CFRHF - Richemont: Calming Q3 Numbers Luxury Is Not Dead Just Yet

2024-01-19 05:43:27 ET

Summary

- Richemont announced fiscal Q3'24 results that beat expectations, with growth acceleration across important regions and customer clusters.

- The market seemed to believe a luxury winter was upon us, but the Swiss conglomerate provided investors with a much-needed soothing call.

- Management continues to deliver on its strategy to decrease dependency on wholesale and divest non-core businesses.

- I reiterate a Buy rating as the company trades at a low valuation historically and relative to peers, while it continues to demonstrate resiliency.

Richemont (CFRHF) just provided a trading update for its fiscal third quarter which ended in December.

Investors can breathe a sigh of relief as the Swiss watchmaker reported decent growth, a much-needed reassurance for the entire industry.

Luxury is not dead just yet, but there is a growing importance for differentiation and strong management, a trend that will define 2024 in my opinion.

Let's dive in.

A Luxury Winter?

In April of last year, many luxury companies, including Richemont, reached all-time high valuations. Following a few lackluster reports from struggling players like Capri Holdings (CPRI) and Kering (PPRUF), came Hermes (HESAF), LVMH (LVMHF), Brunello Cucinelli (BCUCY), and Richemont, with impressive results that reflected strong demand and market share gains. But the party didn't last long.

Investors soon realized that results were only going down from there, with growing macro pressures, disappointing recovery from Chinese customers, increasing geopolitical tensions, tough comparisons, and FX headwinds, bad results were inevitable.

In the calendar third quarter, this became a reality, with many companies reporting a decline in sales and margin contraction. Then, a steep yet justified selloff occurred.

Today, Richemont and LVMH are approximately 30% off their April highs, whereas ultra-luxury Hermes is 12% below. Before latest print, it seemed like the sector couldn't find any positive news to rely on. As recently as a week ago, negativity intensified following Burberry's (BURBY) profit warning.

With Thursday's release, Richemont injects some positivity into the market, showing there's still demand for luxury, although it is more fragmented than ever.

Three Categories Of Luxury Fashion

In a zero interest rate and positive market sentiment, many players win, but when the market becomes tough, that's when you learn to really differentiate between companies.

In my view, companies in the fashion luxury industry can be divided into three categories. The first category is aspirational luxury, which caters to the aspirational consumer. These are customers who can afford to spend thousands of dollars on discretionary items when the macroeconomic environment is favorable, but they are not immune to deteriorating conditions.

The second category is true luxury, which sells to high net-worth individuals who are essentially numb to macro conditions but are sensitive to the Wealth Effect .

Lastly, there's ultra-luxury. This category sells to the extremely rich. Typically, supply in this category will be intentionally limited, to create excessive demand. These are items that usually appreciate in price after the purchase, meaning they can be resold in the second market for a higher price.

Naturally, companies that lean more towards the first and second categories are more cyclical and sensitive, whereas companies that primarily rely on the third category are stronger.

As their results and stock performance show, Richemont and LVMH are in the sensitive group, whereas Hermes and Brunello Cucinelli belong to the stronger list.

Following the profit warnings and bad results from the likes of Burberry, investors started wondering just how bad things were going to get for the sensitive group, and Thursday, Richemont provided some relief.

Calming Call From Richemont

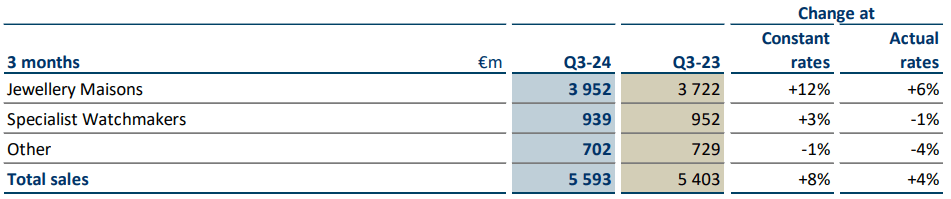

Richemont reported consolidated sales of €5,593 million, an 8% increase at constant exchange rates, beating consensus expectations for 7% FXN growth. Growth was positive in every region besides Europe and was led by an 18% increase in Japan, followed by 13%, 10%, and 8%, in Asia Pacific, Middle East, and Americas, respectively.

