RELL - Richardson Electronics Offers Limited Opportunity

2023-06-29 11:37:25 ET

Summary

- Richardson Electronics, Ltd., a specialty manufacturer of technology products, is underperforming due to various factors.

- Despite these challenges, the company reported its 10th consecutive quarter of Y/Y revenue growth in April 2023.

- I'll argue that the current share price already factors in the good and bad news for, and there is little to entice a retail value investor to do anything other than consider it a selling opportunity.

Richardson Electronics, Ltd. ( RELL ) seems at first glance to be a gem of a specialty manufacturer of technology products for hi-tech industries. But the company’s earnings growth is not keeping pace with its impressive revenue growth. In our opinion, nothing on the horizon warrants a retail value investor holding this stock for another 12 or 18 months. The stock rates a Sell assessment at the current share price.

What Richardson Makes

The company’s products and services are used to control, switch, or amplify electrical power signals; its display devices are used in alternative energy, healthcare, aviation, communications, industrial, marine, medical, military, scientific, and semiconductor markets. +60% of revenue comes from products Richardson manufactures or has exclusively made under contract with suppliers. The company was founded in 1947. It is headquartered in Illinois. It operates through 3 segments.

The Power and Microwave Technologies segment sells products and services for microwave components for broadcast transmission, CO2 laser cutting, diagnostic imaging, dielectric and induction heating, high energy transfer, high voltage switching, plasma, power conversion, radar, and radiation oncology applications. The PMT segment designs engineered solutions for power conversion, power grid and microwave tubes, and related consumables. A division of PMT is its Green Energy Solutions.

GES, formed about a year ago to reach a new market, designs and sells equipment and solutions for customers specifically moving to replace lead acid batteries, components for EVs and charging stations, and customers wanting to replace fossil-fueled equipment with hydrogen. GES manufactures magnetrons to produce lab-grown diamonds.

According to the last shareholder meeting transcript, PMT sales and margins increased 22% Y/Y for the third quarter. PMT contributed most to the 27.2% increase in net sales of $70.4M in Q3 ’23 for the company. Its total operating income was $7.7 (10.8% of net sales) compared to Q3 ’22 operating income of $3.6M or 6.6% of net sales. Net sales for GES increased $5.8M (103%) from last year's third quarter but margins tumbled from 34.6% to 25.7% in Q3 ’23. GES backorders nearly doubled in sales by the end of the quarter. Much of the company’s capital expenditures went to hiring staff, capturing customers, and investing in infrastructure.

