RACE - Richemont: Family-Owned Quality Shareholders Great Price

2023-12-23 03:42:39 ET

Summary

- Richemont is a luxury conglomerate with a diverse portfolio of leading brands in the watches and jewelry industries.

- The jewelry industry is experiencing organic growth and consolidation, providing growth potential for conglomerates like Richemont.

- Richemont is under the control of a family owner and has quality shareholders, including renowned investor Tom Russo.

- This might be a good price for long-term investors.

- Luxury at a good price is rare.

My Thesis

Well, I have a fondness for luxury. While I may not purchase their products, I admire luxury businesses for their control, predictability, and growth. In my perspective, some of the best publicly traded businesses are luxury and ones I intend to invest in at the right price. This list includes Hermes ( HESAF ), Ferrari ( RACE ), and the LVMH Group ( LVMHF ), on which I wrote a few weeks ago. Today, we will assess whether Richemont ( CFRHF ) shares the same traits as these compounders.

Although I believe Richemont may not possess the same level of quality as the aforementioned names, it does exhibit some appealing characteristics. These include a quality shareholder base, family ownership, and outstanding leading brands.

In contrast to other names, Richemont is currently selling at a good-maybe even a great-price for long-term shareholders.

The Business

Richemont is a luxury conglomerate, primarily operating in the watches and jewelry industries. Based in Switzerland, it boasts a diverse portfolio of luxury brands, ranging from high-end names like Cartier to more premium or lower luxury brands such as Montblanc. Notably, 51% of Richemont's business is dedicated to jewelry, a strategic dominance we'll delve into later. Watches constitute 35% of its operations, with the remaining percentage divided among fashion, leather goods, and other ventures. Today, I'll primarily focus on Richemont's core businesses-jewelry and watches.

Cartier and the Jewelry Industry

The luxury jewelry industry stands out as a high-quality sector due to its resilience, high-profit margins, and characteristics favoring long-term performance over short-term goal attainment. Jewelry, being a luxury, often retains its value, making it suitable for multigenerational businesses. This is an aspect I appreciate about Richemont; its leading brands are timeless. In the realm of luxury, longevity enhances the sense of opulence. Buccellati, established in 1919, Van Cleef since 1906, and the iconic Cartier, founded in 1847, exemplifies this concept. Consider this insightful quote from the CEO of Bulgari:

You can't forget that jewelry is the only luxury that never, ever loses value, That is the prime factor why it is growing faster and is more resilient than any other luxury - because it's visceral, deep in our minds and hearts, and global.

The promising growth of this market bodes well for Richemont's profit margins, given their emphasis on the impressive 35% EBIT margin, surpassing that of the fashion and leather goods segment. Additionally, this growth remains noteworthy even without factoring in the fragmented nature of the industry, which was historically dominated by family businesses but is now undergoing significant changes.

Jewelry from high-end brands like Bulgari, Tiffany, Cartier, et cetera used to be around 20 percent of total jewelry consumption, which is a relatively small share if you compare it with fashion," Mr. Carniello, a former Bain consultant, said on a recent phone call. "It meant 80 percent of jewelry was from small regional brands or it was unbranded - the retailer played the biggest part in relation to consumers.

The industry is gravitating towards larger players, paving the way for significant growth potential for conglomerates like Richemont.

That dynamic, however, began to change rapidly about a decade ago. Ms. Levato said that, in 2021, branded jewelry represented 25 percent to 30 percent of the jewelry market, a marked increase from the 15 percent to 20 percent that it represented in 2011.

We find ourselves in an industry experiencing organic growth (projected at 6-8% in the next few years by various sources ), boasting high-profit margins, and concurrently consolidating. This consolidation trend provides major conglomerates, like Richemont, an additional avenue for growth through strategic acquisitions.

At the forefront of this thriving industry is Cartier, the flagship brand. With a rich French heritage spanning almost 180 years, Cartier holds the esteemed position of being the leading brand in the sector. Notably, it is also listed among the top 10 luxury brands by value, according to Brand Finance.

{kind=link}

The CEO of Cartier underscores its unique ability to increase volume without compromising its luxurious essence, aligning it with esteemed brands like Dior.

We tend to think that luxury brands or products cannot go beyond a certain reach without losing their appeal and desirability," Mr. Vigneron wrote. "Yet, a handful of maisons have broken this glass ceiling. The more they are seen the more they get desired.

Furthermore, owing to its extensive history and French heritage, Cartier stands in stark contrast to other consumer brands. I believe that eroding the brand image of Cartier will prove to be exceptionally challenging, rendering it highly resilient.

