approved, under the brand name Imcivree, for chronic weight management in adult and pediatric patients 6 years of age and older with obesity due to proopiomelanocortin (POMC), proprotein convertase subtilisin/kexin type 1 (PCSK1) or leptin receptor (LEPR) deficiency confirmed by genetic testing.

Imcivree was the first drug ever approved for these indications, which the FDA referred to as "rare genetic diseases of obesity" in its approval press release . According to the release:

People living with obesity due to POMC, PCSK1 or LEPR deficiency struggle with extreme, insatiable hunger beginning at a young age, resulting in early-onset, severe obesity. As an MC4 receptor agonist, Imcivree is designed to restore impaired MC4 receptor pathway activity arising due to genetic deficits upstream of the MC4 receptor.

The FDA approval of Imcivree is based on results from the largest studies conducted to date in obesity due to POMC, PCSK1 or LEPR deficiency. In Phase 3 clinical trials, 80 percent of patients with obesity due to POMC or PCSK1 deficiency achieved greater than ten percent weight loss and 45.5 percent of patients with obesity due to LEPR deficiency achieved greater than ten percent weight loss after one year of treatment with Imcivree.

Consistent with prior clinical study experience, Imcivree was generally well-tolerated in both trials. The most common adverse events were injection site reaction, skin hyperpigmentation, and nausea. Warnings and precautions include disturbance in sexual arousal, depression and suicidal ideation, skin pigmentation and darkening of pre-existing nevi.

In July 2020, Rhythm appointed its current CEO, Dr. David Meeker, who replaced interim CEO Hunter Smith, who returned to his former role of Chief Financial Officer. Meeker is also Chairman of Rhythm's Board of Directors. Post approval, in January 2021, Rhythm reached an all-time high value of $40 per share.

In the first 6 months of 2021, however, Imcivree earned just $309k of revenues, and analysts began to question whether the drug could secure approval in larger patient populations, despite some promising data.

In late February 2022, Rhythm revealed that the FDA had extended its supplemental New Drug Application ("sNDA") decision date for Imcivree in patients with Bardet-Biedl Syndrome ("BBS") or Alström syndrome by 3 months, and in March, when the company revealed Imcivree revenues in 2021 of $3.2m, with a loss from operations of $171m, following a $137m loss in the prior year, and cash position reported as $308m, a bear run ensued that dragged the stock price <$3.5 by May.

In June 2022, the FDA opted to reject the sNDA for Alström syndrome, but approve Imcivree for patients with BBS, and in August, Rhythm revealed sales revenues from the drug of $3.8m in Q1 and Q2 combined, versus $0.3m in the prior year. More important, however, were results shared from a study of setmelanotide in hypothalamic obesity ("HO"), as follows:

All 11 evaluable patients achieved the primary endpoint of at least 5% reduction in body mass index ((BMI)) (P<0.0001) at 16 weeks on therapy, with a mean change in BMI of -17.2% and a mean change in hunger score of -2.7.

Shares skyrocketed on the positive data readout, reaching a high of $25 as Goldman Sachs ( GS ) analysts estimated that an approval in HO could bring in peak risk-adjusted sales of $1.6bn, and raised their price target to $28.

In September, Imcivree was awarded expanded approval (to include BBS) in Europe (and in the UK 2 months later), and in November, setmelanotide was awarded Breakthrough Therapy designation by the FDA, sending the share price higher still. In January 2023, the stock price had once again attained a peak high of $35 per share - a 750% gain in just over 6 months.

Rhythm, To Present Day - The Volatility Continues

The positive start to 2023 did not last long. Imcivree revenues of $8.8m in Q422, and $16.9m in FY22 beat analysts' expectations, but net loss for the quarter of $43m in Q4, and $181m across FY22, coupled with guidance for non-GAAP operating expenses of $200 - $220m, plus current assets of $354m, expected to provide a funding runway into 2025, seemed to disappoint the market. By July this year, the share price had fallen to ~$16.

In August, however, a positive set of Q2 earnings restored upside momentum. $19.2m of revenues for Imcivree, and $31m across the first 6m of 2023, triggering a $25m milestone payment from Healthcare Royalty Partners, plus "more than 125 new prescriptions for BBS in Q2, and more than 425 since FDA approval", a net loss of $(99m) across Q1 and Q2, and a cash position of $283m was reported.

On November 7th, Q3 earnings triggered another spike in the share price, back to >$34 once again. Imcivree earned revenues of $23m, cash was reported as $300m, net loss was $(44.2m), and perhaps most importantly, Rhythm CEO and Chair updated on progress in the HP indication as follows:

we are excited by the strength of our 12-month LTE data in patients with hypothalamic obesity where we reported a mean body mass index ((BMI)) reduction of more than 25% in patients on therapy for one year, with several patients trending towards or achieving normal body weight.