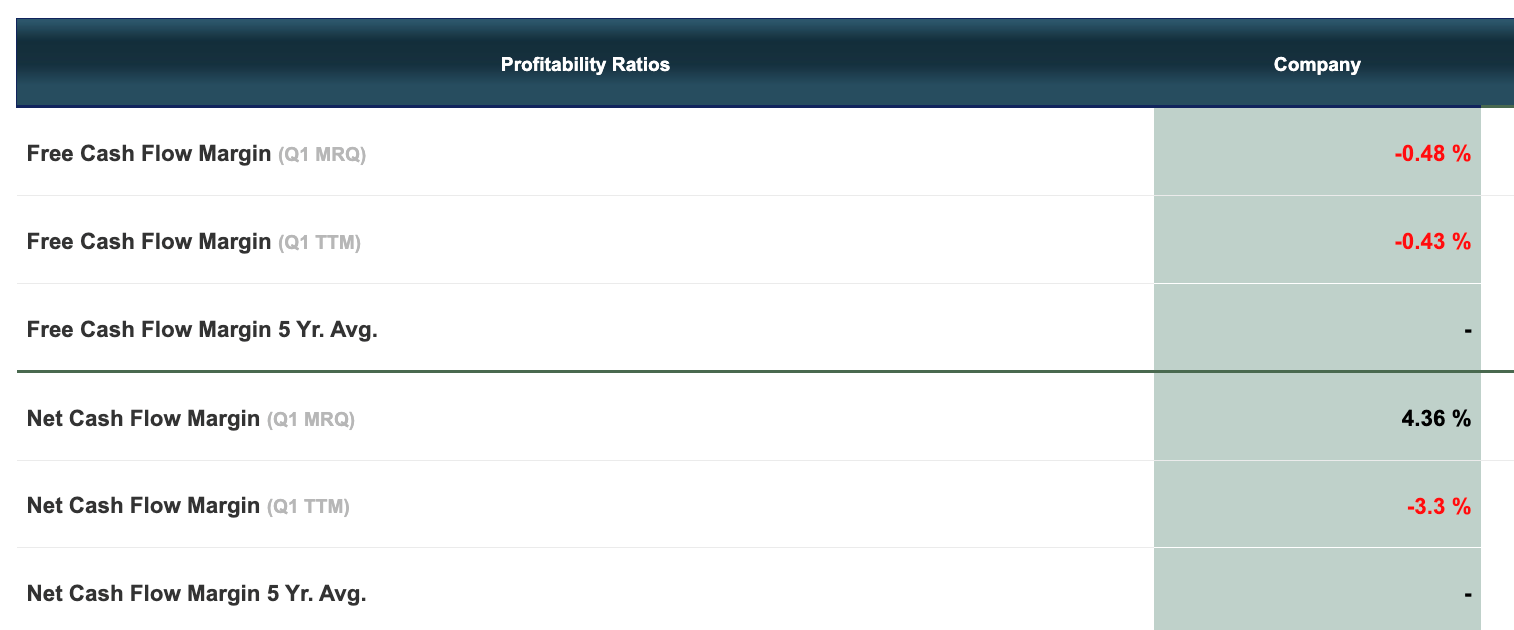

Free Cash Flow (csimarket.com/stocks/Profitability.php?code=RELL)

{kind=link}

The third operating segment of Richardson Electronics is Canvys. This segment designs and sells customized visual technology display solutions. Whether a customer needs a custom-engineered system , modifications to an off-the-shelf product, or advice on specifying the right equipment, experts work with the customer staff to here to produce custom touch screens, protective panels, all-in-one computers, custom enclosures, specialized cabinet finishes, and application-specific software packages.