Factors I Appreciate About Richemont

Richemont is under the control of Johann Rupert, who holds 51% of the voting rights and approximately 10% of the company's shares. As the founder of the group and the chairman of the board, this fact is particularly appealing to me. Rupert's substantial stake underscores his significant commitment, with a substantial portion of his family fortune tied to the success of the business. I value family-owned businesses for their often longer-term mindsets, aligning their interests with those of long-term shareholders in the company. Consider this insightful quote from Mackinsey :

The critical mindsets are a focus on purpose beyond profits, a long-term view and emphasis on reinvesting in the business, a conservative and cautious stance on finances, and processes that allow for efficient decision-making.

Why FOB's outperform (McKinsey)

Additionally, the compensation structure for senior executives at Richemont is robust, with 51% of it being long-term oriented. This is determined by creative factors such as return on assets and a formula involving EBIT and FCF, along with qualitative factors crucial for preserving the luxurious brands.

Another favorable aspect of Richemont is its quality shareholders, including the Russo Fund led by Tom Russo, an expert in consumer brands who generally favors family-controlled businesses. Russo, with a significant stake of more than 5 million shares, has allocated a substantial portion of his esteemed portfolio to Richemont. As a long-term-oriented investor, I believe Russo has engaged with the management and expressed satisfaction with their long-term strategy. Holding a company where major shareholders include quality fund managers or family-controlled entities is viewed very positively.

The numbers I like

Richemont boasts several key factors that appeal to me. Firstly, its consistent linear growth over the last decade signals a secular growth business, seemingly impervious to cyclical economic factors. This aligns with high-end luxury brands like Hermes, Ferrari, and possibly Cartier, which meticulously control their growth rates due to robust demand and a tight grip on supply and pricing.

Secondly, while I appreciate the impressive profit margins, it's worth noting the concern about their instability. This directly influences another crucial factor in my assessment - returns on capital. Currently, Richemont maintains a commendable 17% ROIC and ROCE. However, these figures can fluctuate significantly due to changes in margins. High ROICs serve as a valuable indicator of the company's efficiency and success. It's noteworthy that these ratios align with those of LVMH Group, another highly successful luxury conglomerate. Research by Michael Mauboussin suggests that a high and growing spread between a firm's WACC and its ROIC is a common trait among winners.

Another important factor I appreciate is Richemont's robust balance sheet. With over $10 billion in cash and around $6 billion in debt, the company faces no imminent danger. The current ratio comfortably stands above 2, and the debt-to-equity ratio is below 1. This instills confidence from a solvency perspective, assuring that even in challenging economic environments, there should be no issues with debt payments.

Growth and valuation

The jewelry industry is projected to grow at around 6-8% in the future, and I believe Cartier could potentially outpace this, reaching a growth rate of 8-10%, excluding potential acquisitions. For the watches section, growth projections hover around 5%, and barring acquisitions, I see no compelling case for higher growth. Hence, I'll stick to the assumption of around 5%. Considering these assumptions, the overall growth rate is estimated to be around 6-8%, potentially even higher. Additionally, there is room for potential margin growth, given that the jewelry section operates on a 35% margin, although for the sake of conservatism, I won't factor it in here.

A 5% Free Cash Flow yield for a high-quality business, coupled with (assuming stable margins) high returns on capital and robust top-line growth, is, in my view, a good price. The same holds for a PE ratio of 19.