Richemont FY24 Q3 Sales Presentation

At actual rates, sales grew by 4%, led by 8% growth in Asia Pacific and a similar rate in Japan. Middle East & Africa grew by 5%, the Americas grew by 3%, and Europe declined by 4%.

Richemont FY24 Q3 Sales Presentation

Looking at performance by distribution channel, we can see that retail continues to outperform online and wholesale, a trend that's been steady for many years now. The company is consistently working on reducing exposure to wholesale, but progress somewhat decelerated, as wholesale percentage of sales declined by 1 percentage point compared to the prior year period.

{kind=link}

Segment breakdown shows the strength of Jewellery Maisons, which consists of Cartier, Van Cleef & Arpels, and Buccellati, the company's strongest brands. As I wrote in previous articles , the company divides its brands into three categories primarily based on quality and strength, rather than product mix. As such, it is expected that the superior segment will continue to outperform, showcasing 12% growth at constant rates.

{kind=link}

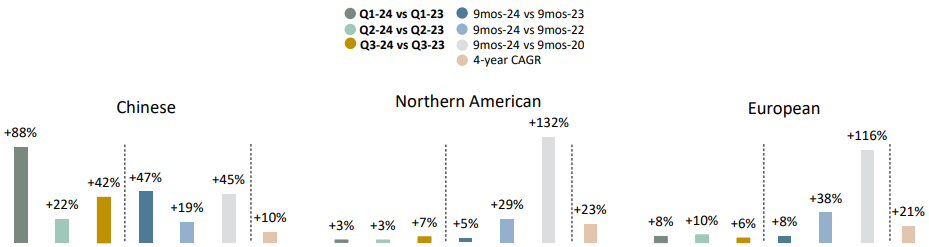

One of the most monitored metrics which is uniquely reported by Richemont is growth by customer clusters. Many industry followers are interested to learn about the performance of each cohort, as it disregards travel trends.

Probably the most positive number here is the Q/Q acceleration in the Chinese and American clusters. These clusters are responsible for a major part of the industry's sales, and both of them showed weakness in the previous quarter. The acceleration is a positive sign for the sector in general and Richemont specifically.

Overall, Richemont provided luxury investors with positive news for a change, demonstrating improving demand and growth acceleration.

YNAP Update

The company's planned sale of its YNAP business to Farfetch was terminated last December, as the acquirer struggles with cash. Management continued to classify the YNAP business as discontinued operations and said they are reviewing strategic options to find a new buyer.

Until that happens, YNAP will continue to weigh down on consolidated profitability, but investors will probably focus on the company's core results, expecting an announcement in 2024.

Valuation & Updated Investment Thesis

Richemont is a unique business in the sector as it's the only jewelry-only player that's not a wholesaler, so there's no perfect comparison. I believe LVMH and Moncler (MONRF) are the most relevant as they share a similar growth profile and quality.

Today, Richemont trades at a significant discount compared to its peers. Even after the 11% increase, the company trades at an 18.4x multiple over 2024 earnings, compared to LVMH's 20.3x and Moncler's 21.6x.

Prior to the pandemic, Richemont traded at similar levels, but the company was weighed down by management concerns and was perceived by investors as an inferior player in the sector.

After withstanding takeover threats and going out stronger from the pandemic, Richemont's management has decided to strategically focus on its core businesses, divest unnecessary operations, and grow its retail presence, all of which are crucial to the long-term success of a true luxury company.

In my view, Richemont will return to the top of its valuation range in the 20x levels as it continues to demonstrate growth and prudence. In addition, I'm expecting a sale of the YNAP business in 2024, which will also be a positive catalyst.

Conclusion

Richemont is usually the first to report results among its peers. The company typically sets the stage for the sector, as it provides a read through to the strength of different customer clusters and regions.

In the third-quarter release, Richemont provided investors with a much-needed soothing call, as it showed demand for luxury goods remains strong.

With better-than-expected sales and growth acceleration across the most important cohorts, I believe the depressed sector is due for a rebound.

Even after the immediate 11% increase, Richemont remains undervalued relative to peers and its historical levels. I'm expecting continued resilience, and reiterate Richemont as a Buy.

For further details see:

Richemont: Calming Q3 Numbers, Luxury Is Not Dead Just Yet