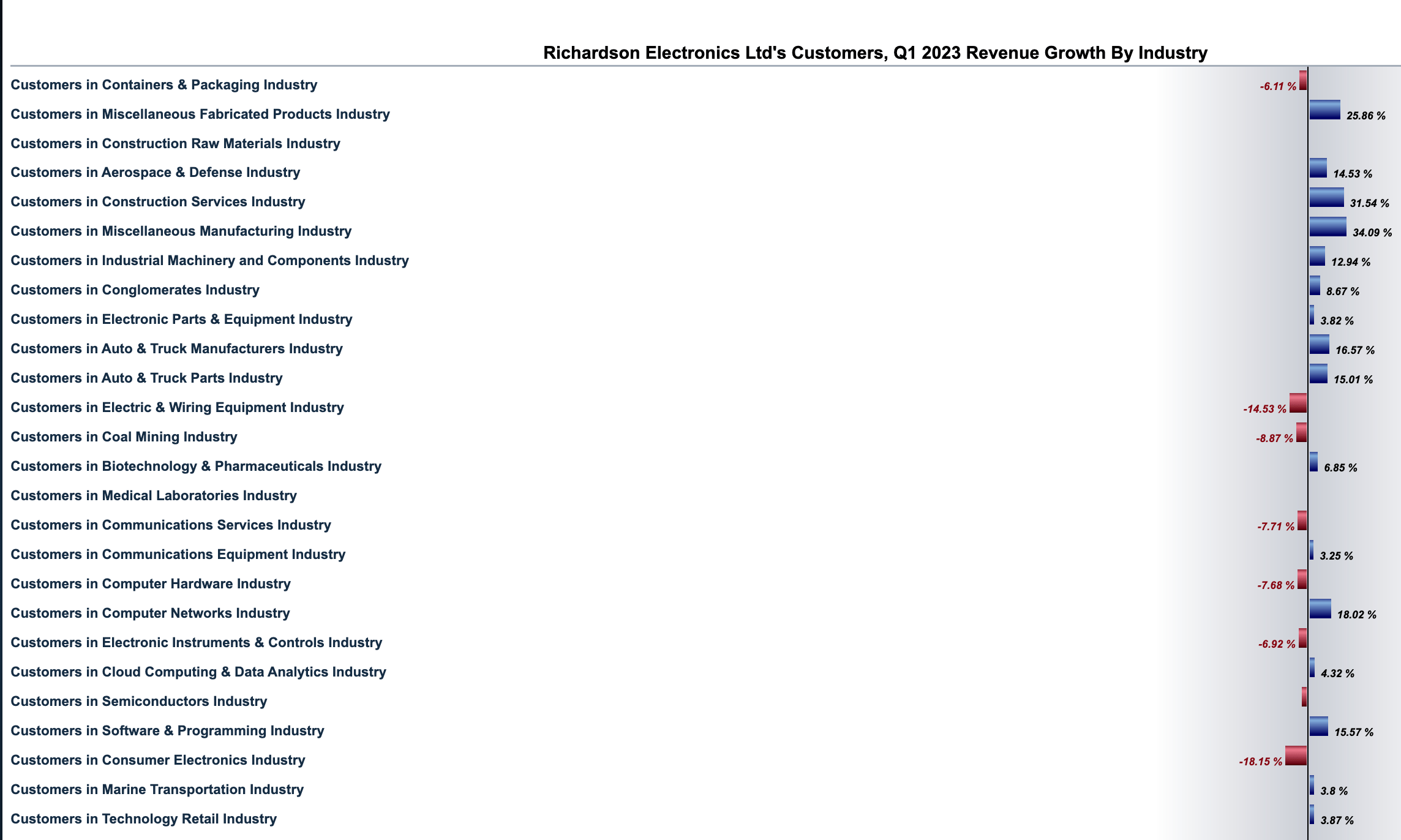

Customer markets (csimarket.com/stocks/markets_glance.php?code=RELL)

{kind=link}

Its Healthcare segment manufactures and distributes diagnostic imaging replacement parts for CT and MRI systems, CT and MRI tubes, MRI coils, cold heads, RF amplifiers, hydrogen thyratrons, klystrons, magnetrons, flat panel detector upgrades, pre-owned CT systems, and additional replacement solutions. The company offers service training to its customers’ employees. This is the weakest of the segments. Margins, backorder numbers, and sales in Healthcare were flat again in Q3 ’23.