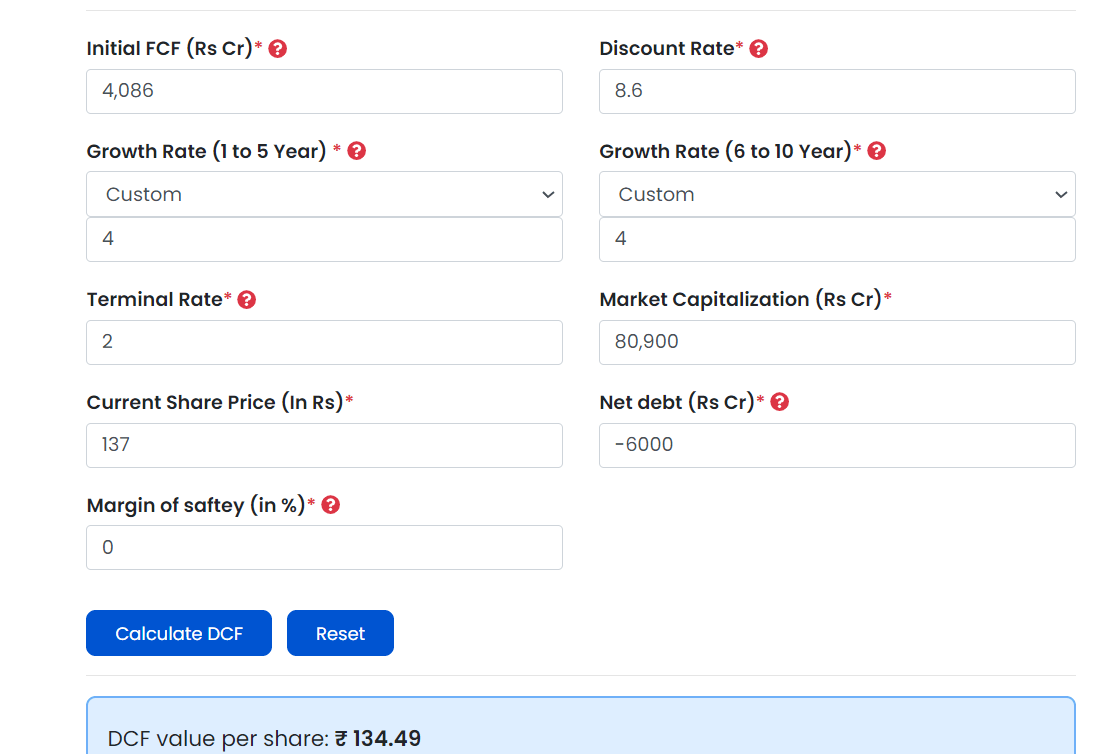

While I'll construct a Discounted Cash Flow model, I must emphasize my hesitation toward it due to its reliance on endless assumptions.

Using a WACC of 8.6%, a terminal growth rate of 2%, and a 17% FCF margin, I'll explore a couple of scenarios. In the first case, the current price of $137 implies a projected 4% FCF growth. While not impossible, I consider this unlikely, given Richemont's organic growth potential and possible acquisitions.

{kind=link}

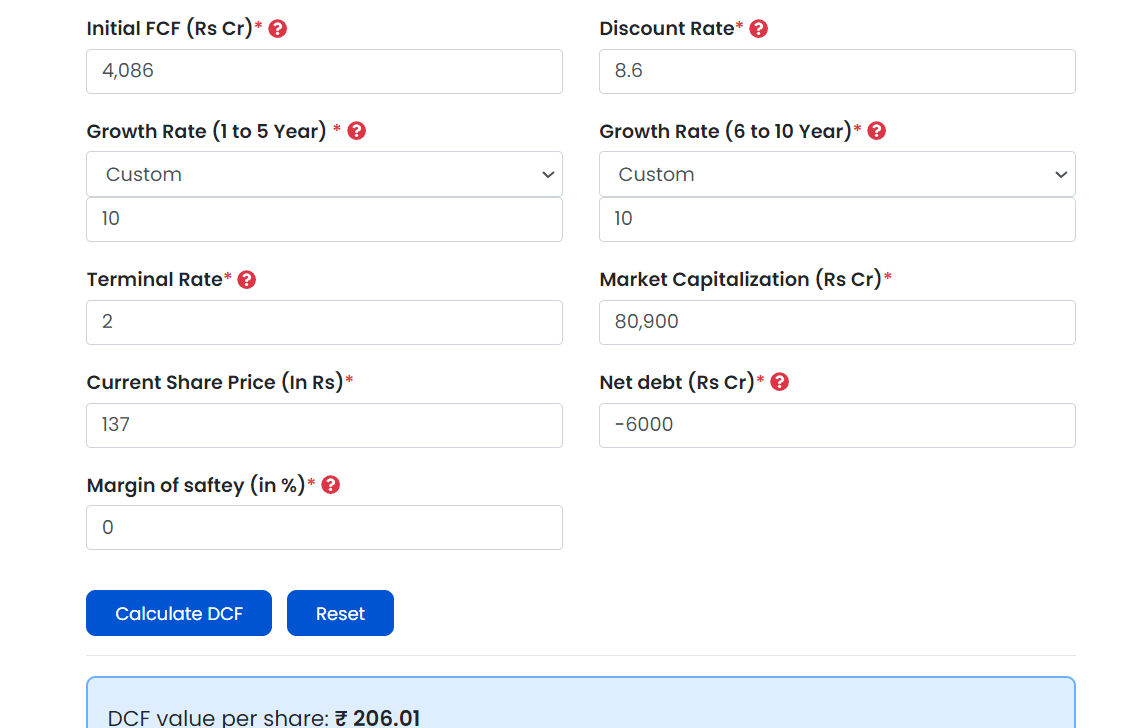

In an optimistic case, assuming 10% FCF growth, which I find plausible considering the potential for margin expansion, the stock appears undervalued by 33%, presenting a potential bargain for a quality business.