These data and continued enrollment progress with our ongoing Phase 3 study reinforce our confidence as we advance this high potential program. We look forward to providing an R&D update, including our RM-718 program, data from the open label part of the setmelanotide Phase 2 DAYBREAK study and data from our Phase 3 pediatrics trial, during an investor event in December."

The Elephant In The Room - Rise Of GLP-1 Agonists?

According to a Rhythm investor presentation, the estimated number of BBS patients in the US and Europe combined is ~9k, and the estimated prevalence of POMC, PCSK1 and LEPR deficiency obesities is ~3k (I am using midpoint of Rhythm estimates), while there could be a 5-10k patient prevalence with HO in the US, and perhaps ~53k patients across all of the indications in which the company is studying setmelanotide.

Imcivree earned $53m across the first 9 months of 2023, and on the Q3 analysts call, Jenifer Chien, Executive Vice President for North America, told analysts:

Throughout the launch from June 16th, 2022 through the end of the third quarter of 2023, we now have received more than 545 new BBS prescriptions coming from more than 300 prescribers. Of these prescriptions, we have greater than 330 approvals for reimbursement from payers.

With the list price of Imcivree apparently ~$250k (based on average 2mg daily dose), if we assume the drug could reach 5k patients in its currently approved indications (an optimistic figure, I'd say), then the peak revenue opportunity could be as high as $1.25bn.

That would double (at least, in a very optimistic scenario), if 5k patients with HO could be reached (assuming approval is granted). That equates to a $2.5bn opportunity, and in a scenario where all of Rhythm's approval shots come off, and 50k patients can reached, we would be looking at a drug with double-digit billion potential.

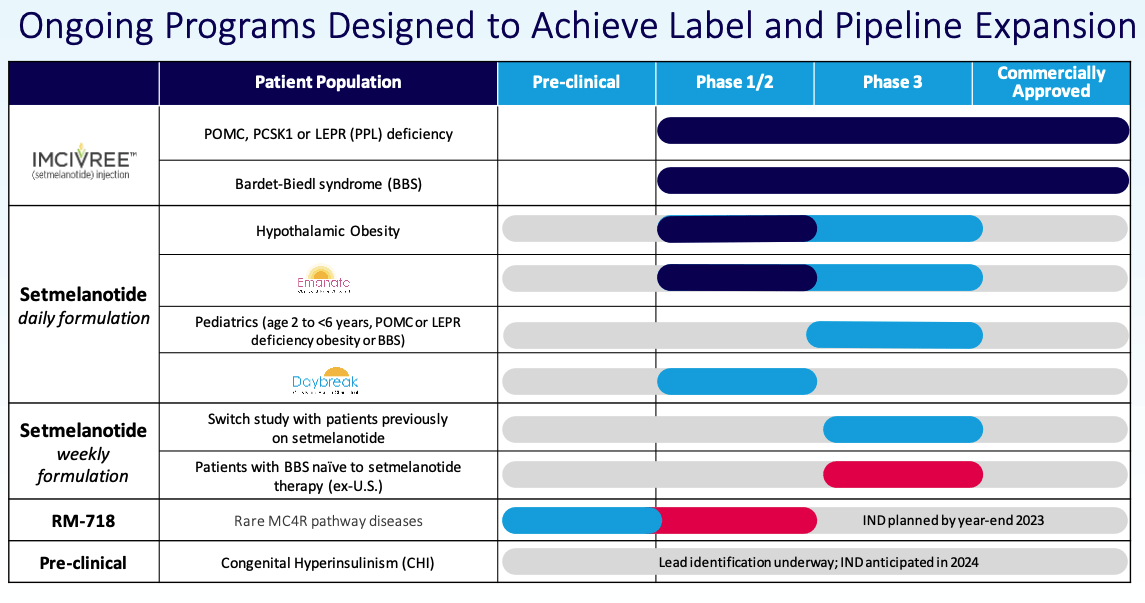

Rhythm drug development pipeline (Rhythm investor presentation)

{kind=link}

That kind of market opportunity would certainly be enough to support Rhythm's current market cap valuation of just $2bn. There is obviously a massive disconnect between the $3.4m earned so far in 2023, which makes Rhythm stock looks substantially over-valued, especially given it is also heavily loss making with a limited funding runway, and "blockbuster" (>$1bn per annum) revenues, or even "mega-blockbuster" revenues.

One class of drug that is estimated to be targeting a potential $100bn revenue opportunity in diabetes and weight loss / obesity are GLP-1 agonists, however. The best known drugs in this class are Eli Lilly's tirzepatide, approved as Mounjaro in Type 2 diabetes, and as Zepbound in obesity, and Novo Nordisk's semaglutide, approved as Ozempic and Wegovy in the same indications. As I wrote in a note on the recent approval of Zepbound , a couple of weeks ago:

In 2020, 2021, and 2022, Ozempic earned revenues of ~$3bn, $4.8bn, and $8.5bn, and across the first nine months of 2023, $9.5bn. Wegovy earned $3.1bn across the equivalent period in 2023. Mounjaro, which was only approved in May last year, earned $569m of revenues in Q1 this year, $980m in Q2, and $1.4bn in Q3.