Good, Bad, and Sell

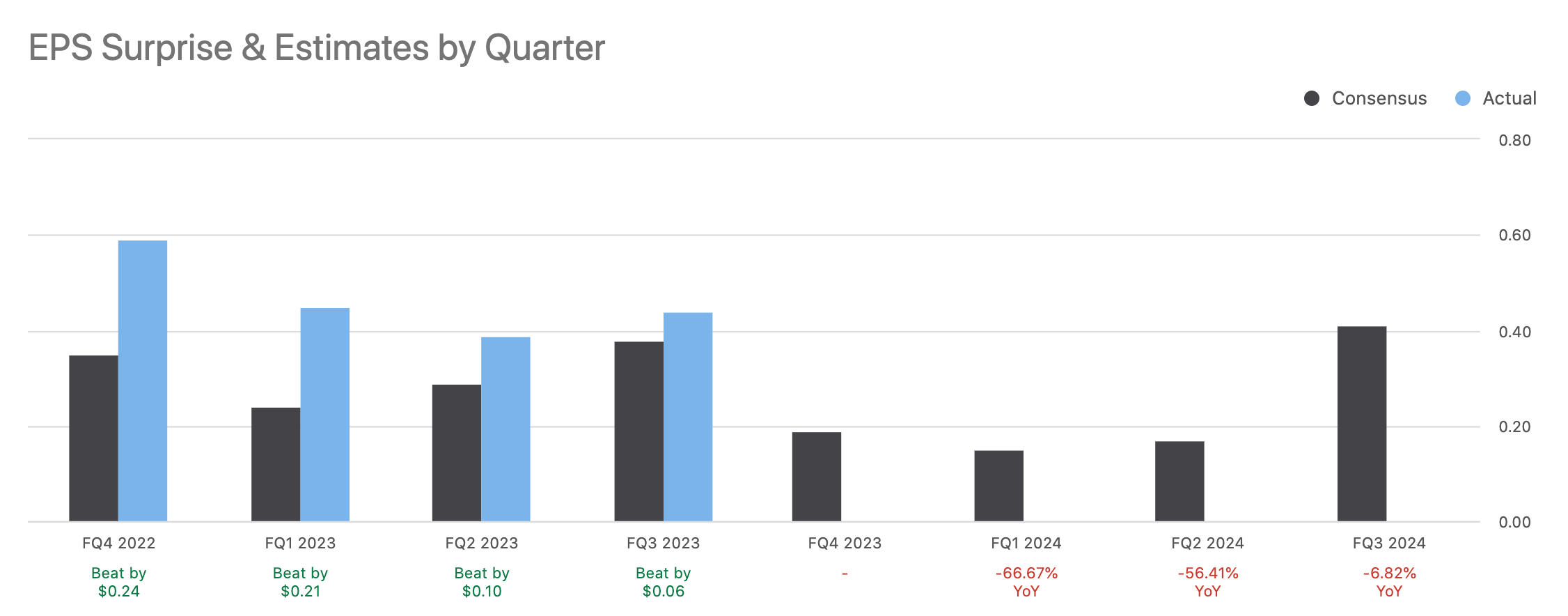

There are bright spots in the financials that suggest Richardson Electronics is fundamentally a healthy business. For instance, last April, Richardson reported its 10 th consecutive quarter of Y/Y revenue growth. Operating income surged to $7.6M in the third quarter of FY 2023 compared to $3.6M for the third quarter of fiscal 2022. EPS (diluted) was $0.44 compared to $0.21 per common share (diluted) in Q3 ’22. Total debt stood at a minimal $42.38M. The Enterprise Value is $215.80 and the market cap is $238.07M. The valuation grades for all metrics are As and Bs.

The composition of stock ownership is impressive. Individuals/insiders own over 16% of the outstanding shares of common stock and institutions own +62%. This means there is a lot of personal investment in ensuring the health of Richardson Electronics.