{kind=link}

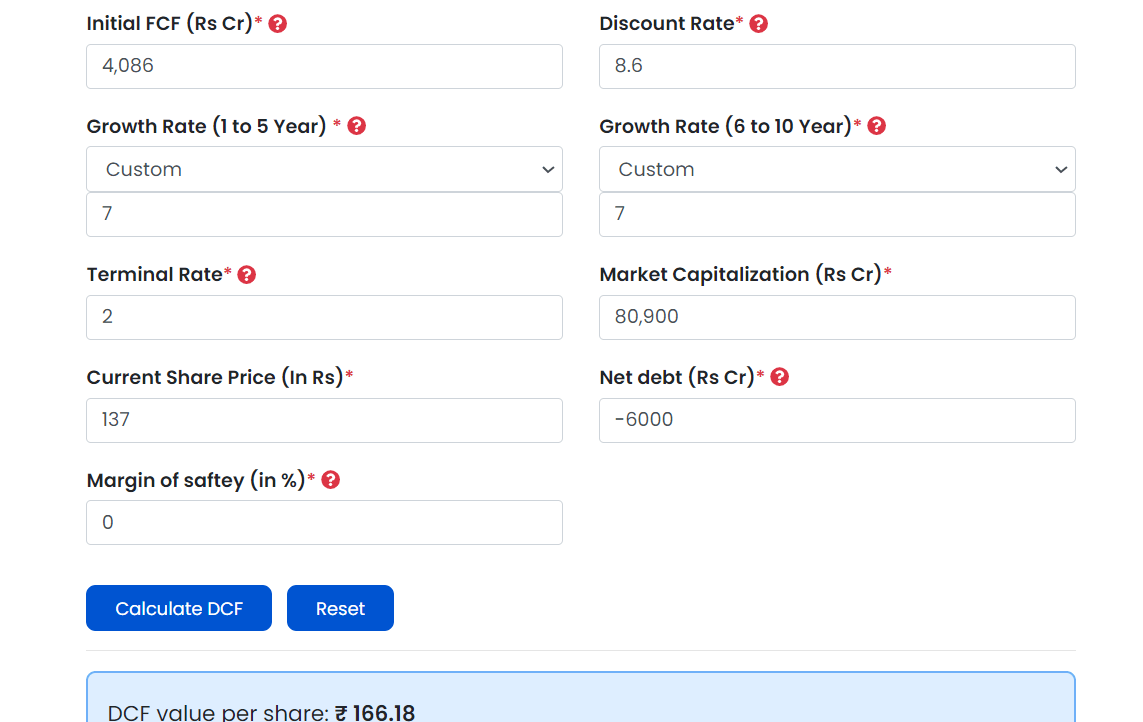

In the base case, assuming 7% FCF growth, the stock is undervalued by 17%. While some may find this margin of safety insufficient, I view Richemont as a long-term investment with predictability and notable quality attributes.

{kind=link}

Risks and rating

While there are several appealing aspects to Richemont, it's essential to acknowledge the associated risks. Firstly, the risk lies in the controlling chairman, who, with the majority stake, holds significant influence over the company. Wrong decisions on his part could potentially harm the company.

Another risk involves maintaining the luxury brand image. Luxury businesses, especially high-end ones like Cartier, require meticulous management. Certain missteps, such as discounting, are considered detrimental in the industry, risking the prestige of the brand.

Competition is an inherent risk, and in the luxury sector, engaging in price wars is not a viable strategy. The primary avenues for improvement lie in effective marketing strategies and delivering superior products and experiences.

A particularly concerning risk is the instability of margins. My valuation assumes Richemont can maintain high-teens Free Cash Flow margins.

Lastly, while I find the current valuation favorable, it's not extremely undervalued, leaving little room for error.

Despite these risks, I believe the risk/reward balance favors buyers. The combination of high returns on capital, solid projected growth, insider ownership, and a quality shareholder base makes it highly appealing to me. Hence, I would rate the stock as a STRONG BUY. It's rare to find a quality company at an attractive price without major flaws in its business.

What are your thoughts on this business?

For further details see:

Richemont: Family-Owned, Quality Shareholders, Great Price