Zepbound was able to show it could reduce patients body weight by an average of ~15 - 20% in pivotal clinical studies, which seems to compare favourably to Imcivree - therefore, are GLP-1 inhibitors a major threat to the blockbuster setmelanotide franchise Rhythm is attempting to build? In its 2022 10K submission Rhythm writes as follows:

existing therapies indicated for general obesity and those in clinical development for the same, including glucagon-like peptide-1 (GLP-1) receptor agonists, such as Wegovy, and glucose-dependent insulinotropic polypeptide (GIP) and glucagon-like peptide-1 (GLP-1) agonists, such as tirzepatide, do not specifically restore function impaired by genetic deficiencies and trauma to the hypothalamus that disrupt MC4R pathway signaling, which we believe is a root cause of hyperphagia and obesity in patients with these diseases.

CEO Meeker also addressed the issues of GLP-1 agonists during the Q3 call with analysts:

The sheer volume of noise around the management of obesity as a disease with GLP-1 specifically has both aided (our) cause, as healthcare providers are looking more closely at patients who present with obesity and doing the appropriate workups, and hindered (our) cause where the availability of powerful therapies such as GLP1 medications has led many to believe that all obesity is the same and GLP1 represent the universal solution.

As we know, that is not correct. Obesity is not one disease, but many diseases and as with most forms of medical therapy, the more targeted and specific the solution, the better. Our story remains relatively simple. We're replacing or supplementing a hormonal signal, which is deficient. So, if you're managing a patient, why wouldn't you start there?

In other words, Rhythm is making the case that its drug is better designed for the indications it is targeting than GLP-1 inhibitors, and this seems to be backed up interim data in HO, in which patients "achieved mean BMI reduction of 25.5% at one year on setmelanotide treatment".

There are a few issues to consider however. First of all, Rhythm needs that data to be confirmed in the final data analysis, secondly, BMI is a slightly different endpoint to the weight loss percentage used by semaglutide / tirzepatide, and perhaps most importantly, by the time setmelanotide makes it to market, assuming the approval is granted in HO, will Rhythm be able to make a dent in a market in which the much hyped Wegovy and Zepbound are already established and dominant. Rhythm simply does not have the same ability to market Imcivree as its far larger Pharma rivals do.

Concluding Thoughts - After Review, Is Rhythm Stock A Buy, Sell, or Hold?

My conclusion is that this a very difficult call to make. On the plus side, you have a drug that is already approved in 2 indications, with a strong efficacy profile, and a reasonable safety profile. You have evidence of growing sales, enough cash to support an approval shot in a much larger indication, and a potentially much more significant, double-digit market opportunity in play over the longer term.

On the negative side, the approved indications are niche, sales have not yet reached the $100m per annum level, Rhythm is loss-making, and there is a ferocious competitor to setmelanotide in the form of the GLP-1 agonists semaglutide and tirzepatide, that could make physicians and patients forget all about the impressive efficacy of Imcivree.

A third factor of interest in the volatility of Rhythm's share price, which has traded <$4, and >$35 within the past 2 years, meaning investors' money is most certainly at risk, especially when buying in at the current high price,

There are also some major upcoming catalysts to look forward to - on December 6th, an R&D event in which Rhythm with update on the HO study, announce preliminary data from an open label DAYBREAK study, which evaluates setmelanotide in several distinct, genetically defined MC4R pathway diseases i.e. major label expansion opportunities, and discuss a second candidate, RM-718, a next generation MC4R agonist. An Investigational New Drug ("IND") application could be approved for this drug early next year.

As such, my current verdict on Rhythm is that a "hold" recommendation is most appropriate. The significant single asset risk could be alleviated by the development of RM-718, the HO opportunity is very much in play, further label expansions are under considerations are being studies, there is cash available to fund operations under 2025, and Imcivree sales are growing.

GLP-1 agonist may be the major threat the market is not factoring going forward, however, and I would be slightly concerned that they possess a superior safety profile to Imcivree, which has been associated with some off-putting (for patients) side-effects, and slightly high levels of study discontinuation. Still, for the time being at least, Rhythm has the opportunity to keep growing revenues in fields in which it has the only approved asset.

This protects the valuation for perhaps another 12 months, although expect volatility to the downside if the investor day data disappoints, and perhaps another spike if the data is strong. The prospect of M&A and Rhythm becoming a buyout target is also very real. In short, watch this space!

For further details see:

Rhythm Pharmaceuticals: Major Catalysts Due For Weight Loss Specialist