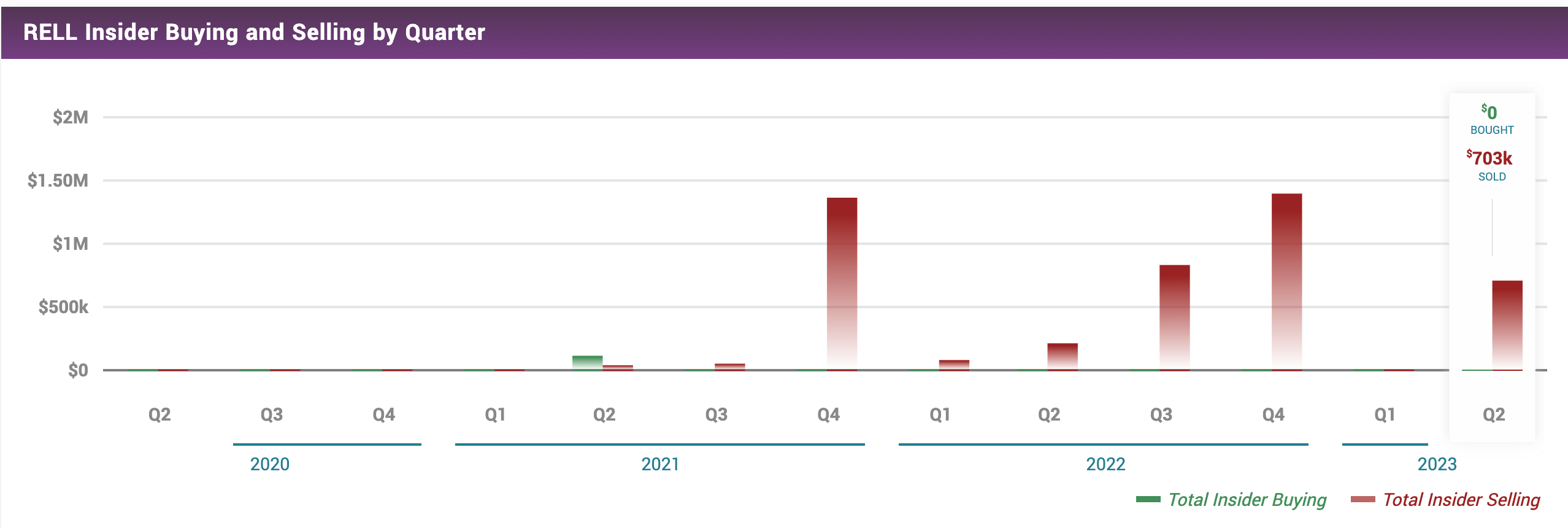

For us, and we think for other retail value investors, however, the downsides have more gravitas for our assessing this as a Sell-stock while the share price bounces around $16.50 as it has since mid-April '23. Our most pressing concern is that hedge funds and insiders are in a selling mode.

Hedge funds sold +70K shares in the last quarter. Corporate insiders sold $702K worth of shares in those 3 months. Insiders have repeatedly sold shares during the last year without any making significant stock purchases, usually after exercising options.

Insider selling history (marketbeat.com/stocks/NASDAQ/RELL/insider-trades/)

{kind=link}

Earnings have been falling and are not expected to grow again until late in 2024. The next earnings announcement is July 19, 2023.

{kind=link}

Some other incommodities from the Q3 ’23 earnings report are

- Shows the company did not dent the $175.6M backlog of orders in Q3 ’22. In Q3 ’23 the total backorders were valued at $175.1M.

- The gross margin was 31.8% of net sales, the same as in the prior year’s third quarter.

- The dividend yield is 1.43% which is down from 1.5% last April, and down from nearly 6% in April of 2020.

- Cash and investments were $24.6M as of February 25, 2023, compared to $40.5M as of May 28, 2022.

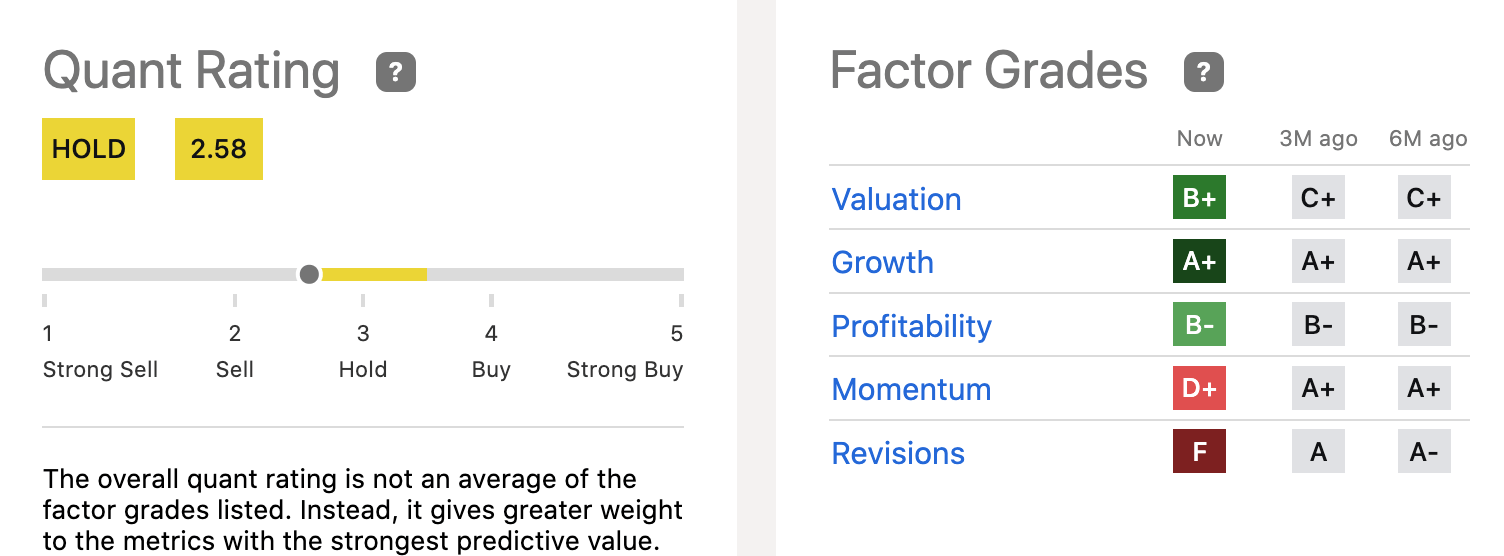

- Seeking Alpha and others do not include a rating from any Wall Street analyst. SA lowered its Quant Rating from a strong buy-in in August ’22 to hold beginning in April ’23.

- Momentum collapsed.

Quan & Factor Grades (seekingalpha.com/symbol/RELL/ratings/quant-ratings)

{kind=link}

Risks

Risks the company faces to greater growth are “a slowing semiconductor wafer fab market… finding enough design and field engineering talent to support the growth strategy,” and the slow recovery in China hampering Healthcare sales there, as highlighted in the last shareholder talk. Green energy equipment expansion is facing new challenges from higher costs, challenges from locals, and high rates of unprofitability.

The share price tends to make notable moves. The dividend yield is best described as erratic and dividends have not increased in the past 10 years. It sports a high Beta (0.95). The stock has few followers and lightly trades; the average daily volume is ~150K shares. It is subject to swings by a few major trades. Short interest climbed to 5.6% with 5.24 days to cover, as the share price climbed. Each share was under $5 in 2021 but then steadily climbed to a 52-week high of around $27 at the close of FY ’22, climbed later in the year to +$26, and dived to ~$16.50 in June '23.

Takeaway

In our opinion, too many line items were flat and Healthcare was a drag on the company’s decent Q3 economic recovery. Shares are up about 80% over 5 years, +4% over the last 12 months, but -20% YTD, attributable in our opinion, to expansion headwinds and Healthcare struggles that will continue through 2023. We forecast the Q4 ’23 EPS will be about $0.20 down from $0.31 in Q4 ’22.

It appears any good and bad news for Richardson Electronics is factored into the current price by investors. We do not foresee any particular stimulus that might drive the share price higher. BRICS countries’ spending in the next few years on healthcare budgets is not inspiring; management does not expect much improvement in the next 12 to 18 months, especially from China. They told shareholders in April that Healthcare sales in China of parts for medical devices decreased “as well as CT tubes sold in China, partially offset by an increase in equipment sales.”

The company’s earnings growth is not keeping pace with its impressive revenue growth. We do not believe the stock is overvalued considering the PE times 2023 EPS. There is little here to entice a retail value investor to do anything at the current share price than to consider it a selling opportunity.

For further details see:

Richardson Electronics Offers Limited Opportunity